The bank is giving 7 % interest for the balance above Rs 1.00 lakh, highiest in the industry.

This may be the reason for CASA growth and sharp increase in interest outflow.

Overall the bank is progressing decently.

1 Like

Thanks for talking about this. I was just reading about this yesterday. I think key thing is for us to understand what this segment breakup is.

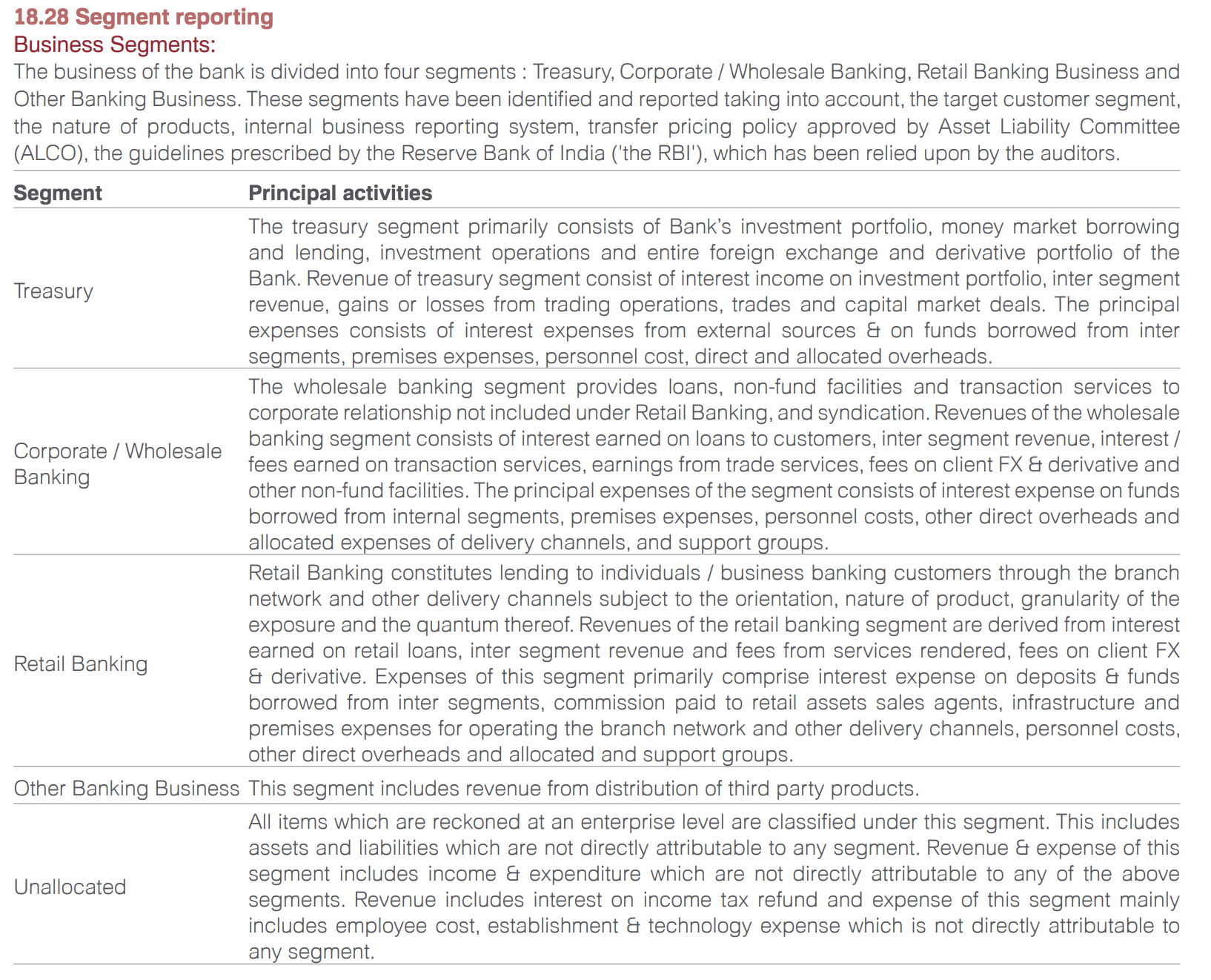

First step is to understand what segment reporting is. Please see and read Page 200 of IDFCFB Annual report for FY20:

- An investor would appreciate that building a sticky CASA franchise has many upfront costs. The newer branches would have fewer customer relations and hence lower branch-level ROAs than average.

