I went through more than 20 job postings on the career website. After reading job descriptions it’s not surprising at all what they have achieved so far.

There is emphasis on the following in almost every job post in retail segment:

Meet or exceed bank’s high growth targets (on both CASA and loan growth, depending on the job)

Evaluate risk and control delinquencies

Recommend process improvements (this is regardless of the job level)

Collaborate with other departments to improve things

While the high emphasis on growth makes me a bit nervous, they’re building a risk averse culture from the bottom up.

Job postings for credit card sales manager have only been up in the last few days so I guess they’re gearing up for launch on Republic day, should provide marketing boost.

First of all, I don’t know about the expenses of maintaining ATMs and I don’t know if banks generate revenue by maintaining ATMs. What I think is that if the expenses are more than the revenue, they would not do it. Rural people usually come to their nearby towns and cities almost on a daily basis and those who know how to withdraw use the ATMs in towns and cities. So what is the purpose of opening up ATMs when most people in rural areas don’t use them? SBI being SBI obviously, may have had the advantage of opening up ATMs years ago. And being a PSU bank, it does not mind running those ATMs even at loss. They may even have an obligation to do so. But banks should make their presence felt, hence the ATMs, although less in number. If HDFC Bank has 8% rural ATMs, there is no surprise IDFC Bank has 1%.

CASA growth comparison with other banks who also made the same disclosures to SEBI. Could not find Kotak and ICICI disclosures. All are YoY and QoQ numbers except Yes bank, they declared 9M numbers for some reason.

Since everyone is being quiet positive about the company, I would like to bring up a point of caution.

While CASA ratio for the bank is going up at a fast pace, it may not be right to compare it with the likes of HDFC and Kotak, since they are doing it at a much lower RoI (3-3.5%) than IDFC (7%).

In fact, I would like to say here that Corona came as a blessing in disguise for IDFC as they got more CASA accounts than normal without increasing interest rates. While it is good for company, I don’t think we should give all the credit to management for that. In fact, if we see other private banks too, most of them have been able to grow CASA over last 3 quarters at a higher pace than before.

Interesting part would be to see the impact of lower interest rates on the Asset side. Although I believe that IDFC’s focus on unbanked part of society would help it maintain the current Interest rates leading to better NIMs.

Having said that, nothing can be taken away from the management in terms of its prudence to manage its balance sheet in the right direction at the right time. Great companies turn crisis into opportunity and it seems IDFC is on its way of doing the same.

Disclosure: invested, tracking on quarterly basis to increase exposure

In the context of the press release, they are talking about average of casa over entire quarter vs casa ratio as of December 31.

In essence on sep 30 only 40% of total deposits were casa. Average over Q3 is 44% and as on Dec 31, 48% of total deposits were backed by casa.

I believe management deserves at least some of the credit, as I mentioned before the crisis is certainly a tailwind for the banks. And also quantitative easing, which has greatly increased liquidity in the system.

From my old post:

In September it was 99657, highest ever jump in a month. I would not be surprised if we see CASA increase by more than 10000Cr in Q3, but since the quarter is loaded with festivals it could be lower as people spend more.

I believe the jump in September was due to the IPL marketing with Harsha Bhogle, and also due to high targets set by the bank internally. They have been pursuing CASA growth aggressively and what we see now is a result of that.

By the way the increase in debit card count in October was ~70000, while not as high as before, it is still the second highest so far. And credit card count reached 20K so I think it covers most employees now.

I agree CASA at this point in time doesn’t mean much as the interest cost is high but I think the bank still has other corporate borrowings that cost more than 7%, so any increase in CASA is still positive even at 7%.

NOTE: I don’t want this post to be received too optimistically, just thought the management deserves credit where its due. And my post wasn’t intended to compare specifically with HDFC, I just looked at all available reports I could find.

Yes I am quite invested in this stock but the lack of criticism from people about this story is signalling a sort of bubble stage in the markets where only positives are being looked at.

