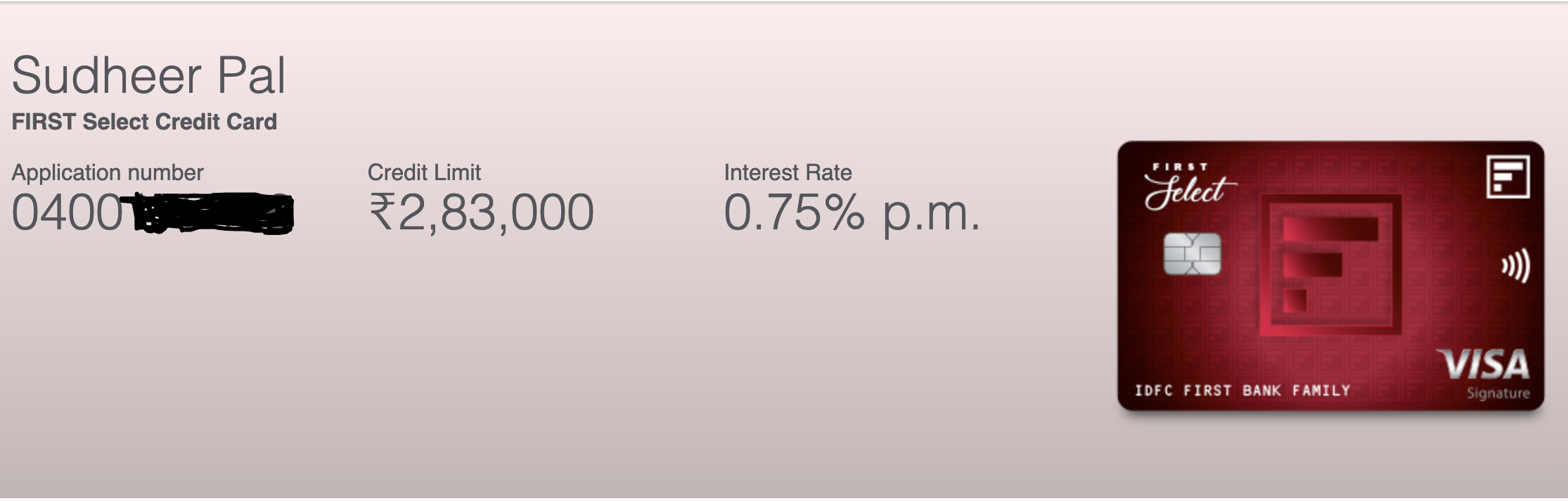

Hi All,

Just thought of sharing my experience of IDFC First Credit card application.

I got an invitation from IDFC FIRST via sms (I am already their saving account customer).

I checked the application form, its very minimal (2-3 step required).

First step - using mobile and otp verify your credential and most of the info they are fetching and filling application automatically. If you have already added your employer then you can skip one more step and next will be review step. It hardly takes 2 minutes to complete.

I intentionally dropped the form in between, just to check if I will get any follow back call from customer care. On next day got call from representatives and I was asking a bit noob question (like cash withdrawal, annual fees, any other charges) showing like i don’t know much about finance. I like the way representatives handled me and she confirmed within a week I will receive my card and its digitally active right away you submit the application.

They offered me first selected range of card and the limit they offered me is around 70-80% what other card have offered me (i already have sbi, icici-amazon, citi). So seems a bit conservative here.

Overall i liked the digital experience and seems very fast turn around. I am a IDFC share holder but this is not a biased review (sort of). Also attaching a screenshot showing the application.

IDFC First investment is candidate for long term, so even if existing these will be very minor hiccups , long term investors need not worry for such minor things.

I agree. IDFCF management is totally concentrated on the long term story. Next two quarters we should expect a couple of more steps for structural strengthening like capital infusion and reverse merger. Covid effect on NPAs in Q4 is an industry vide phenomenon and therefore central govt would see to it that lending ability of banks is not affected.

20,000 crores is a very small price amount to ensure that. In fact govt would gain far more in taxes through increased economic activity, triggered by enhanced bank credit.

