Thanks for helping me out!

IDFCF had done the last QIP issue in apr 21 at Rs57/-. With present fundamentals, I do not think that IDFC will be given share at Rs 58/-… Mr VV may negotiate a good higher price leading to lesser equity dilution.

1 Like

I believe one should read the notification carefully. What they mentioned is that the intention is to invest Rs. 2200 Crore taking the holding to a maximum up to 40%. I read this as the base share price shall not be below Rs. 58.33 per share as worked out by @Shikhar_Gupta above.

Thanks,

AJ

Disclosure: remain invested from lower levels.

6 Likes

We wish to inform that the Board of Directors (“Board”) of the Bank at its meeting held today i.e.

February 4, 2023 has, inter-alia, considered and approved to Issue, offer and allot 37,75,00,859 (Thirty-

Seven Crore Seventy Five Lakh Eight Hundred and Fifty Nine) equity shares of face value of ₹ 10/- each

fully paid-up, on a preferential basis, to ‘IDFC Financial Holding Company Limited’ (“Proposed Allottee”),

wholly-owned subsidiary of IDFC Limited (jointly referred as “IDFC”), at a price of ₹ 58.18/- per equity

share (including premium of ₹ 48.18/- per share), amounting to ₹ 2,196,30,00,000 (Rupees Two

Thousand One Hundred Ninety Six Crore and Thirty Lakhs only) (“Preferential Issue”), which offer/ issue

price is in accordance with the applicable provisions of the Securities and Exchange Board of India (Issue

of Capital and Disclosure Requirements) Regulations, 2018 (‘SEBI ICDR Regulations’) (including any

statutory modification(s) or re-enactment thereof for the time being in force), subject to acceptance of

the offer by the Board of ‘IDFC’ and also subject to approval of the shareholders of the ‘Bank’.

9 Likes

Isn’t it strange that the dilution is happening at the current price? I thought VV will at least negotiate for around 65 to 70 for dilution as the last fund rise happened at around same current price.

3 Likes

Sadly, cant see any value unlocking with this reverse merger. If there is, would like to hear someone explain.

(Invested in IDFCB)

No.

If the bank would have proposed the price higher than the CMP, wouldn’t the holding co. hv bought the shares directly from the mkt??

Remember this for this case nd also for any further equity deals(like OFS) u study, the issue price will always be at a discount to mkt price, else wouldn’t the transaction make sense at mkt price itself. Evry seller aspires cheapest price, every buyer wants highest price - Fair settlements happen at reasonable price.

The value unlocking is to happen at IDFC holding co. level. U can go thru the IDFC thread for more details. To summarize, the reverse merger is to happen bcoz of regulatory reqmt to bring Bank promoter holding below a certain limit after 5 yrs

The only good frm Bank perspective is that once the merger overhang gets over, the stock can get re-rated.

Although initially, thr maybe sm selling pressure wid arbitraguers selling out.

Disclosure :- Invested in IDFC

12 Likes

In my view, we should note that when the reverse merger happens there is bound to be a holdco discount that will be applied.

For example, in the case of Equitas SFB and Equitas Holdings, there was a 16% holdco discount applied while deciding the merger ratio. Shareholders of the holding company were allotted 226 shares(later increased to 231) for 100 shares instead of 273 shares that they indrectly held in the bank via the holdco. We should also note that in the case of the equitas, the boards of the 2 companies were related whereas in the case of IDFC, the boards are independent which favours the bank.

After factoring in the dividend, the market seems to be factoring in a merger ratio of 132:100(ex-dividend price of IDFC of 77.6 vs IDFC First bank price of 58.8) and not 165:100 which is held by IDFC shareholders indirectly, indicating a 20% holdco discount for merger. In my view, the holdco discount could range anywhere between 16-22% depending on negotiations.

10 Likes

What was the discount for Ujjivan?