- Another thing an investor will appreciate is that Treasury as a name is misleading. I quote most relevant line with bolding: “Revenue of treasury segment consist of interest income on investment portfolio, inter segment revenue, gains or losses from trading operations, trades and capital market deals”. As per my understanding, if they dispose off bad debt in capital markets (the way they did for DHFL) that would be included as income in Treasury operations, while the loss (in previous quarters) would have been booked in Wholesale part.

- Operating leverage as a concept cuts both ways. If the bank has shrunk the wholesale book over the years, then the profits could fall as well. Also, A large part of Wholesale book was infra book, and as we know, most of infra and RE players have been in a down-cycle for many years now.

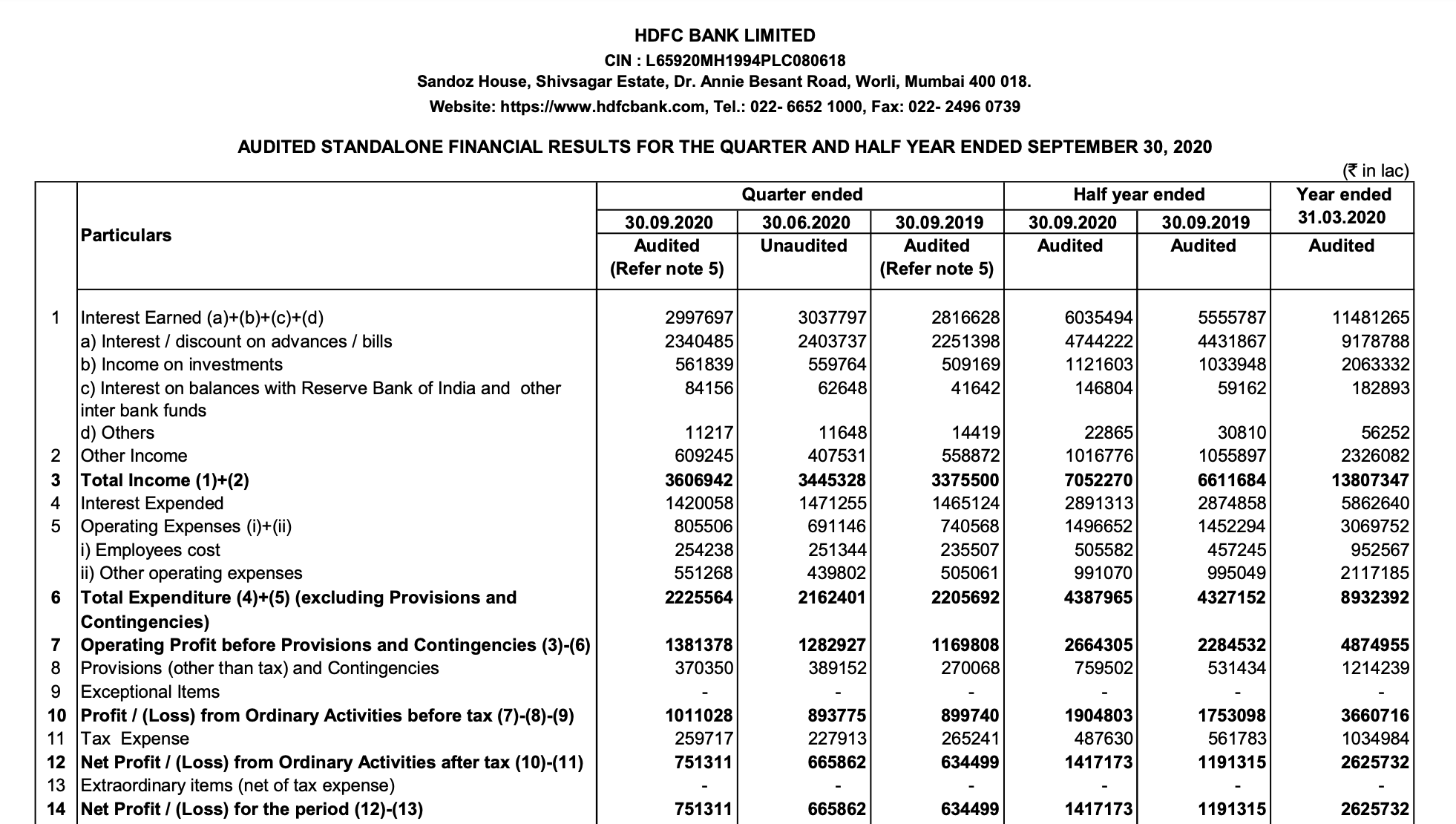

- Look at the same segment revenues and ROAs for HDFC bank (the gold standard in banking). I Quote from Q2-FY21 disclosure:

Look at the Retail banking H1-FY20 vs H1-FY21 Income from operations (PBT basis). It was 7090cr on an asset base of 4,60,000cr in H1-FY20. PTRoA* of 1.54%. It is 4875cr on an Asset base of 4,77,000cr in H1-FY21. This is a PTRoA of 1.02%. Even for HDFCB, H1 has proved