When idfc first bank came into existence, loan book of idfc ltd is taken into the books

Of idfc first. Idfc ltd is now the holding company

Thats not how it functions. Any transfer of loan book is not automatic. In any case IDFC bank has been in existence since Oct 2015. If there was any loan given by the bank it would have appeared against its name directly.

2 Likes

This is trading at a significant (8%) discount in Dec Future series. (~41.7 Rs vs. 44.7 Rs in cash)

Are the big F&O players expecting a crash in this stock? Is it because 6% of their balance sheet is lending to telecom?

i think it because of technical reasons not because of fundamentals.

as this script is about to cross 200 MA which is acting as resistance i think once it crosses , it should reflect it on Futures as well till then technically is not “Bullish”.

Can you pls share the source of this?

No, only 1600 crore exposure… 100 crore to idea and 1500 to jio… If u are expecting multibagger sorts of return in quick sessions, it may not be possible… Just look at the equity size… It will be a slow mover untill FII and institution aquires big chunk

1 Like

I dont think so - otherwise, all futures which are near a 200 DMA resistance, have 5% arbitrage opportunities?

BTW - read somewhere that MS has a SELL (underweight) with a target of 24 - they mention that the banks ROE is way below its Cost of Equity and ROA or ROE are not destined to improve in the medium term.

