If you go through the recommendations of the RBI IWG then they are pitching for allowing corporate ownership of banks. If this is allowed in some form and for whatever reason the reverse merger doesn’t happen then IDFC’s board will be obligated to get the best price for their concentrated holding in the bank. The best price will be offered by a strategic investor like a Corporate or an NBFC which is interested in owning a large stake in a bank. If such an entity ends up owning the stake then VV might not have the free hand he has now; in fact if difference arise between the management and ownership then he could potentially even be pushed out. So really it’s in the interest of all IDFCB shareholders and management to push for a reverse merger so that the ownership issues can be laid to rest once and for all and for IDFCB to have a widely dispersed market ownership like HDFCB, ICICI etc.

Idfc is committed to the reverse merger. We know that.

Would they even be committing to this publicly without sounding out the idfc first board informally first?

If the idfc first board was opposed to the reverse merger then idfc messaging on the conference calls should have been, “this is what we want to do, and maybe idfc first will agree. We don’t know.”

Their message instead has been, “we might have to adjust the exchange ratio to make it work for idfc bank.”

This is a slightly nuanced message. Or maybe I am reading too much between the lines.

@manikya_saiteja_gund If this is the case, why can’t we buy Ujjivan Financial Services which is available at 40% discount to Ujjivan Small Finance Bank. I am heavily invested in Ujjivan Financial Services for the same reason of reverse merger

In my case, I am extremely bullish on IDFC First bank and waiting for the rerating since last year.

I look at below paramters while investing in Banks

ROE

ROA

Brand Value - Liability gathering ability.

High P/B value - signifies strength of franchise

Tech & Product savyness

Contingent liabilities/NetWorth

Fee income as % of Total Income

IDFC First Bank scores well in all the above.

Vaidyanathan promised that he’ll be at 14+% ROE, 1.5+% ROA , Brand value is well known(14lak shareholders count speak for itself) & Gradual P/B rerating to 3+ - high P/B gives dilution edge thereby compounding P/B growth.

I see atleast 20-25% compounding on Book value for the bank after 3 years ( 15% from ROE & 5-10% from Dilution).

So, while buying IDFC Ltd at 47rs - it is as good as buying IDFC First Bank at book value (Rs.33.7) considering swap ratio of 1.43-1.5. Which is a comfortable number for me.

Also, IMO Anyone investing in a lending institution with <15% ROEs or <1.5% ROA’s is wasting their time in markets- Buying such a business even below the book value is not worth it and a recipe for not generating wealth in long run.

So apart from IDFC First and below banks, I think everything else is waste of time.

HDFC Bank - Hulk of the pack , Stable growth low risk investors

Kotak Bank - Wealth preservation Machine- for Stable growth low risk investors

Axis Bank - Decent franchise with growth + stable growth investors

AU Small Finance Bank - 15+% sustainable NBFC Type play- High growth High risk investors

Bandhan Bank - 15% ROE in super stress time(2020), in good times 25+% ROE for high growth high risk investors

CSB Bank - Potential 1.5% Sustainable ROA in long low growth low-risk investors

I feel all small banks[except AU] don’t have enough Brand value, risk management, IT Spending ability, Talent attracting ability, Automated processes, proper risk-based pricing etc which I am not comfortable with.

Also, Around the world banking is always concentrated among top 10 players. Since top players build Solid Payments,Brand awareness,Banking relationships at corporate & government level all the new credit creation will always endup with top players.

even in US Top 3 players have 30% market share in deposits.

I believe IDFC First will endup in that top 10-15 league, which i cannot say for a small bank like Ujjivan or equitas…

so, a personal choice to not diversify for playing this special situation.

Quality of Assets is more important that all the Parameters spelt out.

Some banks take high risk, long tenor exposures to get upfront fees. This beefs up RoA, ROE etc but it all comes back to haunt later.

Judging the book quality and go forward impact is important. Some banks do provide mix of rating of portfolio assets, but what is important is a delicate mix of risk, structure and returns.

IDFC First Bank has garnered a lot of interest in the last one year primarily because fundamentally it’s growth in CASA, loans, products and also stock returns have been far far ahead of competition in the last one year.