to be difficult. It should not surprise us that IDFCFB’s PTRoA has worsened in H1-FY21 for retail segment (the segment which I’m watching most closely). It is -839/61830 = -1.35% vs -489/51337 = -0.95% in H1FY20. This is despite the aggressive branch expansion. - CEO has repeatedly talked about the Cost to Income ratio being lowered. Currently it is very high. as the bank scales up, same branches bring more CASA and loans and fee based income, as same bank launches credit card and brings in Fee based income, the Cost-to-income ratio should go down and hence improve the segmental PTRoA. This remains a key monitorable. But I would not expect it to improve any time soon. Depending on how the Covid-19 pandemic pans out, it could easily take 1-2 years for the segmental PTRoA to become > 1% and hence for Retail to start contributing significant profits.

*PTRoA (A term coined by Me): Pre-tax Return on Assets

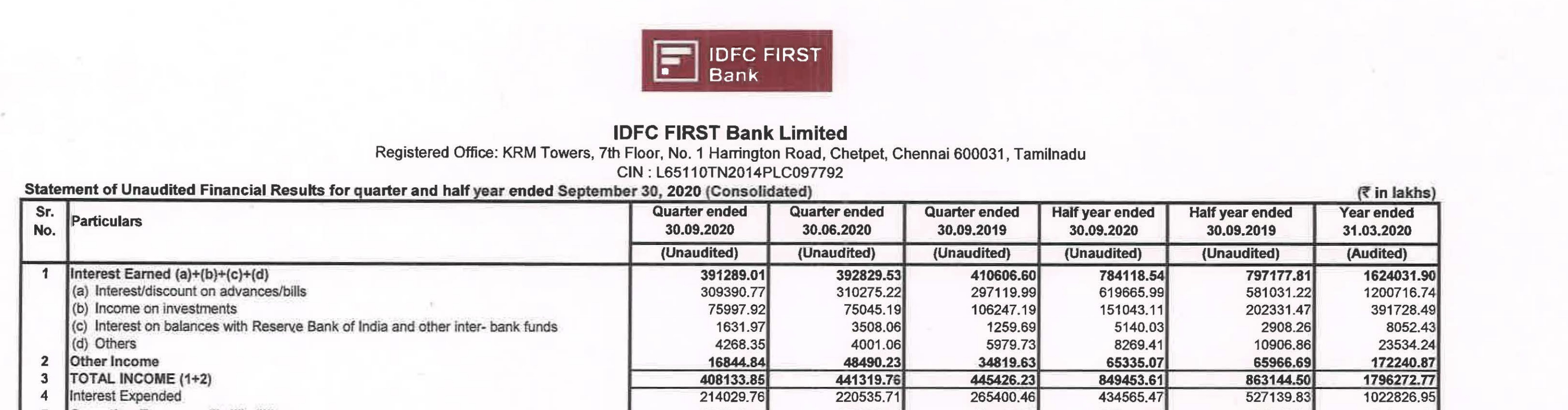

Sorry, I don’t know what you’re saying. Interest outflow has reduced significantly. Have a look at row 4 below:

Also, have a look at data I had posted before:

This was roughly 10% in FY20. It is now at a run-rate of 2140*4/107000 = 8%. So interest expended has come down from 10% to 8% in current quarter.

