POS Transactions are technically referred as card present transactions… which means card being actually swiped or inserted while doing the transaction hence the issuing bank’s revenue is 1.1% this is lower than the online transaction where the card is not present… which means card details are being entered in an online interface. In CNP the issuing bank’s cut is 1.4%.

5 Likes

Hello, please help me understand this, so in online transaction, because the machine is not there, so machine cost is saved and that’s why more cut for card issuing Bank right?

1 Like

IDFC first bank QIP document is a MUST read for all investors of the bank. All 600 pages are not very useful, but one can quickly glance and skip pages which are not interesting. Posting my understanding and things which enable me to average on the way up and increase the position size:

This table is the most important data dump for the bank IMO. It has good summary of a lot of ratios that we track, want to track and seek.

(Table 1)

- IDFC First bank is only a 43% Retail bank: For me personally, most important rows to track are Average yield, Average Interest earning assets, Gross Advances. Being a Retail focussed bank with loans being given at 13-15%, it is puzzling how the Average yield is 10% only. The answer lies in the fact that out of 1.45 L cr of interest earning assets, only 96k cr are loans. This means the rest are investments in corporate bonds, government securities and the like. All of these are low interest assets and the bank will eventually get rid of them thereby increasing the average yield even more. Out of this 96k cr of loans, only 66% aree retail loans. This is why i call IDFC first bank a 43% retail bank. Do observe the improvement in this over the last few years. Total interest earning assets are going down, total advances are going up. Good. A bank ought to lend money, not invest in corporate or government bonds. As the total interest earning assets goes down, retail loans go up, total advances goes up and IDFC first approaches becoming a 80-90% retail bank from the 43% it is right now, the Average Gross yield would also go up from current 10.6% to 14%. This would serve as one key source for NIM expansion.

-

The retail loan book is not as risky as analysts/investors might think: Consider following (table 2):

I have highlighted this earlier too at the time of Q3 results (post). MSME and Rural microfinance is only 27% of retail loan book and has been largely stable/constant as percent of loan book since 2019. -

