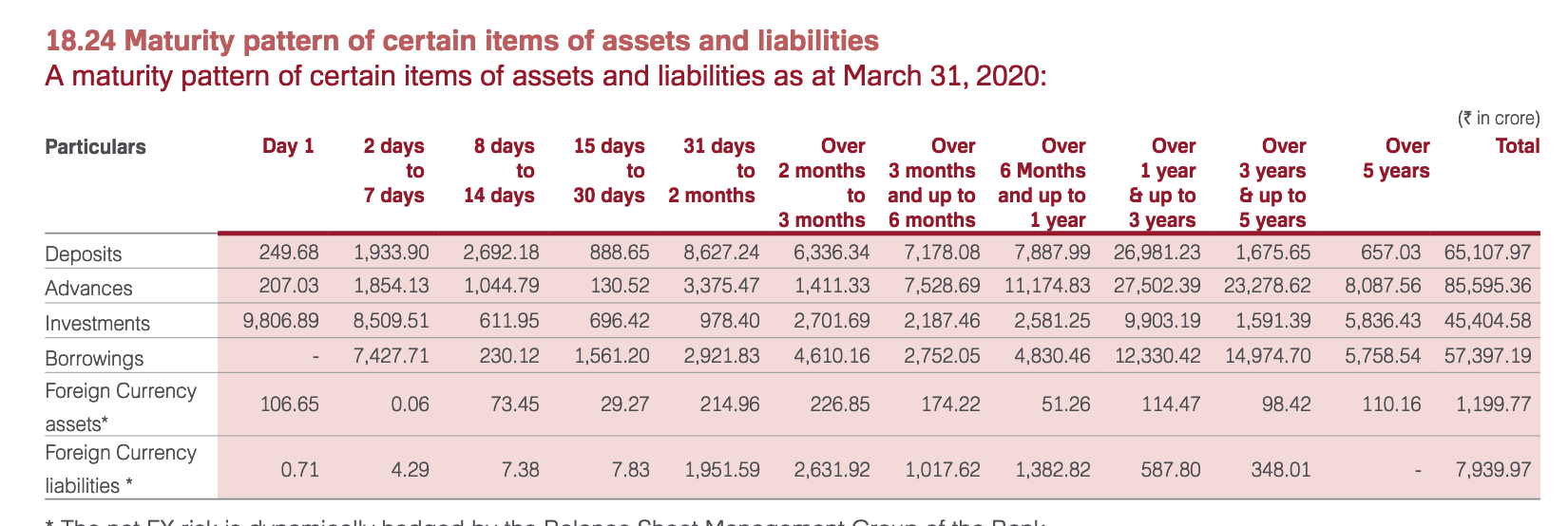

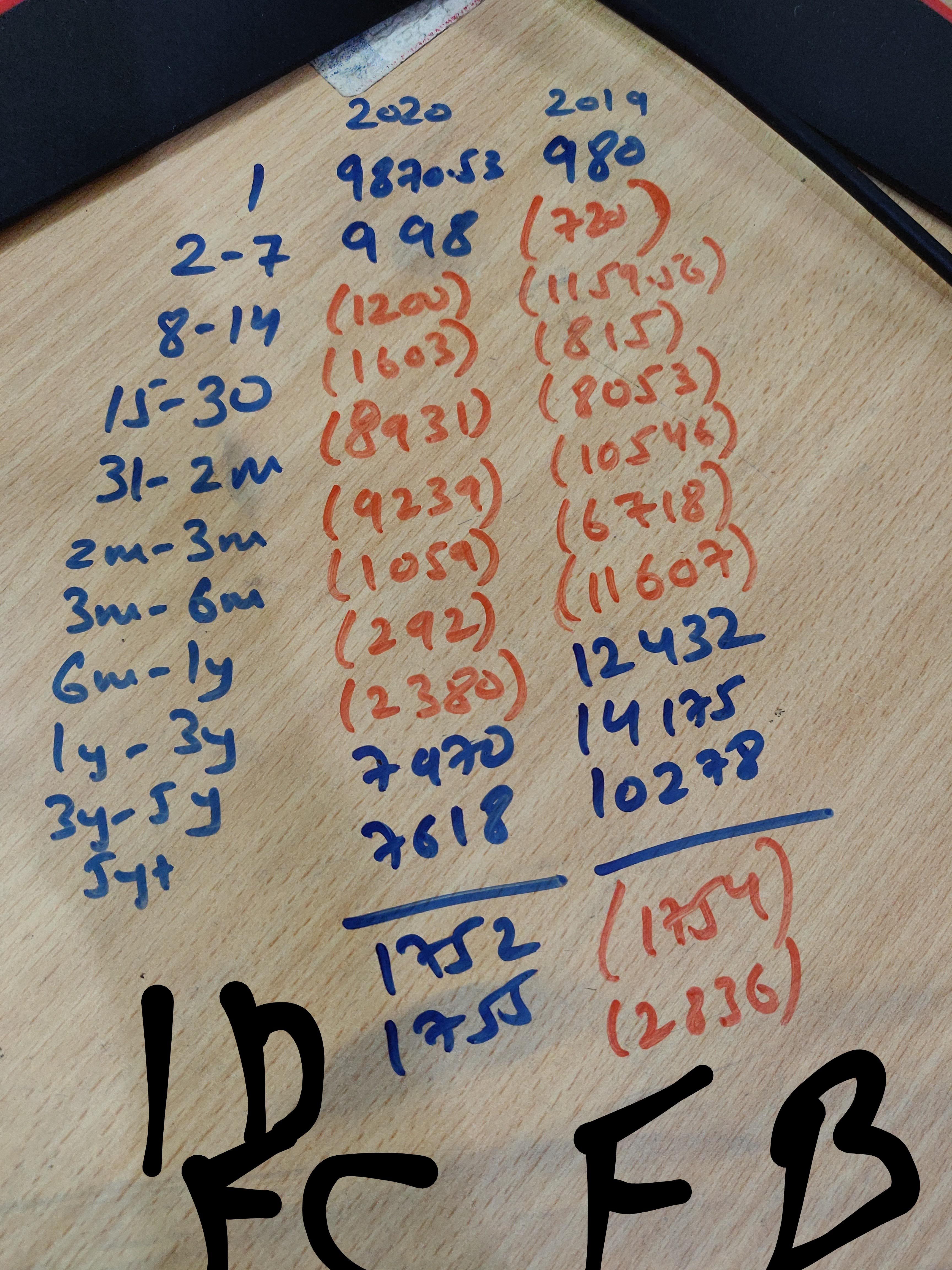

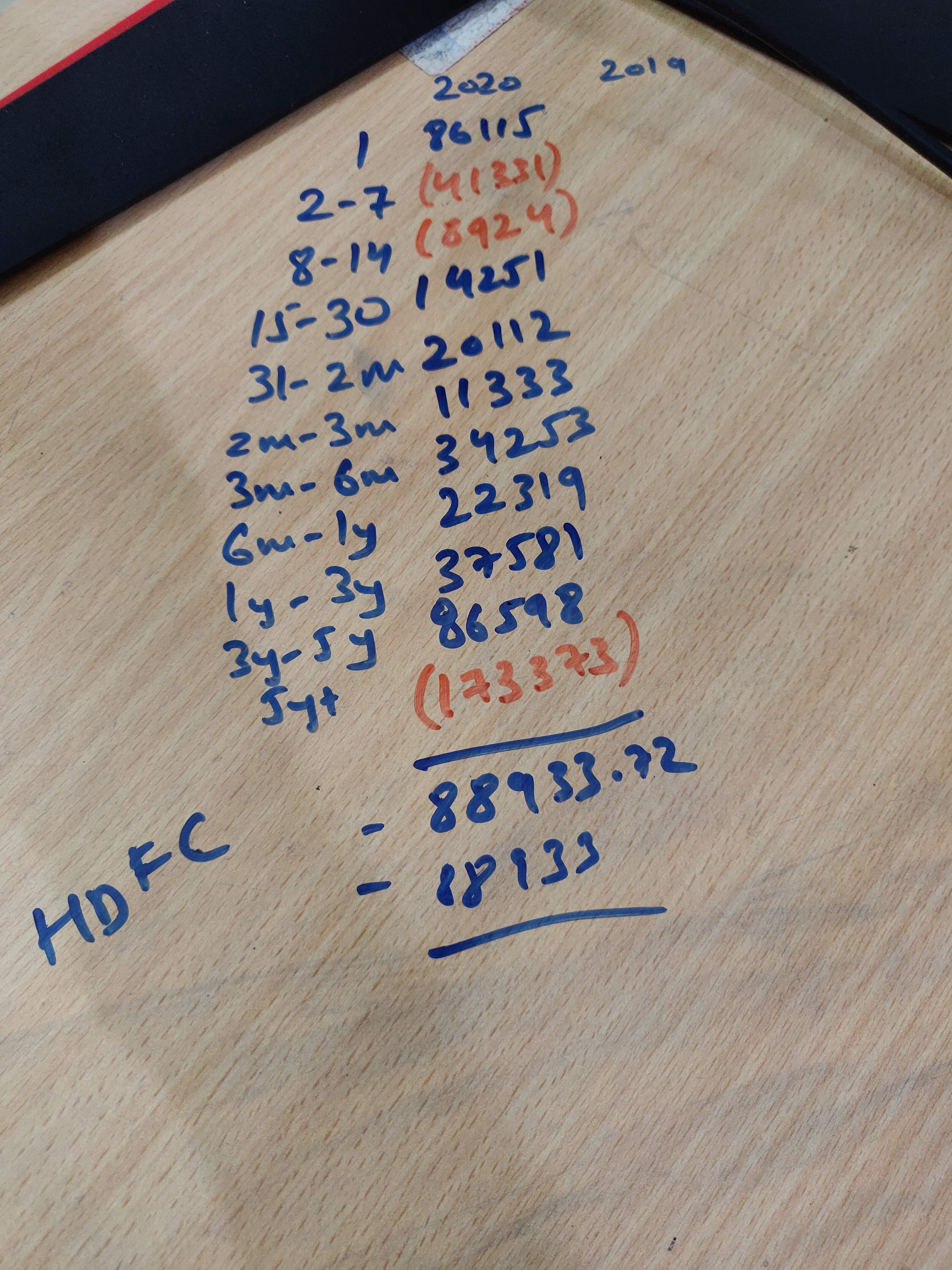

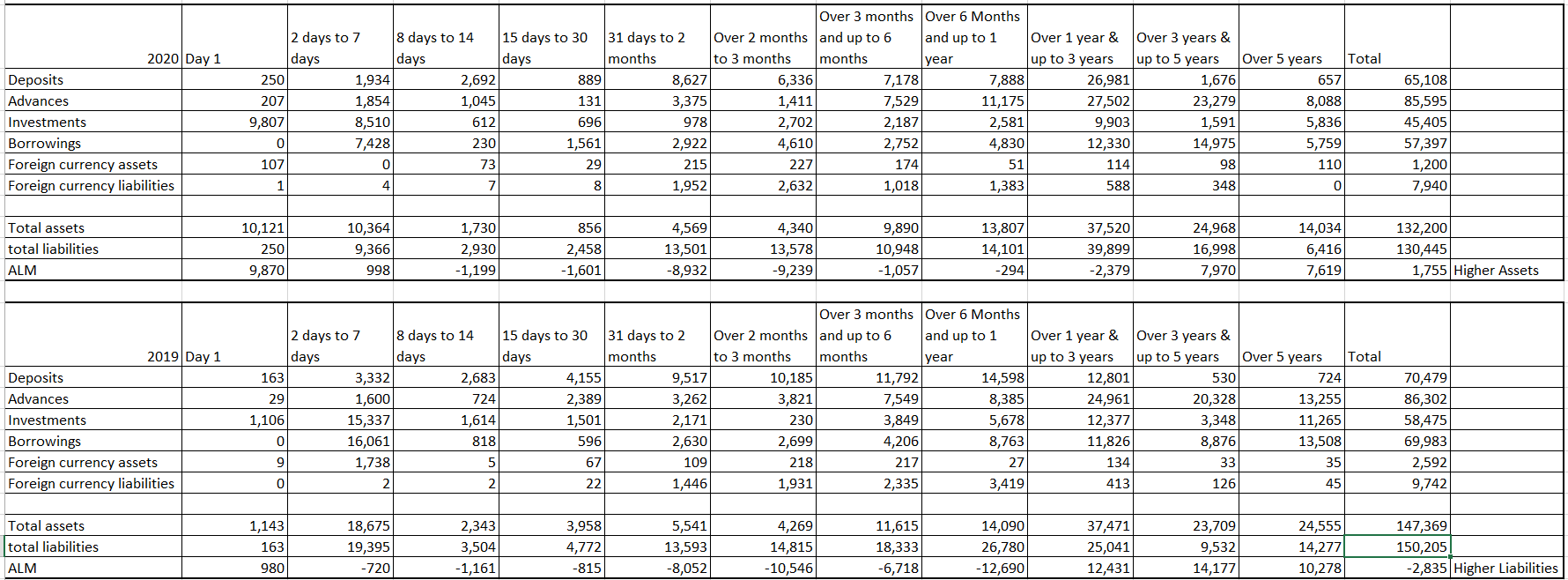

Has anyone noticed the constant negative Asset Liability Mismatch (as per Pg: 197 of the report) is very high for each interval duration and in cumulative starting from duration of 8 days - 14 days going all the way till 1 year - 3 years?

Note: IDFC First Bank has very decent LCR (Liquidity Coverage Ratio) and decent amount of HQLA (High Quality Liquid Assets), but it seems to be a long running pattern to have such huge ALM in the favor of higher liabilities than available assets.

