Hi,

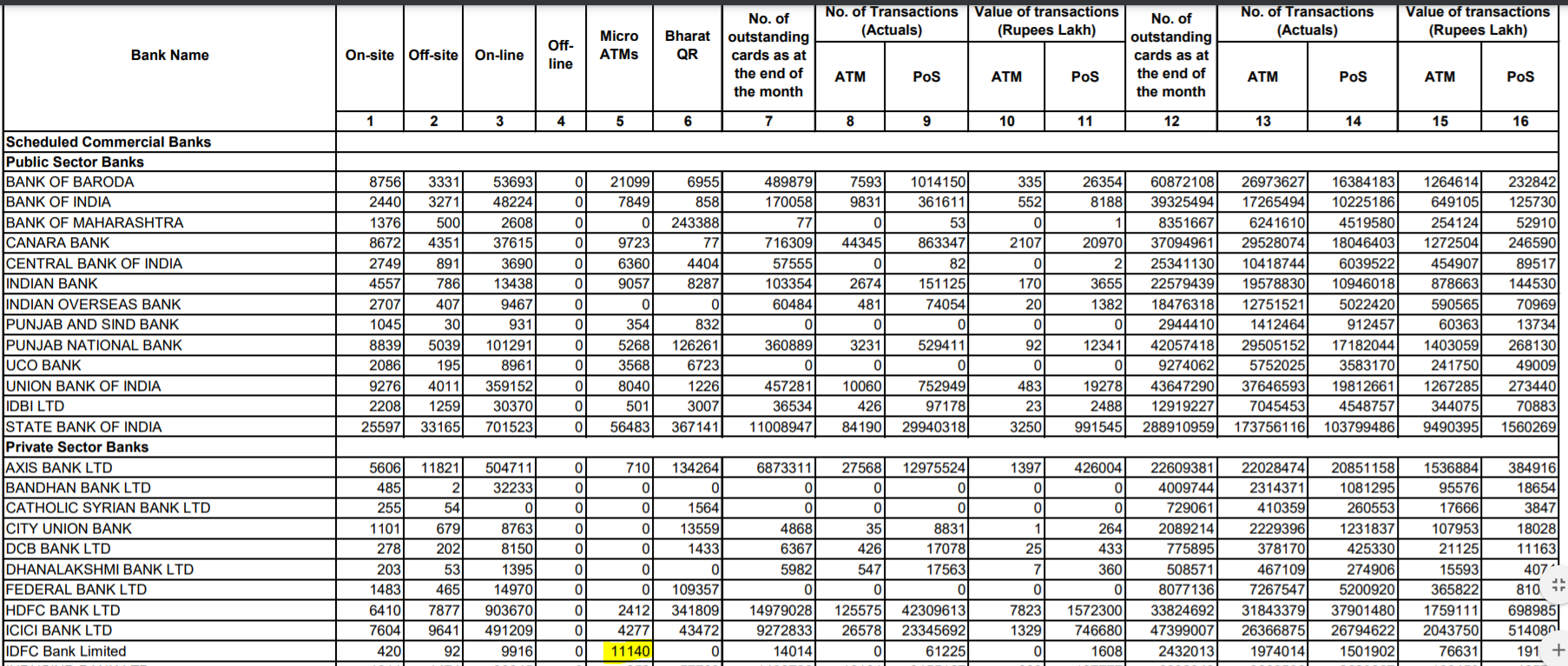

As per the RBI’s data, IDFC has highest no. of Micro ATMs (more than the combined no. of all other private banks put together). Can someone pls explain what is Micro ATM and why IDFC has invested in so many of them?

Hi,

As per the RBI’s data, IDFC has highest no. of Micro ATMs (more than the combined no. of all other private banks put together). Can someone pls explain what is Micro ATM and why IDFC has invested in so many of them?

I think they are part of expansion plans since before merger, most likely to cater to rural, semi urban areas when IDFC lacked branch reach.

Erstwhile IDFC Bank had strategy where they wanted to leverage next door shops as mini branches vs opening branches. These shops were given these machines which will act as ATMs.

But the strategy did not really worked out…

Hi Akhilesh,

Great analysis. While there has been an increase in the average balance per account, it also has to do with the increase in savings of the citizens during the pandemic. I think we have to wait for another 2-3 quarters and then compare the figures to make better sense of it.

Micro ATMs basically help to spread/extend your branch network at a lower cost. I think (might be wrong) htat focus on branches would be much more in urban areas and slightly lesser in extreme rural areas. Having said that, you can check this link for more info on it: https://www.idfcfirstbank.com/banking-products/micro-atms.html

I agree, the pandemic accelerated the already increasing trend. Even if it slows I think it will be easily offset by new customer acquisition.

