A very large percentage of retail investors, apparently those who do not have a close understanding of banking shares seem to be assessing the IDFCB share by only looking at its balance sheet figures and comparing them with other private sector bank figures. Minus the narrative it is an incorrect picture. This has kept the share price subdued and therefore it continues to be an opportunity.

On the other hand the bank has created several potentially robust revenue streams like fast tags, wealth management, credit cards and now Digital Rupee. If DR concept takes off in the country, which is quite likely, IDFCB will have the first mover advantage. DR balances will carry zero interest, thus becoming a large, free of cost liabilities source. Most of our businesses in India need cash transactions as a matter of necessity, convenience and therefore preference.

Also heard from a branch manager that the bank is going to open 200 additional branches in 2023. Apparently a large number of existing new branches are crossing the break even point and turning profitable thus creating capability for more new branches. This however needs confirmation from other community members. If true, then it would be a big positive for sustained growth of both liabilities as well as credit.

On an average it is taking about two years to turn profitable for an IDFCB branch.

Opening 200 new branches in next 1 year can be just to achieve all the milestones of 5 year guidance given at the time of merger in December,2018 (one of which was 800-900 branches)…they mention that in every investor presentation so they won’t like to miss on any one parameter.

They have now aggressively started advertising for saving accounts…

All banks earn good chunk of profits from fees but if IDFC Bank is not charging anything then i am not sure how they are going to manage profits only by lending. But surely they will get loads of SA because of this.

Hidden charges will spoil the brand and relationship. I had an account with Bank of Baroda, They charged me 20 rupees per Quarter for SMS notifications which can’t be disabled. So went to the bank and closed the account.

IDFC here is differentiating it from other banks with No fee banking. I am sure it will attract sizeable CASA .