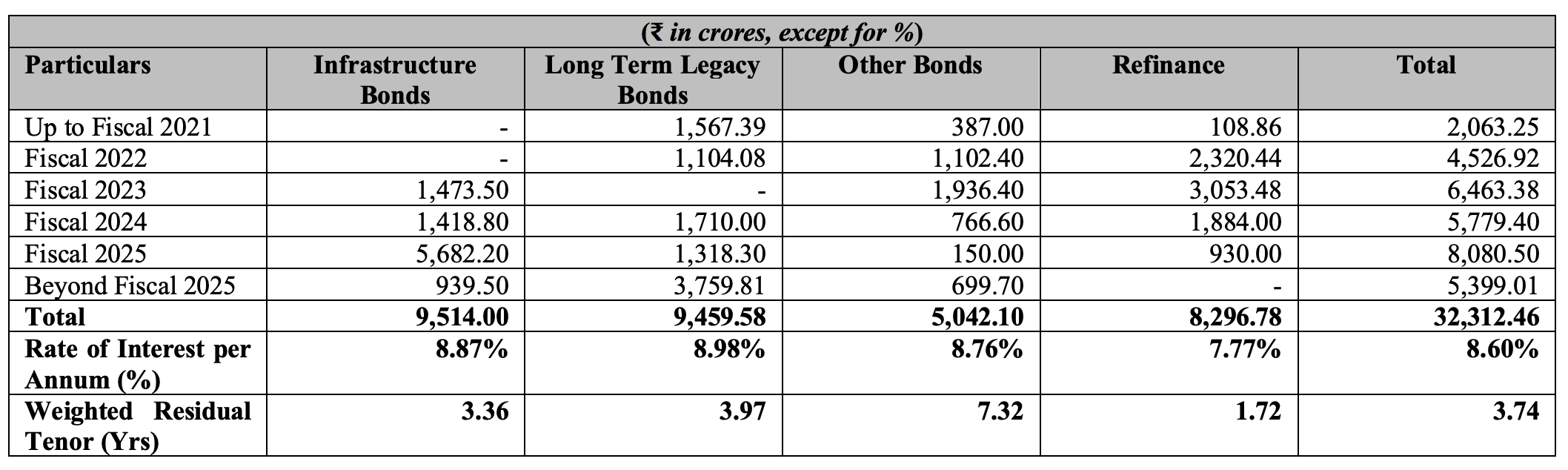

Cost of funds will go down as SA interest rates go down and high interest bonds are substituted by Retail CASA+TD: Consider table 1 and (table 3) as below:

Average cost of funds is at 6.8% for 9MFY21. This is because SA rates were at 7% throughout. As SA rate goes own and the high cost bonds are substituted by CASA cheaper, I would expect average cost of funds to go down to to 5.5-6% over next few years. -

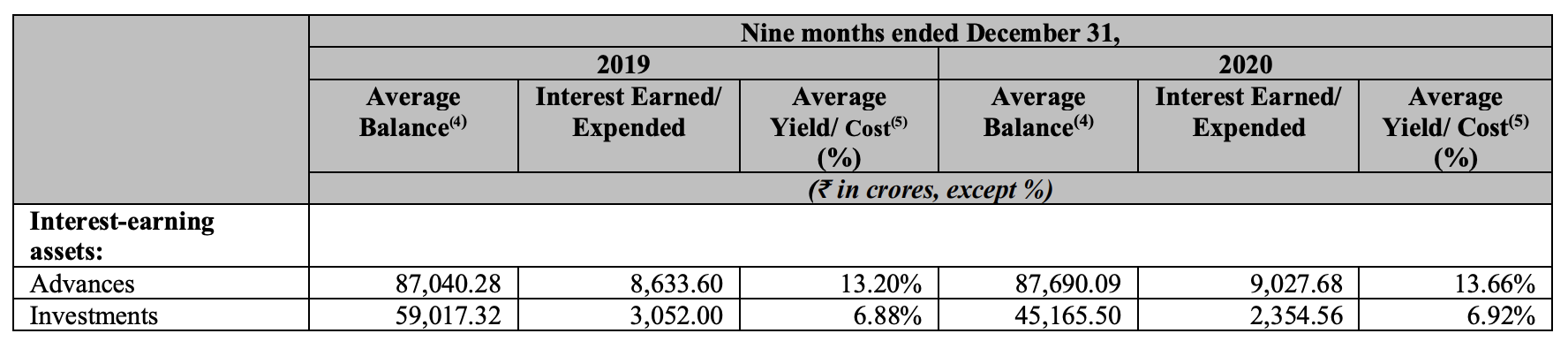

Further proof for point 1: See (table 4) as below:

