Loss carried forward got IDFC first bank the tax credit which boosted the net-worth…after tax rate were reduced to 25% from 35%, the book value should get reduced by 2 rupees to reflect the reduction in tax credit.

Disclosure: invested

Loss carried forward got IDFC first bank the tax credit which boosted the net-worth…after tax rate were reduced to 25% from 35%, the book value should get reduced by 2 rupees to reflect the reduction in tax credit.

Disclosure: invested

It’s reposted as scenario is changing from recovering possiblity to writing off though it’s too early to say

Yes I had given the figure around 300 cr is of remaining 25% as real cap defaults it has to be 100% provisioning, Don’t know what could be the collateral value and this figure should be reduced accordingly

For sometime now, scenario keep on changing for DHFL and Rel Cap continuously and in the limelight for wrong reasons. It would be safe to assume both were 100%. The real threat could be any new issue arising from the legacy infra+wholesale loans and the 5000cr stressed assets. Even though Mr.Vaidyanathan is capable, right now IDFCFirst is a hope based investment. Things might become clear in next few quarters.

Tax is reduced only from oct 1st 2019 right ? The tax credit was for previous qtrs. If company posts profit this qtr then 25% seems like a +ve impact for the company, Is my understanding correct ?

Disc : Invested.

Well, IMO, there are measurable changes that are happening on ground, so wouldn’t say its hope based.

Ofcourse agree its going to take time to clean up the book.

My thesis currently is, IDFC first has a very low base on retailing front. It is at 1 time PB (for good reason). Decent retail banks in India are atleast 3 times (good 4 or 5 times) price to book.With fall in Yes Bank growth, IDFC First has a space to grow into. It needs time. This is a 3 to 5 year play for me.

Disc : Invested.

Deferred tax assets are abt 2800 cr. After q1. There would be 700cr net-worth loss or 1.5 rupees book value loss due to adjustment in deferred tax assets after the new corporate tax.

Disclosure, invested.

If the book is made of disaster loans e.g. Yes Bank, it is better not to have any book.

In banks and NBFCs it is extremely difficult to know the quality of book and all investor can do is to trust the management on book quality. Vaidyanathan can be trusted with book quality. Problem is Infra loan book can be good now, but dont know when they would turn bad and these are large ticket loans from IDFC Bank. Historically Infra loans are worst area to lend.

Blogpost

Nothing new in this article. My biggest concern is - they currently have loan book of 55000 crore in wholesale and infrastructure. We know what 1400 bad loan can do to the stock. Plus additional expense of branch expansion. I am 100% sure this loan book mix will get changed over a period of time - 4 to 5 years.

So the question is - take risk with low price of stock or wait for loan book to change - safety of stock but pay high price of stock for its quality loan book.

I had a large position which I trimmed but I plan to increase over time. Looking for answers from experienced folks on how would they play this situation.

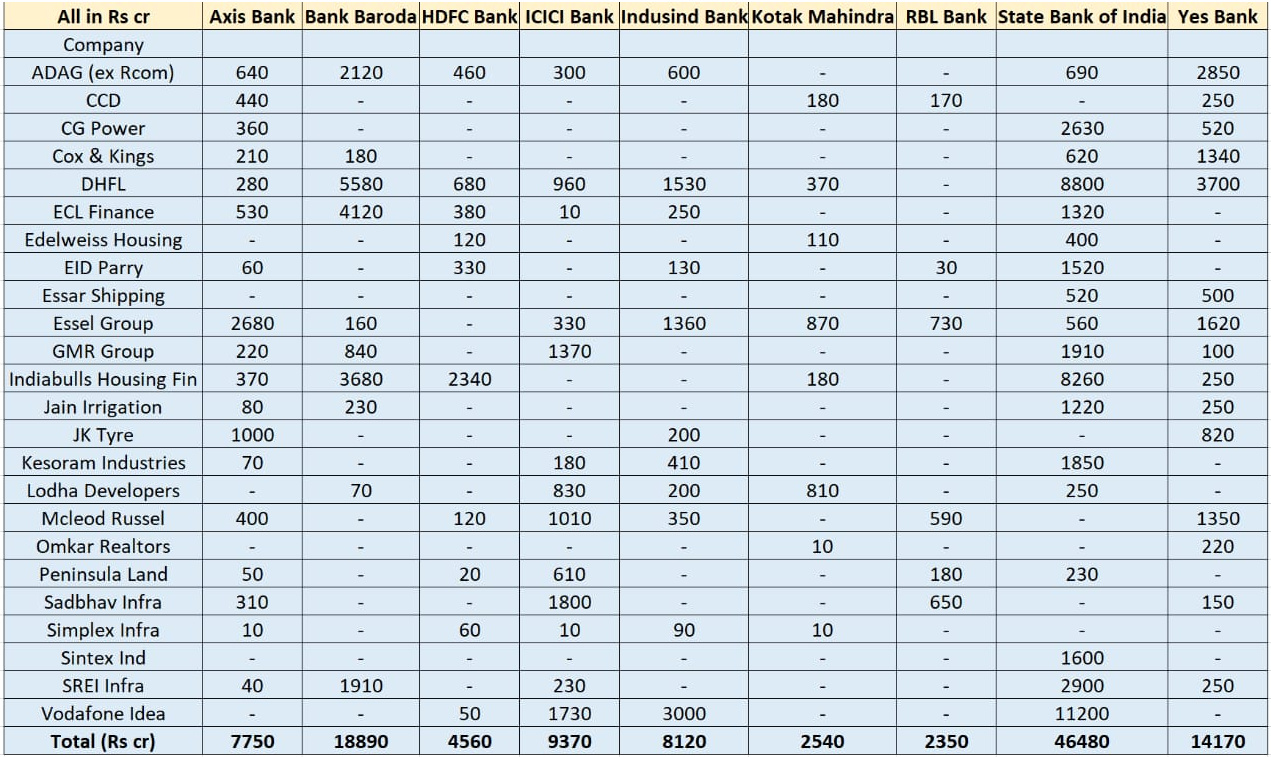

Do anyone know… What’s the IDFC first exposure to IBHFL?

It would be very difficult for most banks if IBHFL starts defaulting…

“Hoping to post a profit on PBT level.” - V. Vaidyanathan

As per the latest CBDT clarification IDFCFB can continue with the existing tax rate and shift once the DTA has been exhausted. This will require no write-off.

Latest ICRA ratings report, rating is unchanged but outlook is changed from stable to negative

Just look at his face when he says these lines :

“I feel that I have one life time, I have one opportunity and I have a banking platform and I have got to make it count…we believe we can make the world’s finest retail bank. I am obsessed with the idea and I am going to go for it.”

I’m impressed with his grasp on numbers - probably a must have trait for top banker but still.

The passion regarding banking license is evident. You can see that from 22:00 onwards.

Remaining Interview is interesting but not very relevant to Capital First.

The total number of branches is now 367 , 279 was the number in previous quarter: https://rbidocs.rbi.org.in/rdocs/Content/DOCs/IFCB2009_180.xlsx

Can someone here give me an idea on why promoters shareholding is showing as locked in… I know that warburg pimcus has pledged their shares but they are not promoters

Due to RBI regulations promoters have to hold 40% stake in the bank. I think it is 10 years from inception of the bank

All is good in video, however he doesn’t speak about the infra loans… He smartly speaks about retail retail and retail. hoping not to see any npas from legacy infra any more.

Disc: invested.