Thank you Sahil for the explanation

While I agree on the general thesis on the bank, with due respect, just wanted to point out that the loan book mix changed immediately after the merger ( Dec 18 ) to March 19 quarter and has remain consistent more or less ever since. We all know this largely happened because of the legacy Capital first book. So I don’t think it’s has been ignored by the critics ( I am not one  )

)

Seems Morgan stanly are also curious by the amazing run the bank has had and have scheduled for a one-on-one meeting with the bank, perhaps to verify what are they missing.

Disc - remain invested, accumulated heavily during the downfall from 30-18 at all levels and is the largest position in pf.

2 Likes

I like this presentation compared to fluffy and repetitive one published with results.

Bank should keep historical information and additional details in separate presentation and focus on current business updates in the quarterly results.

2 Likes

There is a discussion about IDFC First bank in the morning context article on CRED [Pay wall]

Few mentions of IDFC First Bank:

-

CRED disbursed around Rs 1,000 crore worth of loans in the past five to six months [For now, IDFCFB is their only partner. They are exploring other partners with 5-6 in pipeline]

-

Estimating 2-3% revenue for CRED

-

CRED earns “a distribution fee and a share of revenue from the banking partner for curating a high-trust audience for them and managing the overall experience,”

-

IDFC First—which is a young and hungry bank—is getting a free premium customer base, so they might be giving something for lead and something on every loan getting disbursed. Lower fees for leads generated and higher cost for disbursal. Some Rs 200-300 for lead generation (which lenders already pay to Google for showing their ads on top of the search engine), and on CRED they are getting more qualified and richer leads. Conversion would get [CRED] some 1% to 1.5%, if the loan is disbursed at 13% interest

-

“I don’t think banks like ICICI, HDFC, Axis and Kotak, etc., will see any value as this is cannibalizing their existing client base. This only makes sense for people who don’t have a client base and are starting new in this business,” adds the banker

-

A top executive at a Mumbai-based private sector bank explains that for a younger bank like IDFC First, to earn 10%-11% (after deducting CRED’s commissions from an overall 12-15% interest rate) on prime customers is not bad. “IDFC First must have done some risk analysis that, after losses and some cost, we will still be able to make money. This is a customer acquisition cost and and … the cost of funding is 6%-6.5%, so they must be thinking we can still make some spread,” he says. Retail banks have low capital costs because they can rely on low-interest savings and current accounts.

-

CRED becoming an NBFC comes with its own set of challenges; for one, the central bank has been leery of companies that are funded through jurisdictions such as Mauritius, a common route for venture capital firms such as CRED’s investors. Also, NBFCs’ cost of capital is much higher than that of banks, which as we noted have low-interest deposits; NBFCs need to raise their own debt, often at 11-12%, which means issuing personal loans at 12-15% is no longer an option, says another industry expert.

22 Likes

Does anyone feel valuation of the bank is stretched right now? Bank still needs to execute correctly on lot things but already trading at 2.x P/B ratio. Even when ROA and ROE is much lower than larger competitors such as Axis and IndusInd, P/B ratios for all these banks are comparable.

If IDFC’s profitability is stays around 100-200 cr in next 4-8 quarters then bank will need to raise further capital just for growing the balance sheet.

Bank’s strategy seems to be to launch customer friendly products such as credit cards which will be low/negative margin to build market share. Most cost sensitive/low margin customers might not be the best customers for the bank. These are likely to move for marginally better product/services such as slightly better interest rate or credit card offers.

Partnership is with CRED is interesting too. CRED is getting commission from the bank for bringing customers, does that indicate weaker marketing/brand of the bank to reach out to prime customers? Are advertising, attractive deposit rates and credit card offers not enough to get these customers? Capital First has been in the lending business for almost 10 years and merged in Dec 2018 but still relying for CRED (started in Nov 2018 with $1 million funding) to acquire customers. This just indicate challenges for upstart bank like IDFCFB going forward.

FinTech startups are attacking lucrative slices the entire financial value chain either by owning those slices or reducing margins via products such as direct mutual funds, insurance marketing, forex transactions, loan origination etc. CRED has raised $210 million (1550 cr) and has already garnered 20% of the India’s credit card holders as users.

5 Likes

So are you suggesting banks should not be working with fintechs?

