This can be a silly question but:

Non-food credit for every bank is either at the pre-covid level or has fallen slightly. In the same period, the deposit amount has gone up considerably. No increase in lending means no increase in interest income but still the obligation to give interest on the deposits has meant that large banks have cut down on the savings rate.

However, during this time, IDFC Bank is still offering 7% savings rate and the deposits are ever-increasing.

With very marginal profits and during these difficult times for the bank, I wonder how is the bank managing this. Any thoughts and opinions are welcome

Please go through the latest AR and AGM video to understand how and why the bank is easily able to offer 7% interest on SA. They have explained it quite well and in detail.

This is in aggregate of all Banks, though there will be shifts from one bank to another even while the overall credit outstanding of all banks in aggregate has declined (till 25 Sep when RBI data was available)

While IDFC First may offer higher deposit rates, though not sure if it still does (Bank Interest Rates 2023 | IDFC FIRST Bank )

it’s yield on loans is much higher at about 13-14% (https://www.idfcfirstbank.com/content/dam/IDFCFirstBank/PDF/IDFC-FIRST-Bank-Investor-Presentation-Q1-FY21.pdf)

Some finer points to note are that while the headline FD etc may say 7%, it will pertain to a certain tenor, and a good part of incremental CASA may not be that, and could be lower on a blended basis. The marginal cost of funds from 032020 quarter to 062020 quarter has dropped by about 40 bps while retail deposits have done up, indicating the same. These are rough calculations based on Q1 2021 presentation.

Disc: no investments.

This is not the case any more (since September 15). The headline number is 6% (highest) for deposits. For savings account the rate is 7%. As of right now it is more beneficial to keep money in savings account as compared to deposits.

Thanks @sahil_vi I mistakenly mixed up FD with Savings account. The website also says it is only for digital savings account, which is a low cost branchless a/c (https://www.idfcfirstbank.com/content/idfcsecure/en/open-savings-account-online.html ). Nevertheless the spreads between yield on advances and cost of liabilities is wide enough to absorb the high rates, and possibly management feels the compression in NIMs is worth this high rates of retail savings.

Which then leads me to infer then that management is raring to oust wholesale liabilities and replace it with retail deposits from digitally savvy customers, likely to be young and hence longer lifetime value. That makes it really a bank long term and less of a Financial Institution that it once was.

The investment thesis in IDFC First bank rests on superimposing the retail lending model of CapF with the retail liabilities franchise of a bank (Retail CASA + Deposits). One of the critical aspects here is that of credit risks, and how the company manages its credit risks. I analyze the Gross Yields, NIMs, Provisions+Write-Offs, NIM-(Provisions+WriteOffs) for IDFC First bank and Bajaj Finance. All data is taken from their Annual Reports. Data for IDFC First bank uses Capital First data from 2013 to 2018. Hence, the AUMs will be much smaller than the 2019 AUM (blended book of IDFC bank and Capital First).

Raw Data for Bajaj Finance:

| Field/Year | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 |

|---|---|---|---|---|---|---|---|---|

| Provisions + Write-offs (cr) | 3929 | 1501 | 1045 | 803 | 543 | 384 | 258 | 182 |

| Total AUM (cr) | 147153 | 110000 | 84033 | 60023 | 44229 | 32410 | 24061 | 17517 |

| Interest Earned (cr) | 22970 | 16348 | 13442 | 9966 | 7304 | 5381 | 4031 | 3092 |

| Interest Expended (cr) | 9475 | 6623 | 4634 | 3803 | 2926 | 2248 | 1573 | 1205 |

| NIM | 0.091 | 0.088 | 0.147 | 0.102 | 0.098 | 0.096 | 0.102 | 0.107 |

| Gross Yield (cr) | 0.156 | 0.148 | 0.159 | 0.166 | 0.165 | 0.166 | 0.167 | 0.176 |

| Provisions + Write-offs / AUM (cr) | 0.026 | 0.013 | 0.012 | 0.013 | 0.012 | 0.011 | 0.01 | 0.01 |

| NIM - Provisions / AUM | 0.065 | 0.074 | 0.135 | 0.089 | 0.086 | 0.084 | 0.091 | 0.097 |

