Has anyone done a comparison of IDFC vs. Federal Bank in terms of financials (earnings growth, ROE) and Valuation (P/B). My understanding is that Federal has been consistent in reporting good beat on Earnings and appears cheap/reasonable compared to IDFC.

Also, Federal has been very aggressive recently to promote usage of credit cards through various tie-ups on large retail platforms (e.g. Lifestyle, Amazon, Swiggy). Keenly awaiting how it’s marketing effort on credit card business will deliver over coming quarters. Btw - what’s market share of credit card business for IDFC vs Federal?

" 1. An estimated reduction in share count from the impending merger of IDFC (from 264.64 cr to 248 cr) will make no difference to the conclusion."

Wait, There should be no dilution at all.

Idfc first bank has total T shares out of which IDFC holds X and rest of the public/FII/DII hold Y

Before merger idfc first share count Total is T = X + Y

After merger same T = X +Y

If you quote him from the latest conference call, can you please point to when he said that? It wasn’t in the opening remarks, nor did I see it in the google generated transcript of the call.

If you are generating equity only at the rate of 11% but have an ambition to grow at 20 - 22%, where will the additional equity capital come from?

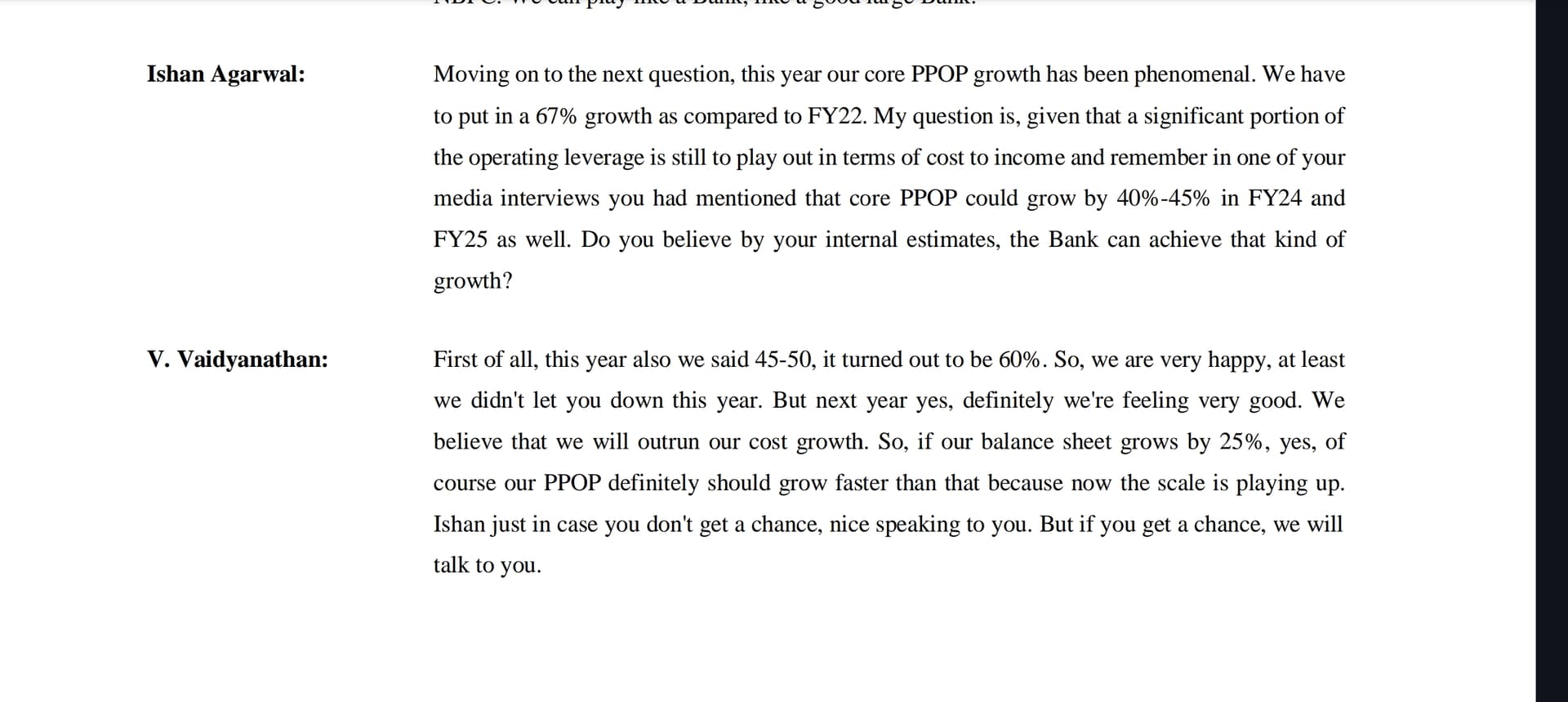

@ishanagarwal89 asked a straightforward question in con-call about equity raising, and Vaidya responded diplomatically. Like others in similar positions, he refrained from providing specific details about raising money from the market well in advance. His response indicated that the bank would consider raising equity when it deems necessary for growth.

Similar to a long-term player, Vaidya is approaching this situation like a test match. He isn’t overly concerned about a subdued quarter and acknowledges that the Q3 performance could have been slightly better. His main focus is on maintaining a low Non-Performing Asset (NPA) level, sustaining income growth, and gradually reducing costs, recognizing that some costs are necessary in the early phases of the bank’s operations.

Personally, I don’t see much of a problem in continuing to hold, even if it drops by 20% tomorrow. My focus, like his, is on 2029 or beyond.

Raunak, your remarks are quite informative for new investors like us. Do you consider present valuations expensive? Is holding IDFC as an arbitrage opportunity worth holding? Again, if we are considering mid term say next 2-5 years?

Thank you for finding my input informative. As a learner, I’m far from being an expert in fundamental and technical analysis, which many proficient individuals in this group can provide. They are better equipped to offer superior insights on valuation.