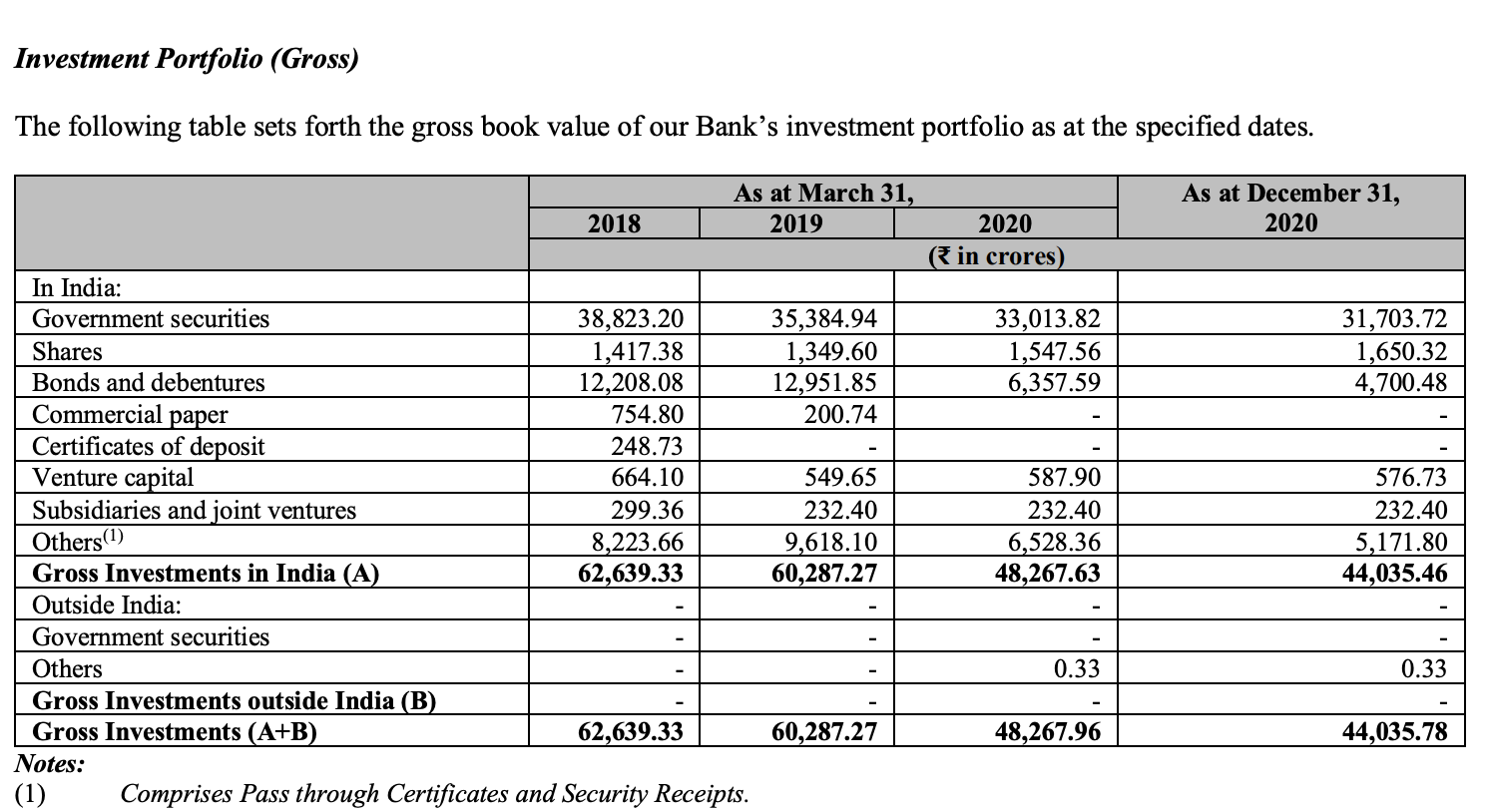

Indeed, as suspected in Table 1, the yields on advances are much much higher than the yields on investments. Thankfully, these investments are on the way down. Bank does not talk about this in their quarterly presentations and does not highlight it in their annual reports either, but this is an important part of the picture IMHO. (table 5) below shows what these investments are in.

As suspected these are government bonds which are very low yield very low risk. Thankfully these investments are on the way down. -

Further proof for point 3: See (table 6) as below:

Indeed, the cost of funds for non0-deposits is much higher. Cost of deposits would fall due to fall in CASA rate (6% at current) and overall cost of funds would fall due to falling percent of market borrowings in total interest bearing liabilities. -

Asset liability mismatch is there, but is small: See (table 7) below:

The last line is most important. At every time, assets should be more than liabilities. There is only 1 mismatch in the 1-3 year period and it is 0.57%. There is no real asset liability mismatch problem. -