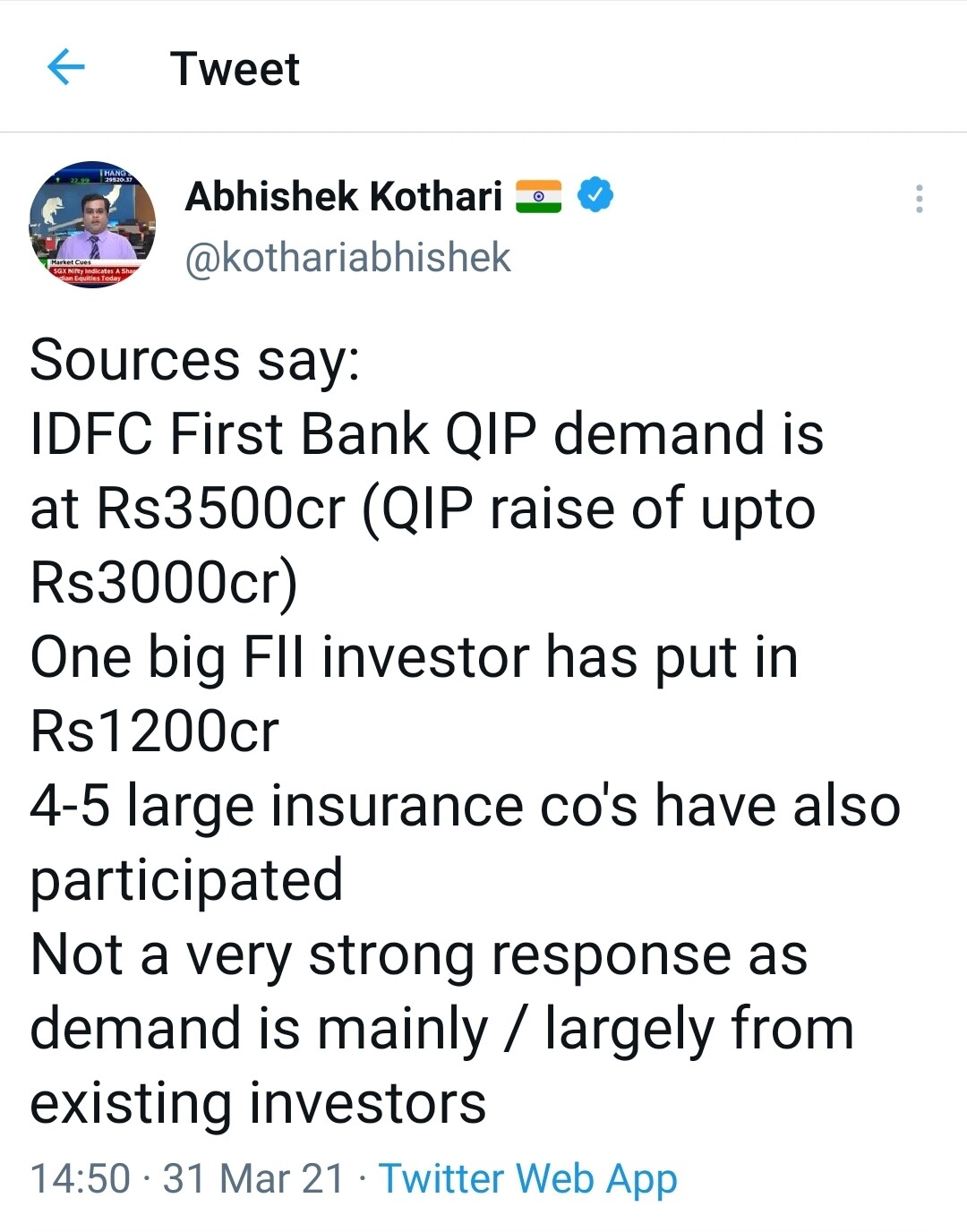

The QIP document is very informative and gives details that we always wanted in terms of break-up of yields, cost of funds, investments etc. A lot can be incorporated in our models using the data here:

I heard on CNBC that they have already been able to secure 3500 crores ( as against 3000 cr ) from one leading FII and a few Insurance companies . Has someone else too heard / read the same ?

