On item 1, the string of problems seems to indicate poor lending capabilities of legacy idfc bank team. Makes me wonder what else is out there from the remaining 10k of infra and 25k of wholesale book. Recently read somewhere that bank has exposure to Future Retail as well…If the bleeding continues likes this, and consequently bank ends up raising capital at low valuations, hard to see book value compounding over the next 3-4 years.

3 Likes

Above all other possible negatives we need to watch out for provisioning and PCR.

PCR target, as guided by the CEO, is 70%.

Thus far 52% is reached.

Therefore, we can expect more of the upcoming quarterly profits to be diverted.

Plus more Covid related provisioning might happen.

The Mumbai Toll Road account’s NPA status most likely will be reversed. Then PCR would be 58% still far enough from the target of 70%, which would take couple of quarters.

Stress pool is now 1371 Cr.

And PPOP 1000 Cr for Q1Fy22

Some entry from the stress pool could slip into npa category like Mumbai toll road did last time.

Moreover, the Voda situation isn’t exactly improving, today the stock was 6% down.

3 Likes

IDFC First has 150 crore exposure to future retail.Which is peanuts for IDFC First bank NPA list ![]()

5 Likes

Sorry I don’t remember seeing this, please do share your source. I thought they generally guided to 2% gnpa 1% NPA 2% credit costs guidance. The pcr is 50% only then. Not 70%. So I’m confused.

1 Like

Ideally, better banks would take PCR to 80%.

But here we will settle with 70%

Got this from Q1FY22 presentation.

What got my attention was the fact that provisioning of 1879 Crores was done in one single quarter. That’s a big number, and yet PCR didn’t improve. In fact reduced 4%.

Out of 1879, only 350 Cr was covid provisioning and the rest 1529Cr, I assume, was for the legacy loan book wholesale NPA. Still PCR didnt improve.

Point I am trying to make is that PCR to reach 70% will most definitely take couple of quarters of robust earnings.

PS: just came in

Looks like issues won’t end any time soon.

3 Likes

Well, yes…peanuts, by standards of this bank…my point was that there are probably more problems in the infra and wholesale book which is still > 30% of book. The erstwhile idfc bank folks seem to have lent to all of the major crooks or inept businesses of the country…DHFL, ADAG, Future, Voda, problematic toll roads and infra projects with political issues…endless list of problems.

7 Likes

any source for this? concall ?

This foundation issue was mentioned in the latest AR of IDFC. I’m not sure abt wher timeline was mentioned. @manikya_saiteja_gund can probably confirm that part.

Else the AGM is thr on 22th Sept to get further clarity.

3 Likes

It’s mentioned in the AR.

Merger of IDFC Alternatives, IDFC Trustee & IDFC projects by March 22 & Detachment of foundation by June 22.

3 Likes

Given that Article is related to Banking in General and not IDFC First bank specifically, is there a specific reason to post it here? It can be because you are tracking/holding IDFC first bank, but it can also be because of it’s recent negative results. Whenever a company comes up with bad results, somehow somebody digs such articles related to that company/ industry and shows why this company is going to bust soon. No such noises come up when the results are good.

Coming to the article itself, it sounds like the noise of 1991 when Politicians used to say that Foreign companies will come and India will become their slave. While PSU banks may face the heat (due to their own issues), to say that Google/ FB/ Amazon can do better than Indian banks on their own turf is easier said than done. It is not to say that these companies are not a threat but to think that Banks are dud and will let anyone come and take their turf is not right. In fact, if we see story of Foreign banks in India, we can see who is the boss when it comes to Indian market/ customers.

In case anyone wants to understand how Indian banks are changing, I would request you to go through this concall of HDFC bank where they are explaining the Technological changes they are making after the RBI ban on them. Banking is not what it is used to be even 10 years ago, it is much more technology driven and Fintech is a part of it.

6 Likes

At present Idfcfirst bank is facing following issues, due to which investor confidence is fading:

Potential NPAs:

*Vodafone, Mumbai toll, They have not been fully provision for. While PCR is not comforting.

-

Stress Assets Pool still has 1347 crores worth of potential GNPA.

-

Most of the NPAs have come from legacy loans, specifically infra loan which still has around 13000 crores of outstanding loans.

