Currently I am investing in IDFC ltd, hoping that reverse merger will convert it into IDFC First bank shares. According to you, when this Trade off will disappear and I can buy directly IDFC First bank shares? When I will come to know that level?

2 Likes

Hi Mudit, Reverse merger should take around 12 months more. We have to follow the timelines as updated by the Bank. At present levels, IDFC Ltd is a better buy since 17% arbitrage is still there as per present levels. Cant comment by when arbitrage benefit shall disappear.

6 Likes

Where can we get to watch the AGM recording which happened recently ?

Hi. Pls find attached a presentation shared by Mgmt in AGM. No idea abt video link. It is quite extensive.

AGM presentation.pdf (6.8 MB)

3 Likes

IDFC First Bank’s AGM are all about these fantastic presentions by V.Vaidyanathan…

Apart from these it is just waste of time … investors reciting poetry or some ungrateful ones cribbing about nonsensical things …very few investors actually ask good questions…

Concalls are much better investment of time…

8 Likes

2 Likes

Idfc first bank is lending recklessly. Yesterday I received a phone call from saying that they will give a top up loan on my car loan if I port my car loan to their bank. Like if I have 10 lakhs loan with xyz bank the idfc will take over it and will offer another 10 lakhs as top up. My car value itself is 12 lakhs and they are ready to offer 20 lakhs loan on it. They are lending like there is no tomorrow. This kind of behavior will not end up well.during credit up cycle everything looks like rosy. Real quality of portfolio is revealed during a crisis. I don’t want to be with these kind of reckless lenders hence Exited the stock completely.

6 Likes

Do you have the income capability for repaying the 20 lakhs, if yes then the credit risk is acceptable, I think. Can you tell us at what rate are they were willing to lend to you.

3 Likes

May be they are blending the car loan with personal loan product. 10 lakhs is car loan and another 10 lakhs as personal loan , blended in car loan. If your income and EMI paying ability is there then its not reckless. Also dont judge a big company with just one incidence. Such incidences are happening regularly with Bajaj Finance and HDFC bank . If we do our decision making on such incidences, you will get many such incidences in every company of your portfolio.

11 Likes

IDFC uses lots of data analytics & monitoring customer’s banking behaviour. The management has long experience of Retail lending and if one listens to CEO, he is comfortable growing the bank at 25% CAGR not more than that even though they have potential to exceed that. He is careful while lending to various customers that dont fit their lending criteria. They have serious focus on getting the money back plus the book is very granular.

I also keep getting the top up car loan offer. If a loan offer is given to one customer, it doesnt mean that same offer will be extended to all. Bank does lot of customised loans based on analytics and credit behaviour.

IMHO Its not right to say that bank is lending recklessly. Even during covid, retail portfolio and restructuring was not thar high.

9 Likes

I’d disagree. As investors we learn that a stock is not just a ticker or a lottery ticket but an actual company with a business. But to take it further, a company is just a vehicle run by some people(management) to create value for other people(shareholders). So listening to the ultimate beneficiaries of the company makes sense to me.

Another way to look at it is that investment is done via 2 broad methods, quantitatively and story. What we discuss in this forum most of the time is quantitative, this AGM highlights the other side(after VV’s ppt). Why markets like/dislike the company. And not to get all mushy here, but it does have its learning. Fox example, a person opined why do we hire Bachchan? I disagree with his opinion but yeah it raises a valid quantitative question as to how does the company track the effectiveness. Another one, is the one with his friend. A very touching meetup. It’s possible his friend was a plant like at a magic show. But if true (which I believe it was), pointed out how VV gifted his cycle to an office boy in college days. If that doesn’t reinforce VV’s character which in itself is a force for the bank (though unquantifiable), I don’t know what does.

The reason we stick to numbers is to be objective but in my experience a truly objective person takes even subjective data but analyzes it objectively. At least that’s how I treat it. Ingest data, clean data, understand data. Make decisions.

9 Likes

I agree with views shared by @Mudit.Kushalvardhan

Idfc first bank may have looked at your CIBIL score, cashflow analysis etc and based on that analysis you would have been eligible & got offer of topup loan as a personal blended loan.( as per the bank’s strategy / analysis )

Just as an example, idfc first bank doesn’t offer credit card at my pincode, bcoz they don’t have branch at my pincode, as told by one of their B.M. ( they only offer wow credit cards to my pincode which are backed by fd and secured ). They provide unsecured credit card to certain Pincode residents only.

Eventhough I hold high end bank account with them, have good credit score, have other company credit cards, they are following their policy and not giving unsecured cards to certain pincodes as per their policy.

On other end, I am getting other bank unsecured credit card offers, which includes RBL / INDUSIND / BAJAJ etc. They also don’t have branch at my pincode.

So should I conclude that RBL/ INDUSIND other banks has bad risk management guidelines and idfc first has good risk management guidelines on their credit card? No

In my view, One has to look at investment decision by looking at multiple angles and not just by certain one-off incidents.

8 Likes

The idfc first bank opened a new branch in a town which is about 30 km distant from my location. They have recruited 60 executives and sent them into the town. They are just visiting all the shops pity businesses and obtaining their kyc and giving them loan of 1 lakh. They are lending at interest more than 24 % and everyone is quing at the branch premises to obtain the loan. This way they can easily grow the book at more than 25% every year. But reality strikes when economy condition worsens. I’m a psu bank manager and have seen enough of such boom and bust periods. First I was very optimistic of this bank future but after seeing their lending practices it seems I better stay away than feel sorry in future.

