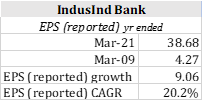

Annual report:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/c7a18e1b-ca8f-4275-abe7-a0fe046dda57.pdf

FY21 AR notes

CEO’s note is so full of information that have to make a separate section for it. The investment thesis is handed to investor on a platter. Of course it is up to the investor whether they buy it, or not. Every individual must make their own decision.

- What we are building at the core is a new age digital Bank which is agile and highly scalable.

- Focus of analyst community is on the here and now. Analysts not focussing on strong fundamentals and incremental profitability. Comparison with banks built over last 2 decades unfair. Converting from DFI to commercial bank is hard (only ICICI succeeded).

- Carrying 28k cr of borrowing at 8.66%. Incremental profitability to be large when these are replaced by low cost borrowings.

- Aspiration: become bank of global scale & profitability, on the cutting edge of innovation, providing amazing customer service, highest levels of corporate governance, generate high return on equity, and enjoying international respect and admiration.

- Product teams design products in a way that it is meant to be sold to our “near and dear” ones. We make products with transparent pricing and fees. Eg: Monthly credit of saving account interest Low, Dynamic APR for credit card revolvers, Cash withdrawal interest rates, Where there is a misunderstanding, instruction to the service team is “credit the customer first” then fix the root cause of the issue, No Fine Print Banking, We don’t pressurize employees to sell high margin products.

- 40% of card holders do end up paying the revolving credit card rates.

- We recently unveiled our new mobile and web app which have a large number of unique features like Google like search capabilities, Personal Finance Management, Pay-to-Contacts, one click FD creation, live mutual fund investing, risk-analyser

- we have also developed specialization in financing artisans, large medium and small farmers, kirana shops, restaurants, automobile spare parts, tailoring, carpentry, salons, chemists, two wheelers, consumer durables, JLG in rural areas etc. The purposes of financing include business expansion, cattle purchase, water and sanitation financing

- have financed over 30 million such loans till date in our combined experience. We have developed unique skills in this area with stable and high asset quality of Gross of ~ 2% and Net NPA of ~ 1% for over ten years.

- On profitability, the issues in infrastructure and certain corporate accounts turned out to be more than expected because of the economic cycle

- our CASA ratio has crossed 50%. this describes our capability to raise deposits, a key raw material for growth.

- The deposit inflows were strong, more than requirements. So, to optimize the flows, we reduced our savings account interest rates. our new account opening continues apace. reducing our savings account interest rates had another positive benefit; can participate in prime Home loans profitably which has multiplied our market opportunities

- we will easily surpass the fiveyear guidance of 1,00,000 crore retail assets given at the time of merger.

- Infra financing: have brought down the loan outstanding to infrastructure from 22,710 crore at merger to 10,808 crore as of March 31, 2021.

- On the Corporate Banking side, we have implemented good controls in our Bank and our recent portfolio performance is pristine. (some hints of incremental asset quality)

- During COVID our retail NPA has increased, but we are confident of reverting to our pre-COVID GNPA and Net NPA around end of FY 22, based on the strong pickup in collections post COVID second wave. We should trust our skills, track record, experience and technology, and not doubt ourselves just because of a pandemic that came our way. We learn, adjust, refine, and move on.

- We expect mortgage backed loans to form 40% of our loan book in due course

- Credit Costs: Our provisions for FY 21-22 is expected to be only 2.5% of the average loan book which is quite reasonable by industry standards, of which a substantial portion has already been taken in Q1 FY22, hence you can expect to see successively reduced provisions in Q2, Q3 and Q4 FY 22. Going forward we expect to keep our provisions at below 2% of the average loan book.

- 2- 1- 2 Formula: We will be targeting a 2-1-2 formula, i.e. Gross NPA of 2%, Net NPA of 1% and provisions of 2% on funded assets on a steady state basis.

- Strong incremental profitability of retail lending business: Our incremental borrowing cost is less than 5% and incremental lending in retail is over 14% at this point of time. incremental spreads on retail is >9%. our credit costs (provisioning) are expected to be about 2% based on the combination of products we finance. our incremental ROE in the retail lending business is estimated at 18-20%

- Strong incremental profitability of Corporate Lending business: Here, the estimated incremental business ROE is 14-15%

- Higher cost of 1,000 crore from Legacy Liabilities currently: As of June 30, 2021, the Bank has 27,936 cr legacy loans at 8.66% interest rate. When our Bank will replace this at say, 5.0%, we would save about 1,000 crore per year on an annuity basis compared to today (todo: figure out when these liabilities are maturing)

- Set up costs (OpEx) in retail liabilities because of investments as we are a new bank: Since merger to March 31, 2021, we have invested in 390 branches, 565 ATMs, added over 12,000 employees, invested and upgraded our technologies, launched or scaled up many new businesses like credit cards, Wealth Management, Fastag, Gold loans and scaled up many retail lending businesses like prime home loans and digital lending, all these are essential capabilities for building a large bank. These investments are giving us a negative drag today but this will become profitable with scale.

- Incremental profitability in a table:

- The comparison with Q1 FY22 was even better. Here the core operating profit was 601 cr which was 118% over the merger quarter, while the book grew only 9% over the merger quarter. This tells you that the incrementally, the operating profit on capital is disproportionately higher as compared to incremental capital consumed

- We expect to grow the retail book by ~25% on a compounded basis for a long period of time. This is already playing out over the last 2 ½ years, as the NIM has already expanded from 1.84% pre-merger to 5.09% in Q4 FY 21 and further to 5.51% in Q1 FY 22

- The negative drag because of high cost liabilities will go away as we will repay these liabilities on maturity. The negative drag because of investments will go away with scale.

- Size of opportunity: the MSME, retail and rural and agriculture markets alone is about 65 lakh crore and growing. We are merely ~ 75,000 crore in this market, which is barely above 1% of this market. For us to grow at 25% is not a big deal.

- VI Exposure: out of the total dues of the company about 1.5 lakh crore are owed to the government itself and hence they will be keen to solve this issue. if we have a strong and profitable model and go on for extended periods of time, then a one-off incident does not dent the long-term story.

- announced a one-of-a-kind Covid Care scheme for employees by assuring them 4X their CTC, salary credit to nominee for two years, waiver of employee loan, extension of medical insurance for family for 24 months, scholarship up to

10,000 per month for two children until graduation, employment for spouse on merits or skill training allowance of2 lakh and so on - We implemented a bank wide cost-rationalization program. We tightened credit criteria and launched new products. We accelerated our efforts for digitising the bank. Our senior management volunteered with salary and bonus cuts to lead austerity by example.

The thing which makes me happy is that i had actually modelled a lot of these things which are finding mention in AR21 earlier in year correctly. 2-3% Credit costs, 8% eventual NIMs, even the timeline (my calculation was 2.2 years and itll probably be safer to say 3 years. Bank says next 3 years will be best so far for the bank).

Hope investors would be happy to see stickiness of CASA despite cutting rates 200 BPS.

Disc: Invested, biased.