While you’ve inquired, I must confess I have no idea whether the valuation is expensive or cheap. Frankly, I don’t dwell on it much because it’s beyond my control. My investment hypothesis is solely based on the business. I prefer to view myself as a business owner of the bank, focusing on the business’s performance. Returns are merely a byproduct of the business’s activities, and valuation is just the market’s perception. My margin of safety lies in various factors:

For instance, in every annual report and quarterly result, I evaluate:

Is the management aligning with their stated objectives? Are they progressing as per their guidance?

Are there any corporate governance issues arising?

Are NPA, SMA-1 & SMA-2 under control and trending downwards?

Is the company generating sufficient profit for growth?

Are ROA and ROE trending upwards?

Is the management conservative yet focused on innovation?

And many more aspects from a business perspective.

IDFC First’s management has executed well on almost all their guidance so far. However, if, in the future, they consistently fail to meet guidance or if there’s a corporate governance issue, that would be a signal for me to exit, regardless of whether the shares are highly or cheaply valued.

Regarding your second question, there still seems to be an arbitrage opportunity of around 10% as of today if you invest in IDFC Ltd. However, this arbitrage percentage is gradually shrinking.

Alternatively, consider this perspective:

Please disregard anything I’ve said because trusting advice from a random person on the internet is not advisable. No one can understand your long and short-term goals, and without that understanding, any investment is akin to throwing darts in the air.

Disclaimer: I am not a financial advisor; I’m just a regular individual who loves learning about business.

Nobody waits. Most investors are tingling to react at first sign of uncertainty. Most businesses do not go up in linear manner, and every business has its own nuances. There’s no sign of trouble here, but people have gone into so much over-analysing every single detail as if the world is falling down for this business.

The only thing that is standing out here is increase in provisions - to which the management clearly said multiple times that sometimes there is ageing of borrowers, past covid recoveries have tapered off, and finally such extreme low credit cost numbers (as were seen during covid years) do not feel sustainable to management and hence they feel more comfortable factoring in higher provisions just to be certain.