6 Likes

One more thing about attending AGM is ( I have attended last 2 AGMs of Abbott India ), you came to know many long term investors holding huge number of stocks from decades. We admire their patience and stable minded-approach instead of running from stock to stock in search of few percentage of gains. We see these people in real and tend to look forward to inculcate these qualities in us.

8 Likes

Idfc first bank has a very strict credit writing system in place . Mr VV has repeatedly told in his interviews that about 60% of the loan applications are rejected by the bank. Also we should not forget the excellent track record of Mr VV in building retail business in ICICI bank and Capital First. Almost all the targets set by bank at the time of merger have been met before time. Having account in the bank for the last 4 years and fully satisfied with their services. I think banks don’t prompt you to use your credit card reward points while doing online payments but this bank does. Invested since 2019.

6 Likes

Totally agree. I’ve seen it personally. I applied to transfer my existing loan (LAP) from another bank. Even after having a perfect track record of paying the EMIs, IDFC First bank rejected my application twice because my employer profile was not good enough. In second rejection, I came to know from a bank representative “unofficially” that my employer company has been posting losses for 2 years and hence my loan applications are getting rejected by the bank.

Although I felt bad because I wanted bank to get benefitted from my loan (fee income + interest), but as a long-term investor, I also got more convinced by knowing that the bank is not compromising on credit quality as per their standards.

Disc: Invested heavily since 2019 for my target of 200+ in 5-6 years (delayed by around 1 year due to COVID).

18 Likes

2 Likes

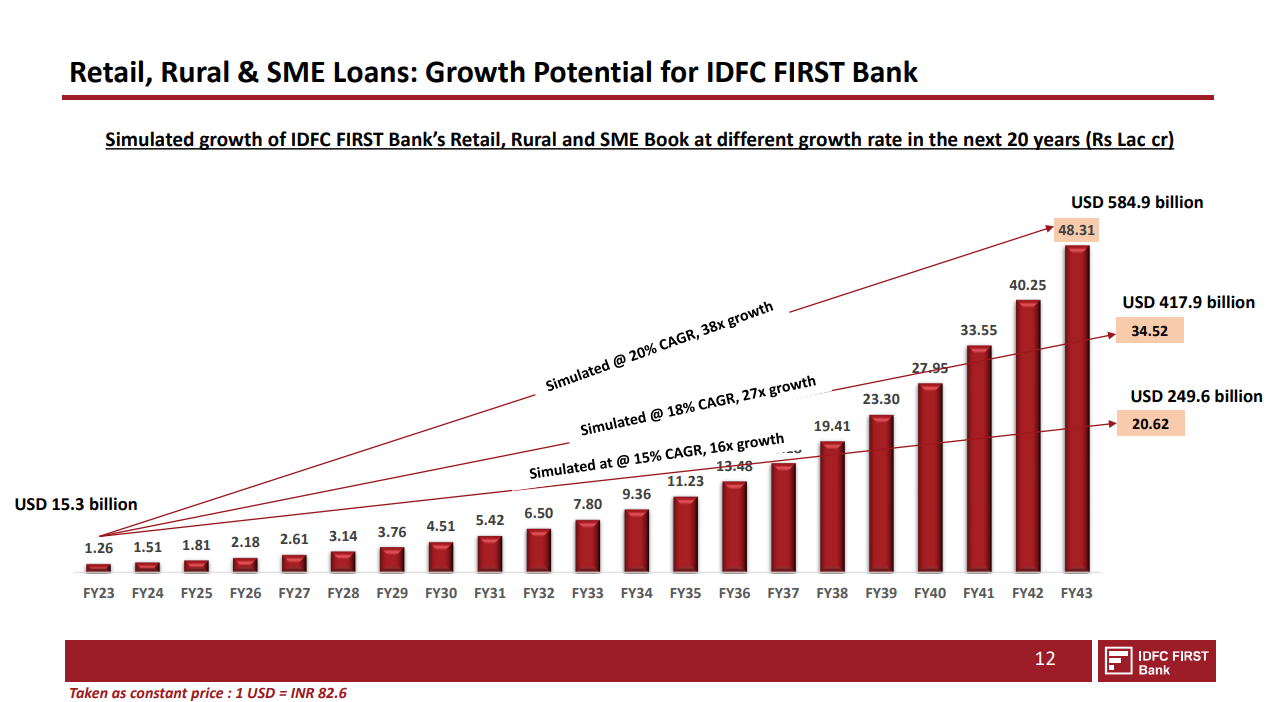

This slide presents a simulated bank loan growth scenario at different rates. It’s truly fascinating to observe the retail portfolio potentially reaching approximately 35 lakh crore if we simply assume a moderate loan growth rate of 18%.

Could someone calculate a projected market capitalization and book value for the year 2043? I know it’s a long way off, 20 years into the future, but I’m just curious to see how the numbers might shape up.

Here are some ballpark number we can use:

ROA: 1% to 2%

ROE: 15% to 16%

NIM: 4% to 6%

GNPA: 2%

NNPA: 1%

C/I: 55% to 60%

3 Likes