Wouldn’t it’s better compared to lending to say some staff to defunct Airline for buying a luxury car of 80 lacs ?

TV price might not be more then 30k and it’s easy for driver to find another job within a week of he looses one.

I think it must be looked at it from both sides, don’t you think Bajaj too has landed in such cases in the past it only now that they are in situation where they can pick and choose things after gaining a scale

Yesterday’s news from Vodafone… that they are really tired of pumping money endlessly in this bottomless pit called India… is definitely concerning.

I could only think of IDFC First… it has inherited a sizeable Telecom exposure ( more specifically Voda exposure) and I think Vaidyanathan is gonna have his A team work overtime to untangle this mess .

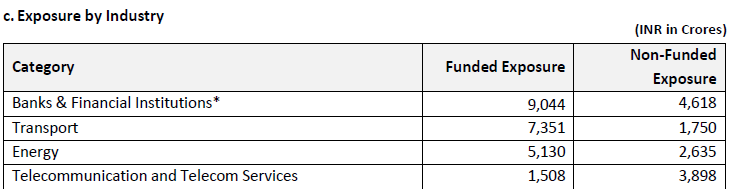

Can anybody throw more light on sizing up this problem statement ? There was a helpful thread pointing out that the total exposure is around 5K crores ( funded and non funded put together).

Sometimes we have to respect Mr Market .It somehow has the ability to price this uncertainty quite accurately…

much ahead of retail investors. No wonder the stock seems to be facing huge resistance, inspite of near unanimous consensus on Vaidyanathan and co. being great bankers with competence and integrity.

That’s just not true - the majority of the exposure can be assumed to be towards the distressed telecom players - otherwise management would not have said "we will disclose the names of the telecom borrowers at an appropriate time"on Bloomberg quint.

Unfunded exposure, although less likely to materialise (i.e. convert into funded / drawn lines) - can materialise in distressed conditions.

Source for the Jio debt is the MCA database. Entire funded exposure of 1500cr is to Jio. Wish others would back their posts with similar supporting information instead of making misleading statements.

Can someone explain me the logic here… NCD is used by company to raise funds. Its actually a borrowing instrument… A bank would raise NCD for itself why would bank sell NCD of another company and how does it affect its balance sheet/book value/advances…

Can some one guide me here

Markets are not fully efficient, but most times, for well known stocks, which have been around for some time I’m the markets, it does now something and gives a valuation accordingly.

Vaidyanathan does have the reputation of being a very aggressive banker and part of the core team at ICICI Bank during Kamath’s time. A number of the other peers of his have ended in disrepute due to their aggressive lending practices. Vaidyanathan was the retail lending head when rampant credit card growth landed ICICI in trouble. His subsequent venture also never really met the promise he always seemed to profess in public.

We need to be careful of over aggressive lenders in an industry where growing is the easiest thing but growing sustainably and profitably over many years is not so easy.

Here he has taken a very difficult task of turning around a very poorly run business with a lot of poor loans and consequently a poor credit culture.

I would request all investors to study the past of the management team, reasons for growth, quality of growth etc and not just go by what is given in investor presentations of companies. (Even DHFL had nice investor presentations )

The most pertinent guy wins in banking. Extremely important for quality growth even if it is slow rather than growth just for the sake of growth. Will keep reassessing my view on Idfc first, if growth sustains and book quality remains stable. Not seeing indications right now though. Too short a period of time to assess. Lenders like Cub who have sustained good quality growth have been handsomely rewarded by the markets.

That is true for all business(es), but more so for Banking.

Many IT companies chasing growth without any focus on R&D, innovation, creating IPR are slowly landing in trouble. You need to chase growth in revenue without optimizing your margins, which was never learnt by many Indian IT companies, which has resulted in today’s situation in IT.

Same can happen with many more industries which chase growth without quality.

In Banking, the time teaches this lesson. Those who learn it early will win, and become tomorrow’s big banks, those who ignore quality would result into problems sooner or later.

We need lot of patience with banking business.

Disc: Invested in IDFC Bank.

Dear Basu, with due respect your narrative seems incomplete, if there were aggressive lending practices inherited from ICICI by VV, Capital first should have continued in the same aggressive route and would have been caught during its tenure

Also how are we measuring the success of Capital first and attributing to VV, its revenues, profits, book growth rates ?

Please go back and read through what Vaidyanathan used to say during the initial years of Capital First. He wanted and tried to make it like Bajaj Finance. After nearly a decade of average results, he decided to take over an ailing company with very large NPAs on its books. There are some things which need to be questioned and thought through.

I am doubly wary as Vaidyanathan was in the core team led by Kamath in ICICI and we have seen subsequently the fate of some of the others in that team like Shikha Sharma and Chandra Kocchar. Also, the fact that the aggressiveness in lending during that period is something that still keeps haunting ICICI even today.

I am not saying that one should not invest in IDFC First, I am saying that one should be cautious and study well, before investing and then continue to monitor it closely.

