Hello community. I am confused about this whole MSCI rejig and its impact. As we all know, futures are trading at deep discount since last many days. I thought that this is happening due to MSCI rejig. But today was something extraordinary - Sep/Oct futures trading at almost INR 6 discount. I am not able to understand the reason. Is it like some institutions are short selling in futures? As I understand, MSCI inclusion should bring in $210M in this stock, so price should go up. Then why people are short-selling it?

Another puzzle is today’s 11.5 Cr selling by “BNP Paribas Arbitrage”. By name, it sounds like an arbitrage fund, trying to benefit from this MSCI story by shorting this stock. Again the same question - why would someone short, if there is clearly an increased fund flow in to the stock (and hence more demand for shares).

The merger can happen by Q4FY24 or Q1FY25. The bank is going to raise capital most likely by Jan/Feb. Both these factors can lead IDFC First and IDFC arbitrage to not play out quickly.

Both Cos already announced that the merger would take 8-12 months. If you consider 12 months, the merger might be completed in Q2 FY25. The earliest we can expect is by Q1 2025. That is already factored in.

I didn’t get how capital raising will delay the merger. Both are independent activities. How the merger ratio will be impacted in case of dilution? My guess is that it wouldn’t change and remain the same.

Merger ratio will not change once approved by both set of shareholders. So dilution will not lead to any change in merger ratio.

Secondly the longer merger takes the funding cost will be a factor in arbitrage.

I think one should keep it simple. If you like IDFC Bank & wish to buy & hold it for a year or more, then it makes sense to buy IDFC today & benefit from the price differential.

IDFC Bank is fast expanding its branch network in all the prime areas, here in Mumbai. I guess the same must be happening in other cities as well. The 7% rate of interest, compounded monthly, on savings account balance above 10 lacs is indeed attractive, along with a host of other services that come free with the account.

Along with the 15% arbitrage that is there for the taking, if one gets another 10-15% price appreciation over the next year, it would make for a decent investment. That said, with Mr. Vaidanathan at the helm, one would be well advised to stay put & not exit with the 25-30% gains. This one could potentially be a really long hold!

Idfc First bank offering 9% interest rate for some of their credit card customers. It is below personal loan rate. This is really aggressive move. (9% APR annual percentage rate)

Good move by IDFCF. This would certainly improve their credit card business. It appears to be a catchy incentive to low risk individuals to acquire an IDFC card and start using it. This is positive for shareholders.

Nobody plans in advance to pay interest on credit cards whether it is 34% or it be 9%. However a 9% card provides an option to delay just in case of unexpected short term cashflow problems. Bank obviously wants to attract low risk entities to apply for the 9% card. It would match individually applicable interest rates to their individual credit risk. For people who never default or have opted for automatic payment system, interest rate does not matter.

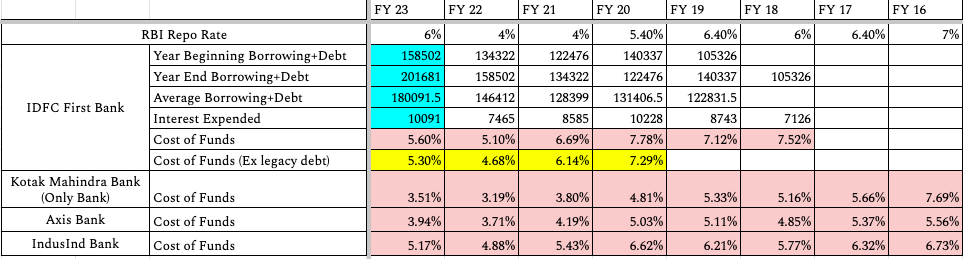

I was studying how the cost of funds at the balance sheet level for IDFCF has evolved since the merger and comparing it with other banks. I have also added the average repo rate prevailing in each FY.

Some conclusions jump out when you look at the last 5-7 years of data:

IDFCF has done a remarkable job of getting its CoF down from 7.8% in FY 20 to 5.6% in FY 23. It has been doing this mainly by initially offering a high SA rate to get customers in the door and then offer them good services to get them to stay.

An underrated contributor to the reduction in CoF has been increase in current account (CA) deposits from 2363 Cr in FY 19 to 14286 Cr in FY 23 - 6x in 4 years.

Kotak Bank has been the pioneers of this model of liability building by offering high interest SA + good service + smooth onboarding with 811. We can see how well they have executed this strategy in the table above - ~400 bps drop in CoF in 5 yrs between FY 16 and FY 21. I believe Kotak can be a model of how the CoF can be expected to evolve further in IDFCF in the best case.

