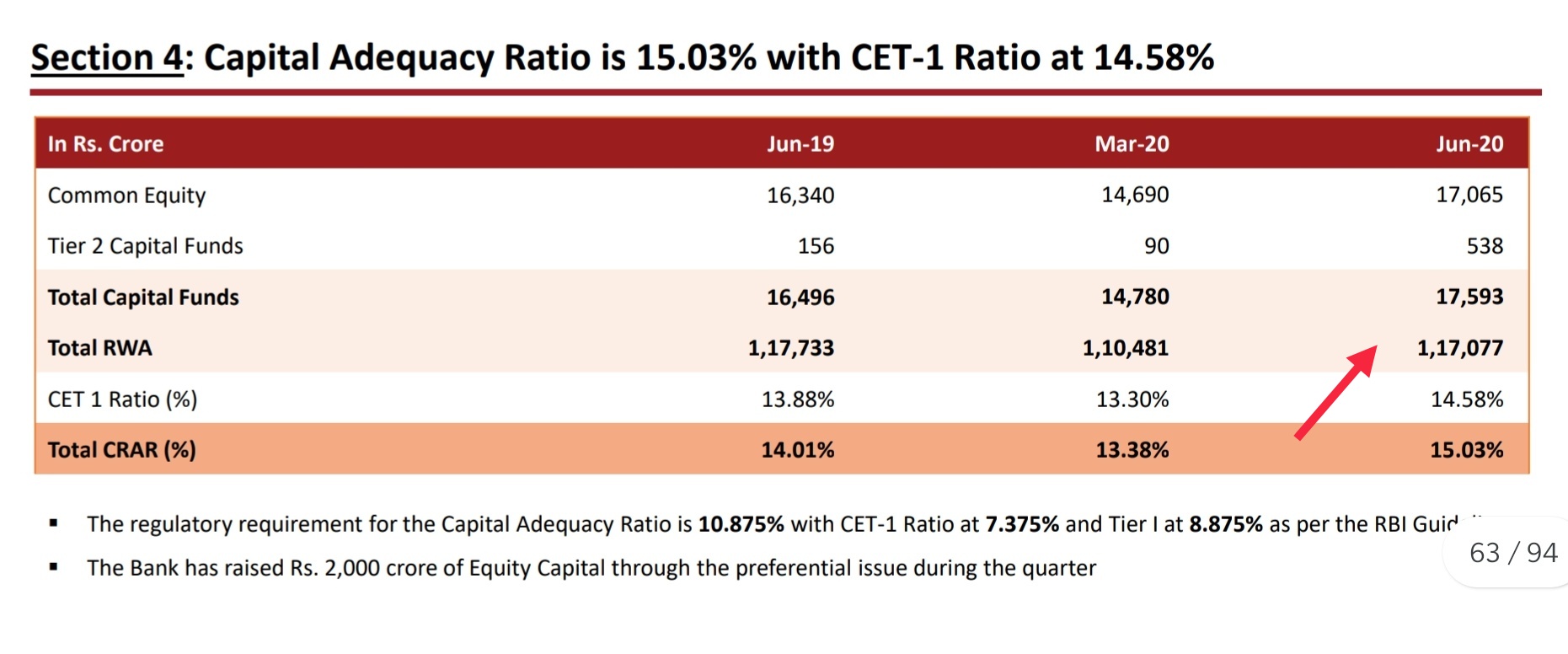

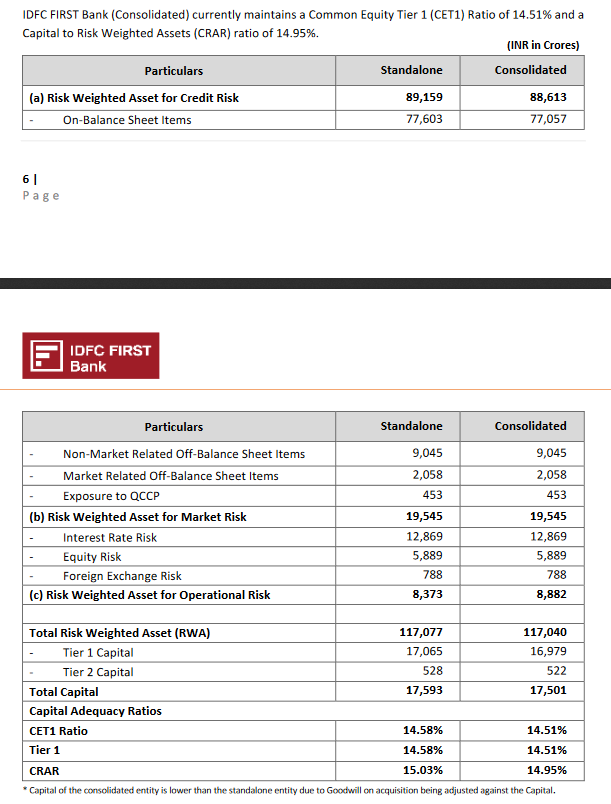

Can someone explain, how has RWA gone up in June’20 as total book ( mainly risker assets have gone down ) ?

3 Likes

True. I echo with you @sahil_vi. One of my friend availed moratorium, but bank people called him and insisted him to pay. He started paying from last month. People had misconception that govt or SC will provide some kind of relief (read as wavier) with interest, so most of them availed moratorium in first place. I hope once the moratorium ends people start paying EMIs.

1 Like

You are missing the point bro. Their business model is different from hdfc bank or kotak. You can’t compare . Moratorium was I guess 45 percent in Q4.

I don’t think it’s right to compare hdfc bank , icici or kotak with IDFC first bank.

2 Likes

it is double edged sword… availing Moratorium is customer right. the amount of loan may not be big in case of IDFC and no of customers also lesser compared to HDFC or Kotak. so IDFC can take a chance considering the growth. If you are opting for Moratorium, it is not that you no need to pay the EMI, but you need to pay with more interest for the time. SO, for any small ticket loans IDFC is having, it may not be big risk. Same could not be opted for HDFC/Kotak because thier base is large… oneway being small is good at this point… as they can be dynamic and grab opportunity.

Disclaimer: I am invested in the stock, having interest in future investing too… My views are biased

3 Likes

Ok my more hyperbolic post got hidden… so I’m just going to post this from page 19 of the investor presentation. Vaidhyanathan Addresses the moratorium issue mentioned above. Cheers.

Mr. V Vaidyanathan, Managing Director and CEO, IDFC FIRST Bank, said, “We are happy to

inform that we continue to progress well on all parameters as per the guidance provided for the

bank. Further, we have liberally provided moratorium to customers who sought it, and our

moratorium was about 45% last quarter. This has reduced to 28% now, which we expect to fall

below 10% by August 31, 2020 based on the strong improving trend in collections we are

experiencing.”

