For example, the CET1 ratio was 13.29% and it has gone down 29 bps to 13%.

The growth in retail deposits inspite of YES BANK issue in q4 is commendable. Other pvt banks have lost deposits

I agree that CASA is fueled by 7% interest rate. At some point this quarter, it will come down but will be higher than what Kotak would be offering. That is just stated strategy.

What I liked is retail deposit base is going up steadily and is now at 52.3% and goal is 75%.

Looks like they will accomplish this much faster than the stated timeline

Can provisions for Vodafone be written back to profits if the scenario changes in the next few months? or will it be adjusted against other NPAs that may crop up in the future?

I don’t think that IDFC bank would be in a hurry to write back the vodafone provisions. If the loan starts getting repaid then perhaps the write back may take place next year. The bank is moving steadily to improve NIM and strengthen its balance sheet. What matters is the competency, integrity and performance of the management team. If that is in place, adversities would automatically be taken care of.

What I was trying to deduce is, if they can use this provision for future NPAs instead of writing back, we might forget the fact that they had made a huge provision. So investors might feel happy that he was conservative with Vodafone and the future provisions are less (since provisions of Vodafone might be used to paint a Rosey picture). They might come to a conclusion that quality of underwriting is extraordinary and might pay a premium for quality of management and quality of underwriting when neither of them is great.

Ideally, this adjustment of provisions shouldn’t be allowed to avoid these issues. I wanted to clarify how this works.

Yes. I also feel that Vodafone default is most unlikely. The present Covid crisis is also seen to be stabilising. If this trend continues, we should see normalcy in most of the country barring sealed hot spots by 15 May. Tourism and air travel will remain affected.

Thanks @Puch , I found the document.

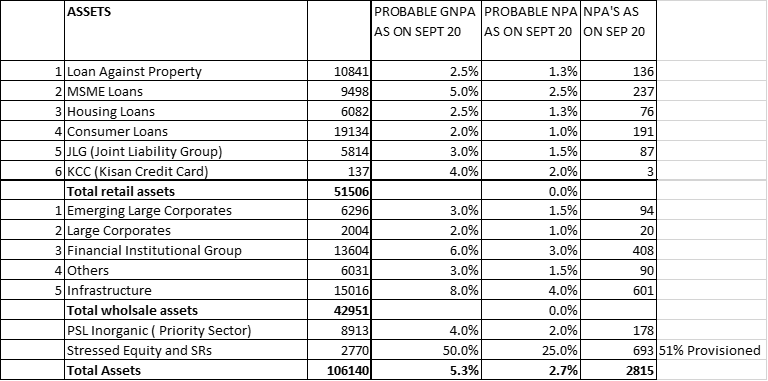

I had another question, What is the difference between Provisions for GNPL = 1,440Cr for Dec19 Q3 and Provisions in P&L Account 2305Cr for Dec19 Q3?