What’s surprising is the price rise in RBL Bank after this news came out that ICICI Pru Life and AMCs will be able to buy up to 9.99% of the bank… no such move in IDFC First… why? Some overhang over the stock price? Apart from the usual culprit of high cost to income ratio?

1 Like

What difference does it make? You understand and like a business, you think the management is trustworthy, you think they have long term tailwind (short term headwinds are an additional opportunity), and given that you understand the basic economics business, and you know the prevailing interest rates you should be able to get to the appropriately deserved valuation of the business.

Then if stars align and the business is available w/ some margin of safety for your assumptions in arriving to the valuation of the business - you buy, if not, you wait. If valued egregiously high, you sell.

What market is doing, whether price is going up or down, whether some insurance/mf is buying/selling, all this is pure noise then as long as you’ve understanding of business and you are able to witness clean / smart management of the business.

9 Likes

Perhaps a more detailed reason b/h why Madhivanan Balakrishnan left IDFC First Bank.

Source: When bankers’ pay was brought under scrutiny, no one saw this coming | Mint

For instance, six months after he was promoted as executive director at IDFC First Bank Ltd, Madhivanan Balakrishnan stepped down in December. In his resignation letter, Balakrishnan, who joined IDFC First in 2019 as chief operating officer, said he plans to pursue an opportunity in healthcare that matches his long-term plans for his family and offers higher pay.

Two bankers aware of the matter said on condition of anonymity that RBI had approved his new salary with a 25-30% cut (from above ₹3 crore earlier) after he was elevated as whole-time director in June 2023. The central bank felt Balakrishnan was already drawing a high package based on his previous experience at ICICI Bank Ltd (where he was chief technology and digital officer), and IDFC First being a smaller bank could not pay as much, they said.

“The logic that RBI gave in Balakrishnan’s case was that IDFC First Bank was in the second cluster of banks. The regulator is doing benchmark comparison based on the size of banks," the first banker said.

The issue gains importance because such oversight by RBI could lead to a talent crunch in the top management of private banks. “Balakrishnan’s exit has touched a raw nerve. The main question is, how to retain talent in banking if RBI continues to be so stringent with compensation," said a former chief executive officer (CEO) of a private sector bank.

When contacted, Balakrishnan said, “The opportunity that I am exploring has a higher compensation, which would certainly be beneficial given the last few years of my career. But I would like to reiterate that the primary reason for moving out is the bigger entrepreneurial opportunities that could open up for me and my family."

Tl;dr - Its money, and bank, despite its desire to retain, couldn’t do so because regulator (RBI) wouldn’t let it overpay to retain.

7 Likes

Once IDFC ltd and IDFC first is merged, then the merged entity will become large enough to afford this salary???

1 Like

There is no business coming from IDFC Ltd so merger will not make any difference except that IDFC Ltd holders hold 1.55 idfc first bank shares & there will not be any promoters.

7 Likes

I mean Market Cap will be big for combined entity and then it will enter in the big league Banks so, RBI will increase its limits of compensations offered to Higher managements

1 Like

If you want to avoid the Mint Paywall, read this article from Finshots:

2 Likes

Market cap won’t change (assuming same price) as no new shares are being issued by the bank. Infact total outstanding shares of bank are set to decline after the merger.

1 Like

1 Like

Thanks @ishanagarwal89 for those great set of questions on concall,

It is the first time I found vaidyanathan’s answers not convincing at all…

Bank has failed to deliver on promises of 40-45% growth in PPOP and on many other fronts…

No solid explanation about elevated provisions is a big worry…time to rethink about our investment thesis it seems…![]()

3 Likes

Below expectation results of IDFC First Bank.

Key concern is about declining QoQ PAT, consol PAT of Q3 is 732 Cr against 747 Cr in Q2. Please note Q1 PAT was also 732 Cr, indicating no PAT growth in 2 quarters on diluted equity. This is despite 280 bps lower tax rate this quarter. Q2 consol Tax rate is 24.0% against 21.2% this quarter. At same rate PAT would have been 707 Cr, much lower than Q1. Haven’t seen such lower tax rate among peers, can lead to adjustment in upcoming quarter. I wanted to ask this question in Concal, was not given this opportunity (happens with Individual Investors), shall write to the company.

