410 Crore of outstanding with Voda Idea. I think part of Toll NPA provision will be adjusted with it.

2 Likes

Mods please delete if not allowed.

So i found out an big issue with Pay later (IDFC is lending partner). tons of complaints of people paying dues on time still getting late fees. Multiple people took no loans but cibil shows loans issued buy IDFC and no resolution from bank. Another issue where peoples accounts got locked out of flipkart, then iphone order was placed (Pay later) and got delivered. the guy now fighting for it.

This is a big red flag for me . Can anyone help me understand why is IDFC First so deep into Pay later? This is just creating a bad name amongst a lot of people.

DISC - Invested with 10% allocation might trim after above observation.

6 Likes

In the civil score that shows loans are the limit which people have been provided in the Buy now and pay later scheme. If am not wrong the outstanding amount might be zero unless you use those.I think Buy now pay later is so popular of the ticket size and interest rate charged on it. May be 16%.

Disclosures: Invested

1 Like

In Q2 the bank had liquidated the Security Receipts issued by ARCs and inherited from pre merger IDFC bank and the consequent release of 200 crores worth of provisioning was not written back but transferred to retail provisioning as unnecessary caution (IMHO) otherwise the profit for Q2 would have been higher by 200 crore.

The bank nifty is meanwhile moving ahead and would provide tailwinds to positive triggers brought out by Q3 and Q4 results. It would therefore be prudent for IDFCFB to avoid excess provisioning in Q3 and Q4. This would help the bank improve its results and consequently pushing market capitalisation.

The bank needs to raise additional tier 1 capital after another couple of quarters. At that juncture a good market price would keep the equity dilution to a minimum. This would become a permanent positive for medium term as well as long term. It appears that the bank management is going in the same direction.

12 Likes

IDFCFB is setting a trend by coming out with Zero Fee Banking with charges have been completely waived in 25 services. Some of the services include cash handling charges, NEFT/RTGS charges and SMS alert charges. It may not force other banks to waive charges but IDFCFB is becoming more aggressive and taking competition head on . Good move in my view. It will attract more CASA.

16 Likes

Dear contributors , This thread is getting polluted with Credit cards, banks marketing news and their offerings. This is no way helping to know about the company. This page is becoming a grievance portal. Please refrain using the page as IDFC banks customer service. Please discuss the financial and stock related activities.

46 Likes

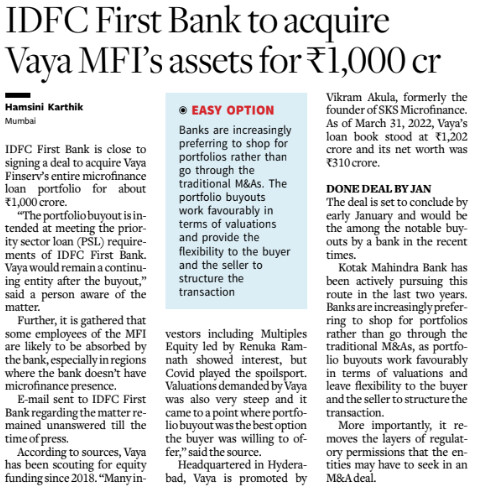

IDFC First Bank is close to signing a deal to acquire Vaya Finserv’s entire microfinance loan portfolio for about ₹1,000 crore** . “The portfolio buyout is intended at meeting the priority sector loan (PSL) requirements of IDFC First Bank.