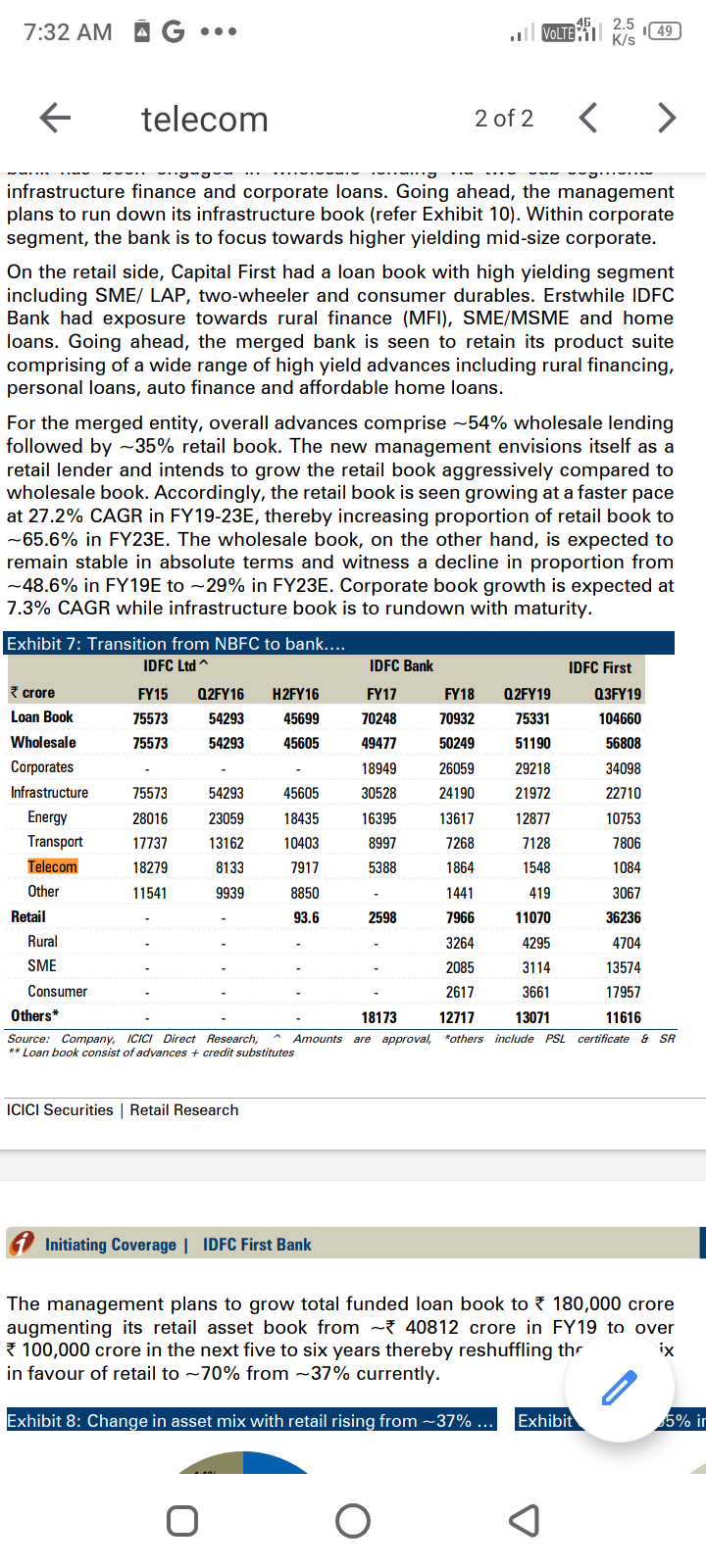

Regarding the telecom exposure, i had seen a chart recently in some report which showed IDFC at 6.x% and INdusInd and HDFC also having significant telecom exposure,