4 Likes

What happened to the moratorium book. Answers appreciated

Please see my first post on the subject. Specifically this part. :

You can see this tweet too: https://twitter.com/JstInvestments/status/1322577421225193472?s=19

2 Likes

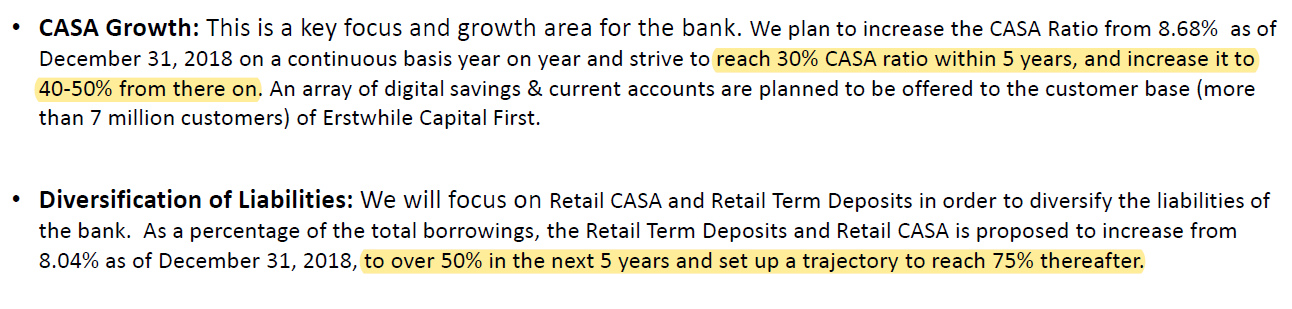

Great summary; VV has once again shown his execution capabilities by far surpassing his 60 month targets in just 21 months (see below). The rest of the 5 year goals will hopefully be achieved soon as well; the retail book is already above 60% (vs a 5 year target of 70%) and NIM’s are close to 5%. Going forward as the C/I ratio comes down to the targeted 50-55% we should see an exponential increase in profitability.

6 Likes

Thanks for the summary, Sahil!