What I hear is that fintechs bear the first loss, and hence it becomes a risk free business for any funding institution provided the cost of funds and capital is sufficiently low and hence leaves room for decent margins(Nims)

2 Likes

If IDFCFB is in business in 8-10 years but still need to rely on upstart for customer acquisitions then it shows limitation of the business. I believe most the credit card customers within India are in tier 1 & 2 city. So basically CRED is bringing these customers to IDFCFB. These must be younger and tech savvy customers which prefer CRED and getting IDFCFB’s loan product via CRED. I am trying to think about this business dynamic and its implication on IDFCFB in the medium to long term. This scenario highlights weak position of IDFCFB in the digital market. It can be compensated with tie-up with CRED but in medium to long term it is beneficial to build IDFCFB as a first choice in mind of customers for their need instead of CRED. So far IDFCFB hasn’t been able to do that and going forward its fintech competitors are only getting stronger. This business dynamic is going to limit bank’s ability to earn higher ROE in future. Can IDFCFB sustainably generated ROE > 12-15%?

What is the alternative to working with fintechs? It’s beneficial for margins but going to limit growth. Bank will have to offer better digital experience to acquire customers using that channel. Now bank has to be good at underwriting as well as digital experience.

CRED might initially work with IDFCFB but going forward, it will list 4 other competitor banks to enable customer to price shop for commoditized loan product.

CRED’s business model has been questioned as well. It seems to me they want to be take a hit initially to acquire well-off customers and these losses will increase with additional customers but losses arising from upfront investments in technology platform will payoff with sufficient scale. It will become barrier to entry for next set of competitors.

Financial industries across different countries are getting homogenous. US/China markets are ahead of the curve for India and hence similar development will be seen in India. Bigger banks have scale to spread fixed cost of technology over larger customer base but for smaller banks it is going to be difficult unless they are really good at executing significantly better.

I am highlighting risks for the business in light of current valuation and expectations.

7 Likes

Regarding valuations, yes it is high right now given stressed book and potential covid related NPAs. I haven’t bought any new shares in the last 4 months and don’t find the current prices attractive.

But IMO other concerns you have mentioned are not a big deal for the bank. You can think of CRED as DSAs or people who download the partner app. The bank only needs to bear a one time cost to acquire a credit worthy customer’s information. After that they can do something like “download our app to get better offers”, where they can reduce the interest rate (which otherwise would have gone to CRED).

Partnerships with startups is inevitable, in fact banks that don’t partner quickly will be left out in the future because of how fast things are changing and how much things are interconnected these days. Startups have the advantage of being nimble, fast decision making that gives them an edge over established corporates, going against them is risky and costs can spiral out of control. They will always have the upper hand when it comes to UX. So partnering is the best way to gain a piece of the pie at low cost and stay up to date at the same time.

Banks, NBFCs, MFIs, and fintechs will have to co-exist, no way around it.

Disc: my top holding, no transactions in the past 4 months, not a recommendation

4 Likes

Compared with banks, IDFC might feel fully valued today but like Vaidya says it’s really following an NBFC lending model with a bank liability structure. This fact is quite evident in the NIMs which are higher than peers and will continue to expand. As a result its best to use a multiple that builds that fact into it, so maybe a combination of banks and NBFC’s.

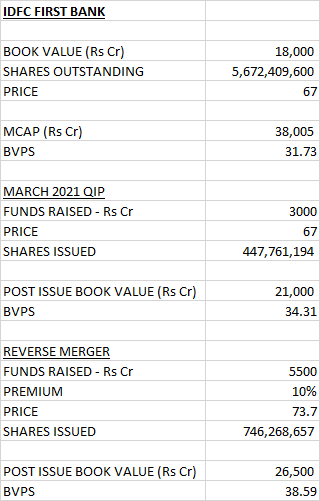

Logically speaking that would be the way to look at it, but theres no point spending too much time on that as the market can surprise you both ways. Is there any argument for why Bajaj Finance trades at 5-6x or a SFB like AU trades at 6x? The way I think about it is if in 2-3 years time the bank is able to hit its 5 year targets (as mentioned during the merger) and is growing its retail book at 25% (as stated by Vaidya) then there is a pretty good chance that its multiple then would be higher than it is today; if market conditions are anything similar to today then could be significantly higher as well but I am not counting on that. Secondly, by then the IDFC-IDFCB reverse merger would have probably gone through as well. This is important, as discussed above IDFC will have anywhere from 4000-6000cr from the sale of the AMC and when it reverse merges two things will happen. Firstly the bank will have sufficient growth capital for the next 3-4 years and secondly if the reverse merger happens at todays price/valuation then the book value of the bank would go up materially. As per my calculations post merger the book value of the bank would be close to Rs 40 which means that at Rs 70 the bank is trading at somewhere around 1.75x BV.

