But if IDFC sells its shares in open market (40% of total bank), it will not create any value for IDFC shareholders either. It will be forced to sell the shares at a huge discount. Imho, it will lead to value destruction for both the entities.

Every major shareholder in any company knows that they will have to sell their shares at a discount to market price if they cant find a buyer who wants such a big chunk of these shares, its a simple demand supply issue. Recent sale by PE firms in Insurance companies is an example.

My personal belief is that 20% holding company discount to market price would be the base case as this is the current market practice as well. And this much discount should be value accretive for both, IDFC will get much less in case of a distress sale in the market and IDFC first will get back a big amount of equity at lower price.

Current holding company discount is 40-50% depending upon how much one values amc business at. As an idfc shareholder even a 20% discount is also too large.

And there is no rush to sell entire 36% stake at once if reverse merger doesn’t happen.

Once RBI approval is received the holding structure needs to be dismantled and shares of bank to be distributed to idfc shareholders.

Many investors who want to own idfc bank for long term are invested in it through idfc.

This discount of 6% or 20% doesn’t seem feasible and idfc shareholders won’t agree for same IMO.

And reverse merger or holdng co. dismantle is not an option, its a regulatory reqmt to bring the shareholding in bank down. Many comments revolve arnd whether dermerger is good\bad etc. However ,as per mgmt commentary, it stands as the most feasible win-win solution for both set of shareholders.

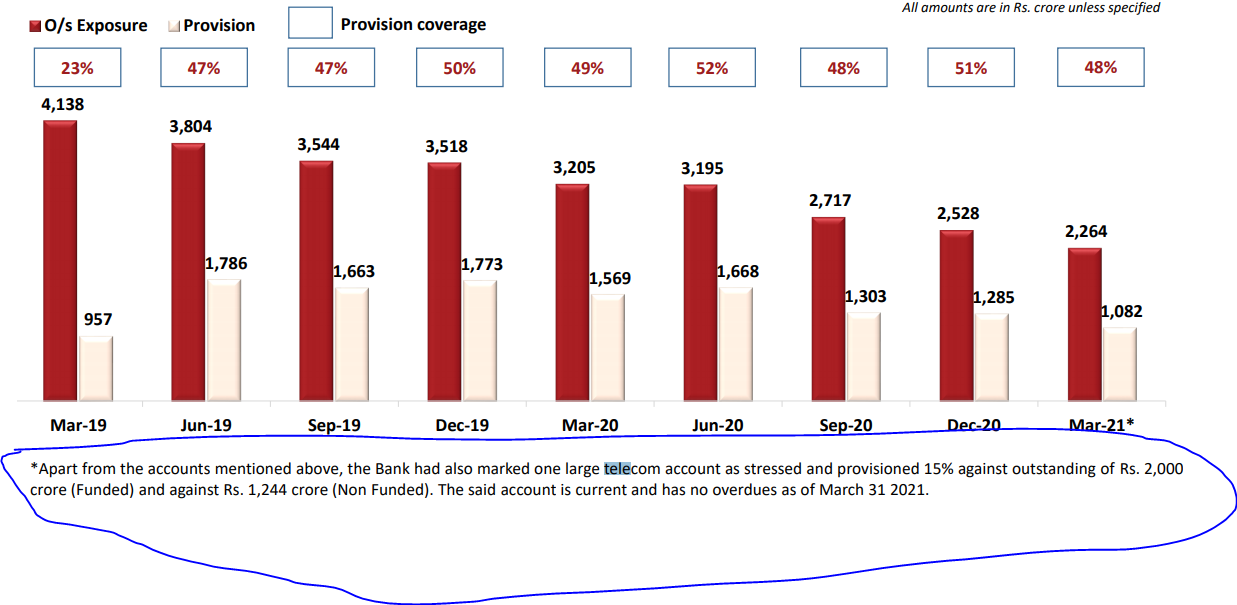

What is the exposure of IDFC FB towards VI? They had removed provisioning on VI on account of “regular payments”, so i’m trying to understand what’s the movement in outstanding exposure towards that account?

Another point which often isn’t discussed is that the downside in IDFC Ltd is much more protected than in IDFC First bank.

Case in point:

Seeing how HDFC Banks retail book is showing stress, I personally expect a painful year for retail focused banks. IDFCFB will be even more affected since the Vodafone saga will play out as well this year. One can never be sure how long the bull market frenzy lasts too. So there are 3 downsides risks to the 2X book valuation.

Here due to the value attached to the AMC , IDFC has a much lower downside than the bank. In case of upward rerating in the bank, anyways the IDFC shareholders will benefit the same, even without the holding company discount coming down.

If any of the downside risks play out and/or there is a third wave and VI goes down(expected) then IDFCFB will be happy to take the money from IDFC and do a reverse merger. It’s not that this bank won’t need capital

We would like to inform you that the Reserve Bank of India (“RBI”) has, vide its letter No.

DOR…HOL.No.SUO‐75590/16.01.146/2021‐22 dated July 20, 2021, clarified that after the expiry of

lock‐in period of 5 years, IDFC Limited can exit as the promoter of IDFC FIRST Bank Limited.

We request you to kindly take the above on record.

What’s the potential impact of this on IDFCFirstBank if IDFCBank exits as a promoter? As I understand they’ll sell the shares they own and that may create a temporary drop in the stock price. Please let me know if there’s more to this.

reverse merger will not dilute existing shareholders of IDFCF as IDFC holds 40% already. it is this 40% that will be split among IDFC shareholders… but before that they will sell existing business.

Vodafone is trying to stay in the business and refusing to give up. The longer they stay in the market the better for IDFC bank.Even if they recover 1/4 th of the total loan it is good.

News:

Cash-strapped Vodafone Idea gets nod for FDI up to Rs 15,000 crore.

Bank is considering to raise funds using debt securities. Does this means bank anticipating more loan growth or this is due to rising retail bad loans?

I think Entire transaction is handled by Flipkart platform unless customer defaults on payments…

A loan from IDFC First shows in CIBIL report of customer though, which many unaware customers complained about on twitter saying that they have not taken any loan from IDFC First…xD

.

IDFC First may be getting important information/data about flipkart customers though to provide them higher ticket loans later just like what Bajaj Finance does…

BUY NOW PAY Later scheme has options to take loan from empanelled banks and one needs to choose the vendor like AXIS bank, BAJAJ Finance etc The List of vendors does not have IDFC First bank listed in options. May be my area is not supported (Mumbai) but that is highly unlikely.

IDFCFB market cap was ~39,000 cr early March when price went up to 68. Market cap went down and then up to 37,700 cr early June but with share issuance price topped at ~60 in early June.

Now market cap is down to ~31,500 cr. Down almost 6200 cr from early June. May be impact of the Voda or expected NPA from rise of the 2nd wave.

P/B ratio is down to 1.6 now. Lowest since mid January 2021. Seems like a good entry point considering relative valuation.

I keep watching IDFC and IDFCDB prices. Few months back, IDFC was around 47 and IDFCFB was at 57 now seem to be heading for the reverse.

IDFC holdco resolution will take at least 12-18 months but both AMC and bank are going in the right direction so far albeit at slower than desired