As of now, it is a hard fact that betting on IDFC First for the next six months is sadly also a proxy play on the Vodafone idea fund raise. If it goes through, Covid wave-2 provisions can also be very easiliy taken care of and IDFC First will be rerated very quickly and swiftly to 2-2.5x Trailing book value (Rs 75-80). If Vodafone idea goes down under, an additional provision of ~ 2400 crs will dent a huge blow to the balancesheet and the stock price.

At this point of time, it is my largest holding in PF(Concentration more than 55%) inspite of selling 20% of my holding at 62-63.

Key Monitorables: Vodafone Idea Resolution, Covid Wave-2 provisions(we do have a sense after the BAF mid-quarter disclosure on asset quality, any probable wave-3 intensity and accompanying lockdowns.

This is a very high-level statement. How does one define “Quality of Assets”?

One needs to understand that there are different Lending segments like JLG, New car, Used car, PL-LAP, HL-MIG, HL-LIG, BIL etc

and

across all these loan products we have different risk appetites for lenders.

For Eg: SBI might keep 55% LTV for a PL-LAP with 15-year max tenure and only salaried, IDFC First Might keeps 60% LTV with 20 year Max tenure for both salaried and self.

So, for taking risk and underwriting to a segment which others are not lending to lenders will have the ability to charge high rates & fees. - This usually comes with a high “credit cost” compared to lenders underwriting to safe and proven segments.

If the lender is able to make "sustainable ROA: after “providing for risk” taken it is good business else, it is charity.

The best part with this journey is, lending to untapped pools will give you an edge over the long run. for example, Bajaj has been a decent player in the Doctors & Professionals segment and has built a massive competitive moat. Today with the historical learnings they know how to price the loans across segments & even reduce the risk and optimize returns. The same is the case with IDFC in their self-employed segments- in long run they build capabilities.

So, “Lending to nonprime segments is not bad. Lending without risk-adjusted spread and not making ROE and ROA is bad”.

for instance, HDFC Bank has 2% credit cost in 2021, which doesn’t mean it’s bad. despite having such number they made cool 16%ROE. That’s what matters.

Quantitative factors like the ones below should give us enough visibility on book quality over the long run.

This is a yes bank investor learning. all these can be identified through publicly available data.

for corporate-focused banks, the risk is highly susceptible to regulatory, economic conditions and even great lenders might go wrong- so, key in the segment to grow big and have calibrated exposure across sector + cutting down on risk based on monthly industry risk weights inputs from bureaus, Having balanced contingent liabilities/ networth (<10)…

Eg: Telecom is perhaps the most stable consumer business for the past 50 years across the world before 2012 no banks might have predicted that these companies will go bankrupt at once.

Also,Stress is a given in the lending business. one can define it by 1 in 5 years, 1 in 10 years, 1 in 100 etc, and all banks will have this stress test plan in place.

Good Banks will have the ability to grow strong during the stress period by cutting down exposures, raising T1 equity at >1 P/B - so, ROEs will go down for short period but ROA’s will hold up.

Bad Banks will have to dilute below book value, Post losses due to poor risk adjust spreads thereby destroying wealth.

IMO our focus should be on identifying if the bank is sustainably pricing the risk- This can be done from the publicly available data.

