School of Intrinsic Compounding made an analysis on IDFC First bank.

here is the link for who want to watch

School of Intrinsic Compounding made an analysis on IDFC First bank.

here is the link for who want to watch

One thing that is missed in the analysis is the fact that Capital first’s cost of liabilities is greater than IDFC first bank’s and the fact the bank has started reducing the rate of interest on the liabilities recently(similar strategy followed by Kotak). So ROE for IDFC first bank can be substantially more than Capital first. Would love to hear thoughts on this

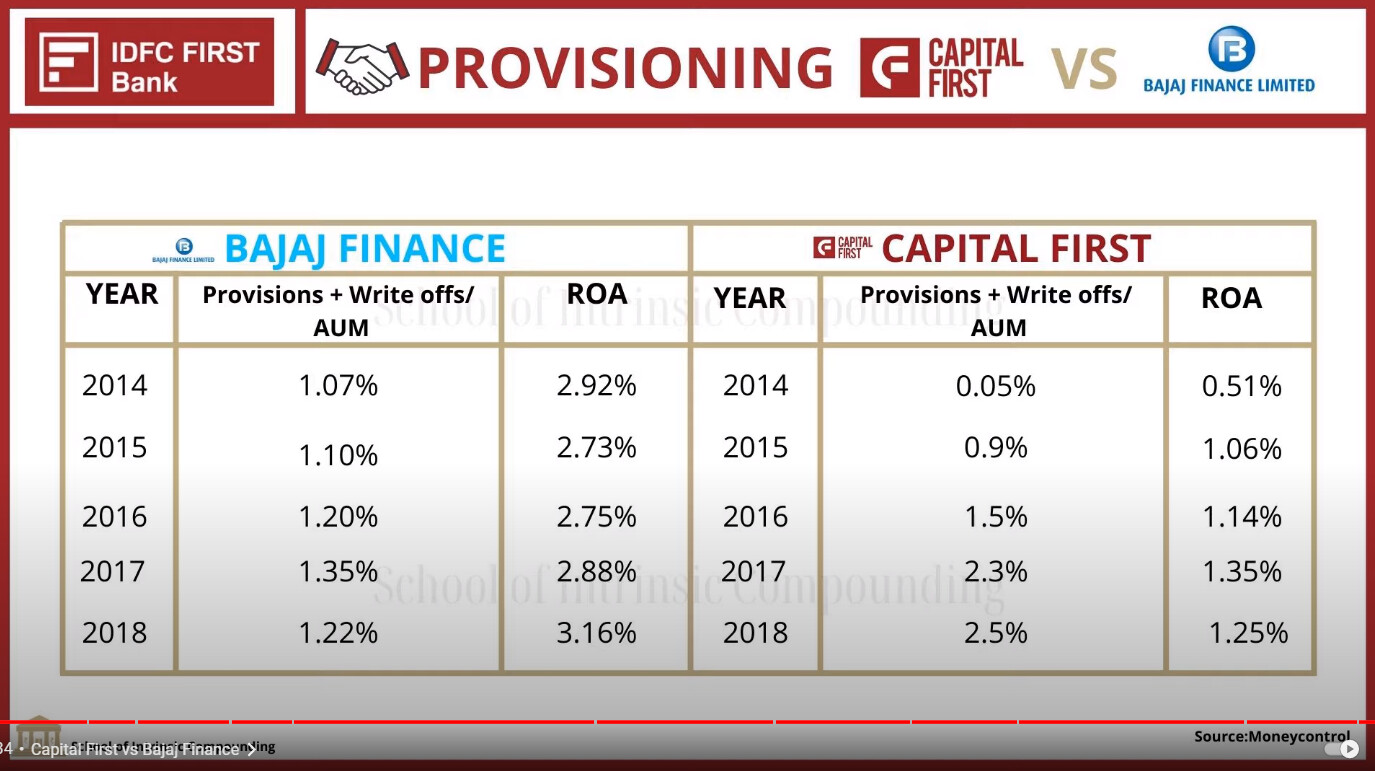

I cant understand his provisions+writeoff / AUM explaination. Isnt he doing double accounting?

Banks make provisions (which impacts the P/L statement) and in write off they remove previously provisioned loans from balance sheet.

