Disc: No investments

I wanted to point out an area of caution, esp in a banking business.

Understandably, a rapidly growing business needs equity capital (via issuing new shares). This is particularly true of a banking business, because there are limits on how much you can grow with existing equity capital. These limits arise, in effect, because of rules that force a bank to get more equity to grow faster than its intrinsic rate (basically via various ratios to be maintained). This is unlike, at the other extreme, US tech firms that operate on negative equity, and which constantly engage in buybacks. Equity capital is also required to fund sudden losses that arise out of mis-steps while growing rapidly.

Thus it is highly likely that a firm, esp a bank, grows really rapidly but issues a lot of new shares in the process. That should be a real watchout for an equity investor. Just as an illustation, if the earnings of a firm grows 3x in 5 years, management will write about the wonders it did, but it does no good to an investor who finds that his share of profits are substantially lower because the company issued lots of new shares (say 100%) to reach these levels. In other words EPS grew much slower (1.5x) than earnings.

In other words an investor has to be cautious of equity shares inflation!

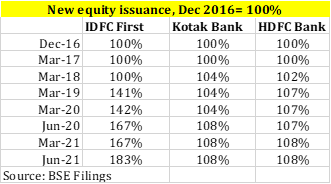

With this understanding in mind let’s look at the equity issuances of IDFC First and how it compares. The table below shows new shares issued with respect to shares at the end of Dec 31, 2016:

We see that IDFC First has issued 83% additional shares since end of Dec 2016, compared to 8% by Kotak Bank and HDFC Bank.

So, a rupee earned by IDFC First is now watered down by 44% for an investor since Dec 2016, vs only 7% for Kotak / HDFC Bank!

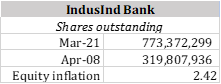

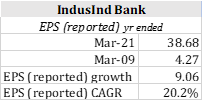

Over long periods such repeated equity issuances eat away earnings for a long term investor. This is illustrated by another bank that was a star at one point: IndusInd Bank. From the beginning of FY 2009 until end of FY 2021 as below. (please bear with my formatting)

- IndusInd Bank issued new shares continually such that end of March 2021 shares outstanding were 2.42 times those at the start of FY 2009

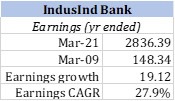

- IndusInd Bank grew fantabulously over this period. Its earnings in FY 2021 were 19 times what it earned in FY 2009 (a CAGR of ~ 28%). Earnings are in Rs crores.

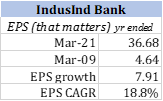

- However its EPS grew by only 7.9 times and CAGR lower by about 1/3rd because of such continuous equity issued.

- As an aside do note that this EPS will often be lower than reported EPS because reported EPS is averaged in a year for such issuances.

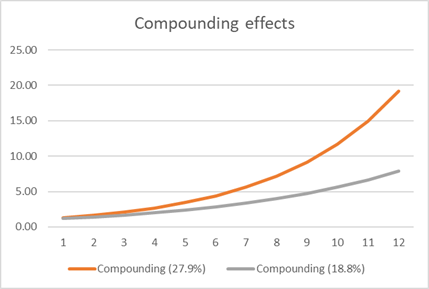

We may be tempted to ask, is it such a big deal. Yes it is. Look at how 27.9% and 18.8% compound in that time frame

To sum, earnings growth is great for management. It is equally great for an investor if his share of earnings grow at the same rate or faster (via buybacks). To that extent when a CEO says I will grow really rapid, assess how much equity will he issue along the way.

There are also other distortions with issuing new equity capital, but this one issue merits a mention