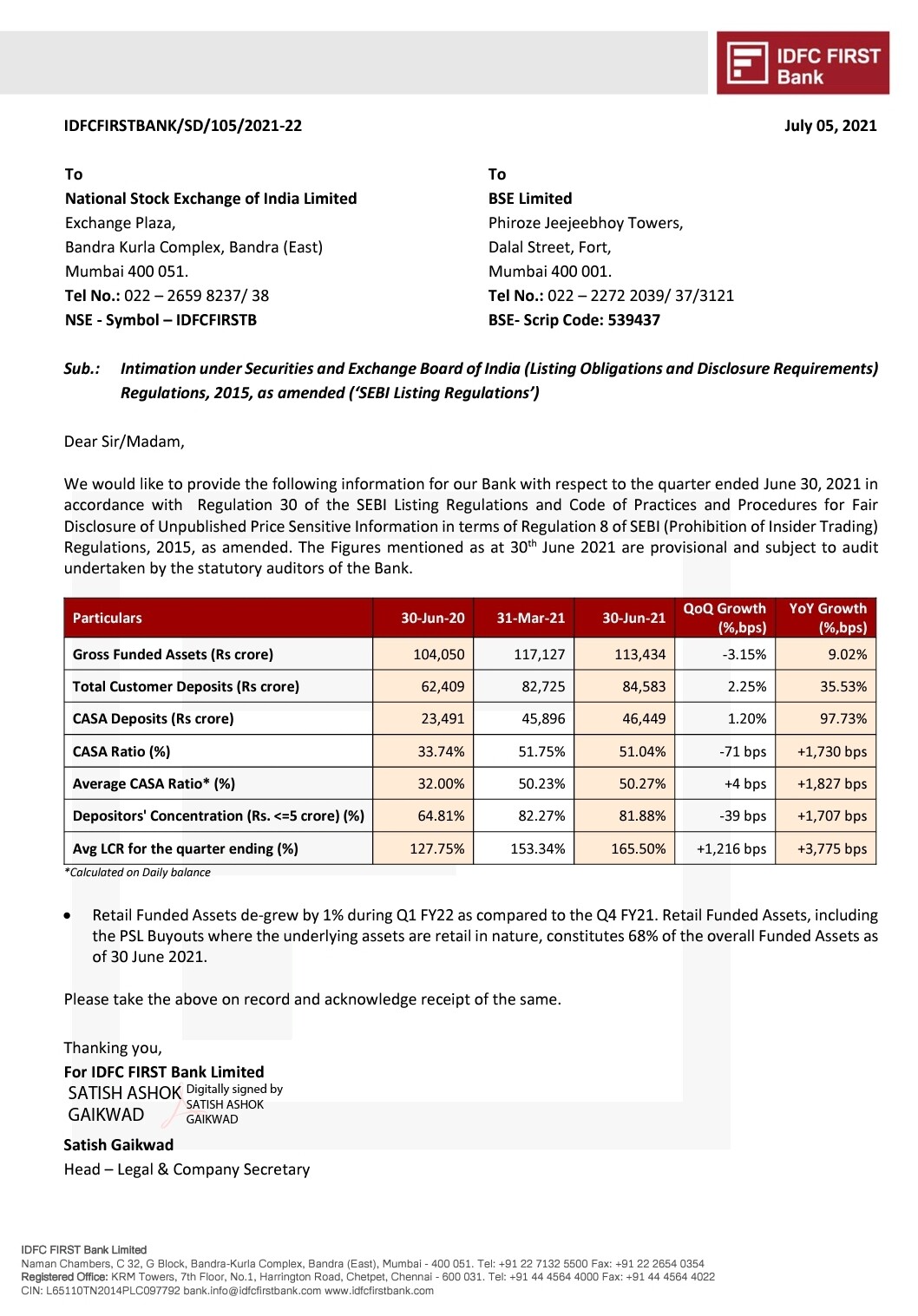

Amid Covid headwinds, this can be a big hit for bank’s medium term financials. Vodafone idea itself has raised doubt over its ‘Going concern’ status, we should see a provision in Bank’s Q1 results.

I am not sure how it fits in Management’s view where Bank is reducing the provision against this account every quarter.

Agree with you, have observed too: in last few quarters VV has got conscious about market cap. The way provisions are being adjusted: decreased somewhere to increase somewhere else is an clear indication of this. In recent past it was understandably for raising 3k crore capital, let’s see Q1’s provisions.

