The NPA numbers 4.18 is for the whole book, 3.88 is for the retail book. Since the bank is moving towards more retail i think he might have emphasized the retail NPA numbers of 3.88. Is the reverse merger bad for the bank shareholders?

2 Likes

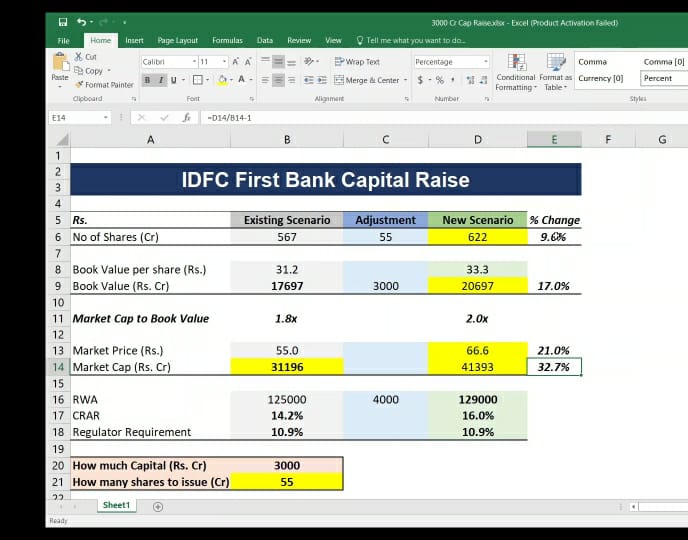

Please see the table below, which shows the impact of capital raise on book value, market value and Capital Adequecy

The same is explained in the Video Below

Hope this helps ![]()

5 Likes

I’m not sure, I have absolutely no knowledge of this, what I’m hearing on forums and other platforms is that it is good, in fact, buying IDFC instead of IDFCF will be better to get IDFCF share at a lower price is what I have heard but I don’t know how this works and instead request someone here to elaborate on this.

P.S. if you asking me because of my post above, then I’m sorry if there’s a misunderstanding, all I said is maybe they are planning with demerger but VV don’t want to say this in the media so early that’s why he seems hesitated when asked about the reverse merger. ![]()

3 Likes

IDFC owns 1.42 times of IDFCB + AMC Business that is valued at approximately 3k to 5k. The current holding company discount is close to 50%. Even if IDFC pays a premium to IDFCB for a reverse merger, it is worth it. IDFC is waiting for RBI guidelines, once it is out AMC business would either be listed or sold to any party, then Reverse Merge is possible. To sweeten the deal, IDFC can pay the premium, so that IDFCB gets additional capital, which will increase the BV as well. As you know the president of INDIA owns 16.37%, which means 23.245% of IDFCB owned by Govt + AMC shares. Govt will have a bigger say in this reverse merger if it happens. Any premium that would be paid will take stock to higher prices. This is what we want as IDFC Limited shareholders. Invested in both IDFC and IDFCB in the ratio of 3:1.5

5 Likes

President of India (Govt) owns directly 4.61% in IDFCB and 16.4% of IDFC. If the two entities are merged then the Govt will own around 11% in the merged entity and not 23%. This ofcourse is excluding the AMC. The AMC is on track to delivery a Rs 200cr PAT in FY22 with a 75% ROE; comparable companies are trading at 35-40x in the market, if we take a 25x multiple for the AMC and a 20% acquisition premium then it works out to atleast 6000cr. The LTCG on this will be around 500cr and the Company will have 5,500cr free cash available for the merger.

3 Likes

Thanks hrdk3110. This was very helpful. Extending this logic, for banks like HDFCB and Kotak which always trade well above BV and therefore always raise capital at a similar price, equity dilution doesn’t seem to be a negative at all. Because the price they raise capital at will be such that their BV / share will increase, despite the dilution.

This is unlike most other companies where dilution is seen as a negative. Therefore for such banks raising capital is an unambiguous positive, provided they can then deploy the capital in a risk adjusted and profitable manner.

3 Likes

From where does the question of premium comes in?

Its a reverse merger and not acquisition of shares.