9 Likes

Thanks for your input. Very helpful.

Grateful if you can provide calculation for reverse merger? Many thanks

These are my rough calculations based on this discussion- IDFC First Bank Limited - #1492 by Puch

The Book Value I have taken is higher at 18,000cr as its my estimate of March 2021 BV ( Dec BV was 17,700cr)

5 Likes

March 2021 Qip is @67 rs? Or ur estimate?

Hi Puch, why on earth will IDFC shareholders settle for 746 million shares of the bank ? IDFC owns 40% of the bank…and no reason why they would settle for anything else. Also your calculation shows that the AMC money ( if sold ) will also go to the bank. That is in no way a possibility…and will naturally flow to IDFC shareholders only…via a payout or share spin off !!

3 Likes

The 746 million shares are in addition to the 40% bank shares already owned by shareholders. These shares wold be issued for the cash recieved from the sale of the AMC. Its far better from a tax angle to get shares in the bank rather than to recieve them as a dividend. Its a win-win situation for all parties involved.

My suggestion would be to read recent IDFC concall transcripts to get a better understanding of what the IDFC management is trying to do with the reverse merger and extract maximum value for their shareholders.

Edit: the point of the above calculation is only to figure out what the book value of the bank would look like post the merger and not show the entire reverse merger process. There are additinal steps in that and those are not shown here.

4 Likes

Quite appreciate the details,thanks ! Unfortunately while a whole reverse merger into IDFC Bank is the win win ( as you rightly say ) the current NOFH holding type companies defined by RBI cannot do/hold anything else…hence the AMC spin off or sale seems the way out. …before the IDFC NOFH / IDFC Bank merger

1 Like

Very impressive and learned views by the participants. IMO with so much liquidity being injected by govts, and the IDFCF bank on a very sound growth track, it should be able to get a premium over market price in QIP ??

1 Like

If your hypothesis regarding IDFC talking customer from Cred is right and having week distribution, then we should also think a HDFC Life distributing on Policybazaar and a Nike/lever on Amazon means the original non digital companies business model are week.

I believe we need to understand that these are all distribution channels and should be taken in that spirit. Yes the distribution channel will have the charges which it has, but each business who is using these channels need to understand the corresponding cost it incurs while using other owned or non owned distribution channels.

Whilst I didn’t update earlier, IDFC Bank has been a long term holding for me, and I have a belief it will continue to be.

3 Likes

In My opinion, this statment is made while missing some important points. In past, Capital First was in retail loans and was NOT providing Credit Cards. The customer base was and is mainly “no credit card” category, for IDFC, they were mainly into Industrial loans. Now that IDFC FIRST is venturing into Credit card business they want to get customers by all means. The present form of IDFC FIRST is just 2 years old and need to establish themselves.

Plus we should look at how aggressively they have partnered with Flipkart, Cred, Niyo etc.

Disclaimer :- Invested.

5 Likes

I agree with Puch and r13rk. I would like to add that acquisition of good customers is a continuous activity and the companies try to improve the percentage of good customers all the time. In a manufacturing company, top 10 percent dealers usually account for 70 percent sales. If we make a list according to profits generated by dealers the percentage would remain similar although the composition may change somewhat. I do not know what would be the situation in a retail bank but I am certain that 90% of troubles are generated by bottom 10% customers and disproportionate profits would be contributed by top 30% quality customers. So it makes sense for a bank like IDFCF to throw their net far and wide for quality customers as a continuous activity and weed out parasites.

4 Likes

@valueinvesting101 I disagree. There can be more than one way to acquire a client. Further, the clinetele of a bank differs from that of an NBFC. Many clients who would not go with a CAPF, wuld go with a IDFC First.

1 Like