1 Like

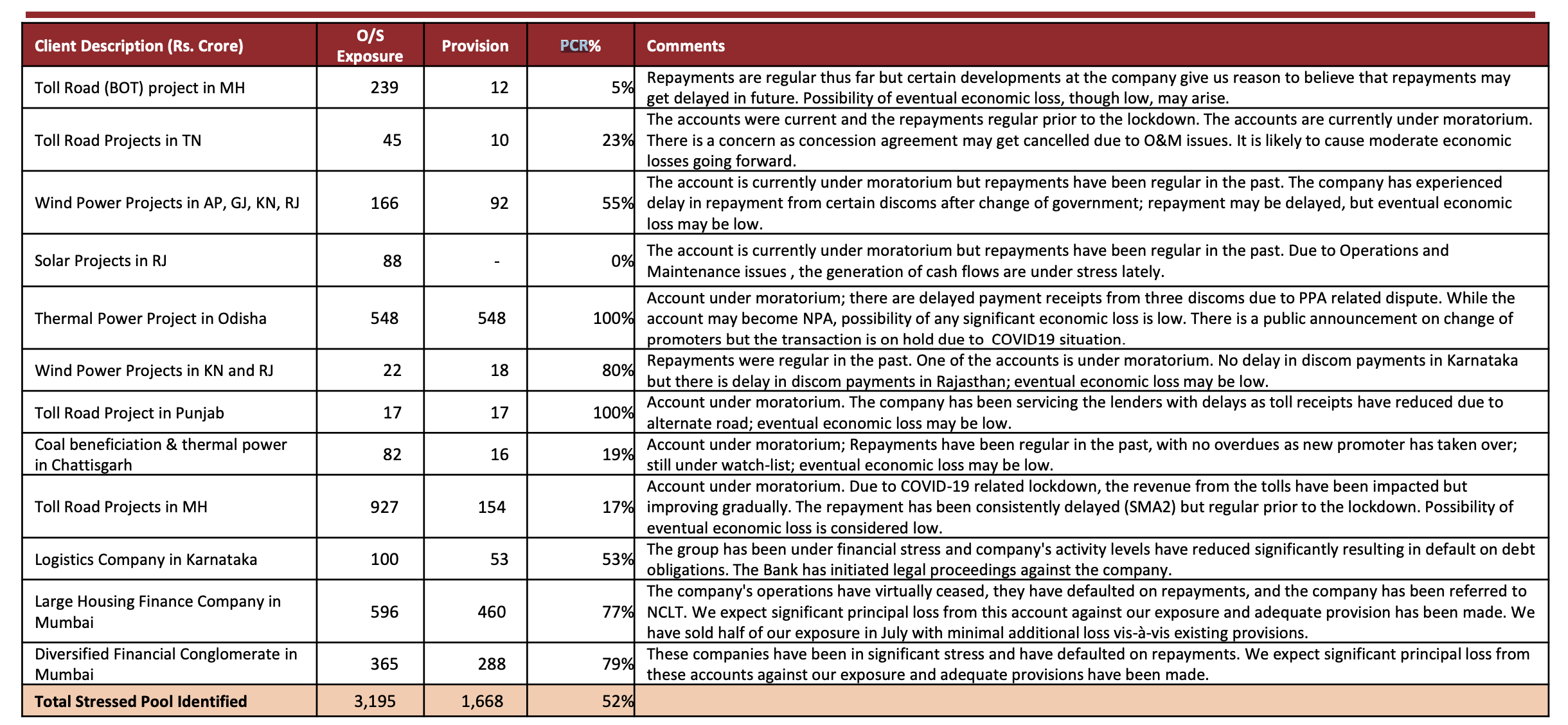

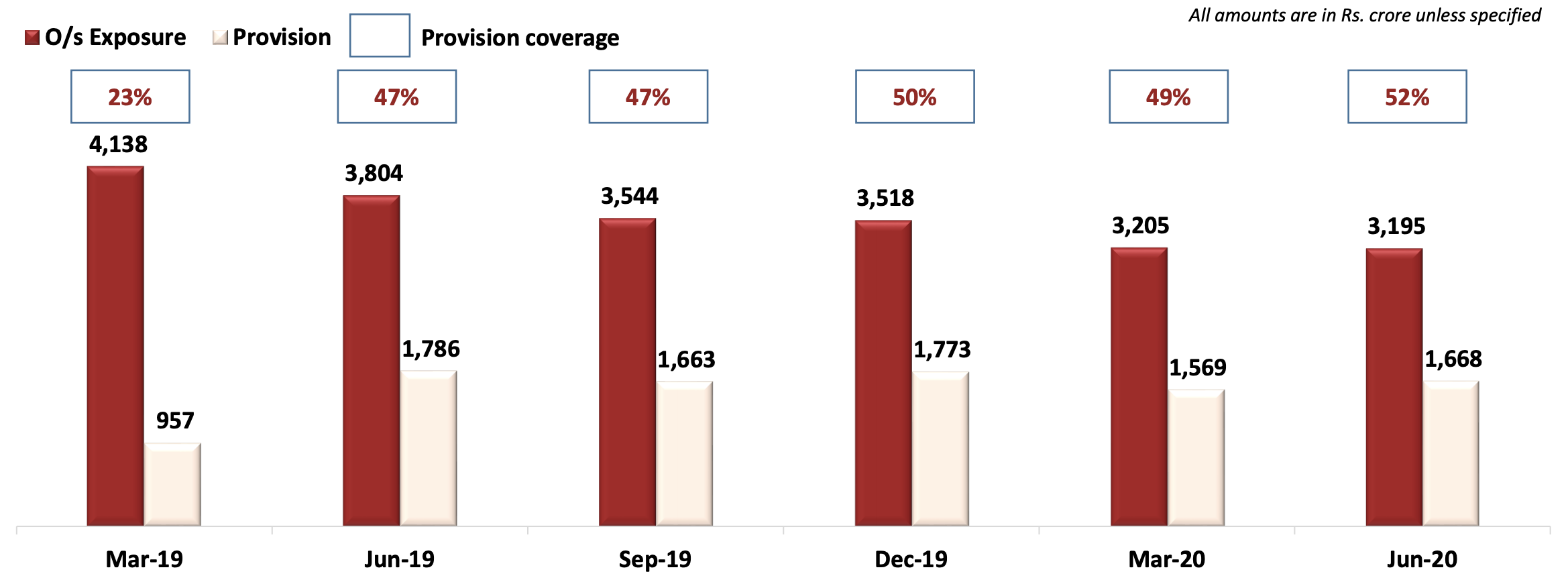

To add to this list:

- Bank has made fresh provisions of 375cr for covid-related stressed accounts in this quarter.

- Apart from NPA accounts, Bank has proactively identified certain accounts, which are

standard on the books but are assessed to be stressed, and taken provisions for the same proactively. Details:

- The stressed assets as shown in last bullet (these are not NPAs yet) have gone down:

- The bank has liberally provided moratorium to customers who sought it, and their

moratorium was about 45% last quarter. This has reduced to 28% now, which they expect to fall

below 10% by August 31, 2020 based on the strong improving trend in collections they are

experiencing. - Improved Cost to Income Ratio (excl. Trading gains): 68.72% for Q1 FY21 as compared to 78.06% in Q1 FY20 and compared to 76.54% in Q4 FY20.

Sahil: To my mind, this is one of the key/critical improvements. The CIR improvement is critical for improved ROE/ROA and earnings. - Bank’s Gross NPA reduced sequentially from 2.60% as of March 31, 2020 to 1.99% as of June 30, 2020

- Bank Net NPA reduced sequentially from 0.94% as of March 31, 2020 to 0.51% as of June 30, 2020

this is a valid question and frankly I think we need to ask the investor relations about how the RWA is computed. One potential reason could be if wholesale loans are considered to be less risky than retail ones or essentially due to an asset mix change.

I also went through a talk given by the CEO of the bank at a Fintech convention on how fintech can help driven digital financial inclusion in the country. Key highlights for me were:

- The CEO spends a lot of time doing scuttlebutt exercises understanding the needs of the underbanked and unbanked communities.