Assuming the reverse merger has to take place:

First IDFC will have to sell AMC business then they will distribute the cash in form of Dividend.

In step 2 they will collapse the company structure and merge it with the bank. Every share holder of IDFC will get 1.4 shares of the IDFC First Bank for 1 share held in IDFC.

Im unable to understand how does this question of premium comes in? What am i missing here? The point is that if IDFC buys shares of IDFC First then how is that a reverse merger, isnt that a simple share acquisition by the promoter?

Very interesting discussion on this forum on multiple aspects of IDFC First’s business and quite enlightening. The bank as per its stated objective set out to increase the share of CASA among its liabilities and has more or less achieved the same. I feel the next target for the bank, as per their stated objective and for investors to focus on, should be the cost to income ratio. Currently it is at 79.2% and is very high as compared to most other banks where it is sub-50%. Even the stated objective of bringing it down to 50-55% is on the higher side.

| Dec-20 | |

|---|---|

| Cost to Income Ratio | |

| Union Bank | 46% |

| Indusind Bank | 41.30% |

| AU Small Fin Bank | 49.20% |

| RBL Bank | 47.90% |

| Bank of Baroda | 47.74% |

| Canara Bank | 49.89% |

| Kotak Bank | 42.3% |

| DCB Bank | 46.68% |

| Indian Bank | 46.92% |

| South Indian Bank | 54.80% |

| Federal Bank | 49.82% |

| Karnataka Bank | 43.24% |

| Indian Overseas Bank | 43.50% |

| Punjab Sind Bank | 74.46% |

| State Bank of India | 53.25% |

| Bank of Maharashtra | 50.70% |

| IDFC First Bank | 79.20% |

If the bank is not able to control this, all other efforts of higher CASA or better NIM will be frittered away in costs. The cost to income can come down either by increasing income and or reducing costs relative to the income. I feel investors would be better off focusing on these two aspects to monitor the bank performance from hereon.

Disc: Long term investor

14 Likes

Regarding reverse merger, IDFC Ltd management has confirmed (check their latest concall) that during reverse merger, IDFCB will have to assume any contingent liabilities (incl tax liabilities) of IDFC Ltd. Hence, the reverse merger has to be negotiated between the bank and IDFC ltd, and the bank shareholders have to approve the transaction. IDFC Ltd only has 26% voting power for its 40% stake. The ratio, therefore is likely to be lower than 1.42 for each share of IDFC. That is, assuming the bank is interested in the reverse merger.

1 Like

Bloomberg report nothing new here…

IDFC First, India’s Youngest Private Sector Bank, Makes A Dash For Growth With Fresh Funding

IDFC First Bank Ltd., one of India’s two youngest private sector banks which came into being amid a multi-year bad loan clean-up, is hoping to leave asset quality concerns behind and make a dash for growth as the Indian economy revives.

The lender approved a plan to raise Rs 3,000 crore on Feb.18 via private placement, a follow-on public offer, a qualified institutional placement or a combination thereof. This is the second time in a year the bank is raising capital. In June 2020, IDFC First raised Rs 2,000 crore by issuing preference shares to entities including its promoters Warburg Pincus and IDFC Financial Holdings Ltd.

The latest round of fundraising will help the bank grow its loan book at a steady rate of 25% year-on-year for the next few years, V Vaidyanathan, chief executive officer of the bank told BloombergQuint.

Our stated agenda is to grow the book at 25% every year for the foreseeable future. Considering that we are targeting the retail and small business segment, it is entirely possible to achieve this growth rate.

Retail, Retail, Retail

IDFC Bank, which started operations in October 2015, had a bumpy ride in the first few years. The legacy of IDFC’s infrastructure lending past was a weight and attempts to grow retail loans and deposits organically was proving to be a struggle.

After a failed merger attempt with the Shriram Group, IDFC Bank merged with Vaidyanathan promoted Capital First, giving the lender its current avatar of IDFC First Bank.

From the start, Vaidyanathan said the bank would focus largely on retail lending, a business where he spent most of his career while at ICICI Bank.

As of December 2020, retail loans made up 60% of IDFC First’s book, up from 49% in December 2019. The bank’s total loan assets as of Dec. 31 stood at Rs 1.1 lakh crore.