It seems funds raised by IDFC First bank from IDFC were negotiated at 58.18/share. It will be bad deal for IDFC shareholders to have stake increased to 39.99% by paying market price for these additional shares and then receive less than 1.65 share of IDFC First per IDFC share. That will be value destructive than returning cash directly to shareholders via dividends.

Not all shareholders of IDFC will be liable to pay tax on the dividend. If IDFC shareholders are going to get less shares than current ownership of IDFC First shares, what’s the motivation for IDFC to increase holding further rather than issuing dividend of additional 2200 cr?

5 Likes

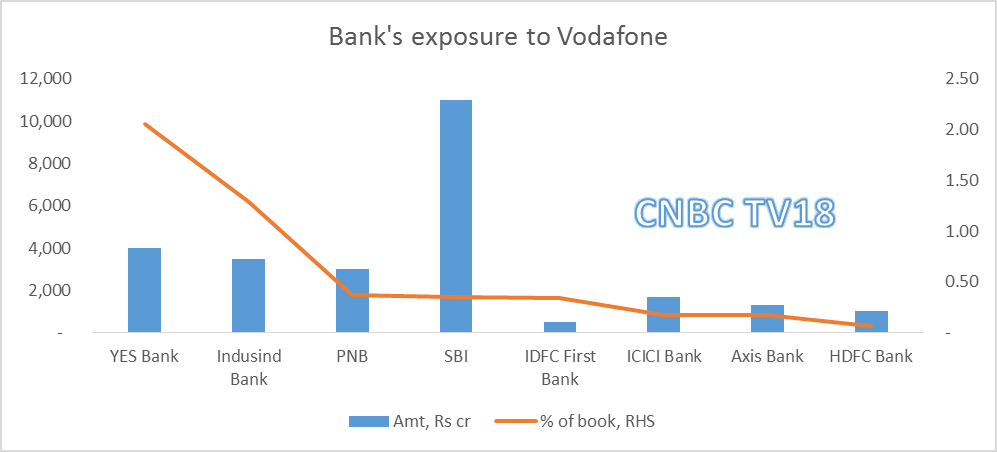

This is totally wrong …don’t blindly believe what these vested analysts project. Have you heard this quarter con call …they clarified they have less than 200 crores outstanding …which they are getting the money without any defaults …this is the fresh short term loan (500 crore approx ) which they have given last year after VI paid their dues

5 Likes

Why IDFC can’t distribute the shares held in IDFC bank directly to it’s shareholders (of IDFC)?

IDFC has no liabilities as such. It can dispose off all assets and distribute cash and shares in bank to its shareholders and get itself dissolved.

3 Likes

Market also knows that I think…

for example :

That is why it is pricing IDFC in such a way before dividends… i.e. IDFC First * 1.4 + 8 rs of dividend (after tax)…

I dont think IDFC will fall full 11 rs. on monday…

also you will pay Capital Gains tax twice on this 83 to 91 journey if you will sell it today and buy it at 83 again…

2 Likes

Whatever be the swap ratio shareholders of IDFC Ltd should gain a bit after the merger right.

Scenario 1

Swap Ratio of 1.66 which reflects the IDFC Ltd 40% holding in the Bank. Price realization for IDFC Ltd will be around 96 per share after the swap and after dividend payment.

Scenario 2

Lower Swap Ratio of say 1.4. This ratio will favor IDFCB as number of outstanding shares will reduce leading to higher book value per share which will lead to a higher price if valuation remains the same. However this scenario is also beneficial for IDFC Ltd because although they get lower number of shares the price of the shares will be higher. Of course this scenario is not as rosy as the first scenario but even in this scenario eventual price realization + 11 Rs dividend will come to around Rs 97-98