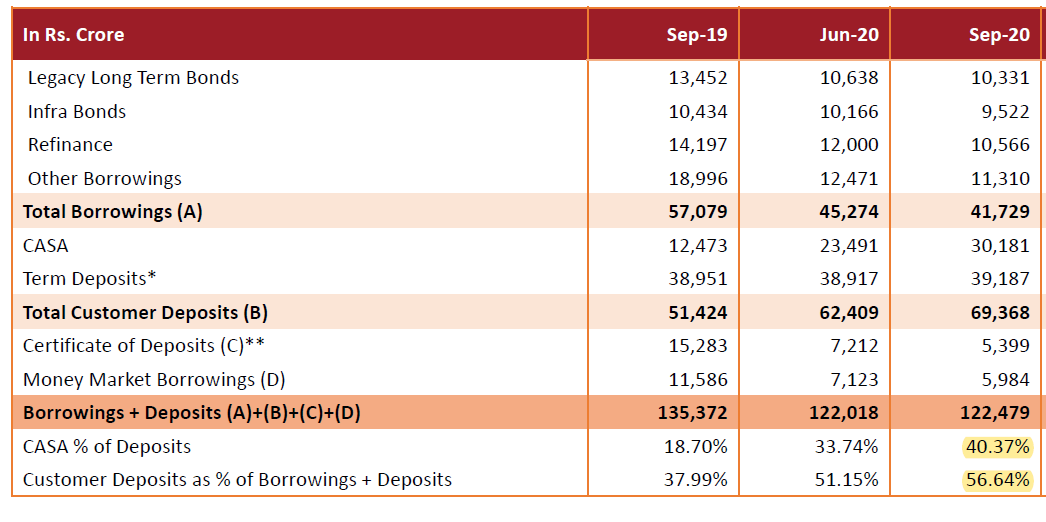

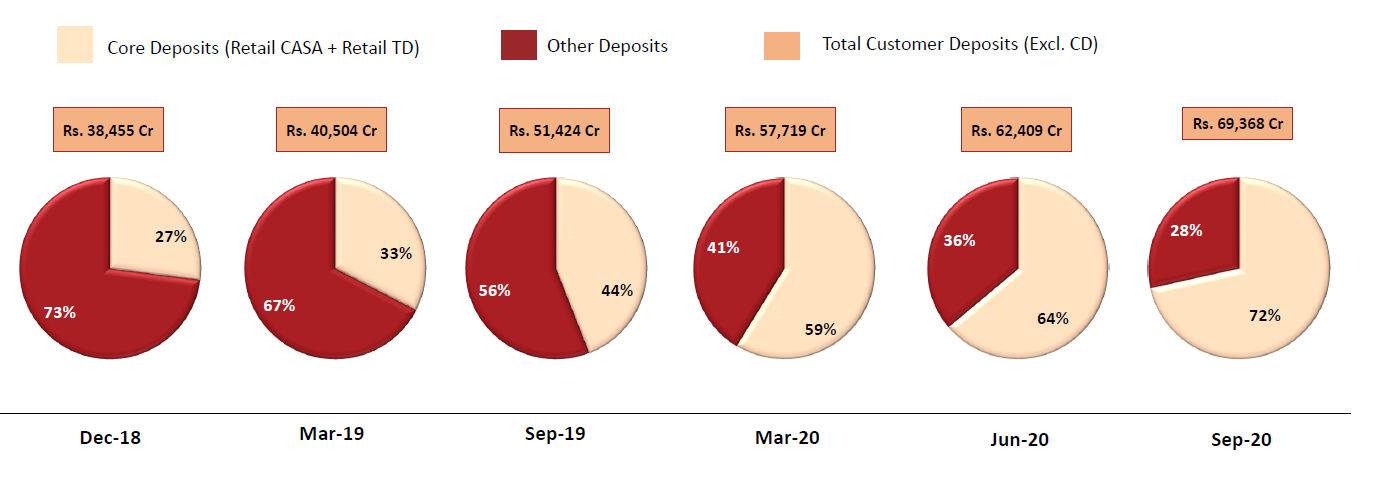

The QoQ growth in CASA is particularly impressive- 6700 crores. I think the new advertising campaigns they’ve been running throughout this lockdown have a role to play here. While advertising campaigns may not be as effective for the wholesale banking business, they definitely help the retail side and are important for increasing the CASA. These investments in building the ‘IDFC First Bank’ brand would pay off over a longer time horizon though.

2 Likes

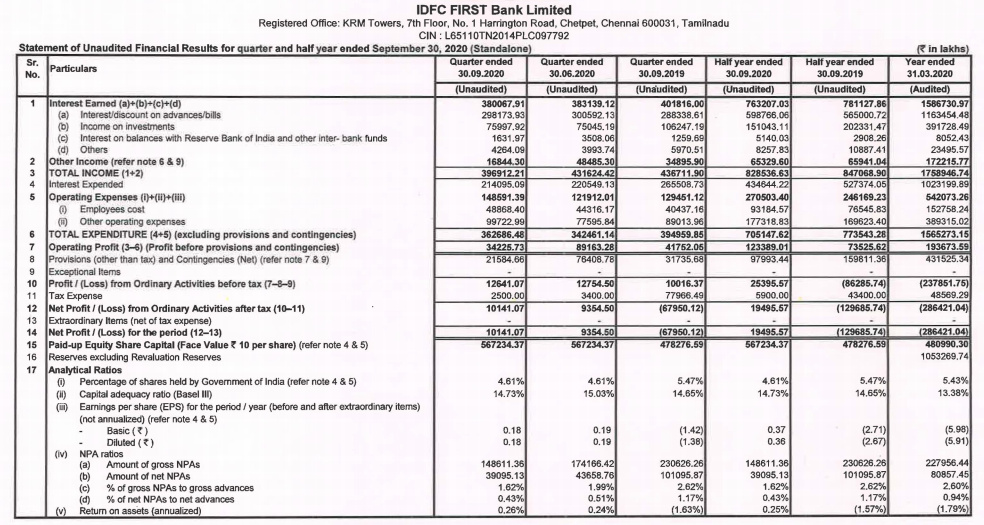

Operating Profit has significantly reduced… down from 89163 to 34225

That is a big fall. (and this is highlighted nowhere in the presentation)

The reason is clear…

a. Lower Income (431624 vs 396912)

b. Increased Operational Exp (121912 Vs 148591)

Employees cost and Other operating expense both have increase this quarter. This is due to the scorching pace at which branches have been increased. This is a risk.