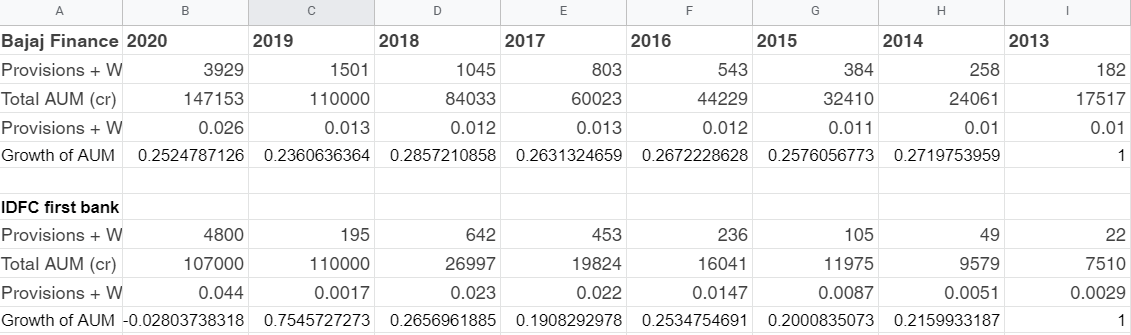

If thats the case why not bajaj finance is increasing

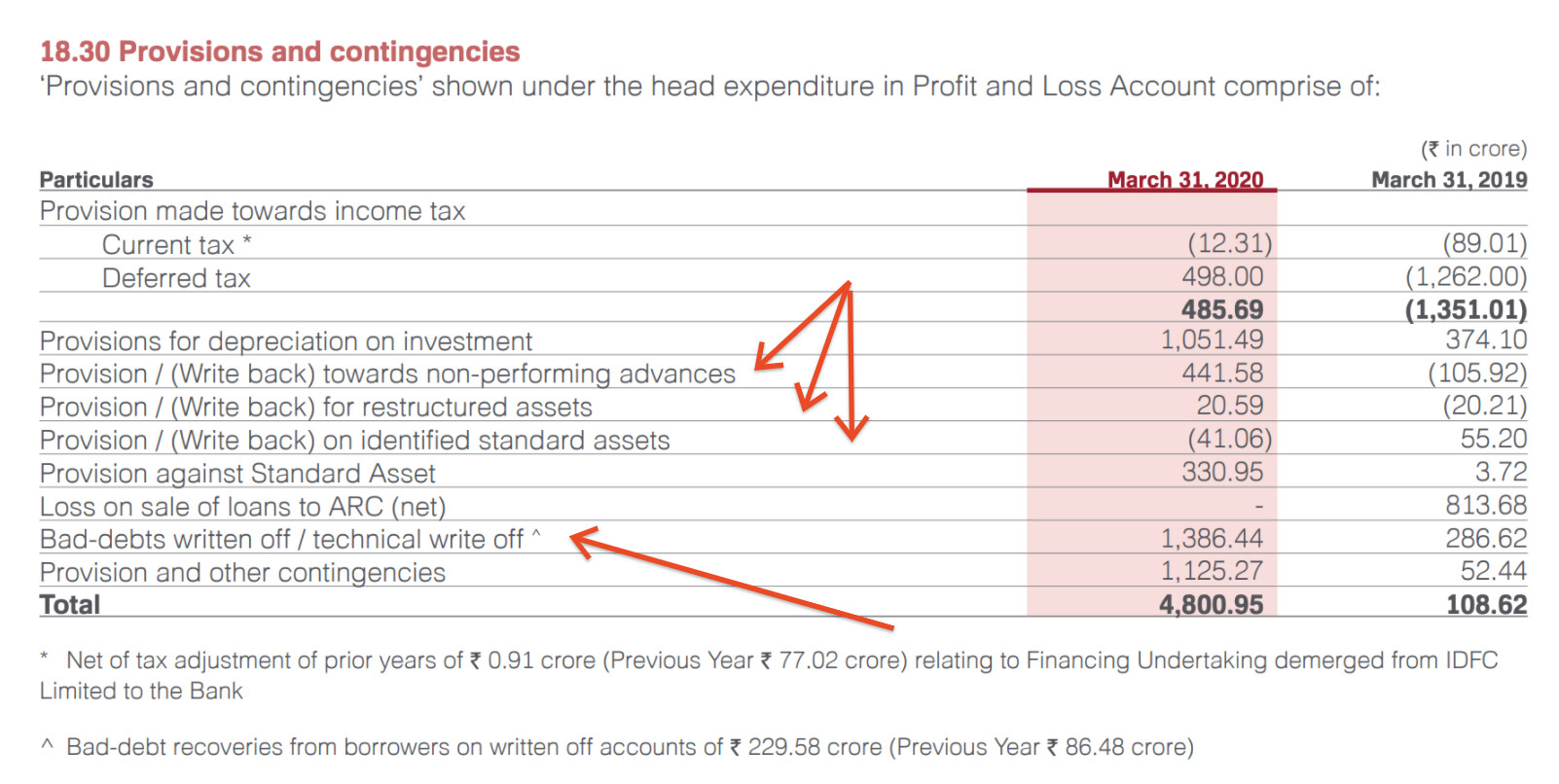

No. The writeoffs and provisionsare just two headers under which banks generally break up their “Provisions and contingencies” sub-header under the expenses header. See the screenshot below:

Why the bajaj finance numbers are not increasing - well they are. It all depends on what data we chose to present. Everyone choses data that suits the narrative they are building (I’m guilty of this too ![]() ).

).

Btw I had already covered this data on the forum: please see this :

Disc: invested.

Lending is a business of risk management.

1.Whenever a loan is made to anyone, it is expected that some percentage of the loan is already lost while booking and provided as provision. This is called standard asset provisioning. Usually this number is 0.4% at max and depends on the product.

Eg: it 10% of the portfolio is in 30+ bucket… final loss can be some 3% so, this is anticipated and provided for usually in the provisions based on product ( remember until 90+ portfolio is usually not counted in NPA nimbers)

EL= Probability of default × Loss given default × Exposure at default. ( This varies across products, companies depending on the underwriting models).

Since ECL is expected loss, it usually marked based on the company history of underwriting and book quality.

There are also regulator defined standard numbers incase companies decide to go with maximum safeguard provisioning.

There are also stress scenarios where you have cases like 1 in 10 , 1 in 50 , 1 in 100 type scenarios where number usually jump for what is usually expected. Some managements anticipate this stress based on market conditions and provide more for anticipated losses even before portfolio becoming NPA.

So, all in all… in some cases total provisioning can be higher than GNPA.

Also, some companies have better recoveries and they improve over time, this will reduce the net provisioning numbers despite stress( due to write backs). So, if should be considered too.

Write off is for removing the numbers out of balance sheet, that said write-offs can be written back if recoveries are made.

9… provisioning is more of having some % on balance sheet and taking the number through P&L.

You’ll have more details in BASEL 3 guidelines if one is interested to dig deep.

