811 is a zero maintenance account. However, IDFC has minimum maintenance balance requirement of 25000 which is 1.5 times what bigger boys like HDFC, Kotak offers.

I asked a representative from the bank in March, he said they have only one product in savings bank account (Which has Rs.25000 minimum bal requirement) but they are going to launch the other products soon. But they have not launched any other product in savings account yet. Disappointed on that front.

But one new thing they have started (erstwhile IDFC Bank) is, LAP… they have launched new LAP products and also there were minor changes in other products. Representative said synergy will take time to place.

Hope they will do better on operating cost front and CASA front for next few quarters.

https://www.idfcbank.com/personal-banking/accounts.html

this are the diff type of accounts they have

High interest rates of 8.50% on FDs in a falling interest rate regime smacks of sheer desperation to raise incremental funds. Any bank worth its salt would tap the NCD bond market for funds instead of offering such high rates for retail deposits. While one may argue that they are trying to build their CASA base at higher costs, the high cost of operation and cost of funds can lead to high MCLR rates and adverse selection of clients in their portfolio unlike peer retail focussed banks.

Perhaps run down in wholesale is not keeping pace with expansion in retail thanks to liquidity issues in the portolio assets. Considering the fact that their portfolio is still exposed to infrastructure (minimum 15% of AUM) and real estate & construction funding (another 15% atleast), one wonders if there has been some legacy assets which are bloated due to evergreening of loans. I wouldnt be surprised if some ticking time bombs continue to remain in their coffers thanks to the profligacy in lending by erstwhile IDFC Ltd (known to hide several skeletons in the cupboard forcing promoter Mr. Lal to relinquish operating responsibility a` la Mr. Rana Kapoor) and Capital First (known lender to Tier 2-3 developers and NBFCs). Expect to see IDFC First featured as lenders among potential defaulters arising out of the ongoing credit meltdown.

1 Like

@coolbhat They reduced it from today. W.e.f 21 Aug 2019, max interest rate offered by IDFC first is 8%, that is too for 1 to 2 yr FD only.

@pratikchandak I don’t know whether they started to offer zero balance savings account yet, but it is mentioned in their website here

3 Likes

fyi…IDFC first bank is official banking partner for KBC

2 Likes

The sb account with classic debit card has minimum balance 10000 as per the website.

No offense but atleast do some research before posting here.

Their average yield on their Capital First portfolio is 13% so they are able to offer such high rates on savings accounts and FD.

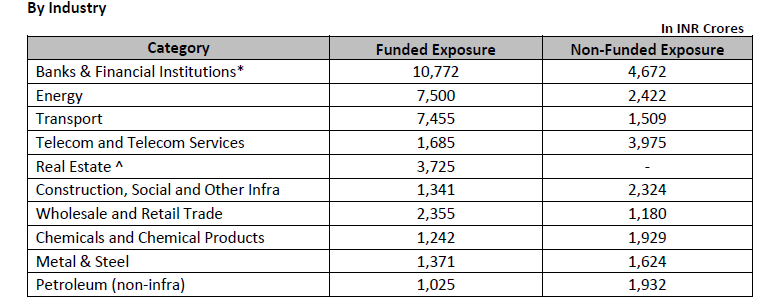

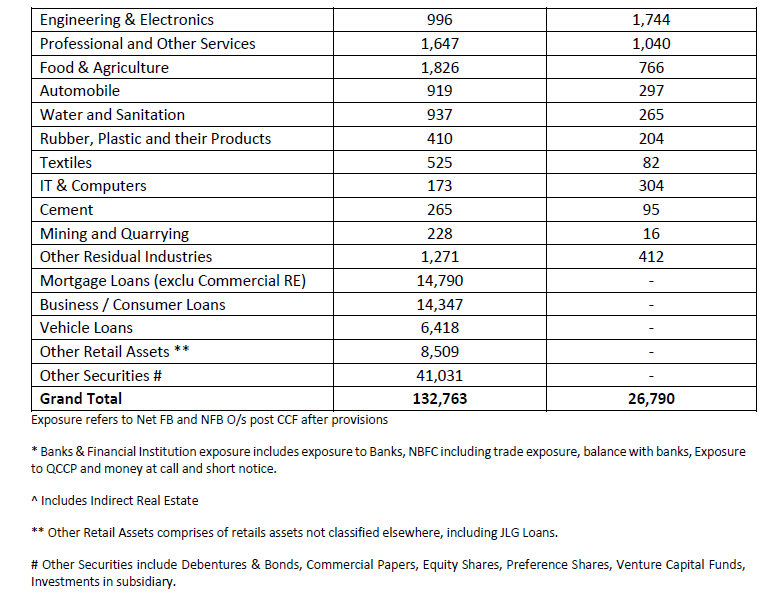

Their exposure industry wise is there on the website; real estate is nowhere near 15%!