B. De-Merger issue is looming

C. Equity Dilution. We Hope the management chose against this option.

3 Likes

The five banks including State Bank of India (SBI), Piramal Capital, IDFC First Assure, and DMI Finance each have reportedly assured business worth Rs 10,000 crore. Further four non-banking financial companies have assured Rs 2,500 crore worth of credit support, according to ET Now.

2 Likes

Stress Pool 1371

Provision 915

Balance 456

Vodafone 3244 outstanding

Provisioned 487 (only 15%)

Balance 2757

Total Balance 3213 needs to be provisioned.

In the recent annual report, senior officials are talking positively about Vodafone, but from the news the picture is still unclear. Just the fact that Vodafone owes the government 1.5 lac Cr does not mean that it could not default.

The recent Q1Fy22 report says that no dues of Vodafone are pending as of 30th June 2021. That’s encouraging.

(Then why was Kumar Mangalam Birla willing to give his stake to the govt, just gimmicks?)

All in all, 3213 is a whole year’s profit. That’s the worst case.

So, going forward the Vodafone news will be crucial for the bank’s share price.

3 Likes

In addition to the known devils in the wholesale book, the bank did retail lending of ~16,000 Cr in the past 12 months. The retail book is yet to be fully seasoned after the bank decided to focus on retail lending and pull back from wholesale lending, especially to infra.

In addition to this we have the upfront costs of branch expansion hitting the operating profit, new branches take 2-3 years to become profitable at the unit level. But once they become profitable, they can become perennial cross selling profit machines.

The possibilities on both sides (positive and negative) are very interesting, up to the management now on how they handle this tricky transition period over the next 12-18 months. If they do well, this could be a worthwhile journey. Else this could become yet another story that had potential but just couldn’t do what it takes to get onto the next level of business quality.

Banking is more about risk management, choosing which battles to compete in, culture and cross selling beyond a point - all of these are qualitative factors that one cannot easily assess by looking at the financials and doing excel sheet work, P/B calculations. In stories like this investors are paying more for possibilities rather than for any assured trajectory, which is why the bank is priced the way it is. By the time the numbers get better (if it happens), the price movement would have been long done.

21 Likes

In the last 3 years the bank has seen issues that none of us( management included) foresaw.

No one at the time of merger in December 2018 could predict the demise of DHFL, Rcap, Cafe Coffee Day, Vodafone Idea and the worst of all-Occurance of a pandemic- COVID19.

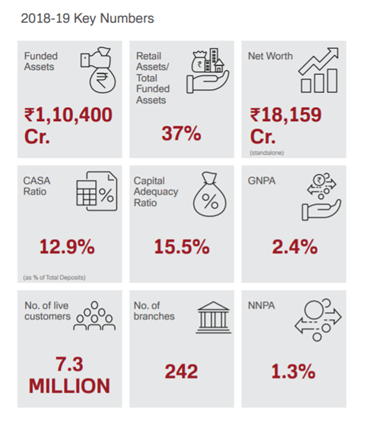

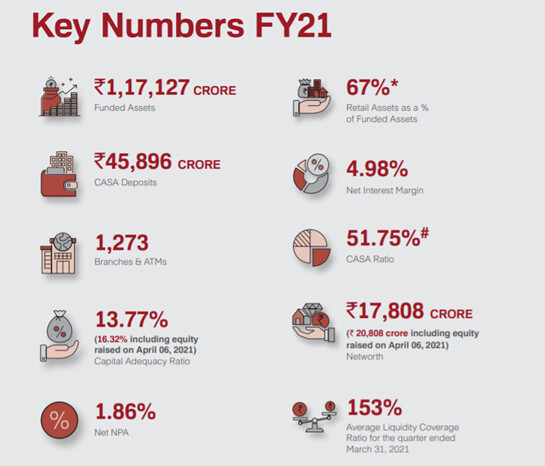

The bank has lived through all of this and has proudly emerged stronger, leaner and fitter. Just compare the basic metrics of the bank in Apr-19 and Apr-21.

Capital Adequacy: 16.32% vs 15.5%

CASA Ratio: 51.75% vs 12.9%

Networth: 20808 crs vs 18159 crs

%age of Retail Assets: 67% vs 37%

Branches: 597 vs 242

NIMs: Touching 5.5% vs 3%

These are the metrics after taking in one-time exceptional provisions during Covid and other mentioned accounts to the tune of 5550 crs.

