Good write up @sahil_vi,the pros and cons are pretty much balanced.

One question I have is their larger equity base, your valuable comments on that would be helpful.

Brilliant effort Sahil . I like your exit criteria specifically.

The only jarring note in the whole doc is extrapolating projections for 10 years . Banking is a fragile business and one big bad decision can undo years of hard work.

While banking entry barriers are well documented …innovative startups are disrupting quite smartly. I personally think the branch expansion metric that VV is obsessed over …may not even be a relevant metric few years from now . Having said all of the above… Even I’m drawn to this scrip quite regularly. Was analysing this scrip from a technical charting perspective as well today . Clearly see this headed towards 15 thereabouts… By then Mar results also should be out I guess . Planning to take an informed position by those levels

3 Likes

very good analysis.

pg5 Another instance of the CEO’s honestly is when he had to sell ~4 cr shares of the company. He had to do this because he had exercised options for IDFC first shares at 40 rupees around feb 2020 [25]. When the coronavirus great crash happened, the CEO was forced to sell the shares due to margin calls from the bank (the options are exercised using borrowed money from the bank). The CEO came clean even before selling a majority part of the shares and pro-actively worked to sooth the investors.

I think he excercised options at Rs15-16/share and not Rs40/share

What i meant was, the options were exercised when the share price was 40 rupees. Yes, the amount of money he had to pay per share for exercising the option was 15 rupees only.

what im trying to point out is that the great crash forced him to sell the shares.

Thank you. The equity base is large for sure. But think about this: how would this impact an investor? I think if anything, equity base correlates with beta of the stock, not its ability to rise or fall.

Moreover, the effective equity base should go down if and when the bank becomes profitable and large mutual funds and FIIs start buying the stock.

Hi @gramacha Since the CEO is transforming the loan book into a more granular and retalized version, I’m unsure whether 1 big decision matters so much. The capital first loan book stood the test of time (DeMo, GST etc). The real asset (and a soft-moat) the company has IMO is their ability to give risk-assessed profitable loans to salaried and small entrepreneurs based on cash flows.

Let me put it this way, just because there is uncertainty, it does not mean, imho, that we cannot or should not forecast into the future. The uncertainty should reflect in our range of estimation, imo. And it does in mine as well, I think. I have clearly outlined the headwinds, but i do truly believe the tailwinds far exceed the headwinds (specially in the long term). This is why even in the most bearish case, I think this is a 18x opportunity in next 10 years.

Those are just my 2 cents.

1 Like

Only question is …whether they will be able to survive this phase ? If answer is yes rest of the things will fall in place.

Atleast that’s what my views are known the track record of VV.

Sahil if you can reply to my query…how can vv get idfc bank shares in esop 5 yrs back when the merger was not even on cards?

Why vv said in interview on cnbc awaaz that he got it at 15 rs 5 yrs back?

Its difficult for me to understand this

He would have got capital first shares. Just use the swap ratio to arrive at the idfc shares he is eligible for

2 Likes

Hi @sahil_vi,

Very well articulated investment rationale. Slightly optimistic while focusing more on the upside than downside imho. I have been a long term shareholder of capital first and now IDFC bank and this constitute 2nd largest position in my portfolio. Was as bullish as you are ( in a way still I am and have only added to my position in recent fall in last two weeks) however what has transpired in last one week in money markets world over is unprecedented and we should be very cautious about any levered business especially a pvt banks like IDFC for following two reasons -

- barring CASA, it will be very difficult for even well established banks to raise capital, and for the new age banks like IDFC it will be twice as difficult. At macro level, very highly likely that the emerging market currencies will collapse because of the sudden rush by FII to buy US treasuries due the current crises ( INR vs USD is already showing signs ) which will make it even more difficult for banks to raise capital from foreign markets. Falling stock price makes it even more difficult. It has fallen more than 50% in two weeks. Their capital adequacy ratio is at 13.3% which is lowest in all leading pvt sector bank. Only yes bank have lower ratio than IDFC first.

- even if above was not very likely, there is more evidence that the current lockdown situation is here to stay and no one knows when this will end. The way SMEs and unsecured retail customers of IDFC are going to get hit is unimaginable. During Demon or GST, there was only disruptions but the business somehow managed to continue. Right now the entire economy has been reset in a way and the amount of NPAs this will result in is unquantifiable at the moment. Aditya Puri has already voiced his concerns that RBI should redefine and relax the NPA norms temperorqrly. No economy world over have experienced something like this before and hence there is no anecdotal evidence to show how this will span out.

