Loan referral scheme launched by IDFC First bank. I am not sure if other banks have this scheme or not but this looks quite unique to me. Advantages that I can think of:

Lower cost of customer acquisition

Only existing customers can refer. This means the bank has the data of the person who is referring. Adds another layer of scrutiny

It was launched in April, few weeks after lockdown announcement. I don’t know if it was already in the plans or they took the opportunity but great timing either way.

I have been thinking about how to project when IDFC First bank can come back to a respectable RoA, something which would lead to reasonable valuations. Here is my attempt at doing that

Data from old posts

As per my november post on OpEx, IDFCFB’s Opex/AUM is 5.4% and HDFCB’s OpEx/AUM is 3.3%.

From my October post on understanding NIMs and Provisions, a reasonable estimate for provisions and write-offs for IDFCFB seems to be capital first’s pre-merger number of 2%. Of course in the interim while they clean up balance sheet the provisions would be high (even for Covid, bank has created ~2.5% of AUM provisions). The FY20 Provisions+Write-offs were 4%.

From the same post, the NIMs for IDFCFB were 5.4% in FY20 and were 8%+ in CapF days. It is now clear why the RoA is negative or marginally positive. All the NIM (5.4%) goes away in OpEx (~5% in FY21 and 3-4% in FY20) and Provisions+Write-offs (4% in FY20 and possibly 3-4% in FY21).

Putting it all together

I think in a steady state, it is reasonable to assume that IDFCFB would have 2-3% Provisions+Write-offs (assuming similar asset quality as CapF).

The Opex as % of AUM has to come down to 3% from the current 5% (4% is a reasonable interim projection for the bank). This would happen as the bank disburses more loans from each newly opened branch and the OpEx scales much slowly than the AUM growth.

Assuming OpEx growth of 5% and AUM growth of 20% we get this equation which means that after 2.2 years, OpEx/AUM could become 4%.

The NIMs would expand back from 5.4% to 8%+ as the % of retail in the loan book and the liabilities increases. This would be supported by both a increasing CASA (taking cost of borrowing from 10% to <7%) and increasing retail loan disbursements. (The NIMs are already at 6.5% in H1FY21). Assuming that the expansion to 8% happens in 2 years time.

This means that in 2 years time, the PTRoA would be = 8-(2.5+4) = 1.5%. This means the RoA would be 1.1%.

One might ask, why I am doing this. The reason is to create key monitorables which can enable me to track the story and understand whether it is proceeding like I want it to proceed.

Key monitorables

Rate of growth of OpEx. Rate of growth of AUM. The larger the difference, the faster my fundamentals projections would be met.

Provisions+Write-offs in a steady state. I have modelled for 2.5% average (2-3% range). If they are much higher, it would spoil the party. Much lower would enable faster profitability.

NIM expansions: key sub-monitorables are Gross Yields and the Retail CASA+TD ratio. Gross yield should expand as retail as % of loan book increases and Retail CASA+TD growth would reduce interest expended line item.

I would wait for these key trends to play out in next 2 years or so and if they do not, then that would be a clear exit criteria for me.

Disc: Invested, Full PF here. I am positively biased. This post is for educational purpose only. Would request all investors to make their own informed decisions, discussing with their financial advisors.

I’m not sure if NIM will be as high as 8% so quickly. If the bank continues to lend at high rates they will risk losing customers with very good credit history to other lenders. Although they can poach customers from banks like Bandhan and NBFCs which lend at higher rates.

To stay competitive while maintaining low risk NIMs will have to be suppressed for a while. It will only expand once they gain strong footing in semi urban and rural areas in most states. I think this is why the current guidance is at 5.5 to 6%.

The bank already has a NIM of 6.5% in H1FY21. One has to discount for differences in methodology. I am only considering the AUM as the denominator. I think IDFCB reports NIMs with total assets in denominator, whereas I am only looking at AUM. That difference in methodology does not discount the conclusion though. Everywhere where i divide by 1.07 lakh cr, divide by 1.5 lakh cr and you’ll get the total assets denominated numbers.

That aside, would request you to kindly read my statement again for why NIM would expand:

Gross yield expansion due to changing PF mix. Retail loan as % of PF will increase. Rate of interest of average retail loan does not need to grow higher. As they expand the retail loan book faster than corporate one, gross yield will go up.