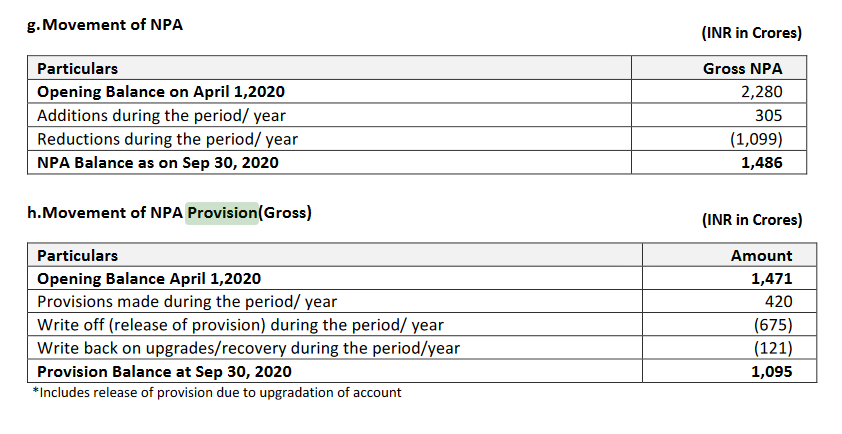

@manikya_saiteja_gund ya you are absolutely right. Even IDFC bank which claims to disclose everthing. I was just looking at GNPA and NNPA are falling down in recent quarters. But they are not disclosing how much they are writing off and recoveries they make (akin to CSB).

We need to ask mangement regarding this.

@sahil_vi provision + write off / AUM. I think AUM growth maybe a confounding factor in comparing capital first and bajaj finance. When there was dip in growth rate of capital first in 2017, provison+writeoff/AUM spiked off. Bajaj finance on other hand growing at much greater rate compared to capital first able to cover it off I think

Write-offs and Provisions have to be disclosed under Pillar 3 of Basel Norms.

This was for the last quarter

This is the link.

You can research for even earlier quarters. The disclosure is compulsory, and not bank specific

This is surprising. Distinctly remember he said the rates wouldn’t come down so soon.

Interesting set of results-

Stress on the balance quite visible now. GNPAs of almost 4%. A bit surprised by the management’s aggressive guidance that it will come down to long term averages over the next few quarters.

Even they can’t be sure of this. Let’s see how this pans out. Hoping that there isn’t any other downside surprise waiting next year.

Also Vodafone seems to be in a fix now and so maybe the 25% coverage to that exposure will turn to be too less over the next year. This might turn out alright if they are somehow able to raise equity.

Huge jump in QoQ costs- hoping that this is mainly into technological investments. No way to know about this without conference calls though.

Cost to income is not rationalizing yet as I had hoped.

Great news on the liability front though. Hoping by end of this year Savings rates are reduced too.

Indirectly Invested.

Two takeaways.

It is going to be high risk high reward game.

I think the 4% GNPA number needs to be put in context as when we see it on a QoQ basis it looks like a big jump but because of the moritoroum we aren’t really getting a clear picture. The last normal quarter pre covid was probably Dec 2019 and then the GNPA was around 2.9%, so a jump of around 100-120bps.

What sort of pro forma GNPA numbers are competitors reporting (ignoring SC order), these are just off the top of my head and please correct or add if any are incorrect -

Kotak - 3.5%

ICICI - 5%+

Axis - 4.5%+

Bandhan - 7%+

Bajaj - 4%+ if we include GNPA + 1.6%Write-off

So compared to competitors IDFC isn’t much higher. The commentary given by most of these banks is similar to IDFC, so the management is not being very aggressive when they say that these numbers should normalise going forward.

One last point is that management has excluded all interest income from these pro forma accounts which has not been done by most other competitors and is quite conservative.

I dont think that this interpretation is correct.

For the currently declared proforma GNPA, they have provisioned 99%.