Plus a sort of hero worship of Mr Vaidyanathan.

Good thing it is reasonably priced though.

Waiting for the cost to income trajectory to come out.

CASA will come if you give 7% assured interest in such times. All due respect to management.

IDFC FB is definitely able to increase SA deposits at a very high rate with 7% rate which is higher than even their TD rates. Hence growth rate of SA deposit is much higher than TD deposit growth rate.

Bank is still evolving and going to need to normalize SA interest rates to eventually attract enough retail depositors with average SA balance of 1-3 lakh range with rising share of TD and CA deposits in total customer deposits.

I am happy to see bank disclosing average vs. end of quarter SA ratios. ICICI bank was egregious in manipulating quarter end SA numbers by trying to get more deposits among all the private banks.

Also good to see disclosure about top 20 depositor share in total deposits.

Building a new bank is always going to be challenging. It is even more challenging than banks started 1990s and 2000s as PSB were still pretty large to poach market share from. Newer entrants in the banking now have to compete with bigger and agile PVB, NBFC, payment, small banks and FinTech firms. IDFC FB is going to play out over period of 3-5 years.

I think it will test patience with dives in the share price bringing sharp contraction in the P/B ratio but it will eventually rise to 2.5 with ROE > 12%.

Many years from now, in the worst case the bank will turn out to be another ICICI. Another Yes bank? Not impossible but highly unlikely. This is how Yes bank’s retail segment has performed (after RBI forced them to disclose more but before moratorium):

In the best case? Can’t really say because a lot what IDFCFB does is experiment, in both existing markets and new markets they create. A lot depends on execution so important to track what they do and how they do it.

In my view, most stocks have an investment thesis (positives), and key monitorables (in some sense negatives). The key monitorables can result in investment thesis getting derailed. Sharing a quick summary of my key monitorables (negatives):

Despite improving CASA, growing retail loan book, the retail Segment RoA is still negative. I’ve added detailed thoughts here.

My own estimate is that this is largely due to very high up front OpEx. The very high OpEx can definitely appear to be a ‘negative’ to many people (see here). I have analyzed the high OpEx here and growth of OpEx vis-a-vis the loan book growth remains a key monitorable/risk (specially depending on investment horizon).

This risk is still there (since MSME can restructure the loans until March 2021). But seems to be reduced since CEO revealed in recent interview that only 0.6% of book has applied for restructuring. They expect in the worst case, 2% of book to apply for restructuring. They have already created ~2.5% of book as covid related provisions. So I think they are adequately covered here.

4. Very high growth has been called out as a possible risk. This is very much possible. We have to understand the pricing of the product. For some price, the provisions+Write-offs are completely supported by the NIMs. Some scuttlebutt would go a great way in understanding how these products are priced vis-a-vis other MFI/MSME lenders to get a sense for whether the risk is adequately priced into the product.

Among things that I do not consider to be negatives which have been talked about recently:

A lot has been written about the CASA and how 7% is too high. I would request members to see the latest interview posted yesterday here. A few things become clear looking at the interview: VV acknowledges that maintaining the 7% is not easy in a falling interest rate environment. For this reason he talks about the specific things bank has been doing: earlier one got 7% until 10cr SA, now it has been reduced to 1 cr. It would not be unimaginable to think this limit could further fall to 10L in the future. I think bank has been very prudent in how they handle this. One thing I’d love to see is the CA vs SA breakup since CA has 0% interest and the growth there is not due to the 7% interest rate. Roughly 55 out of 369 open jobs on their website are related to Current Account holders. The other thing to keep in mind WRT CASA is two fold: the 7% is still a win for the bank because they have been borrowing at 8.5-9% in pre-merger days. CASA ratio is at 48%. CASA+TD is at 75% so there is still room for it to grow and substitute the money market and other wholesale borrowing.