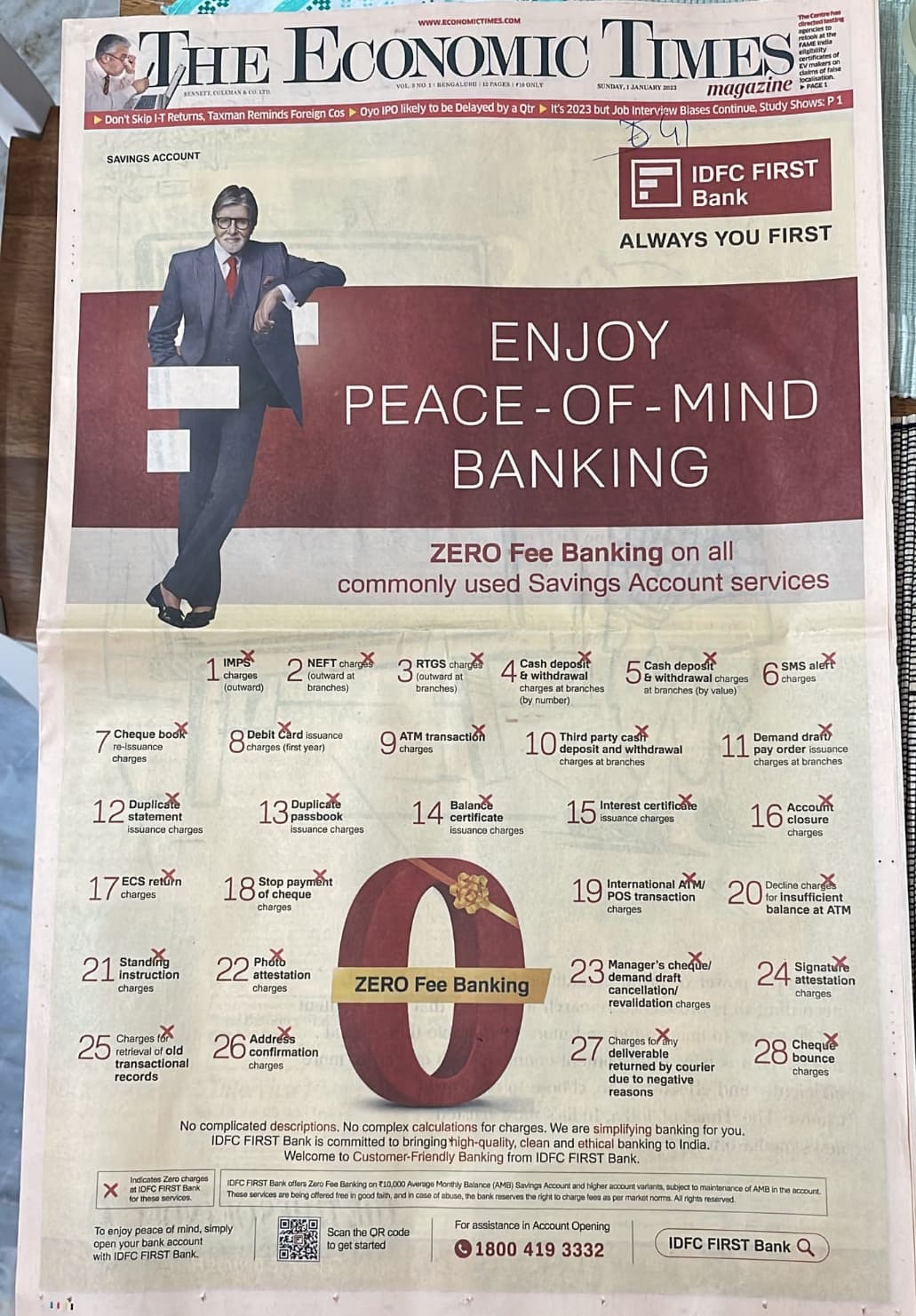

The full page advertisement of IDFCF bank is an education in itself. It brings out that there are at least 28 ways the banks can quietly and painlessly debit your account for various banking transactions one awails from time to time without giving any conscious thought about the cost.

It is certainly a comforting feeling if one visits service providers like a restaurant, hospital or a bank with the underlying confidence that the expenses will be without any surprise additions.

It makes sense to increase the low cost liabilities at the expense of fees instead of going for high cost borrowings or deposits. CASA is sticky and fees may be levied if required after sometime.

And competition for CASA is only going to increase because credit growth is higher than deposit growth as of now.

IDFC First Bank Limited so far has gained CASA based on higher interest rates. Such dependence may lead to volatility in CASA in longer term. Bank seems to be implementing a positioning exercise to delink such notion and project itself as no frills bank instead of simply a bank with high interest rates.

In my view, the practice of declaring quarterly provisional numbers should have been continued by the bank. The logic given the bank that they are going to declare the quarterly numbers soon and hence have not disclosed provisional numbers is flawed in my view. Even during the last quarter, the bank declared Q2 nos on 22nd Oct but still provided provisional numbers to the market(I don’t believe there was any Covid related disruption even during Q2). Once an institution begins a practice of giving timely data to the investor community, it should not be stopped. In my view it is not the best of the corporate governance practices where publishing of information is stopped arbitarily just because the management/board feels the bank has attained ‘stability’ in growth.

Even large institutions like HDFC, HDFC Bank, Bajaj Finance have continued to provide provisional data despite them being much larger and stable.

With respect to the point that other large banks like ICICI, Axis and Kotak do not provide the data, it needs to be highlighted that these institutions never did so even in the past during COVID too and hence haven’t regressed backwards on their commitment to provide timely data to their investors.

Was the practice followed just to provide stability to the volatile stock price of the bank in the past?

I hope this ‘biz as usual’ as pointed out by the bank doesn’t lead to stoppage of concalls too.

I recall in one of the concall Vaidya was asked to publish results on weekdays and give provisional numbers at the earliest. Regarding updates he told that updates will be discontinued because lot figures need to be reconciled afterwords.

Untill and unless some major shake out of retail investors happens in this counter it seems the bank won’t give good rewards to the shareholders of the bank. Please refrain from posting minute things about the bank.

I have Current Account with IDFC FB, I haven’t received any notification for interest on Current Account. A quick google search also doesn’t bring out any info on this. This is a game changer and I am sure the bank would launch it with maximum marketing.

They shall make f d Encash Fd when u need funds

U will get interest as per applicable fd rates for duration of deposit

They shall waive off premature encashment charges

Might keep a minimum balance

Process was followed earlier by citi bank

It is legitimate

The interest on current account is the facility of sweep in which is provided by Kotak Bank from many years.

I think this will be a superb facility as many business owners and NBFCs would shift to IDFC First bank as their rates are more than Kotak and service levels and technology too.