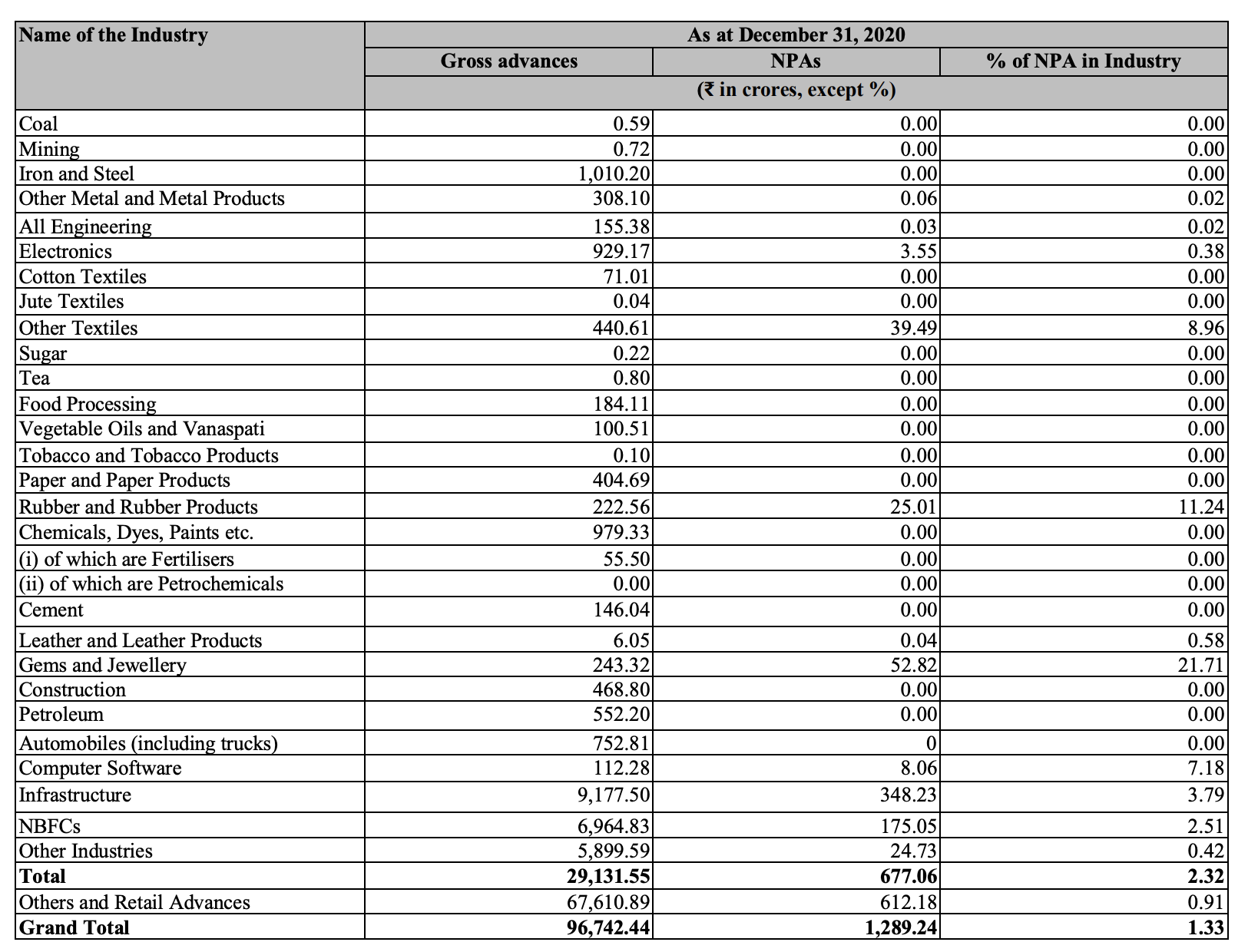

Interesting analysis of NPA distribution over industries for wholesale loans (table 8):

Infra is contributing to half of all wholesale NPAs. -

Operating expenses are rising slower than CASA/retail loan book growth:

This is good because this means that cost to income ratio should also normalize in 2-3 years to 40% from current 80-90%. -

Reason for low profitability of retail segment:

As suspected in previous posts this is largely due to exponential increase in branch network and employees. This should invert (from loss to profit) as the branch network expansion slows down and loan book + CASA grows.