Just imagine the growth in a normalized scenario. This compounding machine is just about to take off!

18 Likes

I don’t think that’s a correct understanding.

Out of total voda exposure, the funded exposure is only 2000cr and out of that 487cr is already provisioned. So the exposure is limited to 1500cr. The non funded exposure relates to bank guarantees etc. Now if IDFC FB has furnished a bank guarantee on behalf of VI, its not clear whether the guarantee is revocable or not.

Lastly, while you can fully provision, but do remember that part dues would be recovered through NCLT or whatever process that happens. The only variable here would be time.

6 Likes

I am not thinking as an optimist. But going just by the numbers the management is giving. Furthermore, I am fairly sure that even next quarter EPS is going to be negative, because there is plenty provisioning to do.

The Saving Ac interest rates have been reduced to what others are offering in the market. So, the CASA ratio growth is likely to cool off. Hence, the pace of reducing the high interest Commercial Loan will drop proportionately. NIM is likely to remain stable at 5.1%

Scuttlebutt at a nearby branch reveals that the bank has stop issuing fresh credit cards. Apparently, NPA problem is far from over. Customer footfall is less, fresh accounts are being opened at a much slower pace. Five employees, and far less hustle bustle compared to an established bank. In fact, their account opening machine was stashed away. Took 15 mins to find it, and trying to get it started. He soon gave up. I concluded, business is very slow.

In the near future, growth of EPS is likely to be muted or absent.

Proper, sustainable EPS growth is going to happen via loan book growth, and now is not a good time to do that.

1 Like

In their throes of euphoria, folks have compared IDFCFIRST with HDFC Bank.

Idfcfirst does not have AMC, Life insurance, etc like Kotak and Hdfcbank do. These comprise of significant portion of EPS.

This is the reason why idfcfirst branches are smaller. The only work there is to facilitate off take of small to mid sized loans, and opening new accounts. They don’t have products for cross selling.

I feel the management is going to focus on its strength, which is retail loans. And hence branch efficiency won’t be like what we’ve seen with other established banks.

Going to a HDFCBANK branch you’ll find all kinds of products being thrown at you. And some are even good. That whole environment is lacking here.

PS: just trying to have a discussion, and cut through the euphoria this stock has gathered.

8 Likes

Agree, we Indian investors love to build stories around what can be the next Infosys or the next HDFC Bank. Fact is NRN himself or AP himself will struggle to build the next Infosys and HDFC Bank with the same team. Everything is a function of time and place, I find these comparisons mostly meaningless as an analyst, though they do have some value in building stories that can connect ![]()

The expectations here have to be more rational on the third party fee income that can be generated, at least in the next 3-4 years. Building a cross selling culture takes time, getting products empaneled and vendors onboarded is the easier part. A channel check across the new age fintech ecosystem at Bangalore tells me that IDFC First Bank is the most aggressive and market friendly bank. This can be seen both negatively and positively.

My experience has been that when you hire people who have done it before, offerings like wealth management and insurance selling are easier to implement. A behemoth like SBI hired seasoned wealth managers from the market and started focusing on wealth management starting from 2013. You can see the rise in AUM of SBI MF after a couple of years from then. Axis Bank never had a wealth culture, they took the same route of getting in experienced hands and launched Burgundy seriously. Today Axis AMC is the indirect beneficiary of Axis Bank Bank focusing on the investment advisory piece.

It will be many years before any other bank gets to the level of efficiency of HDFC Bank and ICICI Bank in cross selling and generating third party fee income from the incumbent customer base.

What remains to be seen is if IDFC First Bank can do a decent job, I don’t expect them to do a great job anytime soon.

17 Likes

One of the aspects that I see is that if the company goes down then the entire value is lost.

The non fund BGs are guarantees to regulator. The telecom companies do not pay the entire spectrum charges upfront. They pay it over time. These BGs are guarantees. It would be for life.

Also, if the company goes down its asset value deteriorates faster than liabilities. So the likely realisation from the assets drops significantly. Realisation from NCLT would ve low. It is not like a steel plant or

2 Likes