(This too is not even mentioned in the presentation)

I understand, a presentation is meant to highlight (gaslight) the good aspects.

Yet, the management managed to post a profit similar to last Q’s because of the switcheroo it did in the provisioning. But, that isnt convincing.

I am just talking frankly, to make this research thread on IDFCFIRST even more resourceful.

In the Qs to come we need to see these two parameters (‘a’ and ‘b’) improving.

Ever since the results, the stock price of the bank has been underperforming the general market. It wasn’t so before.

Amit

10 Likes

I think you can agree that long term investors should not think of this as being a negative. A large part of value investing is finding “Unseen value”. If it is a consensus investment, it’s difficult to make money. We can try to reason about stock underperformance, or, if we understand the direction of the business and are comfortable with the direction, we can load up. I did just that. And i plan to do more of it. “Market is spooked by the high provisions bank is creating” some news Anchors (CNBC Awaaz) say, that may be true. But would an investor rather have a bank which creates provisions up front in anticipation of bad times, or which fails to recognize and anticipate bad days and creates provisions post facto? All good institutions are creating high provisions for rainy days in Q4-FY21 and beyond. Look at Bajaj Finance. Look at HDFC bank.

True for HDFC bank

True for HDFC Bank

They’re actually creating extremely high provisions, which is a huge positive in my mind. By Q4 they will easily provision for 3-3.5% of the loan book. Specially for banking companies, trust in management is extremely important and an individual investors choice. If one does not trust, one is free to invest in other opportunities. I do trust based on my research(I don’t recommend others to follow me, only to make their own decisions based on data).

I think all investors would agree these parameters need to improve. The question is about time frames and investment horizons. I am ok if they don’t improve for a year and then go up sustainably.

I appreciate you playing devil’s advocate ![]() , and I have thought about these issues as well. However, these aren’t strong enough to reduce ownership or dent the investment thesis, for me personally.

, and I have thought about these issues as well. However, these aren’t strong enough to reduce ownership or dent the investment thesis, for me personally.

12 Likes

I do realize that as long term investors we should focus on the business and not much on the stock price really. But post the results (which I think was good), the stock has been grossly underperforming the Bank Nifty. There is surely something that the market knows or sees something as a potential threat for the business. What can be it?

1 Like

IDFC is a bank which would not be making any profits(sizeable) for atleast the next 2 years.

Given this background the market cannot really re rate it specially given the valuations a bank like Axis trades at.

Hence the under performance. Only outliers like ICICI are surfing ahead(that too based on optical profits declared and a strong subsidiary base to sell )

3 Likes

My two cents on this quarter results:

- Bank has smartly managed the provisions. Taking 50% of VI provisions and adding it to COVID provisions. I don’t see any -ve on this move, as VI never defaulted and after AGR VI is doing decent business.

- I think from here they are going to increase the loan book as their retail CASA is now at 40% .

- I am happy that they are expanding their branches especially in rural areas , where others are not operating.

- I personally feel , management is very smart and making good moves.

- They are partnering with various fintech’s to lend.

They are ticking all the right boxes and happy that bank is in growing with transparency

6 Likes

Results look ok,

-

CASA & TD - Massive. Not just in % terms even in absolute terms.

-

First time we are seeing green shoots in foreseeable future i.e. by march 2020, granular book: Wholesale book will be 70:30. credit cost being peaked out.

3.PPOP[Bond repricing, trading gains] is enough to cover the stress and I don’t see book value erosion.

we still got some time to accumulate more of this stuff at book value or below.