Some investors keep asking such pointy questions to which management has no option but to politely say “Get Lost”, and that, they answer diplomatically. Not only that, they even showcase humble behaviour by asking “What do you think? Is 20% growth acceptable?” - Joota giila kar k maarna koi inse siikhe!

While there may be more worms hidden underneath, but that’s purely an assumption for now. We do not have data as of now. So we just need to have patience.

Mohnish Pabrai often quotes Blaise Pascal All of humanity’s problems stem from man’s inability to sit quietly in a room alone and do nothing. As long term business partners, we really need to pay attention to this.

No disclosures or advise, please take it as you may. I may or may not be a current, past or future investor in IDFC First Bank / IDFC Limited.

Just to make it clear, IDFC Ltd. shareholders will get fewer shares of IDFC First Ltd., than their indirect shareholding in IDFC First via IDFC. IDFC First will issue only 248 cr shares for about 264.64 shares of IDFC First currently held by IDFC (+ anything else IDFC has).

In other words IDFC First is giving less to IDFC Ltd. than what IDFC Ltd. is giving to IDFC First (IDFC First shares + net other assets in holdco). This discount is 6.288% and most likely negotiated by IDFC First to clear the Holdco discount, among others.

This also has the effect of increasing the increasing the book value per share because (a) share count goes down for the same net worth (b) IDFC Ltd.'s assets (incl cash) comes on its books

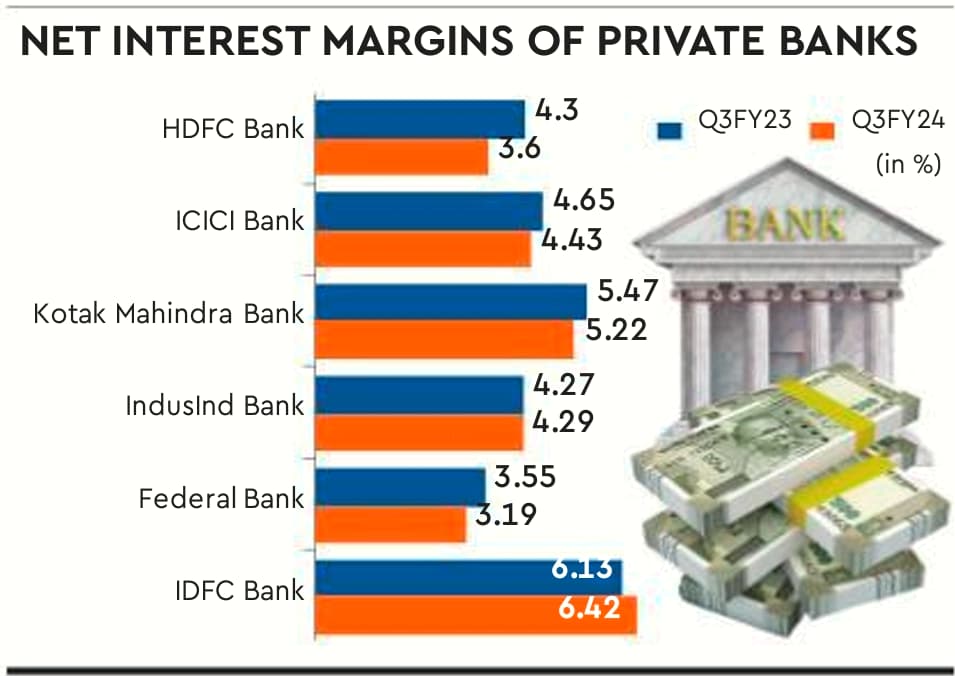

imo, IDFC First was getting higher valuations due to the perception that it is a fast growing bank compared to federal Bank…with that perception gone now, it may correct to valuations equal to Federal Bank i.e below 1.5 P/B or to P/E of 10-15…that would be a huge loss and cause of frustration for investors like me who are waiting for any meaningful stock price returns since ages now…

.