- There is a great need for credit among the aspirational self-employed retail Micro-enterprises. The input data is highly unstructured (no income tax returns for example) and there is a pressing need to serve these communities and fintech can become the enabler taking the financial services like credit, savings, investment, insurance to the last mile. Leveraging digital services to ensure as much of the offline processes can be shifted online: the offline/physical processes simply do not scale. Can we provide products to the masses in vernacular languages?

- Fintech and traditional banks do not have to be competitors, they can partner and collaborate. Fintechs can enable the transformation of brick and mortar banks into using more tech-enabled processes: utilizing ML and NLP to figure out credit worthiness of an individual based on digital (pdf copies of) cash flows and bank statements.

1 Like

Q1 result analysis from equity bulls based on numbers

Regards

1 Like

RWA includes investments in other securities, bonds, equity etc which are not part of the loan book.

4 Likes

Thanks for sharing link and information.

V Vaidyanathan on Q1 result:

2 Likes

This confuses me. The bank had between 45% and 28% of book under moratorium. Hence, there was no interest income from those assets. Even then how did the NII grow by 38%?

2 Likes

He mentions in the interview that he is expecting the book to start growing from the current quarter onwards. My understanding is that he is speaking of the retail book, and the overall book will still remain constant as it has for the past few quarters. This will remain till they hit the retail book of ~70% (as per guidance), and given the slower growth expected, it could take another 3 quarters. So for all of FY21, the overall book may remain at current levels (1 lakh cr). Difficult to see a lot of appreciation, while the book value remains largely constant. Of course, most of us on this forum understand the structural changes happening underneath, but the stock price may not reflect that till we see the actual book value growing.