Such ALMs scare me of IL&FS Crisis hence the query

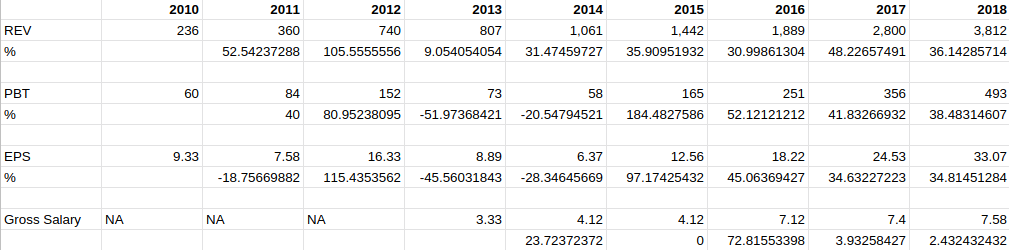

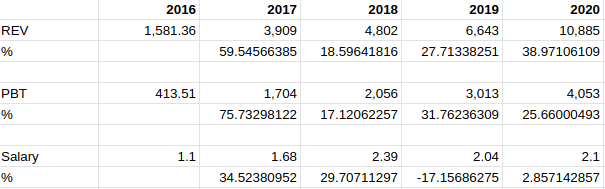

Since I intend to hold this for a long time I looked at Vaidyanathan’s past compensation trend (in crores in the figure) to convince myself that he is the real deal. Data is from CapF annual reports and Screener.

He said no to bonus in 2013. The big jump in 2016 is also due to performance bonus (2 Cr).

Salary in 2020 was 6.42 Cr. Though the reduction can be attributed to the bank struggling after merger, I think it is telling that he accepted such a daunting task while being paid less. IMO this only means one thing - he is utterly committed to leaving his mark as a banker. This reinforces the things he said in the past about dreaming of running his own bank.

All this coupled with the fact that he does own a large stake gives me enough comfort and peace of mind as an investor. My largest holding, not a recommendation.

Here is a very good video for understanding Infrastructure financing and why almost all banks which have tried to finance infra have failed:

Although this is not directly tied to current (& Future) IDFC First bank, it is helpful to understand the nature of the infra related balance sheet problems and what the government is planning to do to address those problems. Very broadly:

Banks like IDBI, ICICI (& IDFC) have failed to successfully lend to infra projects because building anything in India is difficult and a long drawn process.

It takes several decades sometimes to build a simple flyover. There are several reasons for this such as politics, land acquisition difficulties (in fact along with difficulty in enforcing contracts, difficulty ‘building anything’ is one of the foremost reasons for India’s low “ease of doing business” rankings : source1, source2), several permits required and so forth.

This creates an asset liability mismatch since most depositors want their money in much shorter duration of time (say 2-3 years).