Raw Data for IDFC First bank:

| Field/Year | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 |

|---|---|---|---|---|---|---|---|---|

| Provisions + Write-offs (cr) | 4800 | 195 | 642 | 453 | 236 | 105 | 49 | 22 |

| Total AUM (cr) | 107000 | 110000 | 26997 | 19824 | 16041 | 11975 | 9579 | 7510 |

| Interest Earned (cr) | 15867 | 11948 | 3770 | 2772 | 1882 | 1424 | 1053 | 800 |

| Interest Expended (cr) | 10000 | 8749 | 1382 | 1160 | 897 | 787 | 647 | 483 |

| NIM | 0.054 | 0.029 | 0.088 | 0.081 | 0.061 | 0.053 | 0.042 | 0.042 |

| Gross Yield (cr) | 0.148 | 0.108 | 0.139 | 0.139 | 0.117 | 0.118 | 0.1099 | 0.106 |

| Provisions + Write-offs / AUM (cr) | 0.044 | 0.0017 | 0.023 | 0.022 | 0.0147 | 0.0087 | 0.0051 | 0.0029 |

| NIM - Provisions / AUM | 0.0099 | 0.027 | 0.064 | 0.058 | 0.046 | 0.044 | 0.037 | 0.039 |

Some observations from this data + trends:

- Bajaj finance’s provisions + Write offs (net credit losses) have been inching up over the years. From ~1% in 2013 to ~1.3% in 2019 and 2.6% in 2020. In the meanwhile their NIMs have been coming down, as they have expanded the assets to lower yielding ones, over the years. From ~10.5-11% in 2013 to ~9% in 2020. Hence, their (NIM - Net credit losses) has shrunk from ~10% in 2013 to ~6.5% in 2020.

- The merger happened in 2019. Capital first’s NIMs expanded sharply from 4% in 2013 to ~9% in 2018. Post merger, the NIMs came down due to large low-yielding infra book of IDFC bank. NIMs have started to expand again in 2020, reaching 5.5% in 2020. Annualized NIM in Q1-FY21 is 6% (source Q1-FY21 results). The Gross yields have expanded from 10.5% in 2013 to ~15% in 2020. This is despite having a large portion of loan book in infra and corporate loans. When the infra book is driven down to 0, the gross yields would expand even more. The Net Credit Losses have expanded from < 0.5% in 2013 to ~2.5% pre-merger (2018). However, the NIMs have expanded much faster, meaning that by taking incremental risks, they created higher values. (Lend to riskier segments at higher rates, resulting in higher write offs, but price the product appropriately to absorb the credit losses). The NCLs have been rather odd in last 2 years due to several one-offs (including a few tax related ones). The NCLs will be a key monitorable going forward, specially the relation to NIMs. As long as NCLs expand slower than NIMs, the bank is creating value. It’ll be interesting to observe how the NCLs turn out after the book goes out of moratorium period. One thing which should help the NIMs are the falling Deposit rates for TD (which are still one of highest in the industry by a reasonable margin).

PS: I’ve compared IDFC First to Bajaj finance because both have a very similar lending profile. Also because first 6 years of data is for Capital First which was also an NBFC.

That’s really useful thanks.

Don’t you think though that NIMs expanding faster than Credit loss is not possible in the given scenario we are in.

Rbi in its financial stability report expects 8% GNPAs for private banks as a whole. Is IDFC First also not expected to have those levels as well since it has a weaker book.

Let’s see what the management guides on the Month End call.

