The Bank is raising funds via CD.

2 Likes

“IDFC First Bank was an early adopter of the EV market and has established itself as a bankable partner for Ather’s customers. This has become a critical cohort as the company is expanding into Tier 2 and Tier 3 cities.”

12 Likes

.

IDFC First has the potential to turn into a bank with a true fintech company halo around it…

12 Likes

2a073d20-899c-47a2-af13-8ec04b944617.pdf (746.3 KB)

.

This can alleviate fears of equity dilution to certain extent if I am not wrong… ![]()

10 Likes

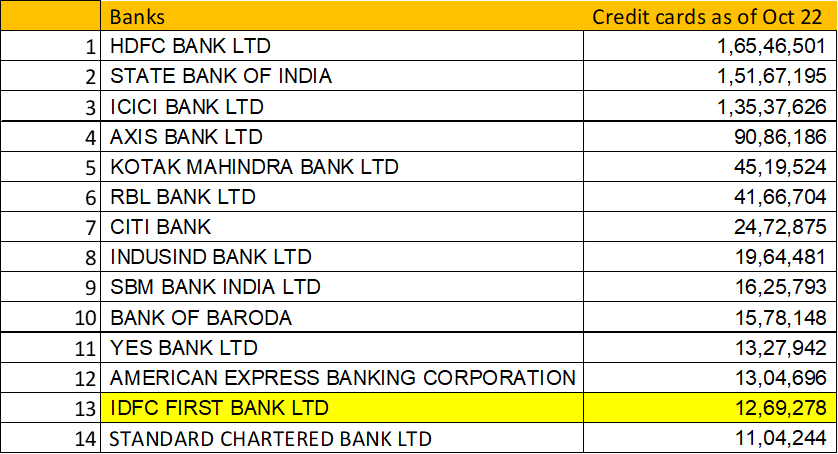

There are few things that takes years to build up. After the NPA cleanup and provisioning done by all the banks during Covid times, this issue has been sorted and in healthy state for all the Banks however, Credit Card business requires years to build-up.

- The offers provided by the top 4 in the above list is usually very lucrative.

- If you visit any mall, shopping centers, you will find sales people of these companies irritating and shamelessly asking you to get the CC. That’s the nature of CC business.

I do not see a huge amount of innovation coming up in the credit space and it is over-saturated. Naturally for IDFC to build-up and reach top 5 is going to take a while.

There is no specific USP of IDFC FB CC which is so attractive that they can snatch existing customers of established banks.

Neo banks and other new age digital companies are trying real hard with some unique propositions but given the risks involved, RBI is very cautious about not spoiling the spending habits of the Indian population which is healthy for our economy.

I would avoid being overoptimistic on the CC business.

PS: I hold IDFC in my portfolio, have multiple savings account in my family and CC as well.

9 Likes

One thing unique about IDFC First is the customer friendly attitude of its employees. A friend I lost to corona used to tell how they always came forward to help.

I have found the atmosphere in smaller banks and smaller branches more friendly. I remember a branch of Lord Krishna Bank in our neighbourhood. they merged with HDFC. That of course is the largest private sector bank with more stuffy attitude.

If leaving my present bank, a big private bank were not so cumbersome, I would have opened an account in IDFC First. As I have written in a separate post, never underestimate how a customer comes to view a company. And this is bound to reflect in its annual report too.

Two examples would illustrate this. I have opted for my pension account in a private bank because I have seen how govt babu like attitude the PSU Bank people have.

Then, people used to prefer Vistara though its tickets were costlier. Search in Google, the most unfriendly staff in the whole airline business was not that of Air India, though they are no angels. Experienced people always advised you to avoid Air Asia.

May be the soft-power of IDFC First will also have its say.

17 Likes

The 1500 crore issue was over-subscribed and saw interest from long-term investors such as pension funds and insurance companies:

9 Likes

14 Likes

IDFCFB credit card is not easily available to the masses. IDFC First Wow asks for FD and others need pre-approval. I don’t think there is a system to approve based on CIBIL score.

HDFC, ICICI, SBI etc in comparison have simple approvals (without FD, Savings account)

Don’t know why a mid sized bank looking to expand so aggressively doesn’t have easy procedures for issuing credit cards.

8 Likes

IDFC First Bank simply granted me without my consent a credit card, as I was having a One credit card, it was backed by first bank. I had a terrible experience for changing mobile no associated with the card. Here I want to bring two things. One approval and sent a card without any consent. I never attended their marketing calls. Second, the software development team do not enforce simple device recognition for mobile change request. And there are ample no of people singing hymn for this bank.

4 Likes

IDFC First wow seems to be a secured credit card. If you deposit say X amount as FD for 366 days @ 6.5% FD, they will give you a credit limit of X amount. So, a very secured way of lending and it will be issued to anyone without checking credit profile in minutes.

This strategy has it’s pros and cons.

I don’t think IDFCFB will get good quality customers with this strategy. It is attractive to only people with no CIBIL score or low CIBIL scores.

3 Likes

8 Likes

They are raising capital at a coupon rate of 8.7%. I understand that deposits are scarce right now and capital is needed for growth by all banks, but this coupon rate essentially means that the entire profit driver of replacing legacy bonds with low cost deposits is on hold, for the moment. Any idea if this is a high rate vis-a-vis other top banks?

1 Like

I think this would fill a need gap in the card market. Senior citizens with low pensions but high FDs, Widows without regular income but having FDs and similar such persons can get high limits on their cards. This will help them to meet travel and medical requirements.

2 Likes

This is subordinated debt … so this adds to capital Adequacy ( can be leveraged by the bank to lend approx 8 X).

The earlier legacy infra debt of 8.8 person was plain debt, not subordinated debt, could not be leveraged.

So the two are not comparable.

12 Likes

Most senior citizens of current age including my father stick to Psu banks due to there past experinces although idfc differentiates itself from other banks in terms of charges but most old people i know are reductant and many have to changed with times ,One person i know who is old and uses credit cards uses it for travel reward it comes with and all the amenties it comes with and when it comes to rewards axis and hdfc are miles apart compared to the Idfc Fd card.

3 Likes

What you say is true. Even if the PSU banks interest rates on FD/Savings account are abysmal people stick to it since capital is protected. I myself suffered when yes bank moratorium was imposed and all my life savings was frozen. So I understand why people are reluctant to put money in private banks.

However, IDFC First bank’s savings interest is quite good and they are the only one who credit the interest every month. This will be like drawing salary for anyone, esp a retired person with a good retirement lumpsum money deposited in SA.

(1cr in this savings account will get approx 50,000 per month credited as interest by the bank)

Disc: I’m not retired. I’m in early 40s.

11 Likes

1fa49f37-b236-4c1a-9d7f-a2017c13e3a3.pdf (2.9 MB)

‘India Ratings & Research’

(“Ind-Ra”) has revised the Outlook on IDFC FIRST Bank Limited’s debt instruments (Basel III Tier 2 Bonds,

Infrastructure Bonds and Non-Convertible Debt Instruments) to ‘Stable’ from ‘Negative’ while re-affirming

the ratings at ‘IND AA+’.

8 Likes