Kotak was offering 6% SA interest on balances between 1L & 1 Cr till FY 20.

Despite a ~400 bps drop in cost of funds between FY 16 and FY 21, Kotak Bank didn’t

expand its NIM. NIM stayed at ~4.4% between FY 16 and FY 21. Presumably, the bank

migrated to lower yielding but safer assets.

Axis Bank has also reduced its CoF in last 5-7 years but its drop in CoF has been less than that of Kotak. As a result, today Kotak has 40-50 bps lower CoF than Axis despite having 1/2 the balance sheet.

IndusInd however has managed only ~40-50 bps reduction in its CoF in the last 7 years when adjusted for repo rate.

I did not consider HDFC Bank and ICICI Bank because their liability franchises are much older and were built during a different era.

How can this evolve in the future in IDFCF - especially for medium term investors?

After the next 18-24 months, once the ongoing deposit wars cool down and bank has built a broad enough customer base, we can expect IDFCF to steadily lower its SA and term deposit rates. This should help the bank reach a sub 4% CoF in due course. A balance sheet level sub 4% CoF (ex-equity) should be considered a benchmark that says you have arrived in Indian Banking - Kotak achieved it in FY 21 and Axis only in FY 22.

Other cost of funds reduction drivers will be - Increasing share of CA in CASA, Runoff of legacy

debt and Decrease of borrowings as % of total funds.

I see the current marketing blitz by the bank (KBC, BCCI sponsorship, Partnership with cab drivers, increased ads on TV etc) as an attempt to get top of the mind awareness (TOMA). This TOMA should enable the bank to gather granular deposits where it would later be easier to drop the SA rates - similar to Kotak’s strategy.

On the asset side, I would expect IDFCF to not pass on this CoF reduction to consumers completely and hence increase NIMs moderately.

Source - Data taken from ARs of companies. I have used standalone statements for Kotak’s data.

Requesting members to kindly share your inputs/feedback.

Thanks @Utkarsh_Bharadwaj for the efforts around COF. Completely agree with COF coming down further and Bank able to maintain atleast 5.50%-6% range of margins in future. Would like to add couple of points around COF, Bank & NIM:

Stabilising technology spends and positive contribution from High yielding Credit cards + Cross sell from branches will further help to reduce COF as commented by Mgmt even after spends on adding more branches over time.

Industry leading services and innovation in age old products like Offering Auto sweep to FD facility for MSME CA Balance of INR 2 lacs will garner lot of Current account business. Bank has also built good Govt banking, startup business, MSME which have strong CA potential.

IDFCB has strong Risk people at the Top from ICICI, HDFC Bank and are focussing a lot on Rural banking, MSME with loans with Avg yield of 12-15% and bank is able to manage risk in that segment with high use of data and proprietary lending models & most importantly strong experience of lending in these segments. These loans will balance the lower NIM from Home loans, Vehicle loans in Tier 1-2 cities resulting from aggressive growth in Secured assets. Having followed banking closely, I don’t see any other Mid size bank with 25 plus loan products in Retail + MSME and still innovating. The problem with other banks is that they have close to 50% corporate book with lower NIM and focus on new products + customer service is lower. IDFC has less than 20% wholesale book where lending is more to NBFC’s and A rated corporates with exposures in the range of 200-250 crore.

Since the bank is going much granular, CASA customers will continue to adopt IDFCB over PSU banks and many other regional banks due to strong brand and services. Further, CASA customers today are not much concerned about interest rates on SA but more on security, ease of banking, products, customer support, App UI, Customer value. IDFCB is performing well on all these and should be able to grow its customers offering lower SB rates as well. Amongst the large banks, ICICI has been a pioneer in digital banking and today CTO of ICICI is with IDFC alongwith many other senior members. For eg: Being a First Select customer of the bank from last 5 years, I have never received a call from Bank/RM to buy any insurance or unnecesary product whereas there are ruthless eg’s of people being mis-sold ULIP by banks. There are many more references of strong customer focus and ethical banking which one will come across by using their services or reading AR.

Motto of the Bank is Ethical + Digital + Social good. Mgmt. has ensured that these are not words only.

If only IDFCB can keep the GNPA within 1.50%-2% bank level, it can do a 20-25% CAGR for a long time seeing the credit opportunity available in the country.

P.S.: Significantly Invested from lower levels & would be comfortable in averaging up over time with the progress of the bank.