The CASA+TD ratio would move up. Current (H1FY21) average borrowing cost (denominated to total AUM) is 8% down from 10% at FY20 end. It is not unreasonable to imagine this move towards <7% as Retail CASA+TD grows.

In conclusion, my modelling assumptions are not at all incongruous with your point. bank might very well continue to lend at current rates.

Also, i think we have to understand the bank’s business model to understand why they have high gross yields: they are the market creators in several areas. One can think of IDFCF as the banker for the unbanked for underbanked. That is not to say that there is absolutely no competition, but those exist today as well and still they are able to disburse at a high Gross yield. That is only due to their primary competition being the unorganized sector which lends at 50-100% Interest per annum.

I usually shy away from analyzing things too much, especially technically (but thanks for all the effort you put in and share), what I look for is a more consistent performance each quarter. I’m not saying high NIMs are bad, if they achieve it without taking on more risk then its more than welcome.

The reason I feel it will be suppressed is because of what Vaidyanathan is trying to do. If you look at organization structure, management commentaries etc all things point to building a proper bank with sound fundamentals (not only fincancial aspects but things like employee culture). Not a bank that only focuses on banking for the unbanked.

If they over do it and ignore other areas the bank’s future growth aspects become unpredictable. I will take steady growth over spurts of short term growth anyday.

Not sure where you’re getting that from. Request you to Please read about MFI and MSME credit industry in India. Financing the unbanked is a secular growth story with in-built risks (which are modelled for in the Provisions+Write-offs section). The unbanked are unbanked only the 1st time they take a loan, then, for the income generating activities, there is a need for repeated consistent credit.

The Arman thread is very good, so is the MFI thread. A lot of these loans are income generating with high ROIC, which is why the lendee needs it repeatedly and is also able to afford 15-25% interest rates.

My primary purpose is: for any turn around story there has a to be a clear exit strategy. Until when would one wait for IDFCF to turn around? That is the question I want to answer for myself (and anyone else who is interested). The key outcome is the methodology. One can always plug different numbers for different high probability scenarios (for ex: if you feel NIM growth would take longer).

I meant that in a general way, too much of something is always bad Growth in just one segment will have its limitations, the bank will accumulate other types of risk if they do that. Lets say their MSME book grows too large relative to other segments, what happens if some future govt creates some adverse regulations that disproportionately affects only that segment?

We do business that is important for society. We are passionate about serving our customers well. We borrow at 7% and lend at 12-14%.

Vaidyanathan’s words from annual report. This indicates a conservative approach, I’m mentally prepared for slower expansion in profits because it is in line with my personal financial goals.

I do wish they would focus more on improving opex though.

Btw we are in complete agreement. 8% NIM on 1.07 lakh crore AUM translates to 5.7% on Total assets. I am using the 1.07 lakh crore due to the usage of Average earning assets in the NIM definition. For some reason, bank seems to be using total assets. In any case, with the usage of total assets in denominator for NIM, the relevant numbers are:

Provisions+Write-offs of 1.8%.

Current OpEx is at 3.8% of total Assets. Target OpEx at 2.8%.

Assuming OpEx growth of 5% and total assets growth of 20% we get the same equation which means that after 2.2 years, OpEx/Total Assets could become 2.8%.

NIMs would expand from 4.6% H1FY21 to 5.7% in 2 years.

This means that in 2 years time, the PTRoA (Total Assets) would be = 5.7-(1.8+2.8) = 1.1%. This means the RoA (Total Assets) would be 0.8%.

I think the interest rate cycle (and thus inflation) has a huge bearing on how fast the bank grows and how fast (and to what extent) does the NIM grows. Please keep in mind that IDFCF bank cannot keep paying 7% interest on savings account forever. At some point in time this has to come down (Although Vaidy has nowhere mentioned that he plans to reduce the rates in the near future but this is how Kotak story unfolded too). What will be challenging for the bank is reducing the interest rates on savings account in a rate hike cycle.