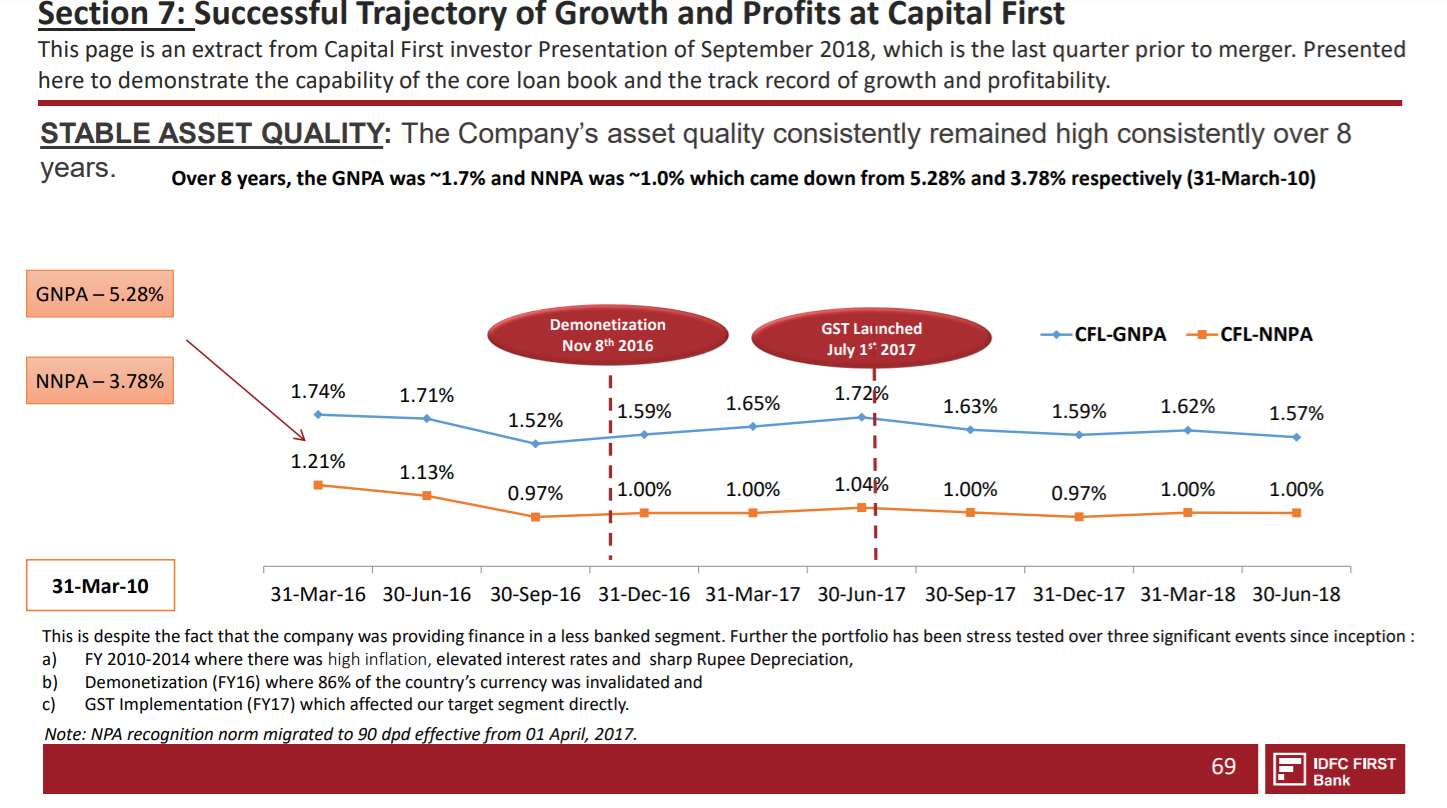

I put this together quickly, but frankly i think IDFCF’s credit culture is quite good:

| Company/Metrics | AUM (in cr) | Pro forma GNPA | Provision Coverage (proforma NNPA) |

|---|---|---|---|

| IDFC First Bank | 110000 | 4.18% | 99% |

| Kotak Mahindra Bank | 214000 | 3.27% | 85% |

| HDFC Bank | 1600000 | 1.38% | 148% |

| Bajaj Finance | 143000 | 2.86% | 46% |

| Bandhan Bank | 80000 | 7.12% | 54% |

| Indusind Bank | 207000 | 2.93% | 77% |

Btw, all institutions have their own terminology so getting this canonicalized data is a bit difficult. any mistakes are completely unintentional. If you believe any numbers are incorrect do let me know.

ICICI bank and Axis bank are at 5.5% and 4.5% as well.

For me the key open question on Asset quality is:

Does the 4% proforma GNPA include the ~2% of projected restructuring book or is the 2% restructuring in addition?

They have actually made some very conservative accounting which is clear when one looks at their investor presentation in detail:

Eg:

“NII for the current quarter includes the impact of provision for interest reversal for proforma NPA cases.” This is some very subtle conservative accounting.

For me the key takeaway was that the bank’s tenacious provision creation has proven how conservative they are when it comes to asset quality recognition. The SA rate reduction is a step in right direction. As long as they are above big banks, they will easily retain and grow their CASA+TD. The opex is not slowing down, but we knew that from the pace of branch opening. At the same time, the opex/operating income is actually showing signs of rationalizing. CII ratio is at 65% for the 9MFY21 period.

Key monitorable for me remains the Retail segment RoAs and the Opex growth slowing down. With the CRAR ratio around 14%, I do expect some more capital raising in next 6-12 months.

Link to the Investor presentation which is a must read:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/5da542e5-7f8c-4581-9b8b-64251ffcbc4a.pdf