Banking/Finance is a very interesting industry. Here leading bankers are treated like celebrities till they come up with a major problem. And then it takes a moment for the ground to shift from under them. Look at Yes Bank, RBL, DHFL, Edelweiss etc. All market darlings at one time. The reason why HDFC Bank and Kotak Bank keep getting a premium is the perception they have been able to create and nurture over many years. If some company is selling cheaply, it may be good to question why? What does the market know that I don’t instead of assuming that I know everything and the market is a fool?

Again, let me reiterate that I am NOT saying there is a problem with IDFC First. My only submission is to be careful when dealing with banks/NBFCs as these are highly leveraged companies and the margin of error is very limited. End of the day, it is our hard-earned money and prudence has kept me in good stead in this sector at least over the last 2 decades.

One way of limiting risk in one holding is to have a limited allocation. If, as and when you can build conviction over time, you can always keep adding. And always keep the exit door open and stand nearby (never get married to a stock), so that if the need arises, you can get out… fast.

Thanks for your insights Basu - let me put these ideas in a different context -

I believe their are certain interesting aspects in his time at ICICI - your point on him being the retail lending head and the way his strategy lead to rampant credit card growth. One thing is clear - we should credit him for seeding the credit card culture in this country at a time when no other banker was really keen on doing it(we are talking about early 2000’s) - and we know the number of credit card users in this country today(read this in the context of SBI planning to list its cards business). Don’t you think what he did was disruptive at that point in time (similar to what many of the new age technology company’s are doing today).

I’m sure he must have learnt a thing or two over the last 20 years being a retail banker - and its important to note that he did not change his course - it was retail banking alone that he worked on over the last 20 years (if my understanding serves me right he worked with Citi bank retail division before joining ICICI).

On your point of being aggressive - I believe all good bankers should be aggressive - take example of Aditya Puri of HDFC who is very much considered the best banker in this country - that guy is ruthless when it come to recovery - remember the way he dealt with Altico recovery.

I agree with his time with Capital First being average - and that shows that he learned a lesson from his time at ICICI - he is not reckless banker. I believe if he can be aggressive with his strategy and not get on to the zone of being reckless, make good use of all that he learned over the last 20 years, IDFC First bank and its shareholders will be the ultimate winners.

Citi started the credit card culture in India. ICICI wanted to be the behemoth and started giving cards free of annual charges etc at petrol pumps, shopping malls etc. This created a massive issue for them after a few years with large unsecure CC loans that were becoming NPAs. In contrast, look at how HDFC Bank went about it and today is the largest issuer of credit cards in India at 12 million cards, followed by SBI at 8.7 million. (Credit card users in India: Credit card usage rides on digital push, grows 27%)

Question is not giving out cards. Anyone can do that. Question is can you make it profitable such that it does not come back to haunt you?

Coming to Aditya Puri. Of course he is aggressive. But he has been a contrarion in aggression. When all banks where giving project loans and infra loans, he pivoted and started giving retail loans. Recently, he has done exactly the opposite. Now, everyone and their uncle wants to be a lender to retail, HDFC is betting aggressively on corporate loans (HDFC Bank doubles mid-corporate loan book to over Rs 90,000 crore in 3 years - The Economic Times).

I am sure if he can do that, it will be great. Both for the company and the shareholders. The question is can he? And for that I am suggesting be cautious and monitor. Don’t be too sure that he will be able to do it, because his track record, though decent, is not great.

Also, banking stocks tend to have a very very long runway. So, you can be sure things are falling in place before committing serious capital.

None of us knew that NBFC will face the fate of asset liability mismatch and would face it tough to get capital. Even the NBFC guys remained blind eyed to this.

Vaidhyanathan felt that this would gonna come someday and he merged with idfc first bank.

I feel this is futuristic and risk management at its best.

Also taking PCR on downgraded stocks that are still standard in the books is also a good risk management practice that no one in thebindustry is doing as of now… As i can recollect no one even made a single rupee provision till march quarter on dhfl.

Yes they are aggressive in retail lending but so is bajaj finance and abcapital.

Lending is a tough business… You never know while lending whether the person will return the money or not.

And under the NPA no’s, there are lot of hidd3n things. Writeoff and restructuring is amongst them…

Since bank is still has regulators, policies, independent inspection and audits.

I still feel considering all the aggressi e lending risk taken by vaidhyanathan that it is better to hold a bank rather than NBFC without proper risk management and regulations

You can’t compare this with Bajaj Finance. Idfc first bank right now truth to be told is mediocre. Untill or unless you see execution happening. It’s better not to fall prey to narrative fallacy.

Banking inherently is a tough business, better to be with a winner unless you see a mediocre bank turning around.

I am not comparing it with bajaj finance… I am just comparing 2 sectors. One is regulated well other is not… I am not saying to invest in IDFC first bank nor i am saying to avoid bajaj finance… All i am saying that a bank is better bet than NBFC