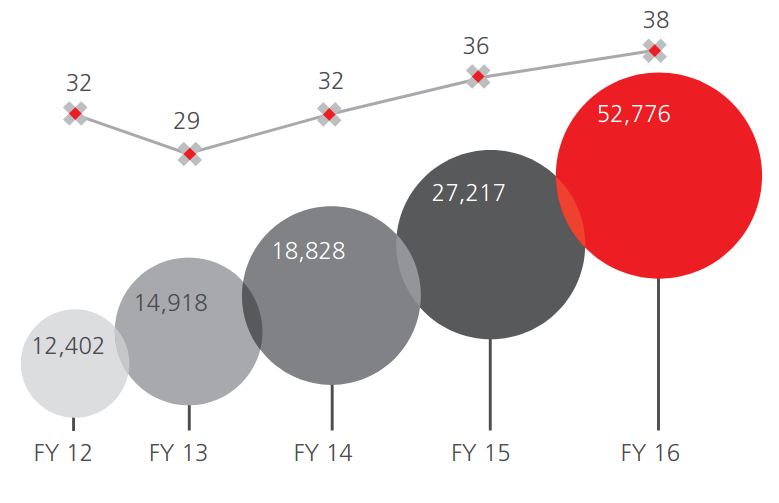

It took 3 years for Kotak to go from 12.4 to 27.2K Cr, the bank beat that in a year. This is impressive even if you consider the tail winds enjoyed by the bank (govt’s digitization efforts and tendency to save due to pandemic).

Kotak CASA is still growing at a good rate so I think lowering interest rates won’t affect too much. The biggest concern regarding raising CASA was gaining public trust and it seems like they have already done that. Even if we assume all shareholders put their money in the bank, that’s only about 10L accounts, based on debit card count we can assume number of accounts is north of 20L and growing fast.

They can still keep riding the psychological effect of 7 as @sahil_vi mentioned (in an old post, I think), first lower the slab from 1Cr to 10L Rs and then to 1L Rs, creating a very diverse customer base.

The headline is a bit misleading, he actually says collections in MSME segment is back to normal. MSME book growth is the laggard, and will be for the next 6 months. Consumer durables, auto/personal loans and housing will see growth.

This is a paid article but very good comparison between Bandhan bank and IDFCFB. My notes:

Both took inorganic routes to scale. Bandhan acquired Gruh Finance (housing finance portfolio); IDFC Bank’s merger with Capital First gave it retail facelift.

83% polled on Bloomberg positive on Bandhan Bank, much higher market acceptance & valuations. If judged on balance sheet strength, IDFC First Bank fares better.

IDFCFB’s advantage is its highly diversified book, particularly on the retail front comprising home loans, consumer loans, vehicle loans, apart from MSME loans.

Gruh’s acquisition lifted Bandhan’s housing portfolio to account for 25% of loans, dependence on microfinance loans hasn’t reduced (65% of book); the share of retail loans is a mere 1%.

NIM at 8% for Bandhan Bank seems lucrative, though margins have steadily reduced over years. Equirus expects NIM to contract to 7.1% in FY23 due to switch to low-yield products. IDFCFB NIM has expanded from <2% in FY19 to 4.57% in Q2FY21 owing to retail book.

On CASA ratios and deposit growth, IDFC First Bank has outpaced Bandhan

How soon IDFC First Bank runs down its wholesale loans will be critical to win the Street’s confidence.

Disc: Invested from lower levels. largest position. Planning to increase position once retail RoAs become steady and positive.

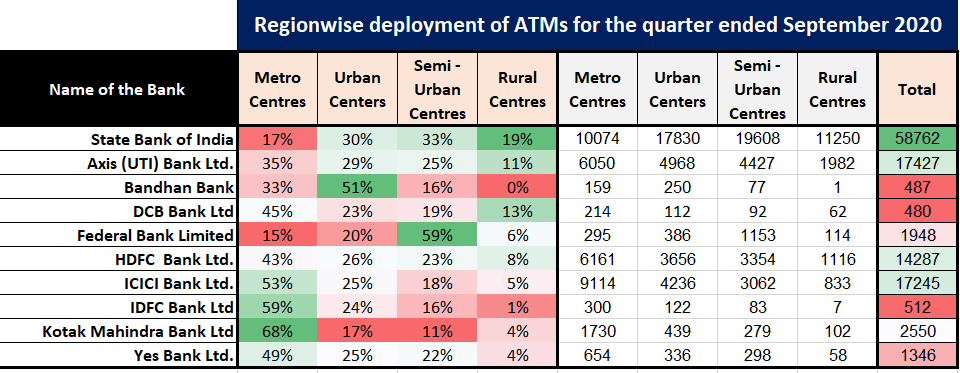

Kotak Bank and IDFCF Bank seem to be following a similar strategy with highest share of their ATMs in the ‘Metro Centres’ and lowest share of their ATMs in Rural Centres.

