How does it matter to IDFC First? Banks should be worried about credit worthiness and solvency of its customers and and I dont think even the research paper questioned the solvency of Adani entities.

I dont think we should confuse a question on market capitalization as a question on solvency/ credit worthiness.

AJ

Disclosure: Invested in IDFC First from lower levels. No exposure to Adani group entities.

I am not commenting on the credit worthiness of the Adani group. However as an Investor in the Bank, it would just be reassuring to know that the Bank has not lent to a mainly infrastructure player (with relatively higher leverage) after having forsworn infra lending.

As for the solvency of the Adani group, I leave the matter to people in the know as I don’t track or have positions either way on Adani group.

Disclosures:

Invested in IDFCF. No activity for last 6 months.

No positions in any Adani entity

The report doesn’t mention any Indian bank specifically. The only reason they mentioned ICICI/AXIS is because the analyst gives recommendations for those banks and they wanted to disclose that.

But, VV has categorically said several times that the bank is focussing on retail. And VV has been known to be a man of his words. I would believe him. However, if news comes that IDFC FB has lent money to Adani for infra projects in the last 2-3 years, my trust in VV would be broken. And since that is the only reason for being invested in IDFC FB, I would liquidate all my holdings.

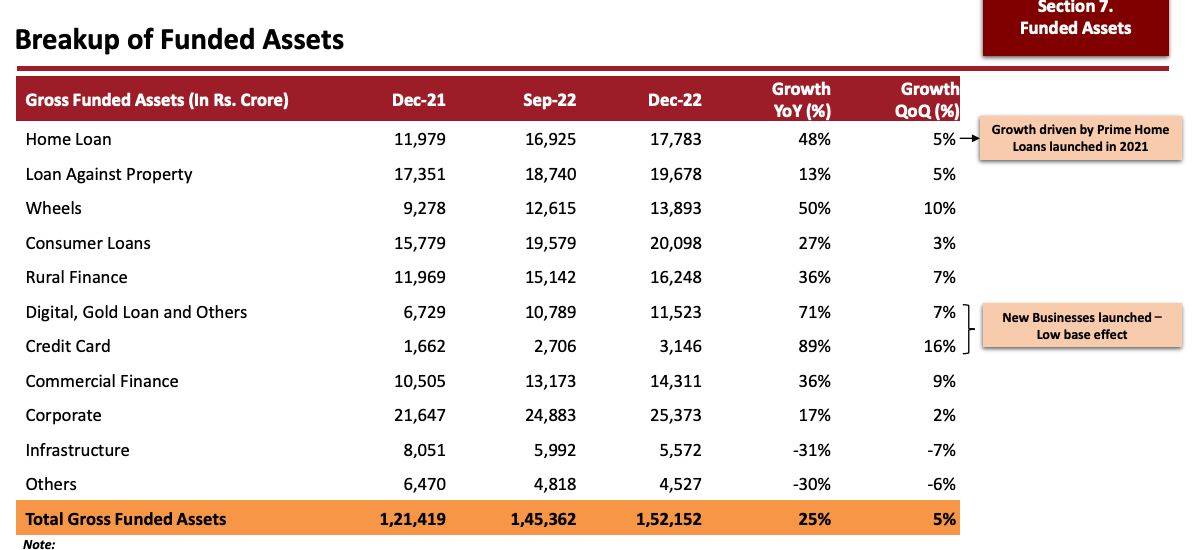

It would be unfair to compare nims of idfc with other banks…idfc has a DSA agent fee component of 1.5% which kills the margins at Cost to income level. So NIM looks inflated, while if accounted with CI ratio, it would probably be lower than 4.5%.

I understand dsa fee is may be one time, but as per renewed guidance from VV since past 2 quarters, CI ratio is being targetted at 65% now , which will be achieved in 2 years from here.

There r two major overhangs here - CI ratio and equity dilution because ROE is not above teir 1 capital adequacy ratio.

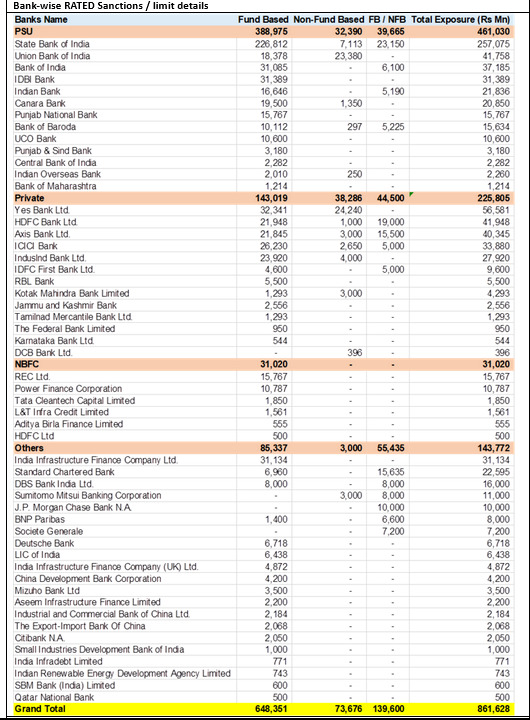

Some additional information came out in today’s disclosure by Adani Ent CFO Jugeshinder Singh. In a gist of the overall debt, 23% is from domestic Banking which comes to Approx $9 Billion worth of exposure. Adani Ent CFO Jugeshinder Singh

I wrote to investor relations to know what is the exposure to Adani group. I suggest everyone to speak to Investor relations to get the exact numbers.