The narrative that CASA is only growing due to 7% interest and TD is not growing enough is not backed by data and is hence false. Here is the data from this Quarter’s filing and previous Quarter results:

Q2

Q3

QoQ Growth (%)

Retail CASA (cr)

30181

34470.894

14.21

Retail TD (cr)

19763.96

23,964

21.25

Retail CASA+TD (cr)

49944.96

58,435

16.99

Total Deposits (cr)

69368

77,289

11.41

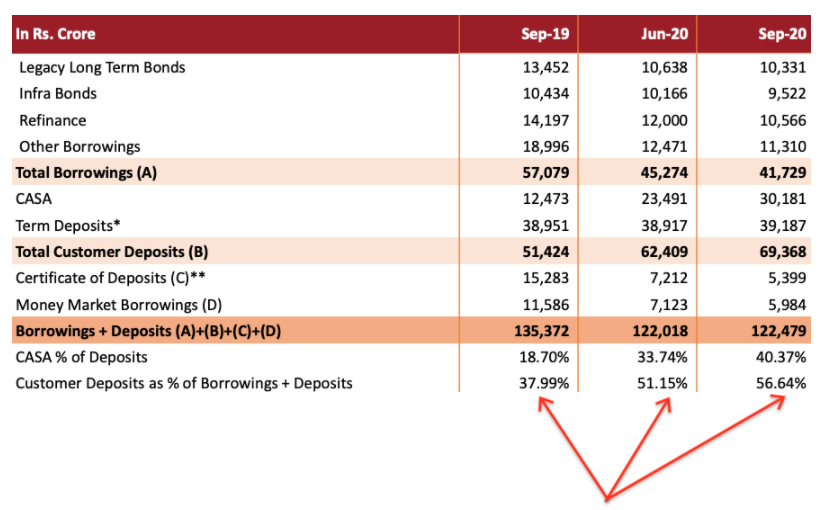

On a side note, one key ratio which i think investors/analysts should monitor but possibly don’t is Total Deposits/(Total Borrowings+Deposits). Here is the ratio from last quarterly report:

Assuming total borrowing to be 1.25 Lakh cr (to maintain same level of liquidity), this ratio might be around 61% (=77/125). We’ll get to know once quarterly results come.

I know many think people are only talking positive things about the bank . But please see the kind of coverage the bank had for the past 1.5 years., the interviews, reports etc everything was outright negative. Credit to the management without a doubt for handling the pressure of six straight quarters of losses. Not an easy job.

They had raisee 2000cr at such low rates with safety & liquidity concerns in mind. That shows Management’s mindset. With regards to getting the CASA ratio up(as guided) so fast. It is not just the high percentage that does the trick. There are so many banks offering 7%, but the hard work put in by the bank’s managment is awesome (systems, customer service etc), hence they grew faster than peer banks offering similar rates.

A small anecdotal evidence which might be relevant here.

Please see this link of Vaidyanatha’s interview in 2008.

Just quoting from the article:

An ex-Citibanker,

40-year-old Vaidyanathan joined the bank in 2000 as the managing

director of ICICI’s consumer finance arm, ICICI Personal Financial

Services.

“I have been in consumer banking since the beginning and we have

come a long way. We had about 50 to 60 employees when I started and

we are now 26,000-strong,” he said. His division now has over 25

million customers, $35 billion in consumer customer assets and over

1,000 branches with a presence in the deepest parts of India. The consumer banking division contributes about 50 percent of the bank’s revenues.

“Consumer banking is important but it’s not just the numbers. What it has done to the bank is to make it very resilient because consumer banking business behaviour is very stable – it doesn’t fluctuate. It doesn’t swing either way dramatically in terms of profits or book size. This lends a lot of predictability to the whole business,” he qualified.

Please go through the article. I would say the idea he has for a bank is what he is implementing now at IDFC First. There is no change in the thought process for more than a decade now.