In the short term (1-2 years) it’s very hard to predict what will happen. RBI has released guidelines for restructuring precisely to ensure that otherwise standard accounts hit by covid impact can continue to be standard while restructuring for lowered cashflows. I do not count restructured accounts as npa because rbi does not. Would there still be > 8% GNPA ? that is certainly possible.

My investment thesis is for a period of 5 years at least. Would we expect the npa situation to normalise in 1-2 years ? Probably yes. The nim expansion in excess of NCL expansion is in that context. Every percent drop in deposit rates allows idfc more headroom for bad assets. The recent reduction in FD rates is a welcome step in that sense.

New Ad

Any corporate embedd it to the core - real growth in indian industry… as many areas we lack customer first attitude…

Speech by V Vaidyanathan:

Rating Update

It’s a non-event for the bank.

CARE withdrew the rating as there is no pending short term outstanding loan on IDFCFB books. Hence, having a rating doesn’t make sense.

We can look at the way CARE has changed the Long Term rating for the bank from AA+ Stable to AA+ Negative to AA Stable.

Thanks for posting the results. They’re quite good.

Key highlights for me:

- The CASA has grown from 23,500cr in Jun’20 to 30,200 cr in Sep’20. That is a QoQ growth of 29%.

- The Retail CASA+TD (In IDFCFB’s case, Retail TD is a better source of funds and hence its important to track Retail CASA+TD) grew from 39,900 cr to 49,600cr. Growth of 24% QoQ.

- This growing CASA is reflecting in the interest outgo and the Bottomline. Interest expended in Q2-FY21 is 2130 cr (Run-rate of 8500 cr) while it was 10,300cr in FY20. The 2,000 cr increase in PPOP is very healthy.

- NIM at 4.57% in Q2-FY21 vs 4.53% in Q1-FY21 and 3.43% in Q2-Fy20.

- Out of the 1600cr provisions for Vodafone Idea, 800cr was reversed and added to Covid-related provisions. Total provisions for Covid-related is now 2,000 cr which is ~2.21% of the standard advances.

- The bank provided complete reasoning for reversing 50% of the VI provisions. Payment of AGR dues have been staggered and no immediate payment for 2 years. Company has obtained board approval for 25k cr of fundraising. Company has met all borrowing obligations including 2800cr of NCDs in July 2020. Following SC verdict on AGR dues Company NCDs are now trading in the bond markets. Bank continues to hold 800cr provisions (25% of exposure) for VI exposure.

- Bank created additional provisions of ~600cr in this quarter for Covid-19 related contingencies. With this (600 until now, 600 in this quarter and 800 from VI provisions) bank has 2,000cr of Covid-19 related contingency provisions.

- Dependency on CoD is coming down. From 7200 in Jun’20 to 5400cr in Sep’20 (This was 15,200cr in Sep’19).

- 523 branches and 509 ATMs (503 branches 417 ATMs in Jun’20).

- Retail loan book increased from 56000 cr in Jun’20 to 60000cr in Sep’20 (7% QoQ growth).

- Infra loan book continues to reduce from 13400cr in Jun’20 to 12500cr in Sep’20.

- Context: Supreme court in its Aug’20 order asked banks to not categorize any account as NPA until further ruling. GNPA as on Jun’20 was 1.99%. Reduced to 1.62% as on Sep’20 (1.87% without SC order effect). NNPA is around ~0.5% (Jun, Sep, with and without SC order effect).

- PCR (Provision coverage ratio) is stable at 74% of NPA amounts (was 75% in Jun’20 and 56% in Sep’19).

- The stressed asset pool self-identified by the bank also shrunk from 3500 cr in Sep’19 to 2700cr in Sep’20. Note that these are not NPA accounts. Still, bank has PCR of 48% for this part of loan book.