Key concern is the high Cost to Income ratio, despite opening lesser # of branches this quarter (35 in Q3 against usual 50) this ratio at 73% is high. Seems fear of some analysts of over spending on brand building is playing right.

With Book value of Rs. 44.51, bank is currently trading at PB of 1.97, while IndusInd bank with better numbers is at 2,09. Seems that Mr. Market shall review the valuation.

Disc. Invested & reviewing.

16 Likes

Could you please clarify your statement about IndusInd Bank with better numbers? While IndusInd has a lower Cost to Income Ratio (CI), their Profit After Tax (PAT) is only growing at a rate of 17% year-on-year. In contrast, IDFC First is experiencing an 18% growth y-o-y, even with its high CI ratio taken into consideration.

I agree with you that IDFC First’s quarter-on-quarter performance is subdued and could be improved by reducing CI and provisions.

2 Likes

Indusind’s QoQ PAT is in growth trajectory with consistent tax rate.

1 Like

Sabar (Hindi word)

2 Likes

| Q3 2024 | Earnings Conference Call")

Concall recording

1 Like

4 Likes

Have you considered increase in book value as a result of merger with idfc in arriving at 44.51

2 Likes

Nope, it’s current BVPS as on 31st Dec.

1 Like

Disc: No investments

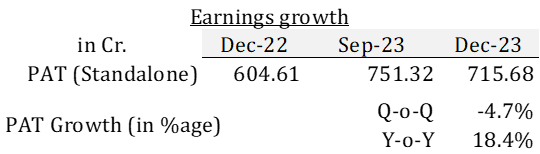

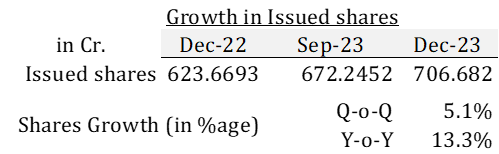

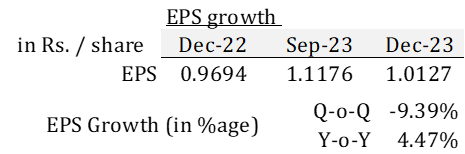

IDFC First’s latest quarterly results illustrate (again) that need to be cautious in analyzing earnings growth (or decline) without taking the corresponding “equity inflation” into account (post #1861 above - IDFC First Bank Limited - #1861 by diffsoft )., esp in a growing bank!

-

IDFC First’s Earnings seemed to have grown quite well in the past year

-

But so too has its share count, which has grown by a staggering 13.3% over the past year!

-

And that gives a very sobering assessment on how much every share earned. The decline in earnings growth q-o-q has doubled and just snailed ahead y-o-y, much worse than a fixed deposit investor in the same bank!!!

-

You may workout for yourself how the impact would be on diluted shares

Notes:

-

An estimated reduction in share count from the impending merger of IDFC (from 264.64 cr to 248 cr) will make no difference to the conclusion.

-

I just took standalone earnings because the two other entities on consolidated earnings are quite immaterial.

9 Likes

Vaidyanathan seems to be giving a message to the shareholders : “The bank is doing well, It will do even better in next 5 years. For proof we give you the guidance no 2.0. Those with long term investment horizon should continue to stay. He even gave the projected estimate of PAT in 5 years at 12000 crores.”

This would translate to roughly 4 times increase in existing market capitalisation, which would make an excellent return. He also ruled out any ‘definite requirement’ of additional capital as the bank will be slowing down to 20-22% compound growth which could be supported by the recurring profits.

I think this is a very fair and transparent approach by the bank management where they have made their intentions for next 5 years very clear. We have already seen the competence of the bank management. We can also guess the performance of the Indian economy for next 5 years provided country remains politically stable and is able to avoid getting into any major armed conflict.

6 Likes