Mortgage financing and consumer loans dominate the bank’s retail loan portfolio, constituting 72% of total retail assets. The consumer loans segment includes two-wheeler loans, used cars financing, gold loans and consumer durables loans, Vaidyanathan said.

“Mortgages will be the bedrock of our growth story. But we would also grow our gold loans, two-wheeler loans, small business financing and rural loans to achieve the 25% yearly growth target,” Vaidyanathan said.

But these are businesses that all large private banks are looking to grow. IDFC First’s relatively higher cost of funds will mean that its asset strategy would need to include riskier lending, said an analyst.

“Considering the higher cost of funds for the bank, it would effectively have to take higher risks in the retail lending portfolio to maintain healthy margins. But the question will be on the quality of underwriting on this book,” said Dhananjay Sinha, director and head- institutional research, Systematix Group. The higher risk may directly result in a higher credit cost for the bank, but the current fundraising plan should address this, he added.

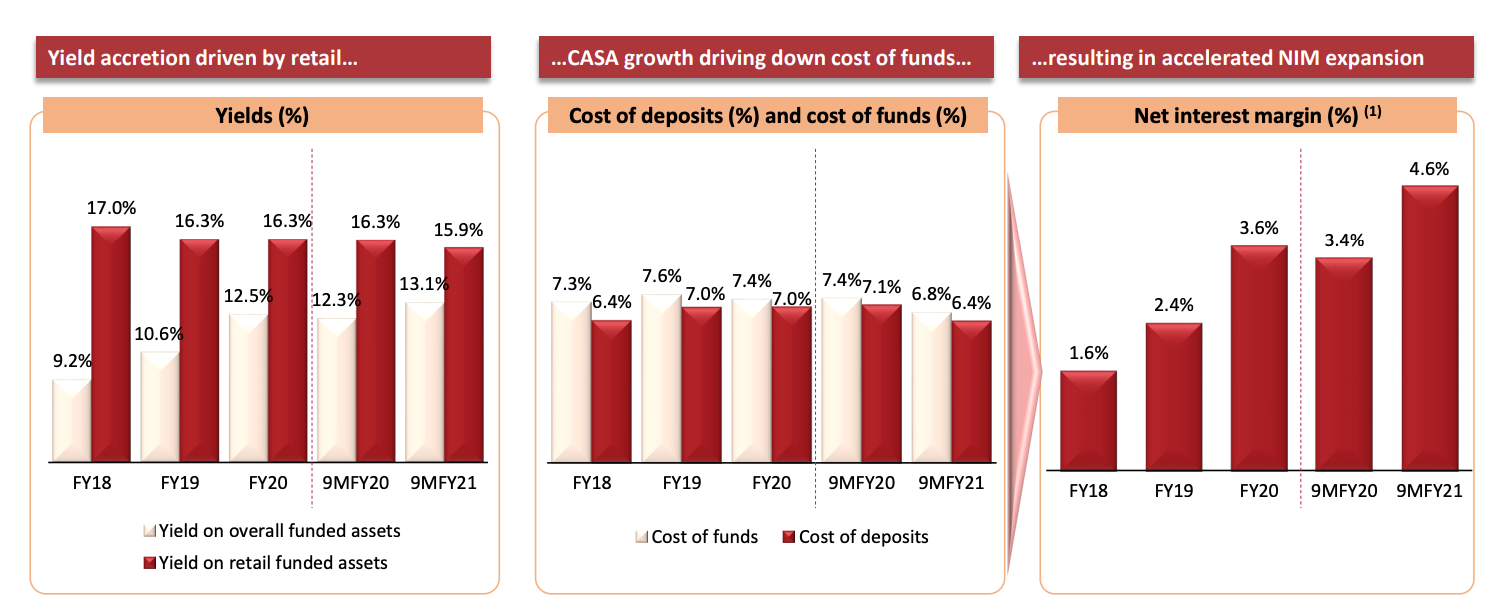

IDFC First Bank has 48.31% of its deposits in the form of current account and savings accounts. However, it has maintained a relatively high-interest rate of savings deposits at 7% till recently. In February 2021, the bank lowered its savings account deposit rate to 6% for deposits up to Rs 1 crore.