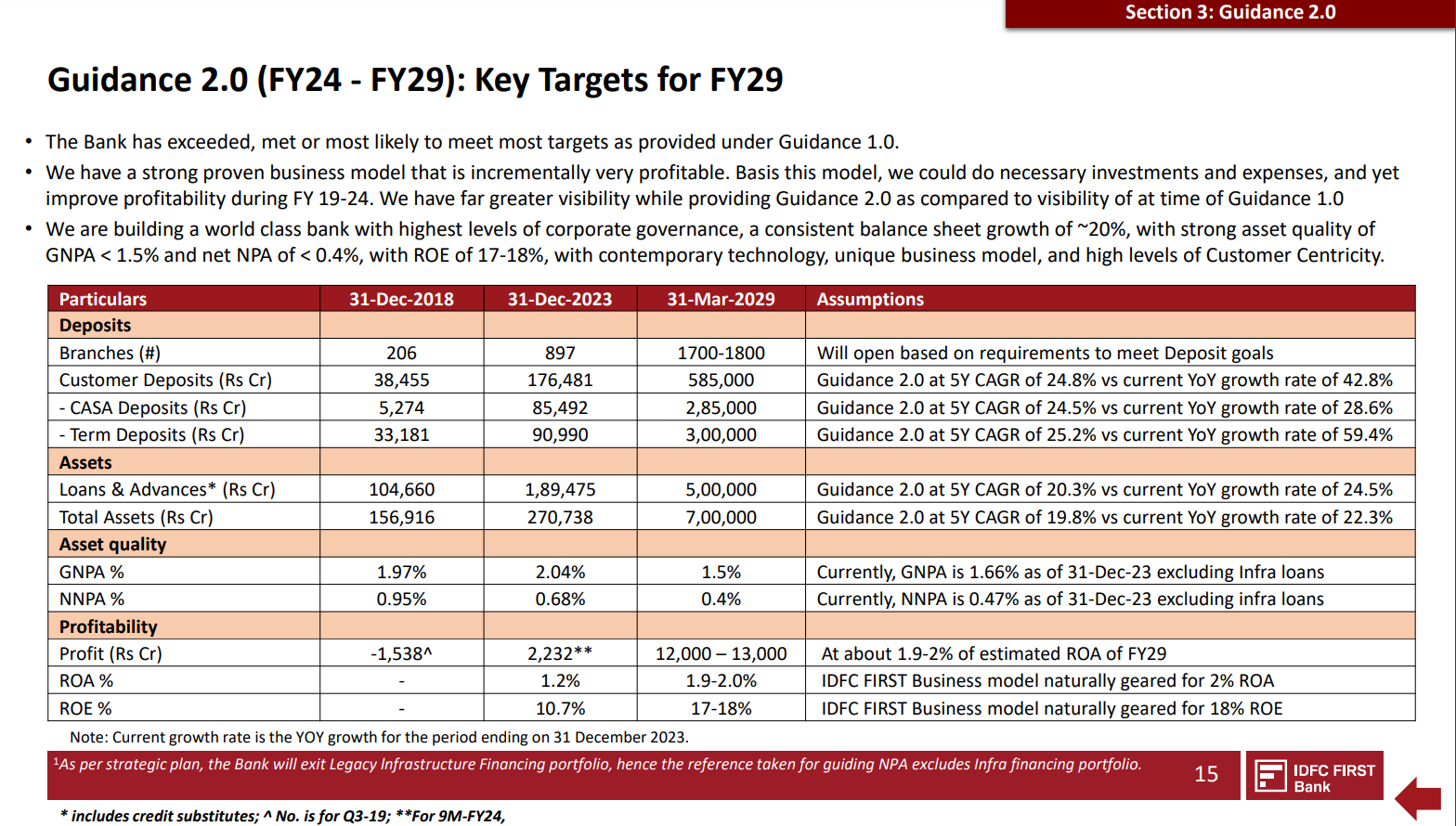

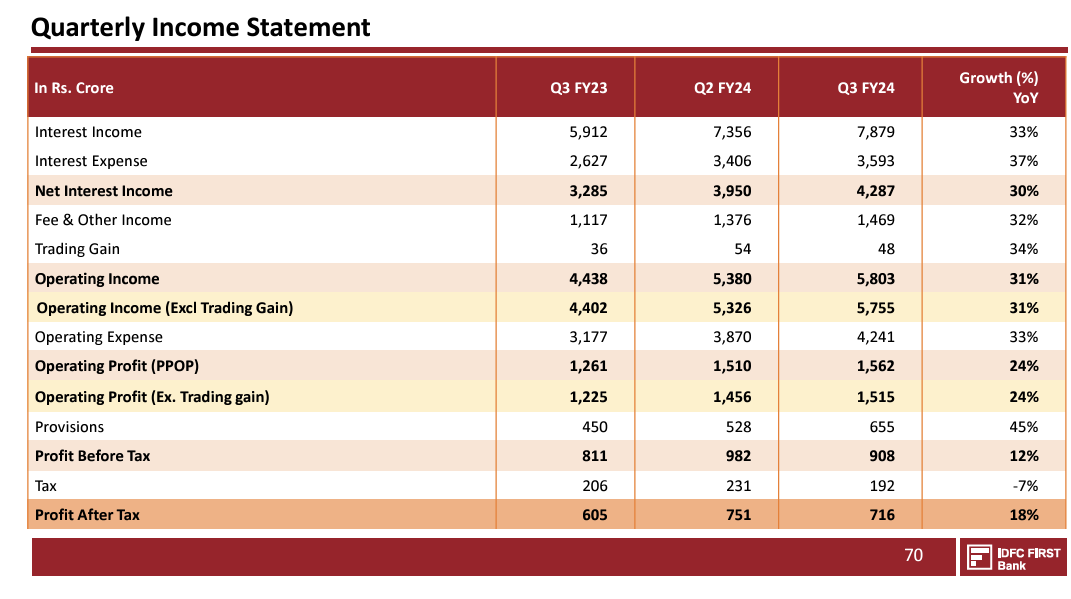

V.Vaidyanathan categorically promised a 40-45% growth in PPOP for 2-3 years few quarters back…while growth in PPOP slowing down every quarter and if we annualize current QoQ growth in PPOP that is just 12-13%…that is a huge miscalculation on part of management while predicting next few quarters and now they are selling fresh set of dreams for next 5 years in the name of guidance 2.0

I wanted to ask this in the call but someone already asked. They replied by saying that some accounts needed higher provisions due to ageing. They follow strict rules for NPAs and as per them those accounts falling in higher age had to be provisioned for accordingly.

I don’t find any other major bank which has given such an operational performance in this quarter. The only issue with this result is high provisions (which mgmt has explained as Aging related matric) and high Cost to Income ratio (not a new issue).

While the bank has changed quiet a lot, many shareholders want mgmt to show improvement every quarter. I don’t think that works in any company. Bank has already moved from sub 5% RoE to 10%+ RoE. The management has now guided for 17-18% RoE in next 5 years. As a shareholder, this is already very aggressive guidance.