What is a big positive however, is that retail liabilities have continued to increase this quarter and therefore NIM has expanded further. Balance sheet is growing stronger and more stable, and hopefully ready to capitalise once the growth period starts.

5 Likes

Key risk - High retail moratorium at 23%. With wholesale moratorium at 35% - blended moratorium is 28%. Highest among mid/large banks. Even Indusind with worst book after Yes Bank (with heavy CV and corp loan exposure) has 16% blended moratorium.

Market view has been that the retail book of First Capital retail book grew rapidly but is of inferior quality. Now 23% retail moratorium is confirming market’s view.

Brokers - Last 24 hour, Goldman, Morgan Stanley and Credit Suisse target price is between 15 and 21 per share. - With all at sell or underperform rating.

Disclaimer - was planning to buy but now won’t!

2 Likes

Due to retirement of the high yield liabilities and substituting it with casa + retail deposits.

2 Likes

@rdhoot Can you share links to these broker calls? Can’t find them anywhere. The moratorium percent has decreased from last quarter and guidance from management says it will go down to 10 to 15 percent by August end since they’ve been offering moratoriums to a lot more people than other banks since they are customer centric… so your post seems a bit suspect if you don’t mind me saying since all those calls were made in May when I did a quick Google search!

@siddarth.nath7 … I’m hoping the share price stays under 30 for a year to be honest. Gives me a year to accumulate it since funds are an issue considering the recession + my investments in pharma/chemical. The long term story is in tact and that’s all that matters. Doubt many people are buying it for short term gains with q4 FY 21 looking like a month of uncertainty for all banks

3 Likes

That is a fair point. Do note that 10% of the book were rural customers who were given the moratorium suo moto by the bank. We need to take these things into account, we should see in the quarters to come how the moratorium shows up.

As per the CEO in the interview above, when the cashflows come back to the borrowers they will pay up. Any incremental lockdowns without equivalent moratorium will cause pain for the borrowers as well as the bank.

2 Likes

CAPF and the bank have a stated strategy of lending to the ‘unbanked’ sector. A lot of their loans are extremely small ticket, or to unsalaried people without ITR records. I can see why this would seem risky and sub-standard compared to bigger banks.

However, I don’t think we can ignore the CAPF 8 year track record where the NPA’s were consistently low, through demonetisation, GST etc. When VV took over CAPF, the NPA’s were around 4-5% and over a couple of years this was brought down to 1-2% where it stayed consistently. We’ve seen with Bandhan that innovative lending models, while deviating from the norm are not necessarily riskier.

The current situation is an extremely good stress test for all institutions. Those who come out relatively unscathed clearly have a superior and sustainable model. Will know a lot more in Q3-Q4, FY21.

3 Likes

stock investing is bit contrarian - as every piece of information available and investor risk appetite and analysis makes the difference. institutional investors dont go by past numbers and factoring worst case in difficult situation around… 60% they might be right but remaining 40% only we can make money… I opened the IDFC first bank account fewdays back just online with my aadhaar authentication it was smooth process… the interface of internet banking screen so simple and very good user friendly one… the technology they had looks good - you can request money transfer via all gpay/whatsapp/phonepe or any UPI or other way means to deposit your account… same for other services… it is showing some serious and good thought process with technology adoption… if such good efforts gone in - they will have competetive advantage and can leverage this as big strength in future… I am working in ERP software and currently working for implementing software for banking - i am impressed with the way efforts gone in internet banking - it is far better than HDFC bank internet banking… i am having vested interest with IDFC First (as i was estwhile CF investor)… if you are fine with fundamental things, this could be true for other areas too - scuttlebutt

8 Likes

Though I am admittedly very impressed by the CEOs entrepreneurial ability, one thing I am unsure of is how important is this customers focus and people first approach in banking.

Being liberal with moratorium for example. Is that a prudent thing to do?

I have never heard of anyone being very happy with HDFC Bank for example and it still is the best.

Maybe being nice in matters of money is not so prudent. Having a fast technological interface and not having spurious charges in your contracts should be good enough as far as customer first goes.

6 Likes

This is a double edged sword. It benefits the bank financially too since they earn interest on the delayed interest payments. It could hurt the bank if this interest on interest results in defaults and NPAs.

4 Likes