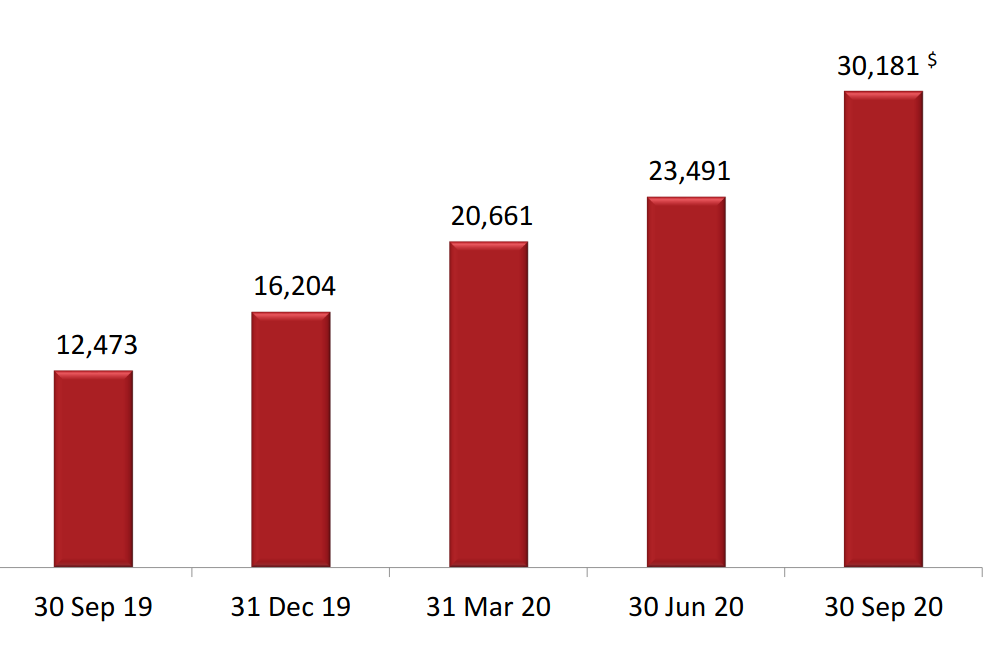

Customer Deposits of the Bank increased to Rs. 77,289 Cr as on 31 December 2020 from Rs. 54,631 Cr as on 31 December 2019 (YoY growth of 41%). This was Rs. 69,368 Cr as on 30 September 2020 (QoQ growth of 11%).

Retail Deposits (CASA and Term Deposits) of the Bank increased to Rs. 58,435 Cr as on 31 December 2020 from Rs. 29,267 Cr as on 31 December 2019 (YoY growth of 100%). This was Rs. 49,610 Cr as on 30 September 2020 (QoQ growth of 18%).

Top 20 Depositors as a % of Customer Deposits has reduced from 23.0% as of 31 December 2019 to 9.7% at 31 December 2020. This was 12.4% as of 30 September 2020

Average CASA ratio (on average deposit for the quarter) for Q3-FY21 was 44.6% as compared to 20.9% for Q3 FY20 and 36.5% for Q2 FY21. CASA ratio on outstanding deposits as on 31 December 2020 was 48.4%.

Retail Funded Assets increased to Rs. 66,635 Cr as on 31 December 2020 from Rs. 53,685 Cr as on 31 December 2019 (YoY growth of 24.1%). This was at Rs. 59,860 Cr as on 30 September 2020 (QoQ growth of 11.3%).

The Overall Funded Assets of the Bank increased to Rs. 1,10,499 Cr as on 31 December 2020 from Rs. 1,09,698 Cr as on 31 December 2019 (YoY growth of 0.7%). This was at Rs. 1,06,828 Cr as on 30 September 2020 (QoQ growth of 3%).

My Interpretation: The CASA growth has been quite phenomenal. It beats even the most optimistic expectations that even I had. CASA ratio of 48% on Dec 31 is quite fantastic. They’re right up there with the likes of Kotak Mahindra bank. This is despite having cut the deposit interest rates a bit on Sep 15. This also demonstrates the stickiness and the granularity of the CASA. Good growth in the loan book as well. 3% QoQ loan book growth is quite conservative. Would be interesting to see how the RoAs and the provisions are looking like now.