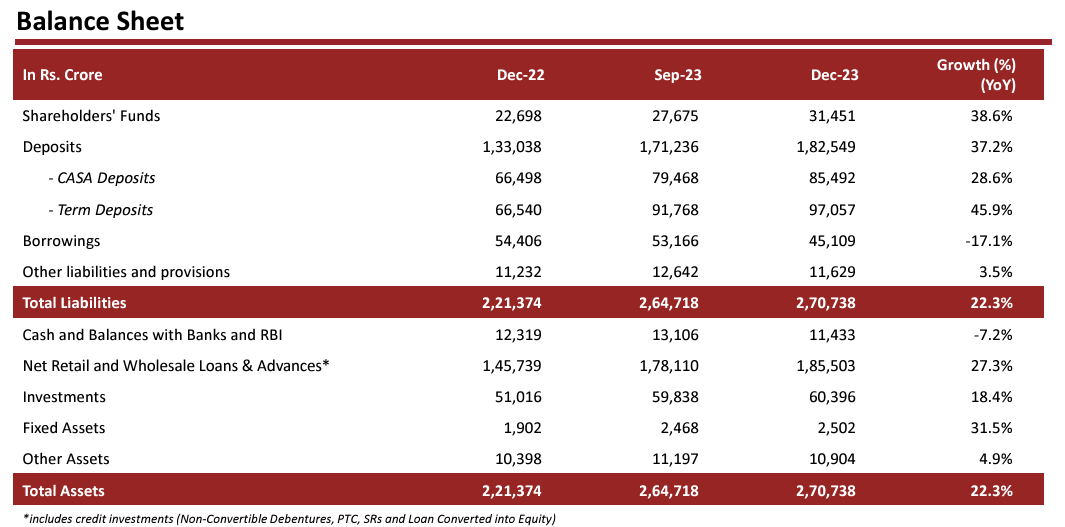

If they even achieve 15% RoE while doubling the Asset book, we are talking about a bank with Book value of 60K+ crores in next 4-5 years. Currently, the bank itself is worth 62K crores. If bank even gets a PB ratio of 2.5 by 2029 (how much will you give to a bank growing at 20% with 15% RoE), we are talking about 2.5x return in 5 years. It means 20%+ returns over next 5 years.

I am surprised that even though bank has shown no operational issues, still people are writing obituaries for the bank as if management is found to be involved in some fraud.

A weak quarter only leads to weak hands giving stocks to strong hands. In investing, only strong hands make profit. If the share falls 5-10% in next few weeks, I would suggest that it’s the best time to add.

Apologies for pinpointing, but it’s important to note that Vaidya never made promises of that nature. It’s a common understanding that neither he nor anyone else in the market can guarantee specific outcomes. provisions has increased this quarter, and the management, along with several members in this group, has already provided explanations for the reasons behind it.

I echo the sentiment of @Sanjeev_Bansal in acknowledging that we might be placing overly high expectations on the management, anticipating improvements every quarter, which may not align with the realistic dynamics of the real world.

It’s essential to recognize that Guidance 2.0 is just that a guidance not a dream. Whether IDFC First achieves it or not remains to be seen, and only time will reveal the outcome. Let’s stay informed and monitor their performance to better understand the trajectory we’re on.

.

This is from Q4 concall on April 29th, 2023…Vaidya repeated same thing in many of his media interviews along with terms like ‘opening of the jaw’ and ‘J curve’ to signal that profits will grow significantly but in reality profits are declining from last 4 quarters along with dilution of equity.

.

Also comparing IDFC First with other established banks and saying that it has performed better than those does not seem to be the right way to looking at things imo, there is NO OPERATING LEVERAGE story at play in other good banks, they are already at a respectable number in terms of ROE, ROA and Cost to Income.

The problem is with management

over promising and under delivering and still trying to promise more in form of guidance 2.0

It’s not about judging it every quarter but about seeing the direction in which it’s going, bank’s performance is slowing down significantly QoQ and it will start showing in YoY number also from next quarter onwards.

Even if they grow profitability at 20℅, EPS growth would be below it due to equity dilution. Isn’t it? For example, if the bank raises Rs 5,000 crore of equity capital and the profit grows at a CAGR of 20%, the EPS growth would be around 16%.

Is it a right assumption or am I missing something?

In the prevailing scenario, characterized by a widespread increase in provisions across the banking sector, it is imperative to acknowledge that a diminished margin of safety persists concerning asset quality or non-performing assets (NPA) for virtually all banks.

Taking a lighthearted perspective, it becomes apparent that short-term challenges are nearly unavoidable. In such a context, it would be judicious to regard five-year projections as aspirational, recognizing the dynamic nature of the current scenario.

It depends on the various prices at which such equity capital has been raised. For instance IDFC First raised around Rs 2,196 crores by issuing around 37.75 crores of shares @ 58.18 per share in March 2023. On Oct 6, it raised Rs 3,000 crores by issuing about 10% fewer shares - 33.24 cr @ 90.25 per share.

I had worked out (my post above) that y-o-y PAT growth had been 18.4%, EPS growth was much lower at 4.47%. I calculated EPS on Issued shares, but the company has substantial exercisable options that would dilute EPS further