Thanks for talking about this. I was just reading about this yesterday. I think key thing is for us to understand what this segment breakup is.

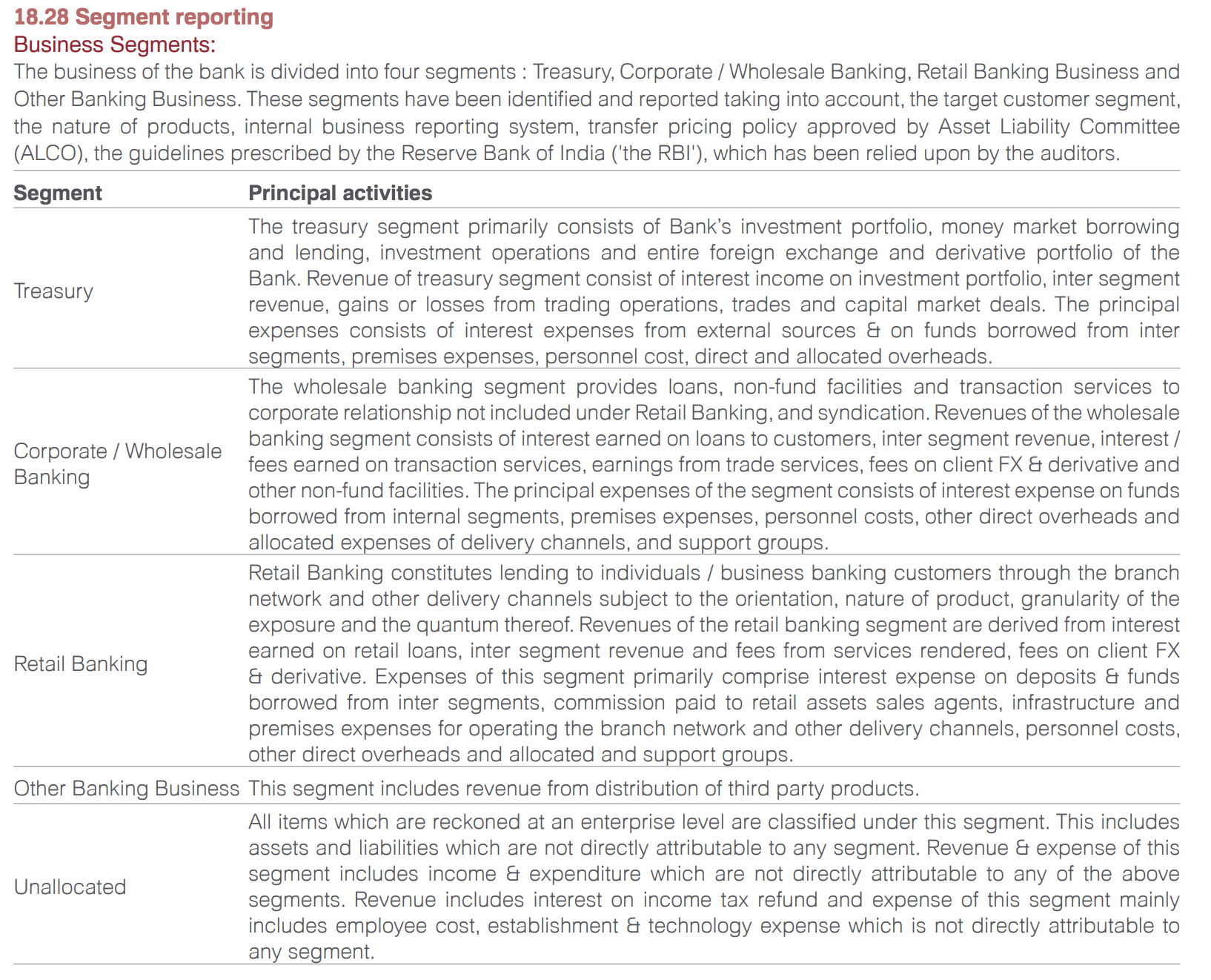

First step is to understand what segment reporting is. Please see and read Page 200 of IDFCFB Annual report for FY20:

- An investor would appreciate that building a sticky CASA franchise has many upfront costs. The newer branches would have fewer customer relations and hence lower branch-level ROAs than average.