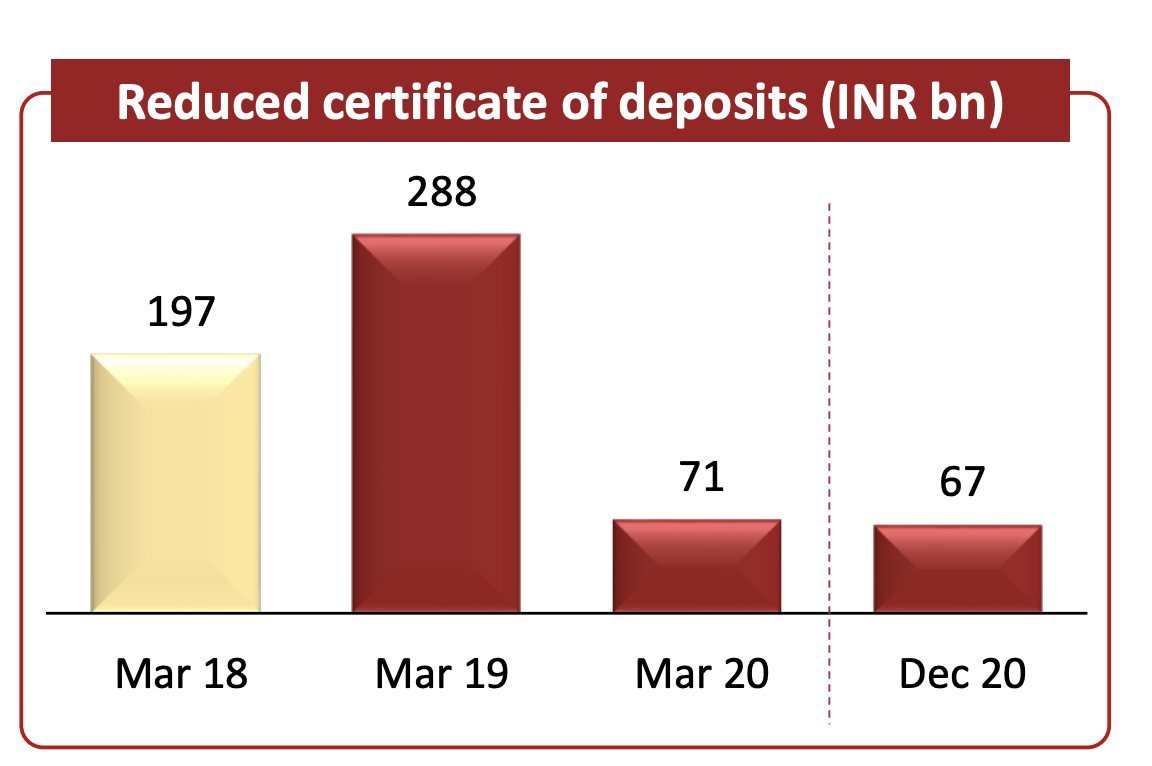

Very interesting development on the CoD and NCD deprecation, it is complete now. No more certificates of deposit. Not going into the credit rating report because it is mostly redundant information.

Cost of borrowing will come down significantly. And I suspect they are flush with casa (otherwise what would be the hurry to pay down the cod). Last part is pure conjecture on my part.

@sahil_vi I think Vodafone Idea fundraising is a key monitorable that has not been spoken of enough in this thread in the recent past … I understand IDFC F has done accelerated provisioning for this account but would be great if you could throw some light on the leftover exposure ?

