true…thanks for sharing your thoughts…better to wait and watch…but am already invested in the bank …so all i can do right now is watch!!

It is indeed amusing and thought provoking that only few days back, HDFC bank was lauded for its aggression in SME loans. SME was next big thing after retail. In below graphs, ICICI looks safest with a mere 3% book in SME.

Now even amusing is that for every month and fortnight since many years, we keep getting such graphs for one case, sub sector, corporate lending or other.

I think we must understand and agree that financials is a very very risky business and if at all we need to take that risk, we must embrace it with most trusted management. Question is, should I switch to an Icici only because in some recent graphs it is lower in risk or should I stick to a more trusted HDFC which may bear brunt of sme over exposure.

2 Likes

True but if it’s trusted management we are talking about … I feel Mr Vaidyanathan is impeccable in terms of his track record and seems like a trustworthy and driven person…So idfc also seems like a decent bet if it’s only management we are talking about ( not taking into consideration the margin call triggering off his stock sale) Anyways waiting and watching as of now!

2 Likes

Whatever I have read of him, it is great. I admired him a lot from info in public domain and had bought into IDFC bank. However, what I did not like was same statements again and again every quarter. I felt management of IDFC bank being over optimistic when commentry should have been cautiously pessimistic. Therefore I sold all IDFC bank shares well before the current crisis. I see HDFC management currently is cautiously optimistic. If I see this not coming true, I will be done with hdfc management also. No second chances in financials for me. Thanks

It’s not related to his margin call or sold shares to pay his ESOP loan. He knows it’s very difficult time and will not see his stocks price go up in next 6-12 month. He sold his shares on life low prices. he is CEO and knows better about the company and stressed accounts.

Idfc first has capital first NBFC client base which is unsecured. Why bajaj finance (NBFC) falling ? same SME and unsecured loans worry. Idfc first did expansion and opened new brances in last 12 month. it’s very difficult to onboard new clients in small private bank after Yes bank fiasco. No businessman want to lock their money and go in uncertain way. All state govt already passed order to move their accounts into PSU banks.

In India, it’s too diffcult for finance institution to do business. We are seeing well established group/companies are collapsing in every quarter and becoming NPA. Banks are getting hit in every quarter through this NPA mess. Now retail sector loans are big worry after this lockdown.

There is no business activity since 2 month and there will be slowdown for next 6 month after lockdown lift up. it’s too difficult time for business people to pay shop/home rent, employee salaries without earning single penny. We are hopeful that will not get any stimuls package or big relief for industry as developed country announced for their industry. We are developing country and handling fiscal deficit target every year through disinvestment in goverment entities.

There is fundamental principal to not invest in loss making company if do not have high risk leverage. Better invest in this stock once dust is clear. Market never gets old. There are lot of opportunity to buy good fundamental stocks in this fall.

4 Likes

True lots of opportunities right now … just thinking exiting at these levels not making much sense … but if warren buffet can exit his airline investments at a loss …maybe it’s not such a bad idea …something to think about !thanks for ur thoughts ![]()

2 Likes

Hi,

Can anyone help me understand why exactly VV sold his shares?

on the one side, he has great words for his bank as if it is worth significantly more than what it is trading at nw… on the other side, he is clearing his loan by selling shares at Rs. 20… exactly why? Infact, he could have saved selling stocks at such low price by pledging further stake or through borrowing or some other way… I am unclear… can anyone help me understand this why there was no other option than selling stock? This will clarify how confident VV is on his bank instead of believing on his words…

1 Like

V. Vaidyanatan had to sell his shares due to ''Margin Call".

He had taken loan to buy the shares when he was offered shares along with his ESOP allocation.

Disclosure: Invested heavily. 10 year time horizon.

2 Likes

I also gave a thought why he can’t pledge more… he claimed that he is holding 12 crore+ share after this sell off also. I assumed he might have thought market can drag the price lower to hit margin call again or he might have realised age old saying don’t use leverage for buying shares.

He said it’s to eliminate uncertainty around it if he further pledge more to handle margin calls in that case uncertainty remains as margin call may get triggered again due to share price drop so to avoid any future uncertainty he sold it off and paid it off whatever he has borrowed.

2 Likes

Thank you guys, but what I think is, when earstwhile IDFC bank used to trade at Rs. 60+, then VV took over, bank metrics improved, management improved and post takeover it traded at ~Rs. 40. A year later it traded at ~Rs.20… Now this was the chance they could have increase the stake… I mean… a management with strong confidence will buy at such low price scenario… if you feel stock is cheap at Rs.40, it is definitely way cheaper at Rs.20… And then he is selling… I mean… margin call is a valid reason… But… in such scenarios, the proper action would have been to increase stake… or at least keep the stake at same level… I see this action as a low confidence of management (at least for short period).