There is one other interesting point I forgot to mention. In AR 2020 they mention owning more than 100 toll plazas, likely acquired from struggling infrastructure borrowers. What makes this significant is that there are only 562 toll plazas in total according to NHAI http://tis.nhai.gov.in/tollplazasataglance

IDFC FIRST Bank continues to be one of the leading banks with acquisition of over 100 toll plazas, having issued over 10,00,000 tags in FY20. The Bank has teamed up with various fleet owners, dealers and Tech service providers in the logistics space to provide Digital solutions which are simple and secure to use for the truck operators.

The bank will likely benefit from increased logistics movement going forward. I would appreciate if anyone can comment on how this would benefit the bank, there could be negatives as well because it’s not core business.

I feel the valuations or stock price movement would be completely dependent on how the core banking business is doing. This income would be a part of Other Income and will not be looked much into. Going forward, the bank might look to sell these too for a one time gain (or for setting off losses maybe)

They don’t actually own the toll plazas, just the toll collection on the plazas is handled by them.

More details here- https://www.dimts.in/National-Electronic-Toll-Collection.aspx

This is precisely where Mr. Vaidyanathan comes into play. I don’t think he’ll be impatient. He has already built a Taj Mahal, he knows it takes time but the end result is worth the effort and patience.

Thank you for your inputs on the tech part, very interesting, such forward looking approach is exactly what sets winners apart.

Yes I’m still bullish on long term prospects, intend to hold it for more than a decade.

I invested because of Vaidyanathan, or rather in his dream of building a solid bank. I’m sure he means it when he says that and the whole team is working hard.

They have released a handful of loan apps recently https://play.google.com/store/apps/developer?id=IDFC+FIRST+Bank+Limited. Different apps for different products and dedicated teams behind them will likely improve operational efficiency, from serving customers to striking deals with manufacturers and everything in between as teams don’t have to step on each others toes.

The one I liked most is the referral app - https://play.google.com/store/apps/details?id=com.capitalfirst.connector. This will aid in reducing commissions paid to DSAs and as the customer base grows cost of commissions as a percentage of operational costs should go down because they can cross sell products. No data to back this up but I feel new borrowers referred by existing customers will likely be reliable borrowers as well.

RBI updated the branch list today (bi-weekly updates) https://www.rbi.org.in/Scripts/bs_viewcontent.aspx?Id=112

If I recall correctly the count was 553 at the end of October, now at 577 so 24 new branches in a month! Branch expansion doesn’t seem to be slowing down

Just regular update -

I have met with Regional head responsible for raising retail liabilities couple of days back. He said They are getting CASA very thick and strong this quarter also. Also from one other employee i came to know they focusing on opening current accounts this quarter. And probably Credit cards will be launched by 15 dec 2020 with very good offers.

Query -

Does any one have noticed why IDFC First bank have lot of complaints on twitter? is it same for other banks also ? It is difficult to track for other main banks as they have multiple handles.

Yes, the number of complaints on Twitter is a lot. Major themes for these complaints are:

-Customers getting pestered for loans

-Automatic debiting of money for loan repayment even after the customer has got moratorium approved

-Automatic granting of loans when the customer didn’t even take it

But, you’ll find a lot of complaints against HDFC Bank too. But the theme is completely different.

Also, one thing I noticed: IDFC First bank’s app has 4.0 ratings on Google Play, kotak and hdfc have 4.3 and ICICI has 4.4, Of course the number of downloads for IDFC app is quite low when compared to other banks, but the management needs to focus here specially when it talks so much about technology.

Can you share what are the themes of complaints against HDFC bank

Don’t you think this is serious?

I would not worry about negative reviews for 6-12 months more, their systems are most likely still in flux as a result of merger and new ideas/proposals experimented with to encourage innovation means less reliable systems overall.

I believe people are resorting to social media more because their customer service is more active compared to other banks. At least seems like that is the case. Of course I’m not saying they don’t need to improve but it will take time to mature.

It may help to compare reviews with banks of similar size rather than HDFC/ICICI/Kotak, at this time they are apples and oranges.

Yes, but what I mean to say is, it’s understandable that they are constantly calling people for loans etc, or someone getting debited for repayment. but loan getting issued randomly? that’s scary.

Please refer this to understand the RBI new guidelines

I am holding the acount and requested for personal loan .They didnt even call me back.i know they wont call becoz margins are less on personal loans

I agree it is a problem but we have no way of telling if it is widespread, in the worst case RBI or consumer courts will impose a fine.

I’m not a customer of any products but I have downloaded the apps and tried clicking around, EMI payment still goes to capital first links, that is the reason I said it is still in flux. As a result the systems might not be in sync, building a software ecosystem takes time and merging two different systems is even harder.

The only thing investors can do is wait and watch.