Summary

Investment thesis: As the bank grows the retail loan book, it would shrink both its government security investments, and its high cost bonds. Former would result in increasing gross yields, latter would result in lower cost of funds, NIMs would touch 7-8% in 2-3 years. As infra loans goes down to 0, the ~4% NPA contribution by infra book would go down and bank Gross NPAs would normalize in 1-2% range and RoA would become 1-2% and RoE would become 15-20%. Retail book would grow at 20-25% and bank would be valued at 3-6x book value.

Disc: Investment thesis is presented as an educational exercise. This is not a buy or sell recommendation. I am invested in this company and hence positively biased.

61 Likes

A large part of the Govt bond holdings are due to SLR requirements set by the RBI and are necessary. You can read more about it here- https://blog.investyadnya.in/what-is-statutory-liquidity-ratio-slr/ and here G-sec rate: Minimum GSec holding limit for banks to be cut by 125 bps - The Economic Times

5 Likes

Yes! and if it is happening then when this will happen. as I remember, the same is being discussed for the last 4 years or so plus recently I guess in Dec-Jan suddenly the news(?) came and IDFC ran from below 30 to above 50 and then the excitement died down again. and even VV denied the news.

1 Like

Please refer to IDFC’s AR of 2020 & Concal of Q3 FY 20-21(available on youtube).

Management has elaborated the plans to declutter the structure.

At current price IDFC is available at 50% discount.

1 Like

A crude calculation of discount between IDFC & IDFC First Bank. Amt in Crs. 30% discount is to take care of taxation implications/expenses etc

| Mcap | Stake | Dis Factor | Value | |

|---|---|---|---|---|

| IDFC | 7614 | |||

| IDFCFB | 32978 | 36.60% | 30% | 8,449 |

| IDFCMF | 3500 | 100% | 30% | 2,450 |

| Net cash | -47 | 0% | 100% | - |

| 10,899 | ||||

| Upside | 43.14% |

3 Likes

IDFC First is going pretty aggressive on premium banking programs too. Received a call from the wealth management team about the same and seems like they are targeting customers from Citigold, HDFC Imperia etc. They will be coming out with a detailed program launch(called IDFC Wealth Select or so) in the next 10-15 days is what I was told on the call.

8 Likes

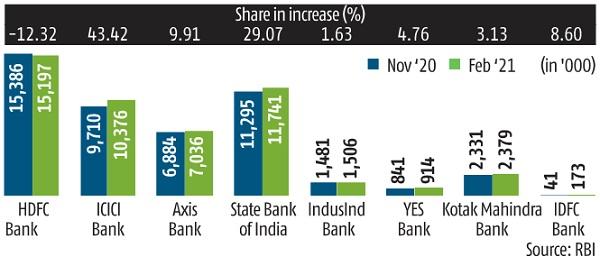

As per ICICI gains at HDFC Bank's expense, issues 665,000 incremental credit cards | Business Standard News

IDFC First Bank saw its outstanding credit card go up by 131,000 from 41K to 173K. That gain is close to Axis’s gain of 151K albeit from smaller base.

18 Likes

Came across this article that mentions that IDFC First is one of the institutions that has provided debt funding to Bizongo; a loss-making startup. Packaging materials platform Bizongo closes Series C funding round | VCCircle

How should one view this news? Though the amount is likely to be small, using any amount of capital for venture debt makes me very nervous. How can anyone get any confidence on the quality of the book long term if the bank is underwriting these sort of debt instruments?

5 Likes

Bizongo has good cashflows from past few quarters and they have good client base like bigbasket, Nykaa etc…Sounds like good business. That’s why they funded.