Disclaimer: invested.

3 Likes

I take your point but VV isnt a Tata or Birla with crores lying around to increase his stake, his entire net worth is in IDFCB stock and he even had to take a loan to be able to subscribe to his ESOP’s. How do you want him to increase his stake? He is a salaried guy like all of us, not from some big business family or conglomerate.

7 Likes

I feel this thread is cluttered with lots of posts with sole focus on VV, almost to the level of sycophancy… It seems all investors are hoping and praying that VV would come out with flying colors, which he may or may not. But none of us know him personally… all of us go by his external persona (public speeches, you tube interviews etc) which could be deceiving. I would sincerely request fellow valuepickrs to focus on the business and check whether he “walks the talks”. For next 2-3 years, I believe all banks except top 2-3 would struggle.

Sorry for being blunt here but its our hard earned money so we need to watch it like a hawk . Hope my post does not get flagged as I am expressing opinion which many VV die hard fans may not like…

Disclosure : not interested

26 Likes

On a side note, IDFC the parent holding company now looks very good to me. IDFC first bank is in doldrums, might hit or miss we don’t know. But the IDFC parent’s valuation is such that you get IDFC First bank for free. So, if the bank succeeds in the next 2-3 years, you can reap the benefits and if it shuts down, you really don’t lose much.

Discl - not invested in both the parent and the bank. Considering the holding company now

2 Likes

going by that logic , if thats really the case then he could have also sold his 13cr shares gradually too when price was dropping from 45 to 40 to 35 to 30.

I am not advocating anything but just that one point must not influence buy / sell call beyond certain weightage .

I am also evaluating whether to remain invested or to switch to some better alternative that has lesser challenges and favorable tailwinds i.e. gold loan etc due to gold price trends and lower LTV ratio higher demands and favorable ALM position as far as gold price remains stable it can prove to be better alternatives.

on other side IDFC is trading at below book value , until now management has not shared any of their assessment / view about impact - duration of impact etc. like some of the other banks HDFC , KMB , IndusInd and Bajaj Finance so just hoping that they do asap .

Strong growth in Retail Deposits (Retail CASA and Retail Term Deposits)

• During Q4 FY20, the Bank’s Retail deposits grew by Rs. 4,631 Cr from Rs. 29,267 Cr at 31st December, 2019, to reach Rs. 33,898 Cr as on 31st March, 2020, a Q-o-Q growth of 16%.

• During FY 2020, the Bank’s Retail Deposits grew by Rs. 20,684 Cr from Rs. 13,214 Cr at 31st March, 2019, to reach Rs. 33,898 Cr as on 31st March, 2020, a Y-o-Y growth of 157%.

• Retail Deposit ratio (Retail Deposits / Total Deposits): The Bank made strong progress in retailisation of the Deposit Base. Retail Deposit Ratio improved to 52.30% as on 31st March, 2020 as compared to 43.45% as on 31st December, 2019 and as compared to 19.08% as on 31st March, 2019.

Strong growth in CASA Deposits

• During Q4 FY20, the Bank’s CASA Deposits grew by Rs. 4,554 Cr from Rs. 16,204 Cr at 31st December, 2019, to reach Rs. 20,758 Cr as on 31st March, 2020, a Q-o-Q growth of 28%.

• During FY2020, the bank’s Total CASA Deposits grew by Rs. 12,865 Cr from Rs. 7,893 Cr as on 31st March, 2019 to Rs. 20,758 Cr as on 31st March, 2020, a Y-o-Y growth of 163%.

Strong improvement in CASA Ratio

• The strong growth of CASA of Rs. 4,631 Cr during the quarter ending on 31st March, 2020 resulted in significant improvement of CASA Ratio of the Bank. CASA ratio reached 32.03% as on 31st March, 2020 as compared to 24.06% as on 31st December, 2019, an improvement of 8% Q-o-Q.

• The CASA ratio of the Bank registered a strong YOY improvement to reach 32.03% as on 31st March, 2020 as compared to 11.40% as on 31st March, 2019, an improvement of 21% Y-o-Y.

Certificate of Deposits outstanding came down sharply from Rs. 28,754 Cr as of March 31 2019 to Rs. 7,111 Cr as of March 31, 2020, a reduction of 75%.

Advances and funded Assets

As part of the stated strategy of the bank, the bank continued to reduce large wholesale loans and increase the retail loan book as per trend of the earlier quarters.

• Retail Assets grew to Rs. 54,027 Cr as on 31 March 2020 from Rs. 40,812 Cr as on 31 March 2019, a Y-o -Y growth of 32.4%.