Source: Hindubusinessline

4 Likes

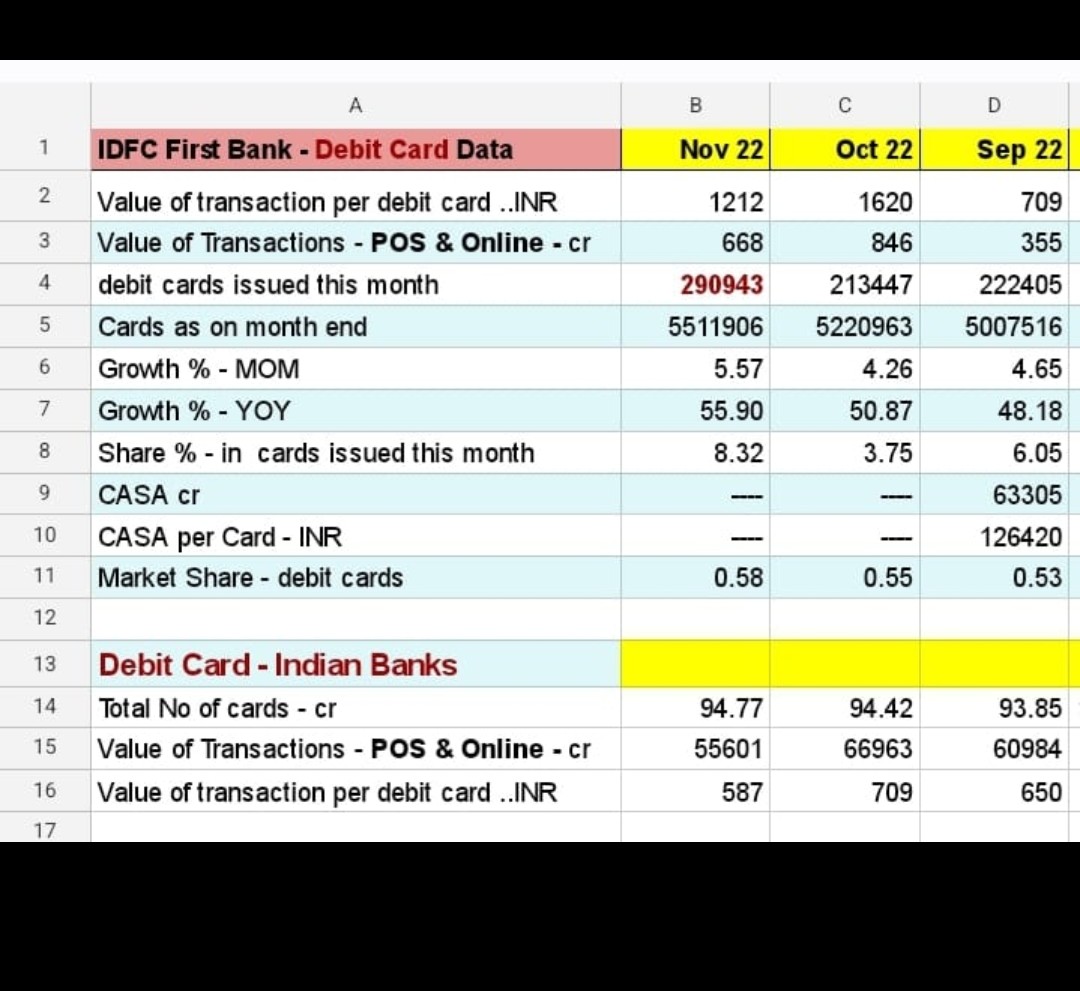

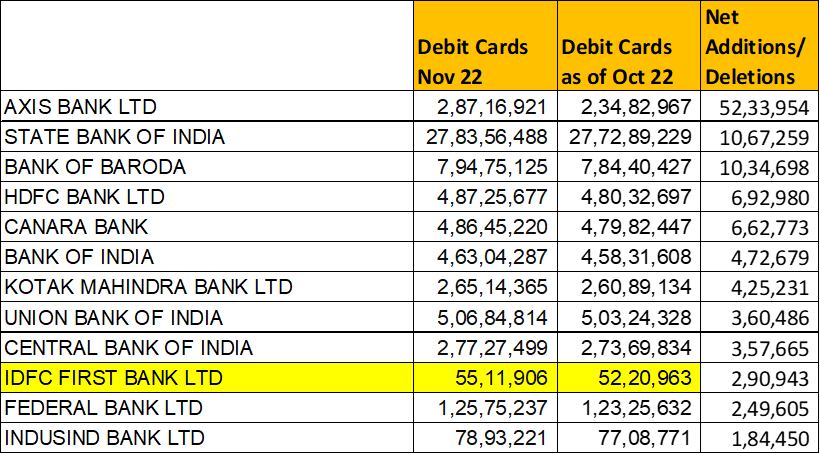

Good Addition in the Debit and Credit card numbers in the month of Nov 22.