I feel this much better rather than funding Infrastructure and telecom companies. I think a bank should also lend good and emerging businesses. You can’t solely rely on retail business. ( My personal view)

6 Likes

part of business, the debt venture - even it is small, if you see the promoter and the entities backing up, the risk reward is worthy… i personally feel nothing wrong in the venture…

3 Likes

As per my understanding, banks cannot undertake Venture Debt. Venture debt typically involves instruments where a portion of the debt converts to equity to capture the upside. These conversions happen in banking only during debt restructuring.

My guess is that the bank has provided working capital/Supply chain finance or some other form of collateral based debt. The article wrongly captures (or rather depicts) it as venture debt.

Again these are my 2 cents and I may be completely wrong

Disclosed: Invested

4 Likes

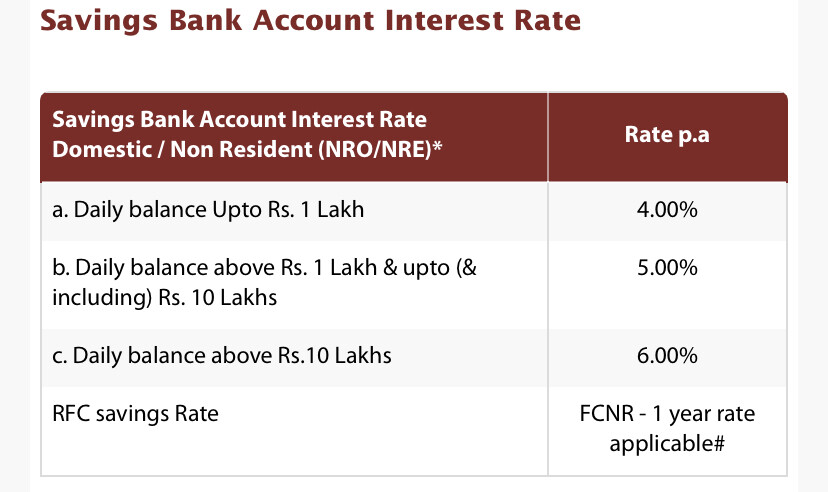

New SB rates from May 1,2021:

6 Likes

@Krishna1 Can you share the source of this press release? Strangely, cannot find this on either NSE/BSE exchange disclosures and this is price sensitive information. Poor corporate governance I’d say.

Anyway, if it is true definitely plan to transfer all my balances to somewhere much more lucrative like Indusind (screenshot) or even Yes Bank (after vetting financial stability). Infact even contemplating closing my account, don’t need so many accounts if not going to use them.

Hopefully for IDFC First investors, most people won’t be like me.

The next 6 months will be a good test of this bank’s retail deposit funding!

Disc: No investments

7 Likes

This is a great sign for investors.

At the least it shows that with currently available data the management believes that giving less than 5% interest on savings accounts is in order even when the NIM currently is around 5%.

If the retail liabilities keep coming in then the bank will then have one half of the 2 competitive advantages in banking- low cost deposits. The other half of low credit costs can then be worked on(a lot of my colleagues are looking at IDFC for their data analytics jobs)

Interesting times!

2 Likes

My view is that the decrease in the rate has ro do with a few points

- Overall system liquidity is high.

- Given covid and second wave, expected slow pace of vaccination, RBI would try to keep the rates low to prop up growth.

- The credit offtake is low. further the offtake from strong clients has not been great.

In such a scenario, excess liquidity is a buden . So there is no point in keeping rates high if you would have to deploy surplus in repo

9 Likes

Rating reaffirmed

1 Like

In the long run, IDFCFB should compete for deposits through good service and safety of deposits etc. Higher deposit rates shows weakness. Now that the bank is moving forward and has sufficient CASA, it should eventually go to 4% uniform savings rate upto 10 crores at an appropriate time.

6 Likes