The solution here is to facilitate creation of a deep infra bond market where asset liability mismatch is solved for, by construction.

I recently joined the discussion on this topic. Very enlightening in many aspects.

I would like to put forth my views on two questions:

Can the bank grow at 20-25% for foreseeable future?

If they are lending at high rates, does that mean they compromise on asset quality?

To the first question, the target credit borrowers (SME Financing, livelihood financing etc any name you give) of IDFC First are under financed for decades now. In fact, to highlight this point, i want to refer to the book “Bridgital Nation” by N Chandrasekaran (of TATA Group). The screenshot of the book is below:

As can be seen, the struggle for finance is real. Infact as per reports mentioned in the same book, Micro firms employed 120 million people in 2014 and they make up 70 per cent of India’s firms. So the target of 20-25% growth is achievable.

This leads to the next question. These Small firms mostly borrow from informal sources. Infact as mentioned in the book 84% of the financing was informal. So optically the lending rates may look high for us, but the person taking it knows well enough he is benefiting comparatively. So the formalisation of lending for such firms is like win-win for everyone. So just because they are lending at high rates doesnt means the asset quality is bade. Thus, If the underwriting is good,the asset quality will be good. In fact they generally grant loans to 38 of 100 application they process (on average). This shows something on asset quality front.

My main concern is that as the bank grows they will look to lend bigger ticket sizes to larger enterprises (medium in MSMEs). That’s when things will get tricky because bigger loans translates to harder collections and as the firms grow in complexity they might not continue to well financially. This report shows that defaults are higher for medium and large enterprises but low for the smaller ones.

As long as they lend small loans the bank should do well. They just need to be more careful as the businesses they already lend to grow, even if a borrower has spotless record of repayment there is no guarantee that he will continue to run his own business well as it grows.

Micro sector with 630.52 lakh estimated enterprises accounts for more than 99% of total estimated number of MSMEs. Small sector with 3.31 lakh and Medium sector with 0.05 lakh estimated MSMEs accounted for 0.52% and 0.01% of total estimated MSMEs, respectively. Out of 633.88 estimated number of MSMEs, 324.88 lakh MSMEs (51.25%) are in rural area and 309 lakh MSMEs (48.75%) are in the urban areas.

From the MSME annual report, seems like medium enterprises defaulting will not be a big problem after all. And most of the defaults among micro and small enterprises will likely be absorbed by PSBs. If the bank develops strong expertise in serving areas where other banks don’t even dare it can become a significant moat, however this is something that will take time.

Do we have any data available the percentage of lending in rural and urban?

@mvc7799 You can check past investor presentations, look for “Rural Micro Finance and KCC”.

They already have this moat and capability from the CapF days. The retail loan book has grown from 36,000 cr in Dec’18 (merger quarter) to 60,000 cr in Sep’20 at a CAGR of 33%. This strong retail loan book growth is on the back of that expertise, and due to the bank understanding the space very well. Retail Loan book has grown even compared to pre-corona and Sep’20.

Key monitorables for me remain:

The amortization of the high operating expenses over a larger loan book, leading to lower cost to income ratio

The way that covid related defaults turn out. They have already provisioned for ~2% of loan book, and I believe would be provisioned for ~3% of loan book by Mar’21. Any GNPA <= 4% would be welcome news and anything more might be something which needs additional provisioning in FY22.

Right, I meant to say something even stronger that will allow them to scale steadily for years or even decades. India is in a very dynamic phase right now and the bank cannot afford to get complacent, they will need to invest in understanding each and every type of MSME out there if 30% growth is to be achieved for the next 10 years. For this reason I expect the bank’s expenses will be relatively higher than other banks for quite sometime.

Having said that, it is reassuring that MSME is not the only area of focus.

Also since I’m long, I’m not too concerned about covid impact. If anything they will learn more about their borrowers and come out stronger.

So on article written by V Vaidyanathan appeared in Mint on December 29, 2020. One point which might be of interest to this discussion is restructuring in the Bank. He mentions:

A total of 76,765 small borrowers availed of online restructuring from us for ₹662 crore at the time of this article.