Found it

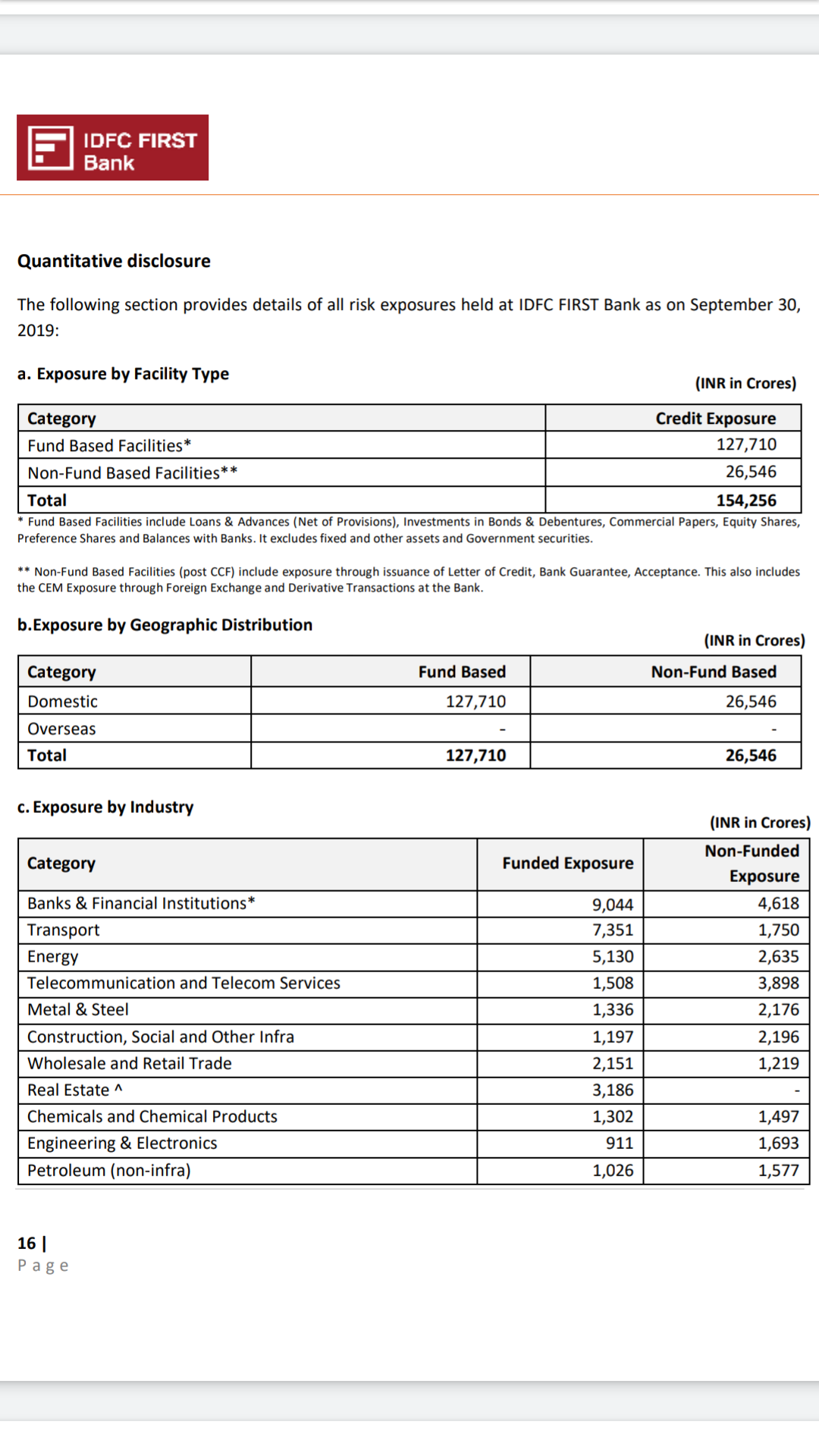

Exposure to telecom is 5700 Crores incl. non-fund based…

3 Likes

Hi Chetan , pls share the report and it’s timeline. Sharing a screenshot from recent Icici report (Aug-2019) on IDFC first . It has exposure (I guess funded exposure only) till q3 fy19…note that it’s coming down

Exposure by industry is given on idfc first bank website under regulatory disclosures. Data is updated every quarter immediately post results.

12 Likes

Thank you

My report is recent and the analyst has just compared the website data I guess.

As we all know that bajaj finance has built a moat around consumer durable loans by creating their presence around shops at nook and corner of the cities. Habe anyone come across shops having idfc first present or their representatives.

If someone attending the concall, can they please ask the same question what are there plans to reach a wide range of shops around the cities.

As i learned from their website one has to first get the approval from idfc first bank and reach the partner shop with approval id for loan… In case of bajaj finance they have a big team present on the ground/shops for document collection and loan aproval.

Bajaj finance took around 7-8 years to reach to this stage by identifying lending opportunity that’s exactly opposite to traditional lending practices ( long term higher ticket size vs smaller tickets size and shorter duration ) .

We will know how idfc is doing only after few years until then we can only monitor progress and take call .

As we have option to buy any of the two or even 3rd one as we aren’t promotor ::))

True… 3rd one will also be coming with price to book value of more than 10, i think more than bajaj

Since last one year or so, every bank and nbfc says they are focusing on retail lending. In this competitive environment, if one capturing retail share way too fast, it means only one thing - aggressive / irresponsible lending. I keep hearing about how aggressive idfc first is. They can end up in soup like yes bank ( but for retail ) or it may be a calculated strategy… For eg read the comments in this twitter thread

2 Likes

Totally surprised to see their advertising at car tyre mechanic’s shop!! Not sure how do they operate there and how many would be potential customers as these shops charge extra for even swiping debit/credit card

One has to be aggressive to penetrate into the market share of other established players. Either aggresiveness in competitive interest rate or lending.

I am sure no one wants to face cheque bounce legal consequences for not repaying 25000 inr or 1000 emi…

I am sure they must have given him the loan after seeimg cibil and since he is a driver and earning a monthly income

Recently a friend informed me that he had a cash credit facility from IDFC First Bank. The bank has written to him that the facility will be discontinued at the time of renewal in next 6 months. He then discovered that the bank has recalled such facilities from several other business owners. Fortunately he had a strong balance sheet and good business and he was able to tie up similar facility from another bank.

Question is why would a businessman go to the bank at any time in the future, knowing that they are capable of taking away the umbrella at any time.

It also seems to confirm that the bank is aggressively changing its borrower profile from commercial to retail.

1 Like

Cash credit is also part of retail lending… I am sure there must be some other reason