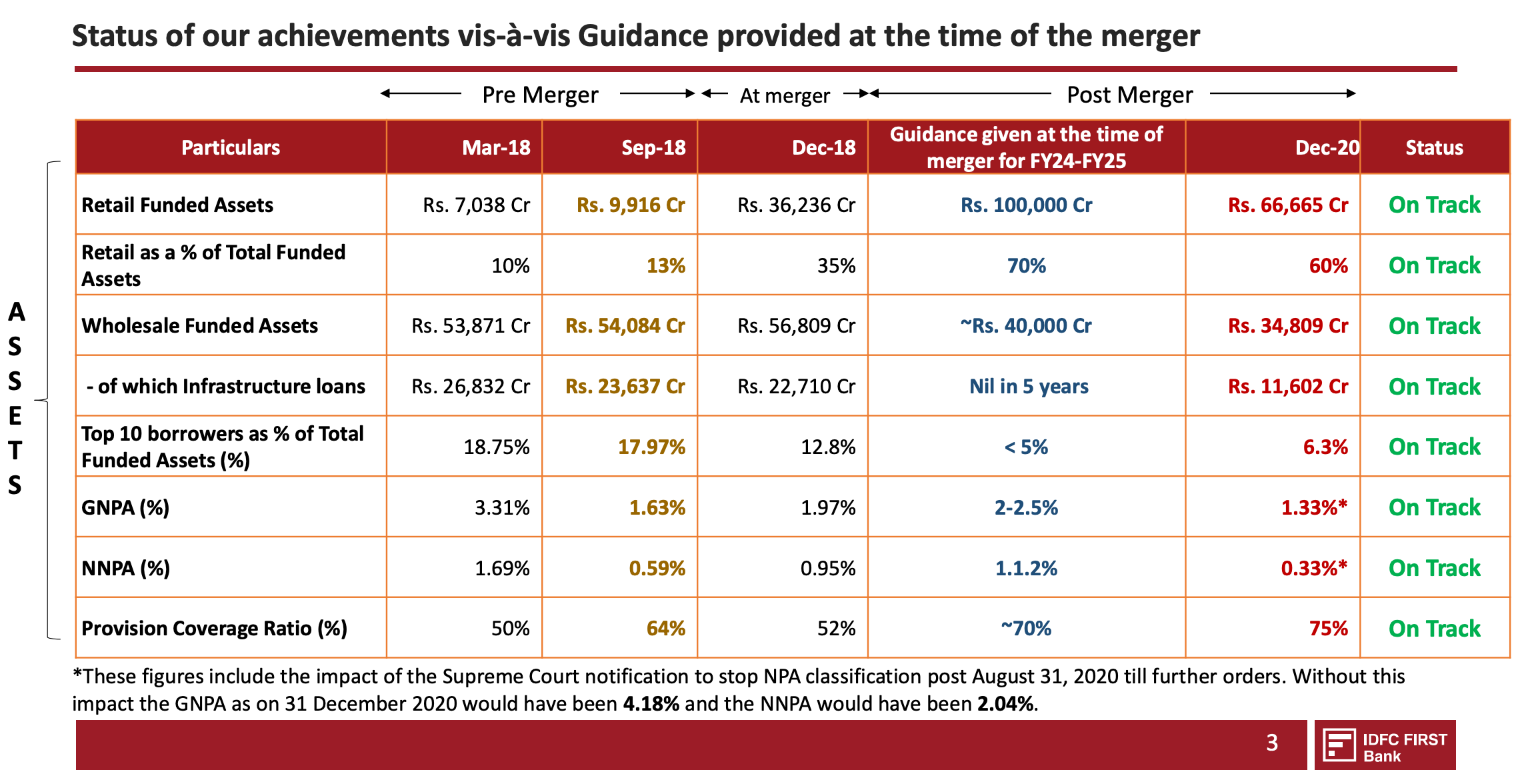

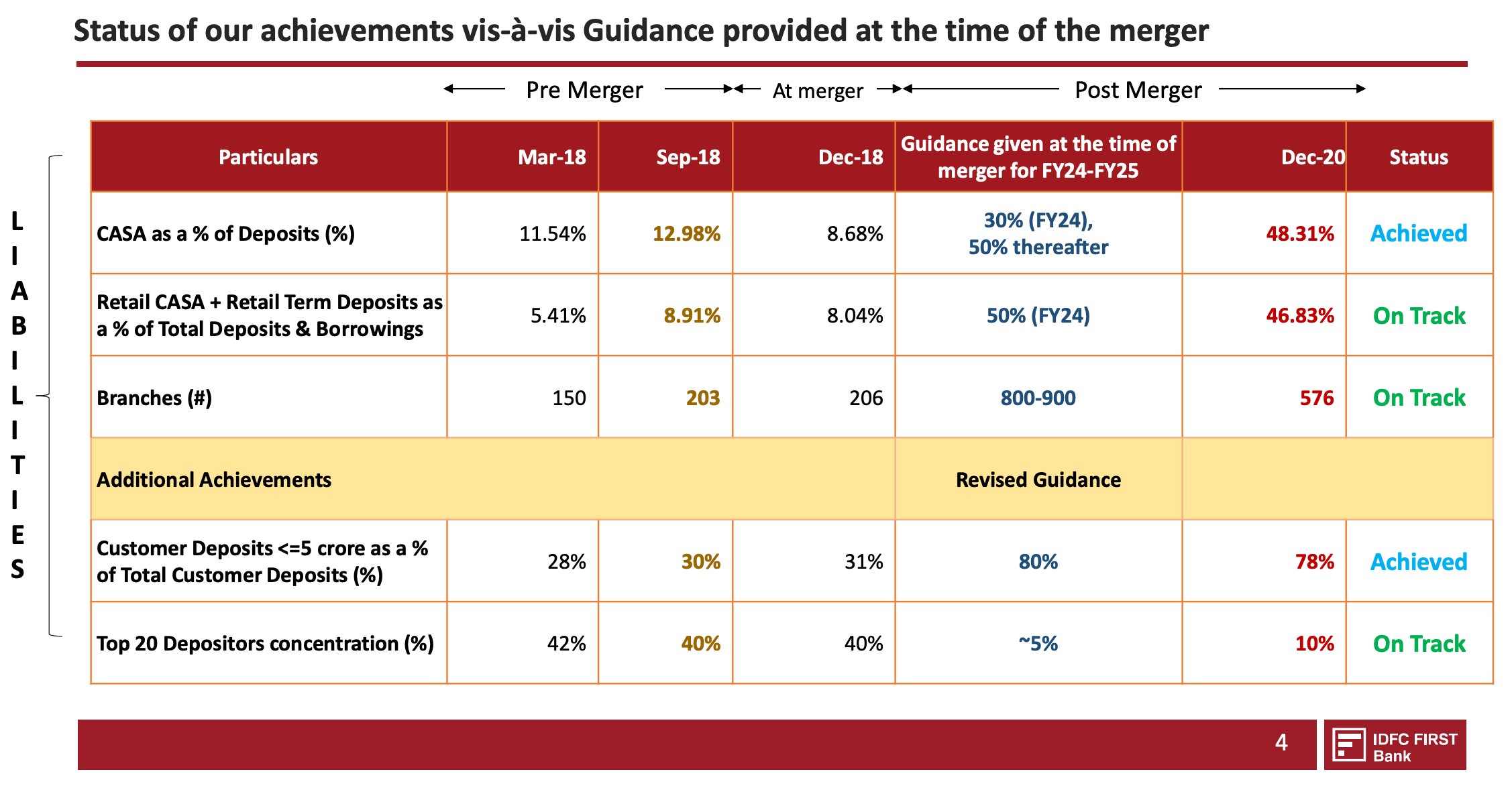

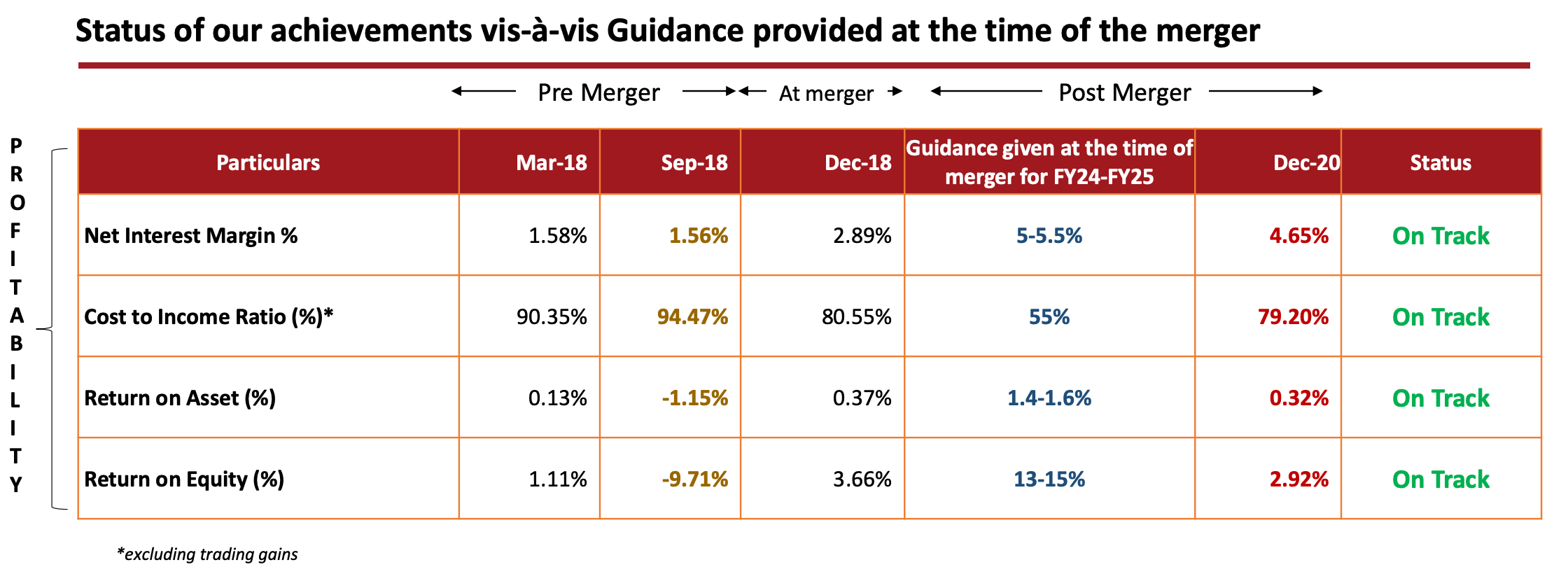

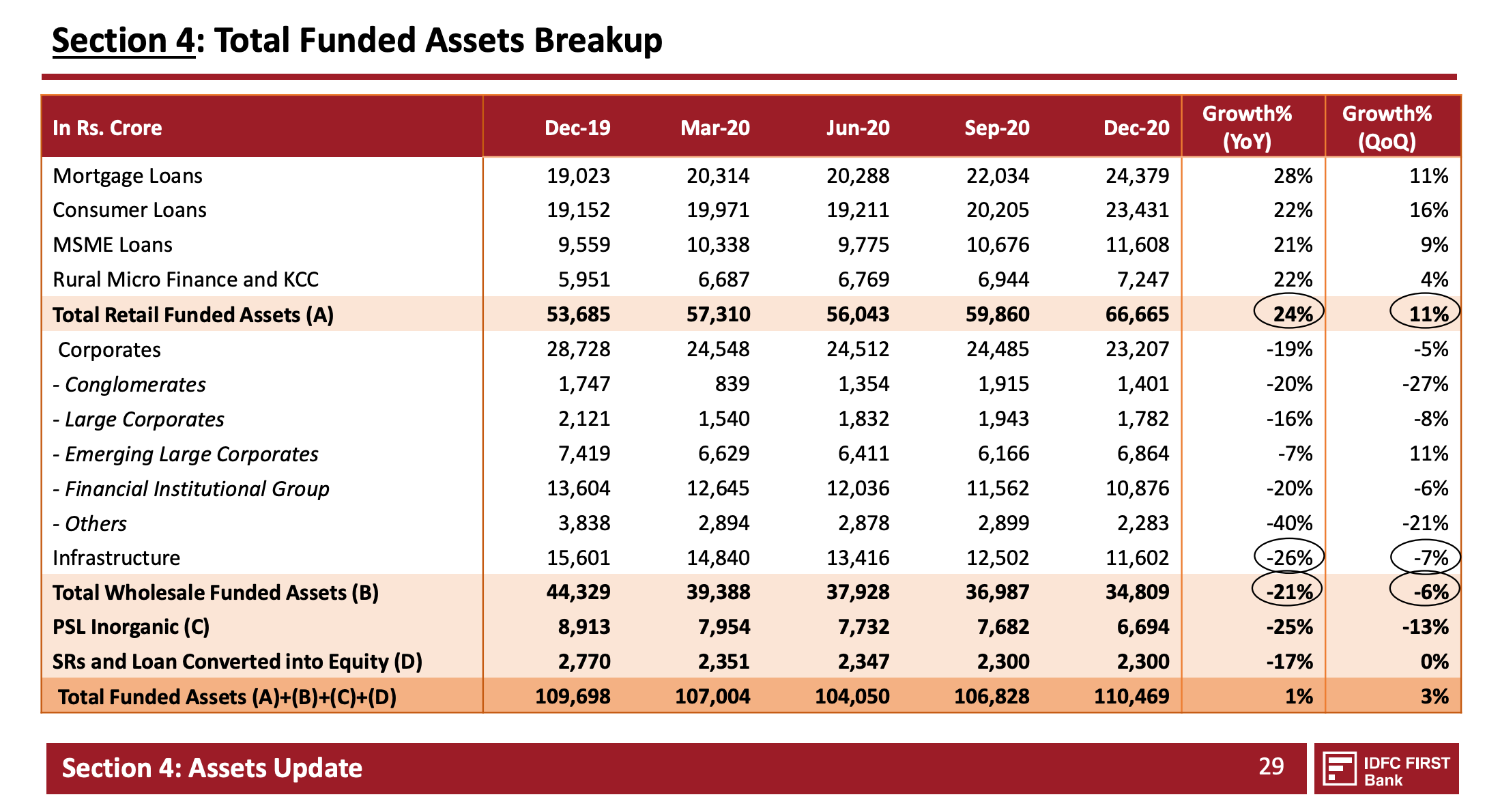

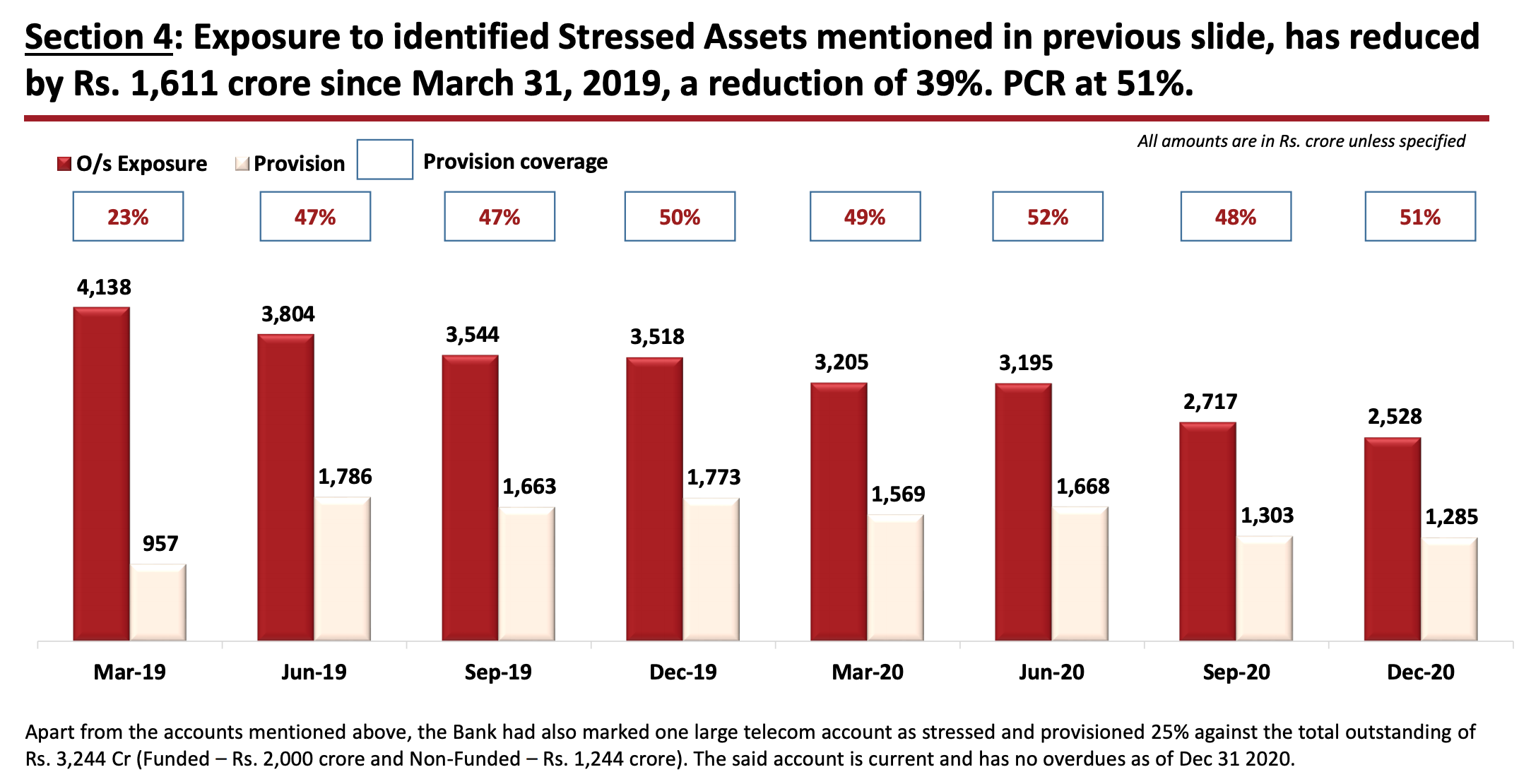

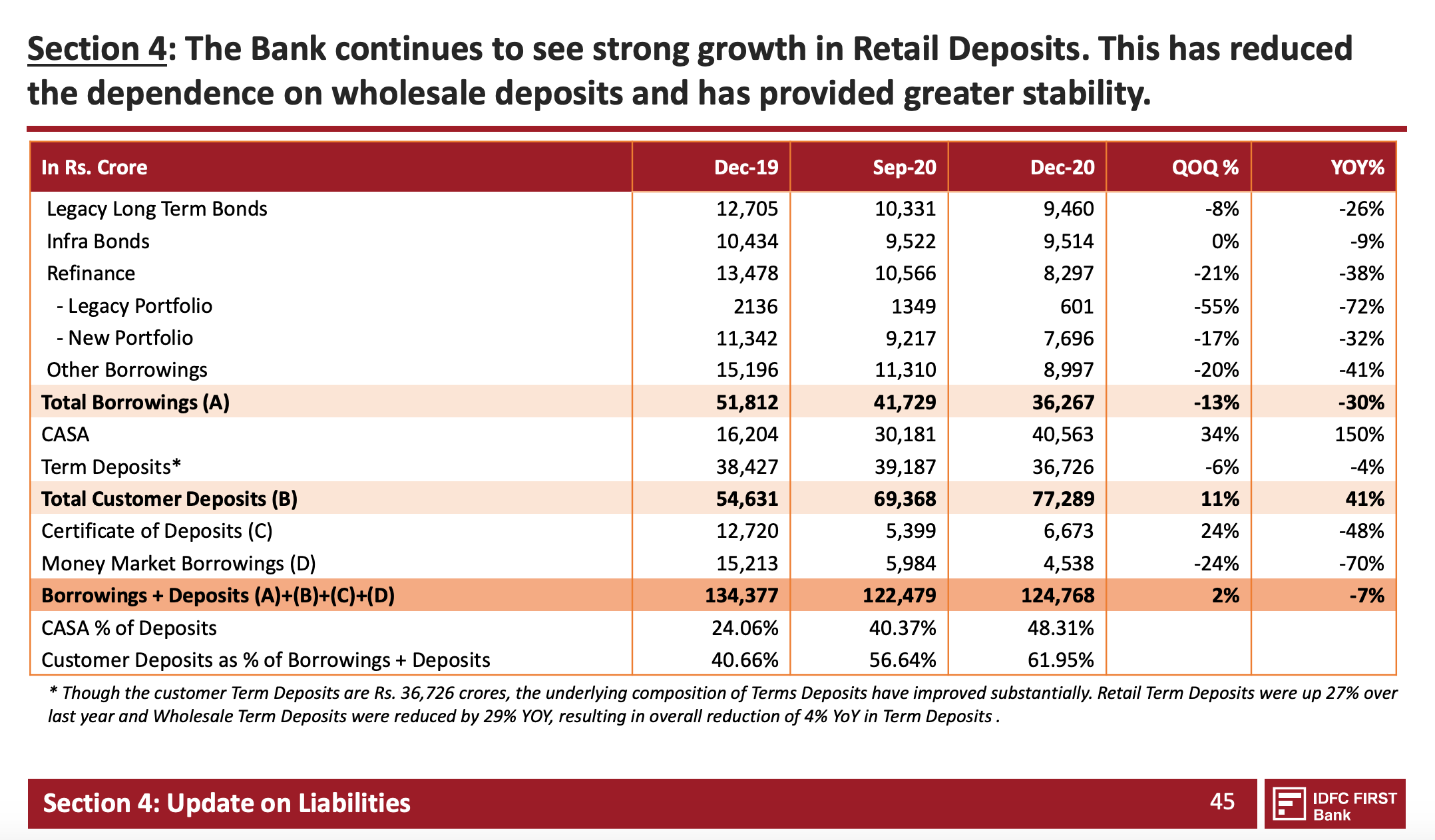

Some key slides IMO:

Disc:invested.

I could be wrong but it is likely from increased disbursals, Fee and other income doubled QoQ so a big chunk of that likely went to DSA’s as commission and payments on the referral app. Unless they entered into some new contract with a tech vendor the increase did not come from software related expenses, tech is supposed to reduce costs. And credit card system has been in the works for a long time now so likely not that either. As to branches, 5 years target is 800-900 (guidance was to add 600-700 new branches over 206) so we will likely see high opex for 6-8 quarters. Job openings a few weeks ago were ~400, now at ~600.