• Wholesale Funded Assets (including stressed equity and security receipts) reduced to Rs. 40,415 Cr as on 31 March 2020 from Rs. 56,665 Cr on 31 March 2019, a Y-o -Y reduction of 29%

Break-up of Wholesale Funded Assets

(Amount in Rs. Crore)

Wholesale Funded Assets Category 31 March 2019 (Audited) 31 March 2020 (Provisional) % Change

Corporate Loans

20,202

11,098

(45.1%)

Infrastructure

21,459

14,315

(33.3%)

Financial Institutions Group

11,988

12,645

5.5%

Security Receipts

1,867

1,199

(35.8%)

Loan converted to Equity (fully provisioned)

1,149

1,158

0.8% Total 56,665 40,415 (28.7%)

• The PSL buyouts as of 31st March, 2020 stood at Rs. 5,312 Cr (excluding RIDF of Rs. 2,735 Cr) as compared to Rs. 9,468 Cr (excluding RIDF of Rs. 3,456 Cr) as on 31st March, 2019. The underlying assets of these PSL buyouts are retail loans.

• The retail loans as a proportion of total funded assets improved to 60% at 31st March, 2020 from 47.0% as on 31st March, 2019, on including these PSL buyouts in the retail funded assets.

Capital & Liquidity:

• Liquidity Coverage Ratio (LCR) of the Bank at 31st March, 2020 was strong at 140% as against 114% at 31st December, 2019.

• The Bank continues to remain well capitalized with Common equity ratio (CET1) estimated to be around 13% at 31st March, 2020.

11 Likes

What can be inferred from the disclosure

- Common equity CET1 Ratio has worsened from 15.2% to 13% YoY. They might have to raise funds via bond issue which will have a direct impact on the bottom-line. However, if the bank shows profit in this quarter, things will get better.

- Though retail deposits have grown at 16% QoQ, it is the slowest in the last several quarters. It has grown at an average of 30% prior to this

- Although growth in CASA numbers satisfy the management (they mention these numbers are strong several times), we should not get carried away. CASA of this “retail” bank is still very much lesser than the industry standards. And more imortantly it is being fueled by 7% interest rates. The moment you reduce the rates, there can be a big outflow to other safer banks. All I am saying is, this is not sustainable in the future. They have to fix this somehow

- Overall AUM has marginally shrunk

They conveniently avoid QoQ numbers wherever the growth is slow or negative which is slightly annoying.

Disclosure: Invested and looking forward to something positive in the bottom line soon ![]()

2 Likes

Sir, this has lost 65% since your days of optimism on the scrip. Now we are in 2020, What is your forecast for next 5 year? Still bullish or lost hope.

2 Likes

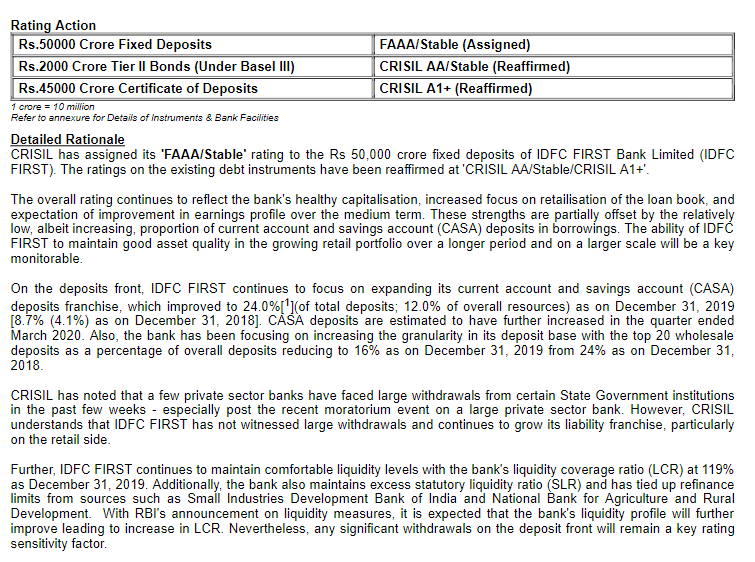

More good news for IDFC Bank-

Pursuant to Regulation 30 of the Listing Regulations, we wish to inform you that CRISILhas assigned

‘FAAA/Stable’rating to the Bank’s Fixed Deposit Program of INR 50,000 Crores.

Further, CRISILhavealsore-affirmedtheCredit Rating oftheBank’s existing Tier II Bonds (Under Basel III)

of INR 2,000 Croreat ‘CRISIL AA/Stable’& its Certificate of Depositsof INR 45,000 Croreat ‘CRISIL A1+’

respectively.

2 Likes