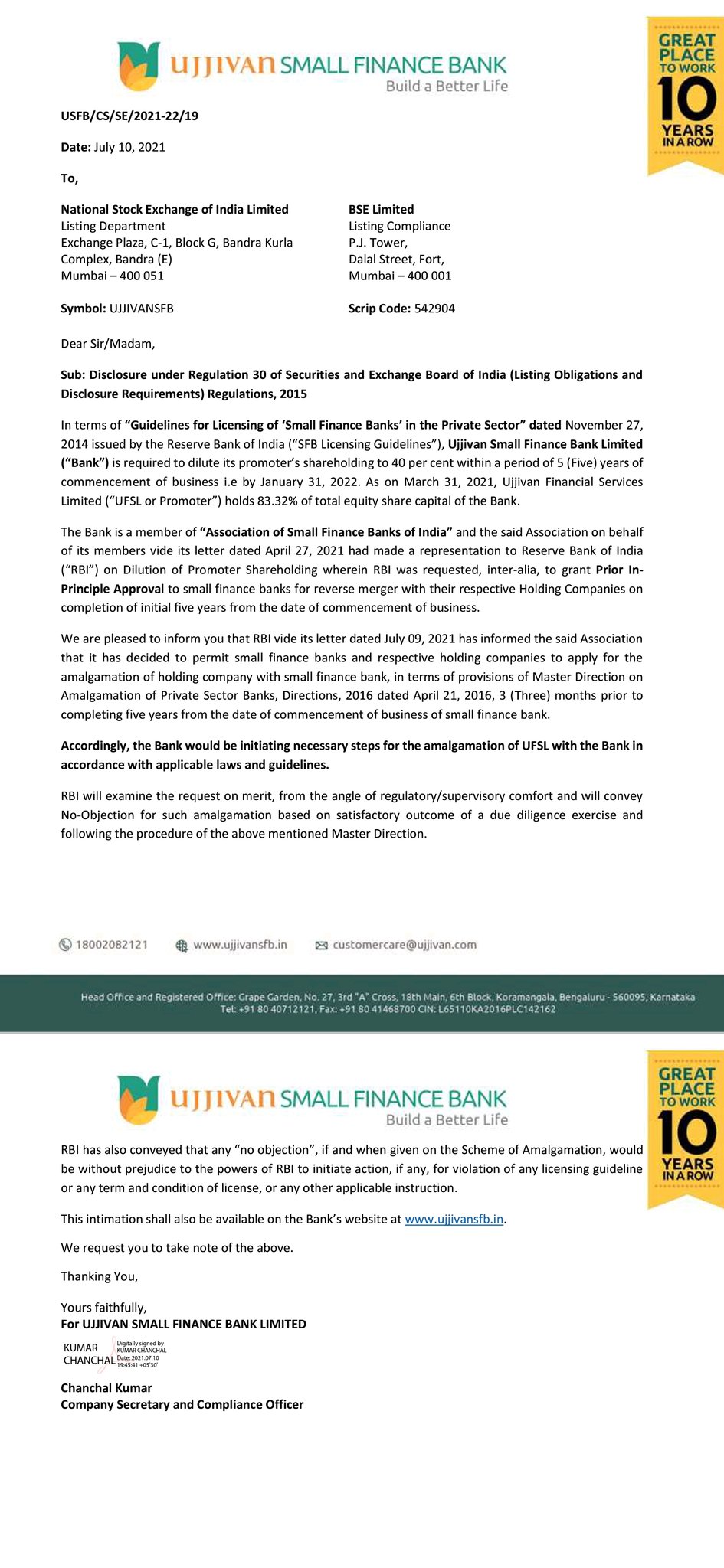

As discussed above RBI has now allowed Equitas SFB and Equitas Holdings to reverse merge. This is a very good precedent and once IDFC AMC is sold IDFC should similarly be able to do the same.

Gents,

My view on this Reverse Merger possibility.

I don’t think IDFCF is keen to absorb the IDFC business and their majority shareholders from whom they raised the capital will not allow. These guys don’t wish for further dilution of the stock.

I don’t see the reverse merger happening in IDFCF & IDFC ( again my thoughts).

Disc: Invested and Biased

Regards,

Ajay

If IDFC First can acquire its ~36% outstanding shares (currently owned by IDFC) by issuing less than ~36% of its shares to IDFC shareholders then transaction is value accretive to IDFC First shareholders. Exact value derived will decide exact terms of the merger or discount offered by IDFC to IDFC First shareholders.

If IDFC First issues 30% of its shares to IDFC shareholder while acquiring 36% shares value created for IDFC First shareholders will be equivalent to 6% of market cap of IDFC First about ~2000 cr. IDFC shareholders will get IDFC First shares worth ~11000 cr (30% of the market cap of IDFC First). So majority of the value captured by IDFC shareholders. IDFC shareholder also have 100% ownership of IDFC MF. It’s value could be between ~4000-6000 cr.

Potential payout to IDFC shareholders could ~14000-17000 cr against the market cap of ~8500 cr.

Taxes and nature of the transaction could change numbers by 10-15%.

RBI permission is only one piece of the puzzle. I believe tax treatment clarity/tax efficient reorganization is also needed from the government when bank need to organize or dismantle under NOFHC company structure.

Why would idfc shareholders agree for 30% shares against 36%. The mgmt of IDFC would be taken to cleaners for proposing any such scheme.

If IDFC bank doesn’t agree to equitable deal…they would be shooting their own foot. Such a large chunk would come to market keeping price of bank under pressure which is detrimental to bank for capital raising.