But I feel we are reacting in haste. Let the heat cool down and think rationally. This group has assets worth billions of dollars. So banks will recover what they can with a bit of cut.( But all these are my assumptions …I don’t think this group will go down)

one correction if I may …VV never said he will build retail only bank. If you listen to last year conference calls …They will continue to lend to corporates which are good and selectively …if you see their corporate loan book is increasing.

they only said they will not lend to infrastructure based companies.

Note : IDFCFB is not retail only bank. If your thesis is that this is retail only bank , you may have to reconsider the decision

I second that. VV has always maintained that IDFC first will have a mix of 75:25 retail to corporate loan book. Coporrate loan book can be in any form (WC lines, Guarantees (non funded), term loans, ODs, and other corporate requirement loans)

the major thing which VV is retracting from now is - the CI ratio - which use to be a standard target of 55% just 3 quarters back - he changed that to 60-65% last concall and this concall - he specifically mentioned 65% and extended the tenure to reach 65%. This in my opinion will not let us reach an RoE of 15% in a jiffy. we are going to see a painful time of fund raise (this time around its going to come from IDFC ltd, so we can still safeguard our interests) however, if ROE above 15% or above Teir 1 ratio is not achieved soon (more likely scenario because our CI is going to trend slowly towards 65% - who knows he will start saying target is 65-70%), we will continue to see further dilution and hence can stagnante the share price.

its prudent for VV to focus on fixing CI ratio by gradually moving away from DSA model and try to reduce CI aggressively, other wise i dont see value creation in longer run if ROE remains lower than teir 1 CAR.

Hope he achieves it.

Discl: invested in IDFC first through exposure in IDFC ltd.

Agree. The Bank seems to be doing exceedingly well on all parameters guided for FY24-25 at the time of merger, EXCEPT the Cost-to-Income, on which they seem to be clearly faltering. The C/I of 55% seems not achievable by FY25 by any stretch of imagination, and some calculations would indicate that reaching even 65% by FY24-25 is difficult. Therefore, while RoE has picked up smartly to the 10.7% level presently, the move up from here to 15% is going to be a slow one, unless they fix the C/I with a greater sense of urgency.

Disclosure: Invested, through exposue in IDFC Limited.

In Q3 the credit growth was 32% yoy, if Infra is not considered. IDFCF is clearly aiming at 30% + growth. It will start showing in composite figures as infra portfolio moves towards zero.

Banking sector is a proxy of the economy.

For the first time in decades we see a courageous budget in a pre election year which is growth oriented to the hilt with zero freebies. With such display of strong faith by the govt in the ability of the common man to trust the govt, it looks like that we are finally looking at a bright future and strong growth. This should push Indian businesses to come out of their skepticism and commit capital on bolder bets.

I feel banking sector will receive tail winds for at least a few years and Idfcf needs tier 1 capital to grow at 30%.

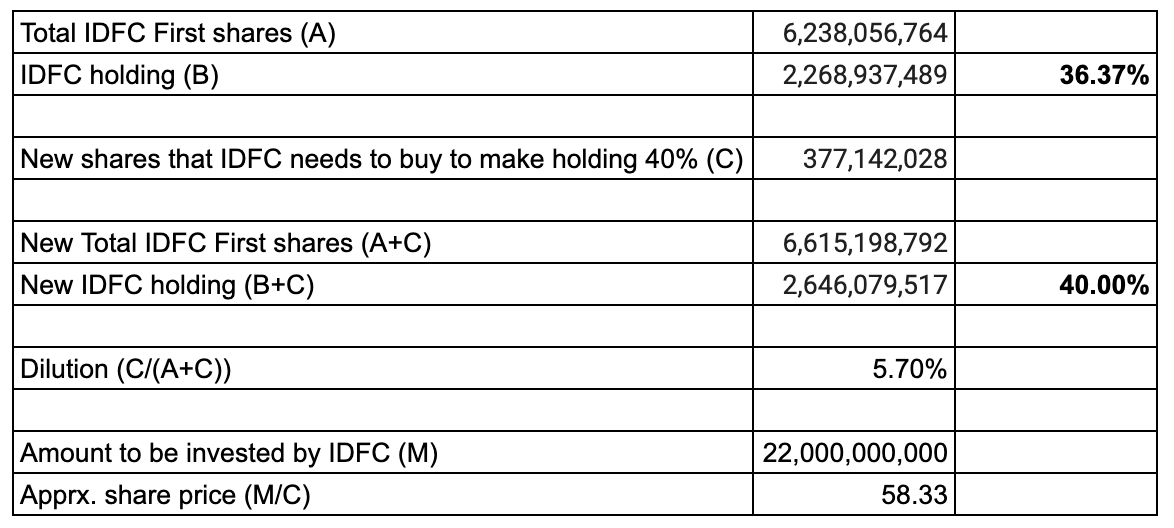

So IDFC Ltd will be investing ₹2200cr for an approximate 10% equity dilution. This should bring the market cap to around ₹24200cr. This is quite a discount to current market cap. Can anyone help with this?

If the share price for this deal is significantly higher that 58.3, then the % holding of IDFC in the bank will be less than 40% post their investment. In worst case scenario, we’re looking at 5.7% dilution because IDFC cannot increase the holding above 40% and they’re already planning to invest 2200cr.

Disc. - Invested and sharing the analysis without any reco