- At a gross level the retail disbursals have reached 74% of the disbursal levels for the same

quarter last year with the urban consumption based retail products touching around 90%

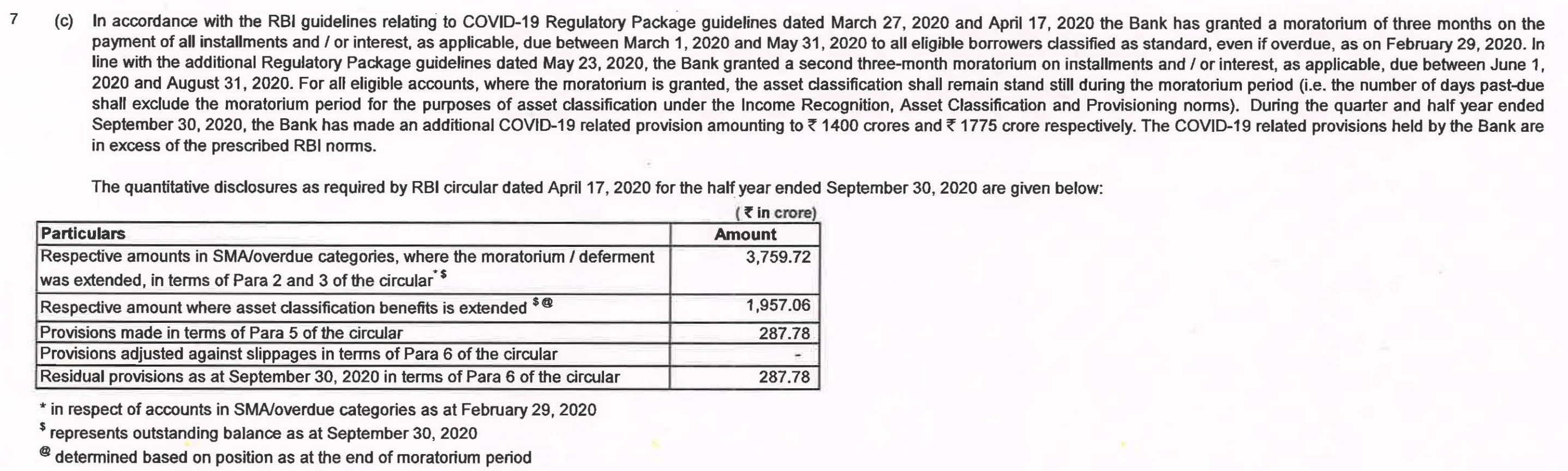

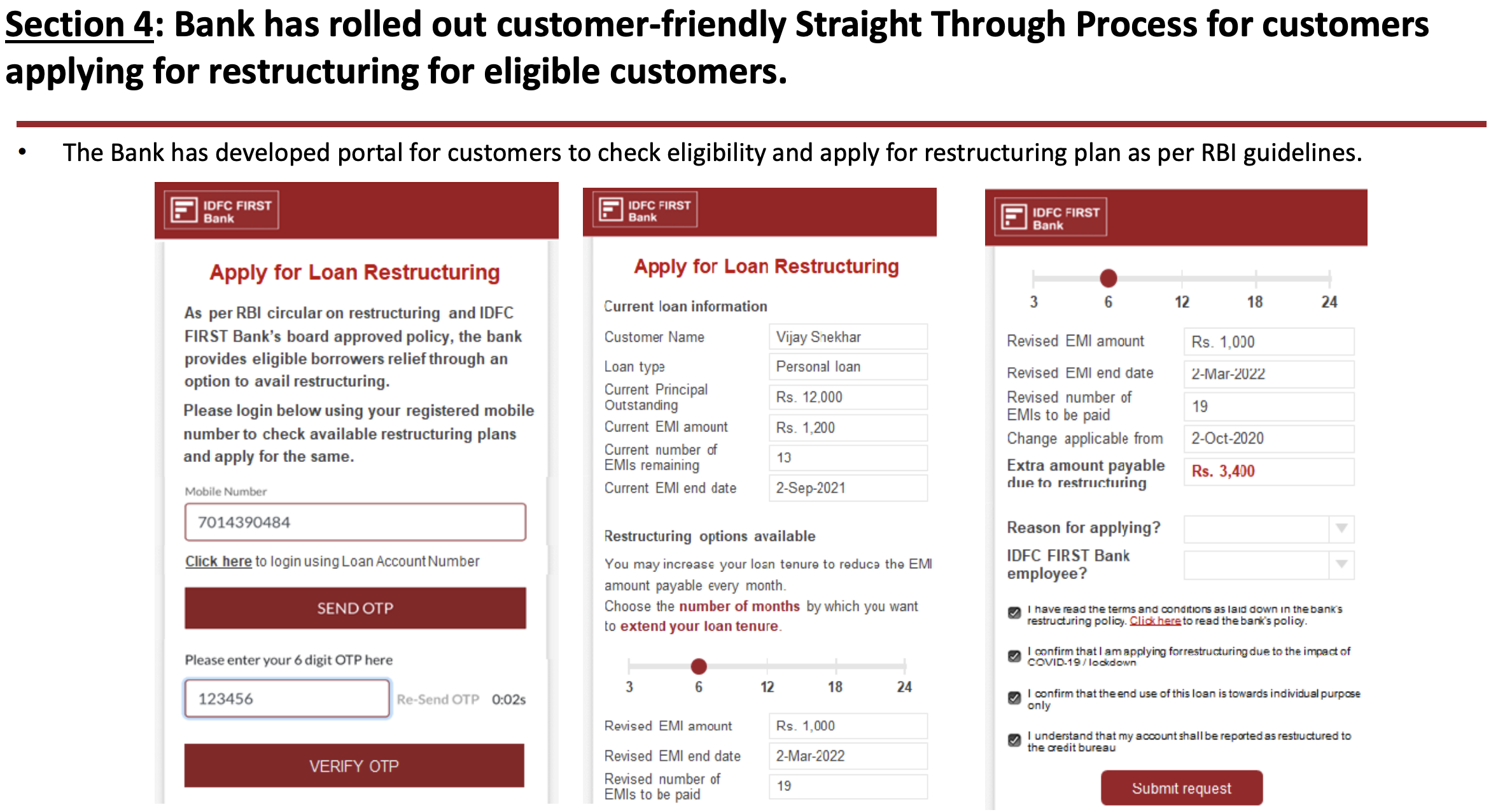

of the disbursal levels for same quarter last year. - During the quarter ended on September 30, 2020, the RBI announced the restructuring plan for the eligible customers with loan ticket sizes below Rs. 2 crore. The Bank has formed suitable policies to provide restructuring plans to eligible customers. The eligible customers can apply for such plan till December 31, 2020. As of September 30, 2020, the Bank has not received any sizeable request for restructuring.

- CEO’s message: “With the liability side firmly addressed, you will see growth in the total loan book from Q3FY21 and onwards. I am further happy to inform you that the collection performance on retail

loans have improved sharply after the lockdown has been lifted, and in fact are much stronger

than earlier anticipated”. - This is an important point related to the loan book under moratorium. So adding it verbatim. Also here is the link to the relevant RBI circular:

My Thoughts: Bank is performing well. They’ve been profitable for 3 quarters now, this is despite creating ~2.21% of provisions for Covid-19 related contingencies. The amazing CASA franchise growth is allowing the bank to lower costs and hence boost profitability (it was only last year that big Investment houses were talking about how difficult it would be for IDFCFB to grow it’s CASA base). Next 1 year would be very interesting to observe the bank and its results. Sharp spikes in NPAs, or Provisions+Write-offs would be a possible negative. Growth in loan book, further reduction in borrowing costs and retailization of assets and liabilities remain continuing positives to look forward to.

Disc: Invested. This is not a buy or sell recommendation.

Agree with you , in current context of looming credit crisis, this act should be seen as a positive.

In the Segment results, it looks like the bank is making profit only from Treasury , both in Wholesale and Retail segment the bank is loosing money.