Another sign of conservative approach is the focus on home loans which has traditionally been a low risk segment for banks. Notice the highest YoY increase. Consumer loans also saw a big jump this quarter indicating improving job prospects as economy gets back on track.

Analysis by CA Ravinder Vats

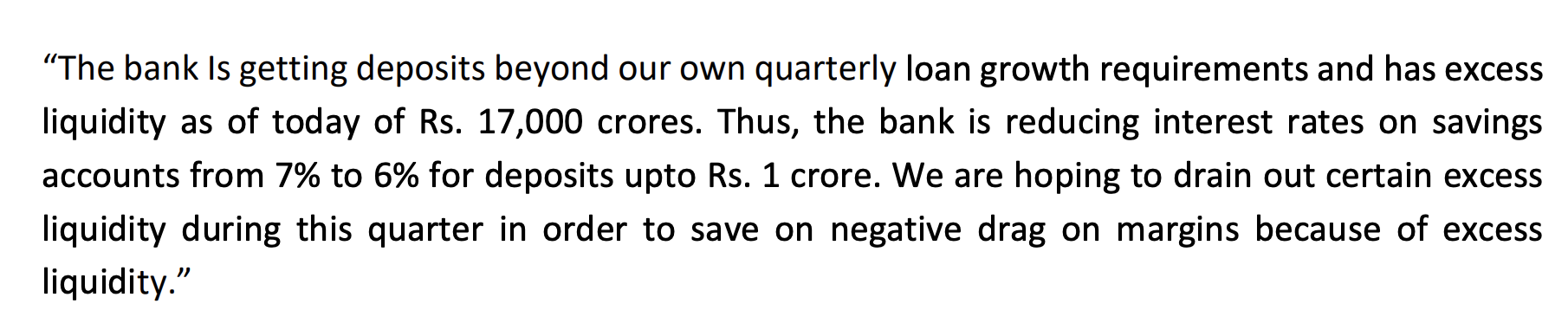

The bank Is getting deposits beyond our own quarterly loan growth requirements and has excess liquidity as of today of Rs. 17,000 crores. Thus, the bank is reducing interest rates on savings accounts from 7% to 6% for deposits upto Rs. 1 crore. We are hoping to drain out certain excess liquidity during this quarter in order to save on negative drag on margins because of excess liquidity.

Could the highlighted part be interpreted as not aggresively pursuing CASA accounts for a while? If so that’s kind of disappointing because new accounts is always good for the future.