Avg loan size of restructured accounts can be estimated be around 85,000 to 1 lakh. Pretty good diversification

I am guessing the restructured accounts to be from the sectors that were highly affected by pandemic and most of the them would be servicing their debts as cash flows improve on economy reopening.

I do have one doubt though. Interest for Loans under Emergency Credit Guarantee Scheme are capped at 9.25%. So the bank wouldnt be making much on it ryt? But still the bank did give loans under he scheme. Can anyone think of the rationale for the same?

While the returns are low, there is virtually no risk. And only existing customers are qualified, which will strengthen the bond between the bank and reliable customers. Saying no might do more harm than good in the long term as there are many other lenders.

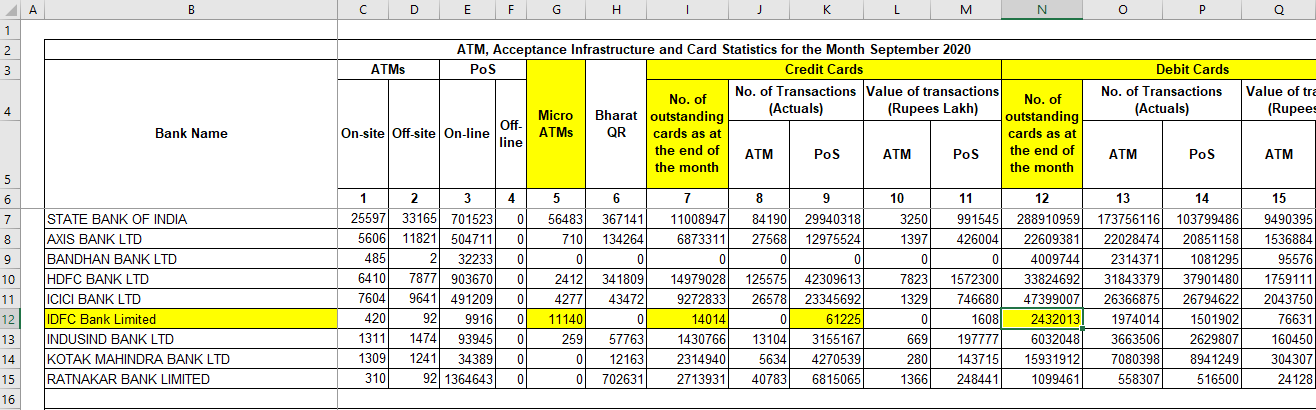

IDFC First is going big with Micro ATMs. This probably was strategy of erstwhile IDFC too IMO. Second highest number of Micro ATMs after SBI (in the banks that I have compared). Upfront expenses also obviously would be less than regular ATMs.

14014 credit cards were outstanding at the end of September 2020 with 61225 transactions. So on an avg of 4 txns per card. Good traction.

2432013 debit cards were outstanding at the end of September 2020. This can roughly be equated to the number of accounts.

Thanks for this information. I would like to delve a little deeper into this. Can you please guide me under which section I can find this information on the RBI website?

Noob Question: Where can I find the figures for no. of savings accounts for each bank? Do I have to visit their Annual Reports individually? I cant find much with respect to this on the RBI Website.

I previously mentioned that the bank may have to spend more to increase reach and understand MSMEs but realized today that some of their CSR activities are designed to benefit the community and increase bank’s reach of targeted demographics at the same time. Very efficient use of funds!

For example, the Shwetdhara Programme:

More than 11,000 rural households have been reached via this programme through services like artificial insemination, cattle treatment, feed and fodder services, medicines supply for the cattle. Aligned with IDFC FIRST Bank catchment areas, this programme was run at the grass root level by a cadre of women leaders in the community called ‘Gram Sakhis’ who enabled last mile service delivery. We have reached 30,300 beneficiaries and trained 224 Gram Sakhis that cover 192 villages across the two states.

Programs like these not only increase reach but also increase financial literacy, efficient borrowers → low risk of default.

The trainings administered by Shwetdhara tutors prevents us from getting duped by local veterinarian doctors who charge us five times more and do not produce any result.

This feels like a small thing now but I think it creates a positive feedback loop as the bank grows. Growth → increased profits → more CSRs like this → increased outreach → growth.

Some other examples are MBA program → potential employees, employment program → potential consumer durable loan customers.