I think the CASA number for Q3 you have mentioned grossly understates the CASA ratio of 48.4%. My understanding is that CASA would have closed somewhere near 37-38000 crs for a CASA ratio of 48.4%. Please check. Retail TDs must have grown at a much slower pace because of the high rate on SA.

I opened account in IDFC First on November 2020 online , within minutes able to see data on mobile app, and further KYC completed within week by collecting documents from home. 7 percent is almost double than HDFC & ICICI where i used to keep my balance. I was sharing same with my friend few days back and he also opened his wife account in IDFC First ,reason 7 percent interest .

From bank’s perspective TD deposits are preferred and hence are offered higher interest rate than SA deposits. IDFC FB is unique where SA deposits rates were higher than TD deposits rates and hence almost no incentives for customer to keep TD with bank except to lock in the interest rate. Especially given marketing campaign by bank, SA deposit would make more sense than TD of less than 1 year timeframe or above/below certain thresholds amount thresholds. This explains lower absolute number for TD deposits vs CASA deposits.

I felt IDFC FB is offering higher interest rate for SA deposits than TD deposits due to shareholder/media pressure to build CASA franchise. May be it is a genuine business tactic for faster customer acquisitions as customers are likely to move SA balances faster than TD balances from different banks.

Now current strategy of limiting promotional 7% interest rates to 10 cr in Sept 2020 and to 1 cr in Jan 2021 makes more sense from bank’s perspective. This will help with bringing down CoD while maintaining edge over competitors.

I am invested and bullish on the bank over 3-5 years period. It’s in highly competitive and commoditized industry so getting to ROE of 12-15% will take a while. I wonder if ROE of the sector can be higher than 10% on a sustainable basis.

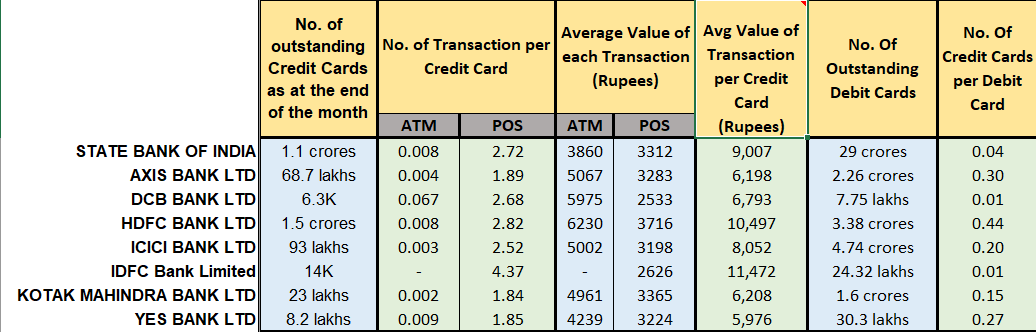

• We do not have data on the number of CASA accounts that each bank possesses. And hence, I have used the next best alternative i.e. the number of outstanding debit cards that each bank has

• IDFCF has the lowest penetration when it comes Number of Cards per Debit Card issued. The number is 0.01 whereas the number for the leader in this is 0.44 (HDFC Bank). This suggests that there is a huge scope here. This number is also very low for IDFCF because as of now it has tied up only with fintechs for the issue of credit cards. It is important to track these numbers after every quarter.

• One of the major income sources for any bank/credit card company is the ‘merchant fees’ charged on the transactions done by the customers at POS. Higher the number of transactions, higher the merchant fees income. Higher the amount of transactions, higher the merchant fee income. IDFCF boasts of the highest number of transactions per credit card. Next best are HDFC and SBI who promote their card business with a lot of offers. IDFCF is the distant first here suggesting that the offers/schemes are pretty attractive for the customers.

Good compilation but this analysis will be more accurate after credit cards are offered to the public, employees will be naturally biased The latest count (October) is now 20K and number of transactions at ~5 per card.

The bank now has introduced the referral scheme In the latest update of the net banking app as well. Hope this helps sustain/increase the CASA growth we have seen so far.