1 Like

Also HDFC just raised 5,000cr at close to 8% with a 10 year lock-in so 6-7% on savings accounts and 8% on term deposits is a good move.

2 Likes

@Puch

No offence but you should add up Construction, Commercial RE and Mortgage portfolio constitutes real estate exposure of approx 15% of total asset book.

1 Like

IDFC first bank Annual general meeting.

5 Likes

insider buying: 25,000 equity shares worth Rs 10.75 lacs two days back

bought by this guy

https://www.linkedin.com/in/ashish-singh-472351/?originalSubdomain=in

7 Likes

It seems DHFL survival is in question now and it will hugely impact all financial companies

IDFC first has to provide 100% provisions and it will extend its losses

Now there is very low chance that IDFC first would get any money back from these accounts…

Disc: Invested

1 Like

75% provisoning is good enough. I personally feel there won’t be any more provisoning on these accounts. Next quaterly results will be very interesting. My only concern is what other accounts. I hope they don’t have exposure to altico.

2 Likes

I recollect Vaidyanathan sir clarifying on TV that the bank’s exposures to DHFL as well as Reliance Capital are backed by collaterals. So there will not be a 100% loss.

2 Likes

Bad news are not going to end soon…

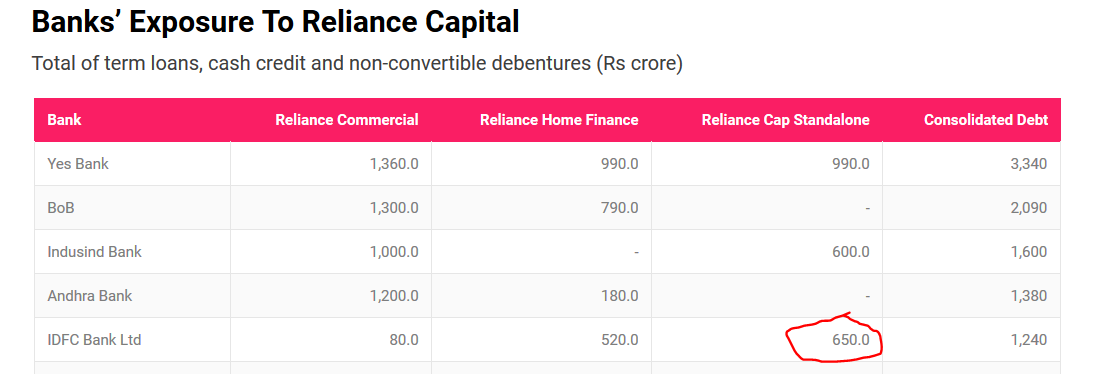

IDFC first is having 900 cr exposure to reliance capital which is bigger than DHFL

So extra provisions of around 350 crs would be be seen in next qtr results if provided excluding incremental provision for DHFL if any…

Not more than Rs 650 crore for Rel Capital.

Overall exposure of DHFL+ Rel capital is 1461. Retail NPA provisions at Rs 300 crore every quarter so hopefully it should not be big number as last quater

5 Likes

Go through this interview in which V vaidyanathan had given exact figure.

Please read the thread fully, all the info that you posting are old ones happened months ago; mentioned in the thread and some were discussed in detail.

Out of the total DHFL + Rel Capital exposure, 75% provision given months before. There may or may not be new provisions for the same… as they have collateral and depends on management view. Mr.Vaidyanathan said they will be turning profitable from this quarter which I believe will happen in this quarter.

Here is new info that is not posted yet in this thread. ICICI direct started to cover the IDFC first bank with buy rating & target of price of 65 in 12 months.

1 Like