1 Like

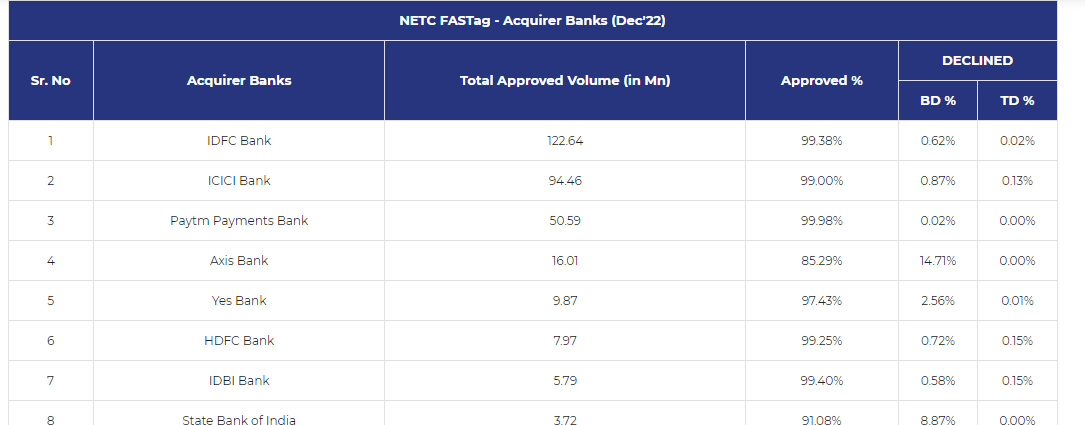

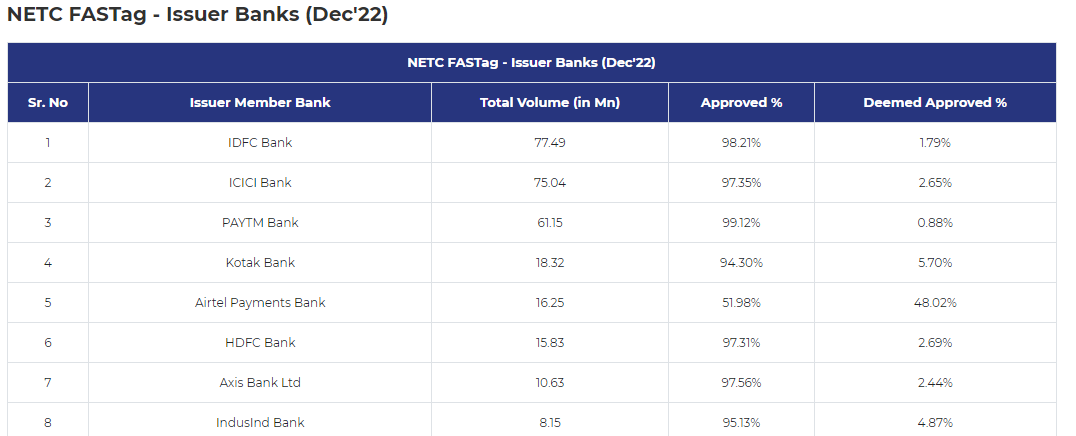

Is it true that IDFC first bank has highest market share in Fastag business. As per NPCI website, It has highest market share as issuer and acquirer also.

8 Likes

Yes, Tis the truth. Tis what the data shows us

6 Likes

Nitin Gadkari says they will be launching Satellite number plate tracking for Toll collection in next 3-4 months. Does anyone have any idea if that means Fastag goes away and the revenue from Fastag will not be in the banks bucket.

3 Likes

IDFC Bank is a partner of Amazon for Amazon Pay Later, can we as a shareholder ask what is the NNPA, and GNPA figures for this specific partnership? if not exact numbers, maybe percentage data.

Or

Can I find this information somewhere, in the public domain?

Currently you are paying a fixed amount to cross a tollgate irrespective of whether you go 1 km after the tollgate or 50kms. Obviously the people paying to just 1km won’t be happy. The govt is trying to implement a way to charge people based on the distance. But the fast tags aren’t going away. Hope it answers your question. Thanks

11 Likes