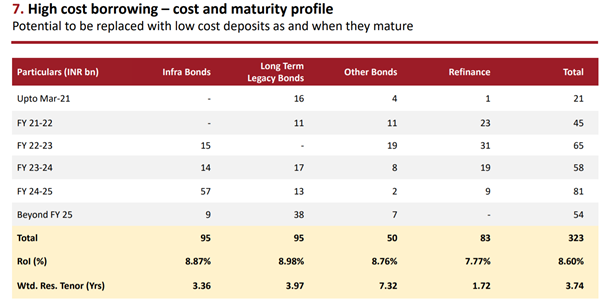

In addition, it has high-cost legacy borrowings.

We have about Rs 35,000 crore worth high cost legacy borrowings on our liabilities, where the average cost is 8.5% and that is trending downward. Considering the growth in our retail deposit base, there is a great opportunity for us to repay the high cost liabilities in the next three to four years and improve our cost base.

The bank’s current blended cost of funds stands at around 6.8%, he said.

Should the repricing of infrastructure bonds go smoothly, the bank will benefit, said Asutosh Mishra of Ashika Institutional Research. “We feel that with the repricing of the infrastructure bonds on the bank’s liabilities profile, its cost of funds is likely to improve significantly. This would have a positive impact on the margins,” Mishra said.