81k in Credit cards and 2.9L in Debit cards.

2 Likes

5 Likes

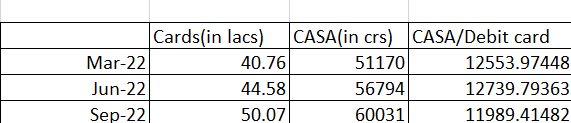

Just some number crunching of RBI data on cards and bank’s reported CASA in the past. My analysis says there is bound to be some correlation between the 2(although not linear as there are a lot of other factors affecting it). Number of new debit cards issued should ideally be associated with new account openings. If past data is looked at, I get the below trend:

CASA per issued debit card for the last 3 quarters has a value of Rs 12400/debit card(average). Till 30th Nov’22, the bank has 55.12 lac debit cards outstanding(vs 50.07 lacs in Sep’22). Assuming that the bank adds 2 lac cards(at a minimum) in Dec’22, we will arrive at 57.15 lac cards for Dec’22.

Assuming that average CASA/debit card further trends down to 11600, we are still looking at a CASA of Rs 66300 crs for Dec’22 which will be a 10.5% QoQ growth in CASA.

Waiting for the quarterly update in the first week of Jan’23.Expecting the bank to report yet another stellar quarter for growth in Deposits and Loans.

18 Likes

Wanted to highlight that lot of CA comes from Corporate Customers and the quarter end CA can be very different from average CA. So unless Retail CASA details are available, the analysis may be incorrect.

Disclosure : Not Holding any position. Have exited with a decent profit.

1 Like

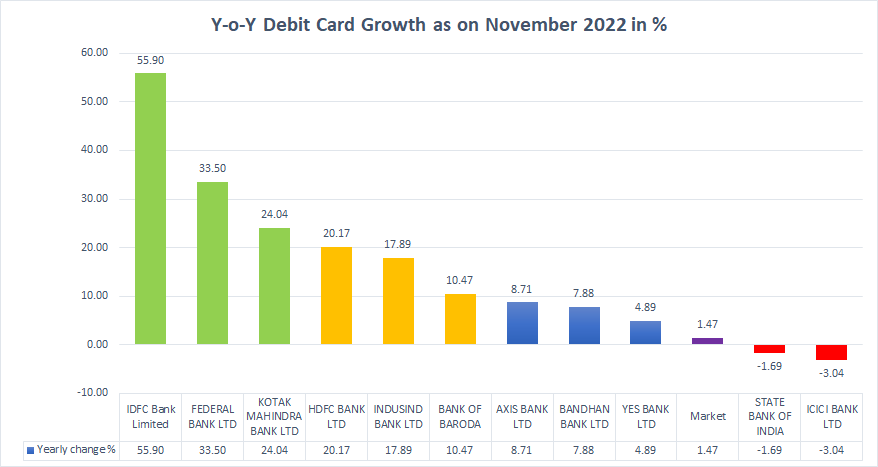

What is heartening to see is the incremental share of debit cards. Which basically shows the strength of the caSA Gathering franchise.

Every 1 in 12 cards issued in November was from idfc first bank. For context its overall share in credit is around 1-2% india wide. Definitely punching above its weight at least in liabilities gathering. This is specially interesting given that the casa & fd differential between idfc first & hdfc has been narrowing. Incremental money may not be coming just for the higher roi but possibly for the higher customer satisfaction & engagement

18 Likes

Recently I interacted with the branch manager of idfc first bank who is my friend’s friend. I enquired about the business and environment and work culture in the bank. Here are the takeaways.

