605 crore net profit.

450 crore provision in this quarter.

4 Likes

Good set of numbers.

NIM is not very clearly highlighted in the presentation hence putting it here:

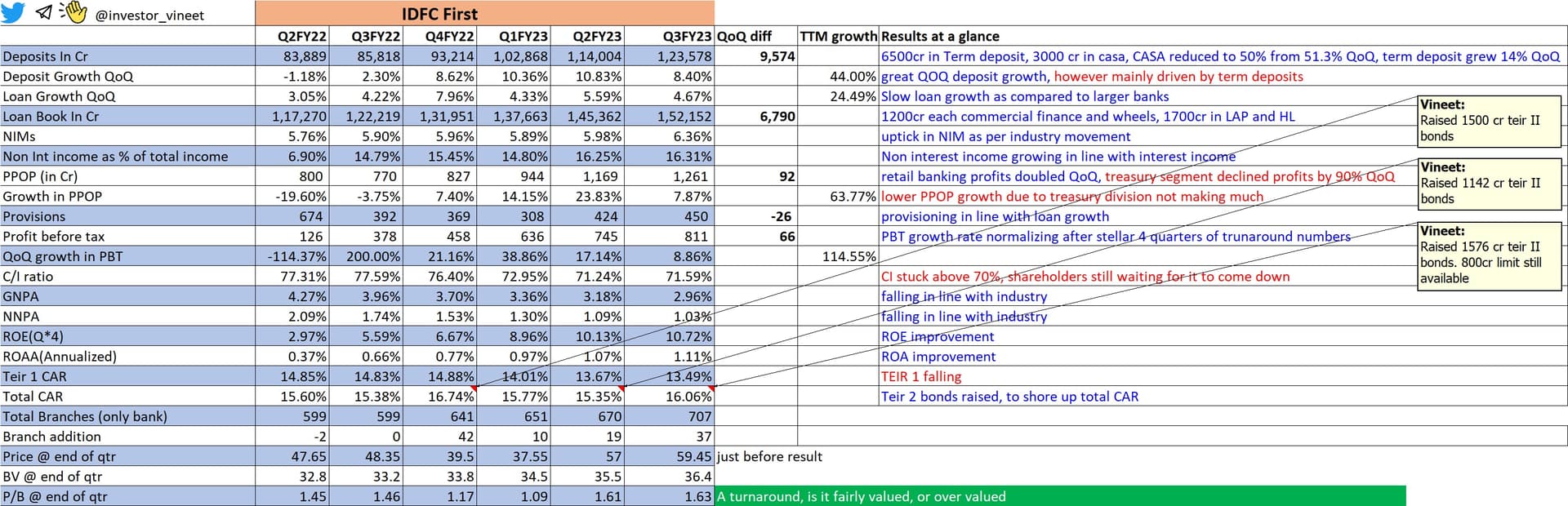

On slide #55: For Q3 FY23, the Net Interest Income grew by 27% YoY. Also, the NIM% (annualized) for Q3-FY23 stood at 6.36%

6 Likes

This quarter is where IDFC first has overtaken the second tier of banks like Bandhan bank, RBL bank, Yes banks of the world.

IDFC first bank is the only bank that is getting more deposit than the loans they give out.

Best part is they are aggressively raising Tier 2 bonds where dilution is stopped and Capital consumption is very very low even though loan growth is high. Capital consumption is just 1.3% were as Risk Weighted Asset increase by 4.4% this quarter where as loan growth is 4.67% means they are giving lower risk loans at the same time their NIMs increase from 5.98% to 6.36%.

I couldn’t ask anything more from the bank.

V V is very very categorical not to dilute further at cheap rates and hence aggressive in tier 2 raise.

37 Likes

Can anyone please post the link of the Q3FY23 con call. Thank you.

2 Likes

5 Likes

The results are very good. The machine is consistently delivering and now it’s been a few qtrs of consistently good loan growth and low provisions, percolating down to good profits. The investor skepticism will definitely further reduce post this result

| Jun-21 | Sep-21 | Dec-21 | Mar-22 | Jun-22 | Sep-22 | Dec-22 | |

|---|---|---|---|---|---|---|---|

| NII | 2,186 | 2,272 | 2,580 | 2,669 | 2,751 | 3,002 | 3,286 |

| Fee & Other Income | 449 | 658 | 744 | 841 | 899 | 945 | 1,117 |

| PPOP | 1,013 | 654 | 783 | 840 | 958 | 1,184 | 1,277 |

| Provisions | 1,879 | 475 | 392 | 369 | 308 | 424 | 450 |

| Provisions/Net Ret…Wholesale Assets | 1.73% | 0.43% | 0.34% | 0.30% | 0.23% | 0.30% | 0.31% |

| PBT | -865 | 179 | 391 | 470 | 650 | 760 | 827 |

| Tax | -244 | 68 | 101 | 118 | 165 | 193 | 210 |

| PAT | -621 | 111 | 290 | 352 | 485 | 567 | 617 |

| Net Retail and Wholesale Funded Assets | 108628 | 111353 | 116422 | 124075 | 132555 | 140239 | 147109 |

| CASA Deposits | 45896 | 46269 | 47859 | 51170 | 56720 | 63305 | 66498 |

| CASA % | 51.75% | 51.3% | 51.6% | 48.4% | 50.0% | 51.3% | 50.0% |

| GNPA | 4.61% | 4.27% | 3.96% | 3.70% | 3.36% | 3.18% | 2.96% |

| NNPA | 2.32% | 2.09% | 1.74% | 1.53% | 1.30% | 1.09% | 1.03% |

the management has gone about the transformation of this organisation in a near surgical manner. Attacking issues one by one, rightly prioritizing - focusing on liabilities before switching on the asset growth engine