IMO, yes but it is a good thing. The excess liquidity serves as a bane rather than a boon due to excessive interest outgo. For 1% reduction on CASA+TD increases profits by 600cr. This is almost 150% of current profits. It would be interesting to see how CASA moves in next quarter. I would expect the growth to moderate, which is a good thing because the loan book cannot grow as fast as the CASA is growing right now, and I think they have largely replaced most of the older higher interest borrowings.

Even after the reduced rate, IDFCF still has fairly high interest rates. I think I have seen IDFCF Ads in many places both in Physical world and digitally. Attracting CASA is a combination of interest and also ads. With all major banks giving 3.5-4% SA interest, I personally dont think CASA growth would slow down a lot. Maybe a little bit, but a prudent institution always drives a good balance between growth and profitability.

Yeah I guess the bank doesn’t need to actively pursue CASA anymore. All the marketing stuff is out there and then there’s referral in the netbanking app itself. It should sustain on it’s own from now.

Funny how the CASA narrative went from “hard to raise” to “we have too much” in just 2 years  The bank has made good use of market forces.

The bank has made good use of market forces.

Gross NPA including moratorium reached more than 4% with 80% growth is highest concern…

Now they have to raise capital from equity for further growth. It is already having high equity base and there will be further dilution.

Operating expense is another concern. It would be better if they had slow down expansion in last two quarters to give comfort to balance sheet.