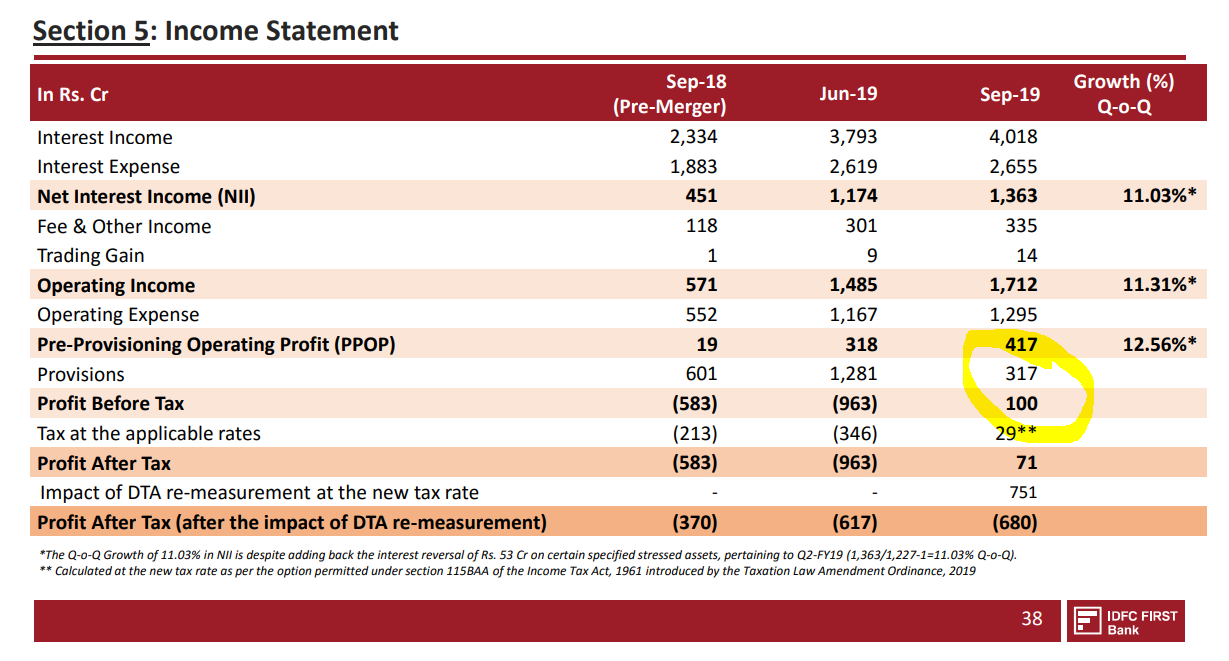

IDFC FIRST Bank Q2 FY20 Profit Before Tax at Rs. 100 crore;

Strong and sustained growth in CASA Deposit franchise, Retail loans

Highlights:

Profit Before Tax of Rs. 100 crore for the quarter ended September 30, 2019, as compared to a

Loss of Rs. 583 crore in the corresponding period last year and loss of Rs 963 crore last quarter

Bank decides to mark down Deferred Tax Assets as a result of reduction in Corporate Tax Rates

from 35% to 25%

Because of the DTA markdown, Net Loss (after tax) of Rs. 680 crore for the quarter, as a result

of one-time tax impact of Rs 751 crore due to markdown of existing Deferred Tax Assets

CASA Deposits posted strong growth rising 99% YoY and 30% sequentially to Rs. 12,473 crore as

of September 30, 2019

Retail CASA & Retail Term Deposits (which the bank calls Core Retail Deposits) as percentage of

the overall liability book increased sharply to 16.72% as compared to 8.04% as on December 31,

2018, at merger

Gross Loan Book stood at Rs. 1,07,656 crore

Total Retail Loans as a percentage of Total Loans increased to 45% post-merger from 13% as on

September 30, 2018 (pre-merger)

NIM for the quarter rose sharply to 3.43% from 3.01% in the previous quarter Q1 FY 20, and as

compared to 1.56% pre-merger.

Net worth of the Bank was strong at Rs. 16,866 crore

Tier 1 Capital Adequacy was strong at 14.51%. Total Capital adequacy is 14.65%

Total Balance Sheet size of the Bank was at Rs. 1,63,777 crore

NIM at 3.43% and so as CASA is really impressive. Wondering how the market will react tomorrow wrt 680cr loss… ( dont understand why they moved to new tax regime now and not later ).

IMO, good set of numbers. Vaidhyanathan did indicate in one of the recent interviews that they will be PBT positive but could go red on DTA after corporate tax cuts - so results are largely inline. GNPA & NPA down QoQ is good to see. So, is increase in CASA & NIMs. Provisions though, seems to be at same level. We will have to wait for the concall for details.

Disc : Very small position. Tracking

Sinces advances has degrown, but the npa remain at the same level. That means there are writeoffs being done to manage npa at the same levels

Good details but overhang may remain due to large portion of Telecom sector mainly Vodafone/idea…

Yes thats the scary part which I came to know today. IDFC First has significant exposure (atleast a big chunk) to telecom sector. I however strongly believe govt will intervene and ensure the telecom sector will not be let down.

Casa ratio of 50% in 5 years is what he said from earlier guidance of 30%, that would be comparable to the best banks which are trading at 3-4x price to book ratio

Very true. Given his track record I am expecting that somewhere down the line he will sell at least a portion of the wholesale loan book to clean up the mess once and for all.

Really, Mr. Vaidyanathan makes herculean tasks look so simple! He is very focussed and seems to know the power of retail very well and is very confident that the bank needs to do nothing else but just focus on only one thing that is retailiasation.