The first and foremost was NPA , he told me he has 860 sme accounts and each and every account is standard and not a single account is over due and has never been over due.

The average interest rates on offer is upto 3 lakhs it’s 20 to 24 % and above 3 lakhs it’s 18 percent. No wonder their nim is 6%. Their customers small kirana store owners , bike repair mechanics and other small scale business who normally dont get bank credit. The turn around time is 2 days. If they are able to keep this book clean then there is no stopping for them. They followup agressivly even if the account becomes over due for even a day. So what Mr vaidyanathan saying regarding their asset quality is correct as per what is told to me.

Another thing is cross selling. They don’t do agressive cross sell. Recently it has been a norm in sbi ,hdfc and axis Bank to sell insurance policies which is nothing but organised loot. They deduct 30% commission on the first premium. If you asked the employees of those three banks they will say how stressed are they to sell these loot products. It was icici bank under Chanda kochhar who pushed the bankassurance but after Mr bhakshi takeover as CEO they completely stopped agressive misselling. Why I’m emphasing on this is misselling erodes the customer trust in that bank. Soon sbi and hdfc will also realise this. No wonder the ICICI bank is a star performer for the last 4 years.

Idfc first bank will gain the trust of the masses if they continue on this clean bank plank. Because misselling will ruin the life savings of senior citizens middleclass people. And the pressure of crosselling will make the lives of employees miserable as hell. They will resort to cheating the customers which is not at all good for the bank. Happy employees will contribute more to the growth of the bank.

All in all what I can conclude is for idfc first bank the key competitor is Bajaj finance and other nbfc players. They are playing where nbfc’s making their bread. It has the DNA of NBFC and advantage of a bank.

Diclosure : invested

27 Likes

On the cross selling part, My opinion has changed recently. Off late their employees promotions are linked to the cross selling sales numbers.

One of my friend’s brother is a sales and branch executive in a Semi-urban(Town with 1lakh population) branch in Andhra Pradesh.

Off late he keeps calling me, my parents and friends to take Bajaj Allianz health Insurance thru him. He keeps telling me that his promotion to deputy manager in January is partially linked to the Insurances and wealth management products he sell to the potential customers.

Upon his continuous follow up, I told him that I will take Term insurance for my younger brother but not this Insurance & Investment mix product. Two days later he said the commission % on Term insurances are low and his manager was not so keen on getting such policies on boarded.

Disc: Invested

16 Likes

Scuttlebutt analysis.

Recently, a relative of mine bought high end expensive bike. He wanted to get vehicle loan from idfc first ( as idfc first is one of the loan partner banks for that bike franchise ) , but as per him, idfc first’s due diligence & documentation was bit tough, they wanted good checks before loaning a customer.

So,he took loan from retail NBFC giant, who gave loan without any big due diligence, & quickly too.

His analysis,

Idfc first has far far better due diligence process than NBFC giant: 1-0

He was so impressed with representation & behavior of IDFC first employees that he eventually opened a savings account with idfcfirst - far better Customer service behavior- 2-0

Disc: Invested

17 Likes

Bajaj

Their interest rates ( at that vehicle franchise) are 2% higher + 3% processing charges.

However, very limited documents, no home visit. And quick process too. Risky.

3 Likes

Based on the MOM additions they are in top 10 now.It should only improve from here since I see lot of messages in social media of people being fed up with other banking apps and suggesting to moved over to IDFC.

Interesting that the gap of rate of Interest offered compared with other top banks is also narrowing.

9 Likes

IDFC app gaining traction !!

4 Likes

Its not risky. The expertise of bajaj finance is that they have the data of maximum people from our country. As per them the customer was not risky. And dont doubt thier data or thier underwriting skills, the continuous low NPAs from last many years confirms the same. At the end of the day they ended up giving him the loan at higher interest rate and at higher processing fee.

Disclosure: Invested in idfc first bank, transactions in last 30 days.

9 Likes