- Another thing an investor will appreciate is that Treasury as a name is misleading. I quote most relevant line with bolding: “Revenue of treasury segment consist of interest income on investment portfolio, inter segment revenue, gains or losses from trading operations, trades and capital market deals”. As per my understanding, if they dispose off bad debt in capital markets (the way they did for DHFL) that would be included as income in Treasury operations, while the loss (in previous quarters) would have been booked in Wholesale part.

- Operating leverage as a concept cuts both ways. If the bank has shrunk the wholesale book over the years, then the profits could fall as well. Also, A large part of Wholesale book was infra book, and as we know, most of infra and RE players have been in a down-cycle for many years now.

- Look at the same segment revenues and ROAs for HDFC bank (the gold standard in banking). I Quote from Q2-FY21 disclosure:

Look at the Retail banking H1-FY20 vs H1-FY21 Income from operations (PBT basis). It was 7090cr on an asset base of 4,60,000cr in H1-FY20. PTRoA* of 1.54%. It is 4875cr on an Asset base of 4,77,000cr in H1-FY21. This is a PTRoA of 1.02%. Even for HDFCB, H1 has proved to be difficult. It should not surprise us that IDFCFB’s PTRoA has worsened in H1-FY21 for retail segment (the segment which I’m watching most closely). It is -839/61830 = -1.35% vs -489/51337 = -0.95% in H1FY20. This is despite the aggressive branch expansion. - CEO has repeatedly talked about the Cost to Income ratio being lowered. Currently it is very high. as the bank scales up, same branches bring more CASA and loans and fee based income, as same bank launches credit card and brings in Fee based income, the Cost-to-income ratio should go down and hence improve the segmental PTRoA. This remains a key monitorable. But I would not expect it to improve any time soon. Depending on how the Covid-19 pandemic pans out, it could easily take 1-2 years for the segmental PTRoA to become > 1% and hence for Retail to start contributing significant profits.

*PTRoA (A term coined by Me): Pre-tax Return on Assets

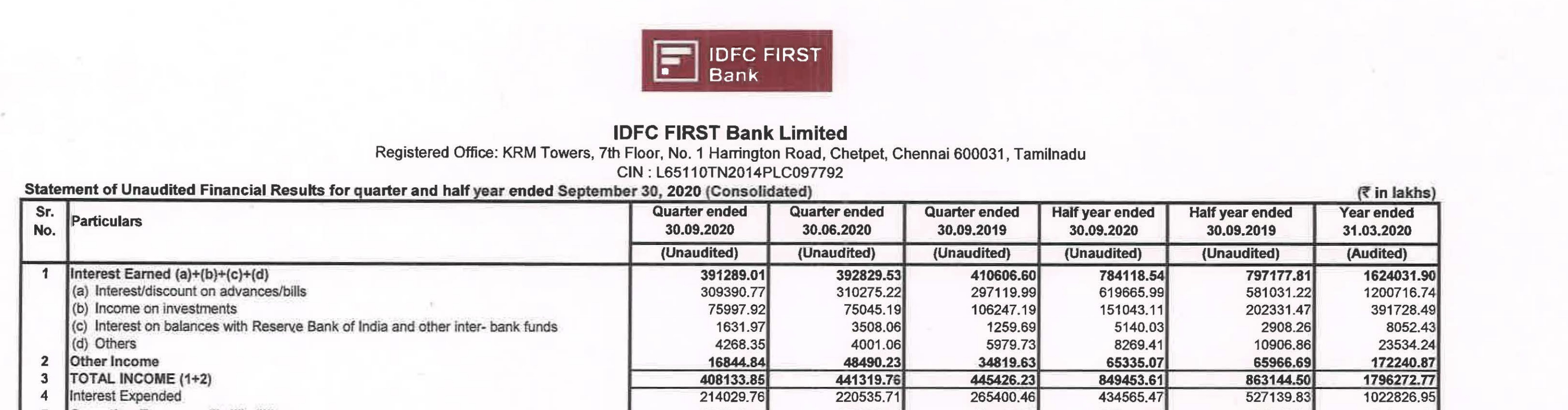

Sorry, I don’t know what you’re saying. Interest outflow has reduced significantly. Have a look at row 4 below:

Also, have a look at data I had posted before:

This was roughly 10% in FY20. It is now at a run-rate of 2140*4/107000 = 8%. So interest expended has come down from 10% to 8% in current quarter.