Bad Loans Not Yet A Problem Of The Past

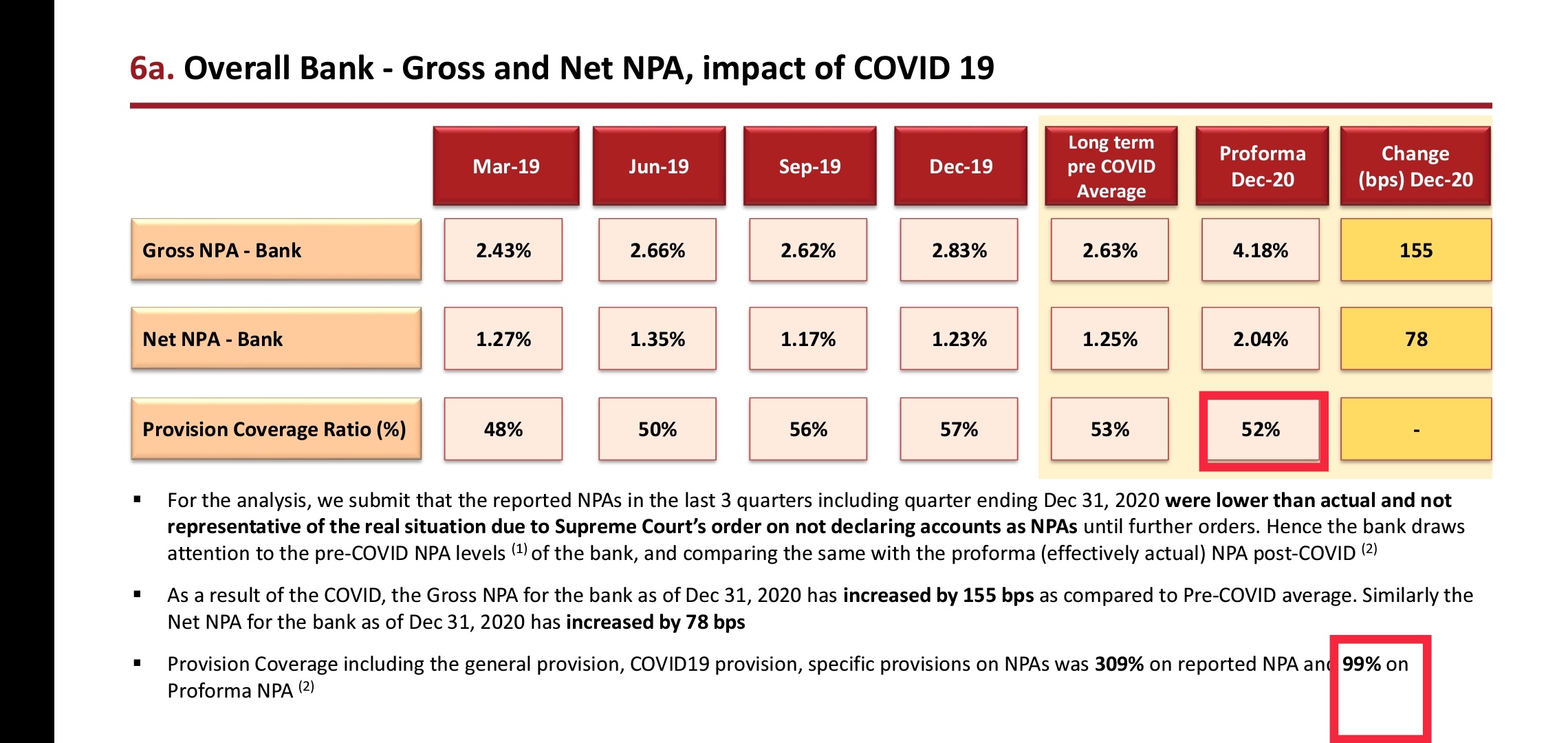

While IDFC First Bank appears eager to grow, asset quality concerns are not yet a thing of the past. The Covid-19 crisis has pushed up bad loans at the lender to nearly double of its long term average.

IDFC First Bank’s proforma gross non-performing asset ratio stood at 4.18% in the third quarter, as compared with 1.87% in the September quarter. The proforma bad loans include those accounts which should have been classified as NPAs if the Supreme Court had not barred lenders from doing so after August 31.

The proforma gross NPA ratio for the retail portfolio rose to 3.88% in December, as compared with 0.79% as of September 30, the bank’s investor presentation shows.

According to an analyst who spoke on conditions of anonymity, the weakness would largely be coming from the legacy book which the bank had inherited from Capital First Ltd, after the merger.

Vaidyanathan acknowledges the rise in stress but believes it is not out of line with the rest of the industry. A Macuarie report from December notes that the retail bad loan ratio for the banking industry stood at around 2% as of March 2020, which could rise to 4% this year.

“Our long term average rate for retail gross NPA has been around 2.27%. This would mean that the current NPA rate is about 161 basis points higher than our what we usually see. We feel this is okay, considering the scale of the pandemic,” Vaidyanathan said.

Further, IDFC First Bank’s total restructured loans stood at 0.8% of total assets or Rs 884 crore at the end of the third quarter. Considering the restructuring proposals which are pending execution, this amount could increase to 1.8-2% of total assets, or Rs 2,000-2,200 crore, the bank said in its investor presentation.

Looking at factors such as the collection rate of 98%, the vintage of these loans and the resolution rate of the bank, the elevated NPA rates would come down to the long term average in the next 2-3 quarters, Vaidyanathan said.

In the July-September quarter, the bank made Rs 1,400 crore in additional provisions to protect its balance sheet from the impact of Covid-19. Again in the December quarter, it set aside Rs 390 crore as additional provisions. Total provision coverage ratio for the bank stood at 75% at the end of the third quarter.

Despite the recent spike in bad loans, the IDFC First Bank stock has outperformed other mid-sized lenders since the start of this calendar year, largely owing to the strong financial performance displayed by the lender, said Mishra of Ashika Institutional Research.

The underwriting of loans at IDFC First is based on cash flow-based projections, rather than just the quality of the security, which is something other large retail lenders like HDFC Bank have used successfully, he said.

IDFC First, India’s Youngest Private Sector Bank, Makes A Dash For Growth With Fresh FundingIDFC First, India’s Youngest Private Sector Bank, Makes A Dash For Growth With Fresh Funding

IDFC First, India’s Youngest Private Sector Bank, Makes A Dash For Growth With Fresh Funding

With adequate funding, IDFC First will hope to clean-up the existing balancesheet and lend into India’s economic recovery.

According to Vaidyanathan, out of Rs 71 lakh crore worth commercial credit in India, Rs 52 lakh crore is to entities with ticket size of Rs 50 crore and more. “If ticket size is Rs 50 crore, these are obviously relatively larger corporates. The small borrowers have clearly not been financed, and that is an area the banking system must grow” he said.