Can anyone give more details on how much exposure to Telecom is for IDFC and also for other banks and whats the mix between Voda/Jio and Airtel. Thanks

Hi… great presentation overlaying your views on top of bank ppt. Good stuff .

Do you intend to refresh this with sep 19 numbers? I’m seeing positive news n casa, branch count and retail penetration progress… all on track/ ahead of schedule

What is worrying though is the junk that idfc has brought to the table … worrying about legacy loans … how do we plan a worst case for that ? Yesterday’s SC verdict n Telecom could be a drag … potential impact of 3/4 RS on book value ( if the entire 1500 cr exposure becomes bad) .

Have taken a position at RS 40… would like to add more

thanks Ram

Two important points that i believe is that describes the quality and prudence of management.

- provision of 75 per on standard assets(1261 crore exposure is still standard)

- in one of the slides they mentioned that they have not counted 2641 crore of govt deposit in casa because of volatility.

I am a banker and i know no one does this.

This 2 points are pure gem from vaidhyanathan increasing the conviction to hold the stock.

Disc : invested

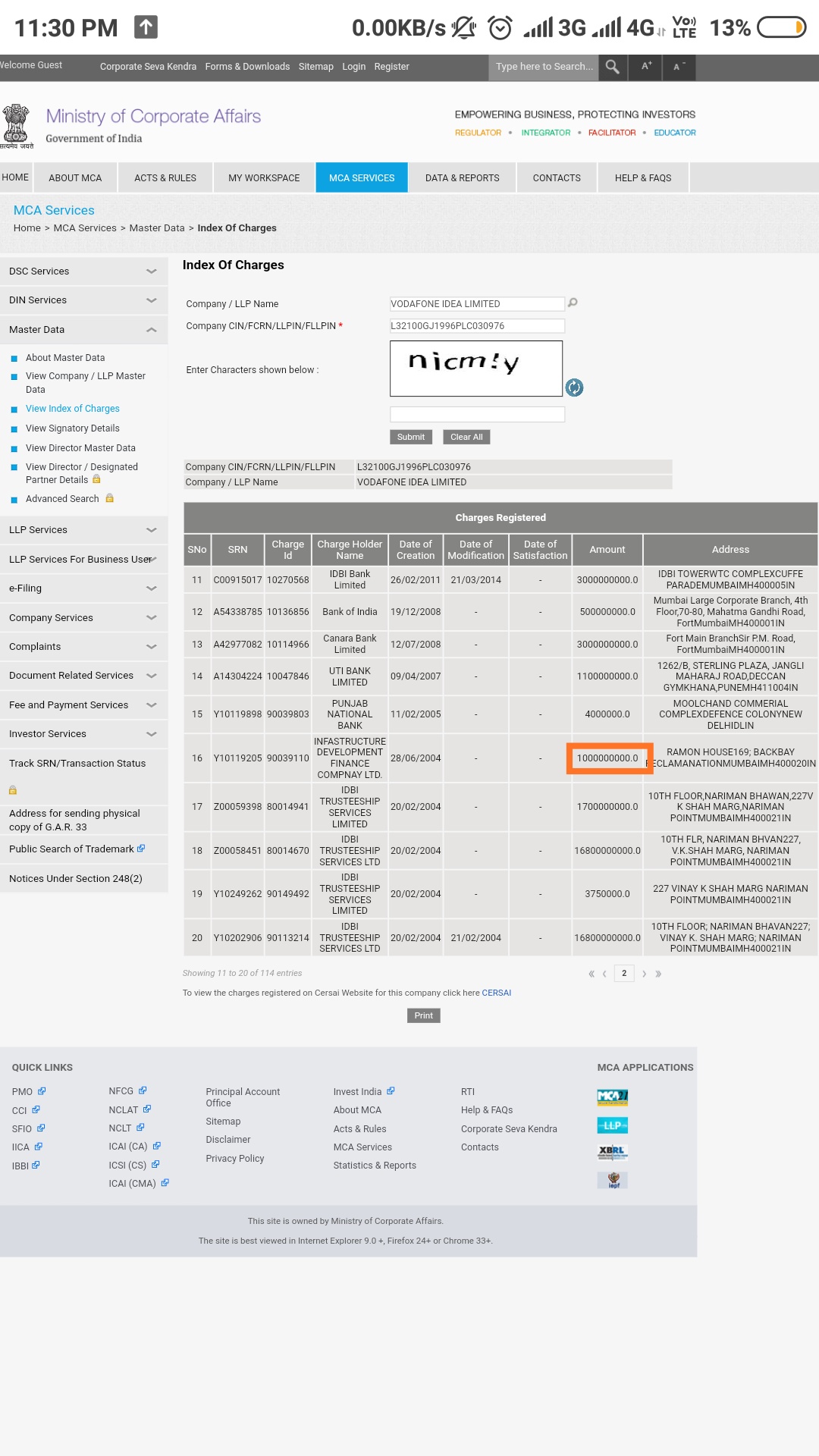

As per mca, exposure to idea is 100.00 crore only, no exposure to bharti. 1500 crore on jio

I have attached the screenshot of Mca portal… The 100 cr loan of Vodafone idea is of IDFC Ltd loan and not of IDFC First Bank ltd… And I doubt if this would be the right method for finding the exact exposure of IDFC First BANK towards teleco companies.

The loan pertains to 2004 which was granted by IDFC limited which was subsequently transferred to IDFC first bank

Any source for your stated information? Because if I am not wrong they have to update about such transfers of loans to ROC within 30 days and therefore on the MCA portal it should be reflected as IDFC FIRST BANK and not IDFC LTD