Our Bank’s single largest borrower (fund and non-fund based) as at December 31, 2020 had a loan balance of ₹1,508.53 crore, representing 8.42% of our Bank’s total capital (comprising Tier I capital and Tier II capital).

Does this mean Vodafone account has been reduced?

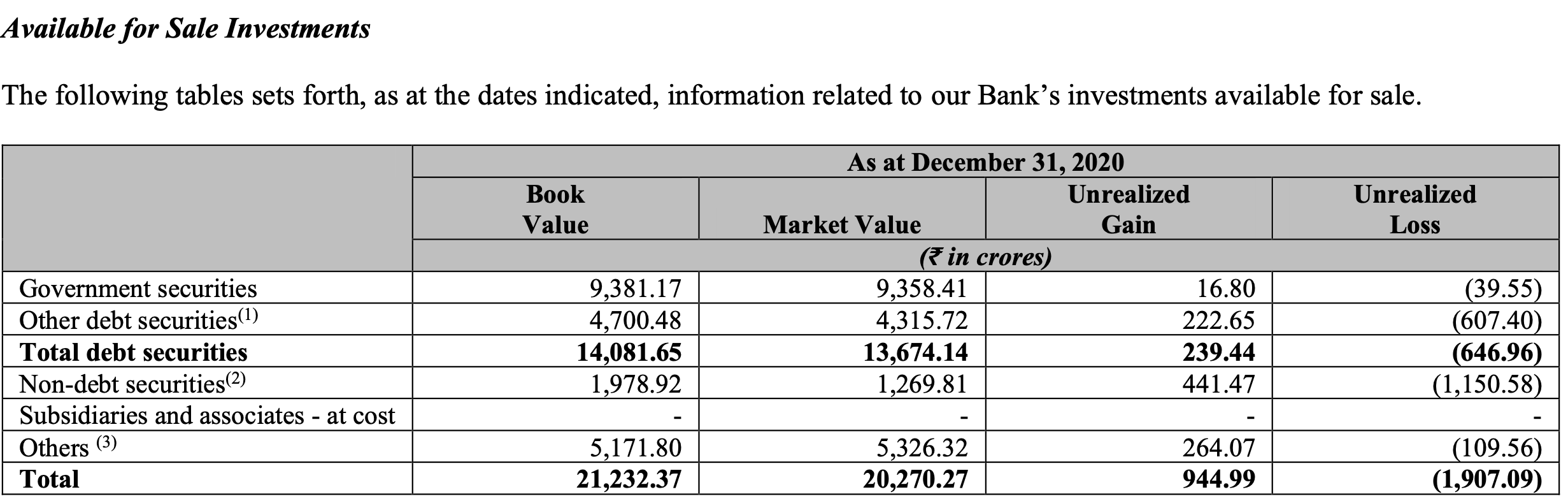

Bank has investments of 45,165.50 cr with yield of 6.92% and borrowings of 55,394.74 cr with yield of 7.29%. It seems they have been holding excess investments than regulatory requirements. (Page 41)

Corporate Bonds Portfolio has come down from 12,208.08 cr on March 31, 2018 to 4,700.48 cr on Dec 2020. But now concentration of BB & Below is high at 47%. (Page 46)

Large losses in Other debt securities and Non-debt securities of close to 1000 cr. (Page 46)

They own Vodafone bonds which is probably why they don’t show up as a large single borrower exposure. This is also why the BB and below book is high as these bonds are included in that category.

Could someone please help with some queries if they’ve previously tracked the reverse mergers of ICICI and ICICI Bank in 2001-02? Were the rules different back then? How was the bank allowed to retain the non banking financial activities in parallel to conducting banking activities? An interesting point being KV Kamath having overseen ICICI during that period who also happens to be VV’s mentor and Godfather in a way. @hitesh2710

If an IPO comes in market and its subscribed 2X then it means it was successful , however if its oversubscribed by 200X then it was still successful but response was overwhelming, so there is a difference.

Don’t worry too much for this thing as existing investors know the potential , Infy was undersubscribed when it came , so don’t worry too much as long as QIP was fully or a bit oversubscribed at decided prices.

Sets The Agenda For India Economic Conclave 2021")