1 Like

Sorry, how do you conclude that the bank won’t be making significant profits for 2 years? From what I can see, the profits are currently hurt by the covid provisioning. If that ends by March, shouldn’t the profits increase significantly from that point on even with a constant loan book but increasing yield due to retail composition? Add to that an increasing loan book, and I would imagine profits should be healthy quite soon.

Happy to be corrected.

1 Like

The bank looks expensive from earnings point of view.

Last 3Qs earnings is 0.16+0.18+0.19

(before that it was posting big losses)

Lets assume the best case scenario of TTM Earnings for Q3 ending as 0.80

Then PE comes to 37 for CMP of 30. This is very expensive for a bank which doesnt look like will be posting hefty profits anytime soon.

I am guessing that the market is probably seeing this. Which is why while Bank Nifty rallied 1600 points in last three days… IDFCFirst has not moved at all (slightly negatively actually).

In the same breathe, banks are often valued on PBV, on basis of which the bank is cheap at CMP.

1 Like

Valuations should be done on the forward earnings and I don’t think their past results show the correct earning potential. Although valuation lies in the eyes of the beholder, but in my opinion the correct way would be to look at their loan book, gross NPA, NII growth, future operating expenses, future return on assets and then value the company (There would be other parameters as well).

I wish valuations could have been this simpler where you just check the current P/E of the company and compare it with peers.![]()

2 Likes

Since, Bank will have :

-

Continued high provisions due to covid and legacy issues. Also capital first has also always had high provisions and GNPA of 2%.

-

High operational costs will continue for the foreseeable future.

-

High cost of deposits to continue as well.

- Continued high provisions due to covid and legacy issues. Also capital first has also always had high provisions and GNPA of 2%.

I think 2% GNPA is industry best standard in India. HDFC Bank and HDFC have similar long term ratios. Legacy issues exist, but to a much lesser extent with the wholesale book much smaller. 12k cr infra book needs to be wound down soon and is a worry.

- High operational costs will continue for the foreseeable future.

This is true due to branch expansion. It is investment in the long term, but will be a short term drag.

- High cost of deposits to continue as well.

I don’t think this is an issue, given the well publicized story of the business model. Industry high NIM at 4.5 lays any concerns on this ground to rest, imo.

There’s no doubt that IDFCB isn’t HDFC bank today, and does have risks. But there is a significant value investment opportunity, to ride the journey from 1 P/BV to hopefully 4-5 P/BV in 5 years. It remains a bet on the execution.

5 Likes

Interesting discussion guys. I have one question: Why have the NIM increased only by 4 bps (4.53 to 4.57) from last quarter while the CASA ratio improved so significantly and retail loan book has also increased? Earlier it had been growing by 40-50 bps every quarter

Does this mean their gross yield has not grown that significantly or de-grown?

1 Like

I’ll try to venture a theory as to why NIM might’ve stagnated.