Not trying to sound bearish, but just relook at the risks which were not evident just a month ago. Aside, I personally did not like VVs decision to pledge the shares to exercise his Esops.

I believe we should have a wait and watch approach until further clarity on the COVID-19 situation emerges. Your counter views on above are welcome.

Disclosure- invested and have added to my position in last 30 days.

17 Likes

On a random thought, Corona virus may create an opportunity for all retail lenders. By May/June 2020, many of the millions of small entrepreneurs would need small bridging loans to restart their businesses or short term personal loans. This would be applicable to NBFCs as well as retail banks.

2 Likes

I think, concerns raised by Mr. Aditya Puri are important, that, we have taken long time to decide the quantum of rate cuts/tax cuts, and economic stimulus should have come little early.

In some cases in the past, we have seen that, drastic changes were done in span of 2-3 days, and now we are taking so much time when urgency is much much higher.

We have to hope that, gravity of situation is understood by all, and economic decisions are taken at right time.

Apart from that, now we need to also identify some stimulus package for poor/people losing the work, due to this situation.

Disc: Invested in IDFC First Bank long back, and know that, lot of patience is needed in this stock.

1 Like

In the past, whenever such situations were there, the damage could be contained and the devil was visible. In this case, the situation is v fluid and no one knows how long it would continue, the extent of damage to life and economy.Therefore the govt is in wait and watch mode and see as to where the resources need to be deployed. Its also possible that if the pandemic spread, the resources are deployed there as they are limited.

1 Like

Hello,

Has anyone modelled or seen any report quantifying the NPAs in IDFC First due to the current situation?

Would a base case of 5% GNPA over the next year make sense here or is it expected to be worse?

Apart from NPA going up, do we have any risk w.r.t maintaining balance/fixed deposit like in case of yesbank etc. Please guide.

Fear of losing your money with any reputed bank is unwarranted. Even in case of Yes bank, the regulator stepped in and saved the retail consumers. The state of Yes bank was because of its non complaint, unethical underwriting practices. The likelihood of that being the case in IDFC is very remote ( although I firmly believe, no one knows anything about any co beyond a point) but to answer your point, your FD and money with IDFC bank are safe and you shouldn’t be worried. Rising NPA will hurt the margins and profits but won’t effect depositors money.

2 Likes

Thanks for clarification.

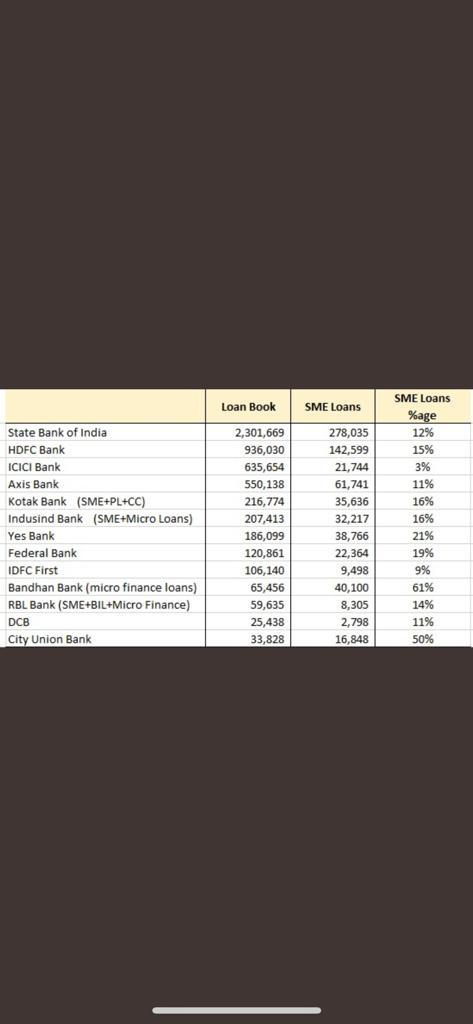

In terms of exposure to sme loans as a % of total

loan book IDFC first has only 9% exposure to sme , lowest being ICICI with 3% and just for reference hdfc has 15%.So I feel that is one plus.

1 Like

It’s around 10,000 crore. It’s big for this new bank.

It also has huge infrastructure book around 17,000 crore. may show new stressed assets because now no toll and infra activity due to lockdown. All banks may show good result for this quarter due to moratorium and 90 days NPA lifeline. wait for next 2 quarter result for getting clear picture