6 Likes

Can you please throw light on how you came to valuation ratios for AMC Business? This sounds very interesting!!

1 Like

Very useful statistics. However, I feel the present high cost ratio presents a highly visible opportunity in the profit growth. Once the bank has stabilised the number of branches, number of employees and the desired casa level at 65%, then the cost control will follow through increased loan book and further reduction in savings a/c rate. In my estimate if there are no new big upheavals in the economy, the bank should arrive there by end of 22-23.

6 Likes

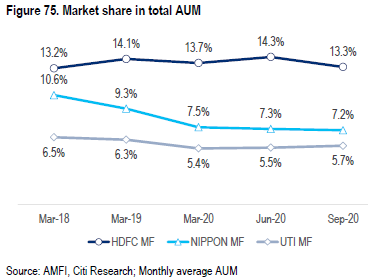

See below, both companies are losing market share yet trade at these valuations.

IDFC AMC has increased market share in the same period going from 60,000cr to 120,000cr and in the most recent quarter reported YOY AUM growth of 16% and PAT growth of 38%.

6 Likes

Assuming these 32,300cr bonds are refinanced at 6% rather than at their current rates adds 840cr to NIMs. If they are refinanced at 5% (asuming CASA rates are futrther reduced in the future) means incremental NIM’s of 1,160cr.

2 Likes

Very interesting presentation.

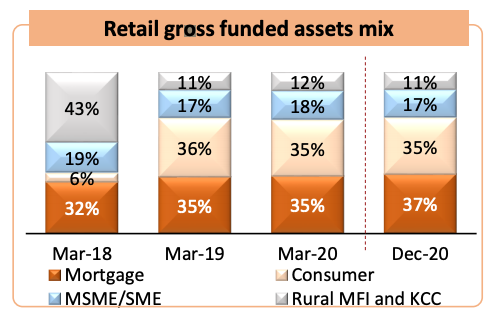

I feel like some problem is there in the way IDFC first bank is perceived. People think that their retail loan book is very risky. But IMO the transformation has been probably ignored by large parts of investor community:

look at how the ratio has changed from MSME+MFI (risky retail loans) being 62% of book in Mar-18 to being 28% now. Complete transformation of the risk profile. At same time yields have not really moved down a lot, definitely something worth investigating.

This presentation is a treasure trove of information.

This picture gives us a portal into what NIMs can look like in future. With latest cut in CASA rates, cost of borrowing can go down 1% with gross yield expanding 2% to 15% (when retail is 90% of the loan book after 3-4 years). That is how we would end up with a bank with 7-8% NIMs.

disc: invested, largest position, positively biased, this is not investment advice

15 Likes

I have some questions (can be very basic too) and would be really grateful if the people here can help me:

- I see that MFI and KSS lending as an overall lending component is coming down. Is it not mandatory for every bank to lend to the priority sectors? What is the % and how is IDFC keeping up with the requirement?

- Presentation suggests that Vodafone o/s loan is 32.4 bn INR of which 20bn is funded and the rest is non-funded. What is the difference between funded and nonfunded?

- Con someone please explain this table? Does this suggest the different maturities of different bonds?

3 Likes

Item 2: 2000crs is NCDs from Voda, of which 1500crs are due end of this year and 500crs due Jan 2022. The remaining 1200crs is a contingent liability tied to bank guarantee that IDFCB provided for spectrum. If Voda doesn’t pay the charges to Dept of Telecom, bank is on the hook as they provided the guarantee. That exposure is valid until 2025 per my understanding.

10 Likes

Why is the bank referring to two different provision coverage ratios for proforma NPAs? Is it 52% or 99%

?

2 Likes

Out of the 4.18% proforma NPAs, 2.04% is provided for. Apart from this, 2.14% is provided for the rest of the loan book (100-4.18%). This is standard asset provisioning.

So depending on how you look at it, the PCR is either 52% or 99%. I agree that communication could have been clearer. I think we discussed this earlier in the thread and @manikya_saiteja_gund had raised some points too, to clarify this.

6 Likes