COVID (retail NPA shooting up), unexpected credit issues (telecom etc.) were big challenges. In retrospect we can say that these were handled well

We still have issues related to the sustenance of

- stickiness of the high interest driven CASA and

- high NIMs with low credit cost

CEO is consistently explaining the reason for the same without changing the script. CASA rates are dynamic that can and have changed at will. The money has come…

the bank has broad based its products suite to improve customer engagement at multiple points - credit cards, not ignoring the corporate book - case in point

The organisation has developed over a decade an expertise in serving a customer segment that pays well – from Capital First times, this segment is now being served out of the bank instead of NBFC

The management has demonstrated the ability to capture the public interest by crisp and imaginative communication. high interest rates on deposits, crediting on monthly basis against qtr, getting AB as ambassador, 0 fees… backed by increasing branches and a good technology backbone… gives comfort that the bank will continue to get traction

Consistently reducing results announcement timeline is also a good step

Equity dilution is clearly an overhang, hopefully it will be accretive to existing shareholders – marquee investors at premium to CMP

18 Likes

For information & to compare with idfc first 6.36%

BANKS Q3 NET INTEREST MARGINS (QOQ) SO FAR

HDFCBANK ↔️4.1 % V 4.1 %

ICICIBANK ![]() 4.65 % V 4.31 %

4.65 % V 4.31 %

KOTAK ![]() 5.47 % V 5.17 %

5.47 % V 5.17 %

INDUSIND ![]() 4.27 % V 4.24 %

4.27 % V 4.24 %

FEDERAL ![]() 3.49 % V 3.3 %

3.49 % V 3.3 %

RBL⬆️4.74 % V 4.55 %

CENTRAL BANK⬆️4.07 % V 3.44%

BANK OF MAH⬆️ 3.6 % V 3.55%

UNION BANK⬇️ 3 % V 3.15 %

14 Likes

Excellent comments so far. However, nobody has touched upon the reason for vertical fall in treasury income. Is it due to RBI rate changes ? Is it real or notional ? What would be likely position in Q4 ?

4 Likes

Good Comparison; What are the main reasons for better NIM? or IDFC FB taking undue risk to get better NIM? Generally in Banks and NBFCs, NPA creap up after many years or operations. And many of the mistakes are committed many years before.

3 Likes

According to management in Q3FY23 conference call, higher NIM is due to expertise in providing specialized loans to customers at higher rate.

2 Likes

They were NBFC & was having a model of giving 16-24 % loan earlier . that model they are leveraging with some more strigent norms as bank they need to be more conservative and they do have access to low cost of fund

3 Likes

I am not a an expert on financials and learning quite a lot from the comments above. Appreciate all the inputs.

But can anybody draw a parallel between bank’s financial performance and the management creating shareholder value? Is it truly something worth holding on to?

(Invested)

3 Likes

In his CNBC interview VV did not answer the question about what percentage of the loan book is secured vs. unsecured. Instead replied that the unsecured is as good as secured due to availability of cash in the borrowers’ bank account which the bank can pull from when required. Does anyone know the numbers or have they been reported anywhere?

Disc: Invested.

6 Likes

Availability of sufficient cash in borrowers a/c. How can bank pull out with or without the consent of the borrower? The borrower can draw his cash from his a/c anytime, right? Though I am not a financial wizard, my common understanding is unable to digest this supported argument.

3 Likes

Banks have the right to take the cash out of the deposit accounts of the customers if their loan account becomes overdue. It’s not particular to idfc first bank but for all other Indian banks…

4 Likes

The larger point Vaidyanathan was trying to make was today the ways of evaluating a prospective loan customer can be done based on the cashflows they have vs traditional ways of doing secured lending. Cashflows are indicative of the EMIs they can pay and thus unsecured lending MAY not be risky. I am sure they look deeper than that however high level that was the point he was making.

6 Likes

Mr Vaidyanathan deserves full marks for the excellent performance. Bank numbers have matched the narrative set out at the time of merger, rather achieved certain targets early in spite of the covid. The management is very innovative. Mr Vaidynathan in his interview to CNBC has given a target of 6% NIM for 2024. So for the long term story is in tact.

12 Likes

Does anybody know IDFCF’s exposure to the Adani Group? Ideally it should be 0 as Adani group is mostly in Infrastructure but will be good to confirm.

2 Likes