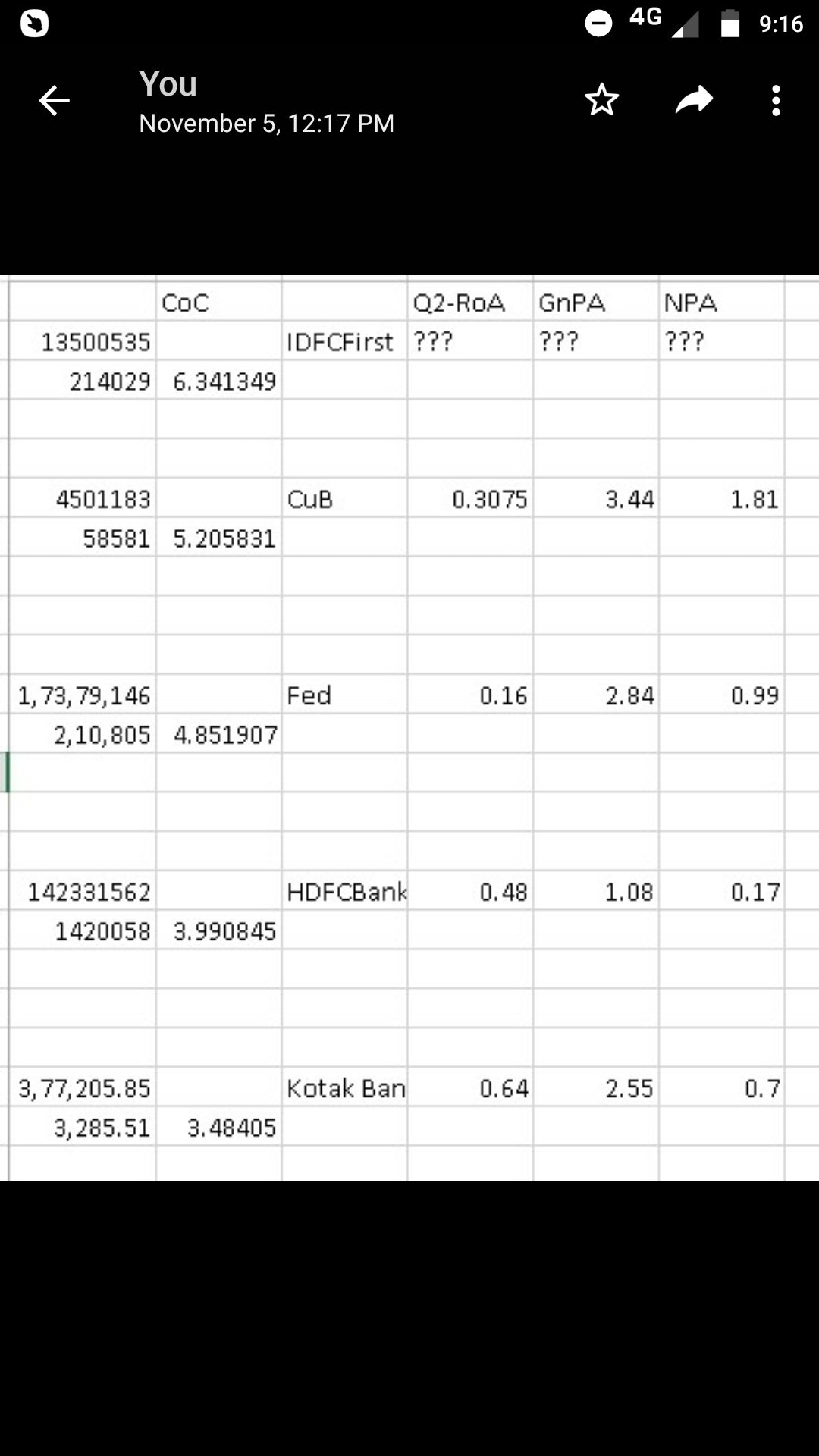

This table shows Cost of Capital, which is highest for IDFCfirst. I’ve crudely calculated it, by simply dividing the interest Expense with the Liabilities. And looking at the other Banks CoC and their RoAs, it all adds up.

High CoC cuts into margins.

As yet 7% is the best and major source of funds for the bank. However, there is hope. CuB and Federal bank hv CoC around 5%. So, IDFCFIRST might also hv that much room. But, in the distant future.

The good part is the bank has not compromised it’s asset quality for higher earnings, by giving risky retail loans. Now is the worst time to do that. There is competition from other players so margins cannot grow beyond a point. There is plenty of room on CoC side and Operational Expense side. But, these do not ook like will reduce anytime soon.

VV aims for 1lakh Cr Casa, has reached only half way. And many more branches still to open. So, NIM isn’t going to improve a whole lot. The only play left is reducing high cost wholesale funds and increasing lower cost Casa at 7%.

2 Likes

IDFCF bank management was being conservative and took provisions even when it was not mandatory. Sometimes, they have taken extra provisions for even standard account. It makes sense to show provisions when supported by cash flows. So, if account is not paying and making loss, then it good to show provisions which would reduce the profits. However, account is still paying and may continue to pay. So, whats the benefit of being conservative in terms of cash flow (and not the future non cash entries such as provisions and NPA)?

For example, I thought of following two possible positives:

- Provisions will reduce the profit and will result in to low tax. This will reduce tax outflow and will save the cash. This cash saved will be used for disbursements.

- Provisions will reduce the loan values. So, money that should be kept aside for loans amount (such as any ruglatory requirement) will be saved. Again this saved amout will add to disbursements.

So, I just want to know what is exact cash effect for being conservative?

4 Likes