Can you please share what you mean by this? Cost of funds for idfc first is now 5.2% blended (including 22k cr of high cost legacy liabilities at around 8.5-9%).

HDFC bank for comparison is at 4.2%. I would not be too surprised if idfc bank converges to within 0.5% of HDFC within 2-3 years. Do you think that makes a material difference to what sort of customers they are able to target?

Retiring the legacy book is the easier part of managing cost of funds. The tougher part is when legacy levers are all used up and one still has to pay higher interest on SA to keep CASA at 48%+. Real CASA strength is when the bank does not incentivize customers through higher rates, yet customers park their savings with the bank. Like an HDFC Bank, Kotak Bank or an ICICI Bank today.

The lending rates are determined by competitive forces, a customer would rather go with a large bank at 8% rather than go with a mid sized bank at 8.25%. Lending is a spread game for the most part, a 0.5% differential is huge on the cost of funds side as the lending rates are fixed by market forces. This 0.5% difference is what translates into higher NII and eventually the ROA. The last leg of 0.5% is not easy to make up.

In such a situation, to grow the lending book (without lower spread) banks with higher COF will have to look at segments where the customer is willing to put up a higher spread. Else in every quarterly conf call analysts will ask management about lower NIM’s and why HDFC Bank has higher NIM at lower NPA. This perennial treadmill forces banks into mistakes over a period of time as every management wants higher market cap and the best CEO award - which is usually given for aggressive growth and not for managing risk well. Customers put up higher spreads only when they do not have better alternatives, this is where risk gets introduced incrementally over time. Eventually a bad cycle for such a customer segment comes in and NPA’s start spiking.

It’s a slippery slope for mid sized banks if they have aspirations of become a large one. Some South India based NBFC/banks have good asset quality only because they don’t have aspirations of becoming a Top 5 bank. They are happy to run their own race but their valuation multiple suffers due to this. It is a trade off that every financial institution needs to reconcile and execute well on over time.

Going by VV’s persona and statements, he has high growth aspirations. This is what gets the market wary about over the top statements. Market generally loves confidence from the management, but with banks it introduces a bit of worry too ![]()

I feel IDFC first is not competing with the leading banks. Its competing with nbfcs, the lot of them.

And it’s winning hands down. With a long track record of NPA less than 1.5%

Only formidable opponent, competition, is Bajaj Finance.

I feel, retail lending is still a raw untapped market because lending happens at 20% plus. Healthy Growth of 20% is not an issue.

Just to add on to casa point, the casa usually grows as ur customer gets older. For the reference you can check you own saving acct balance 5 years back, 10 years back and 15 years back, i am sure ull get number in some multiples.

Same happens with every branch a branch which is 1-3 year old will be 1x casa while a 5 year old can be 2-3x casa, a 10 year old branch can have 10x casa and 15 -20 year old branches can have 30-60x casa from their opening year.

So its more of a game of longetivity rather than interest rates.

Longetivity comes from salary accts and home loans. Thats where the focus should be if u want to have good casa in long run, high interest rates are just initial jump start to catch what they dont have, in long run probably above should work around.

Agree, that’s where every bank would want to be over time. Which is why cross selling payments, cards, wealth management and other services come handy, these lock in customers into regular usage and build in switching costs that prevent customers from moving to another bank.

All this takes time, normally takes 2-3 years for a branch to turn in operating profits and around 5+ years for the book to start contributing meaningfully to profits. But once a threshold is reached, profitability is non linear due to a confluence of factors since cost escalation does not keep pace.

Which is why comparing per branch revenue, CASA and profitability with a leading bank is not fair. Even within these large banks, their seasoned branches subsidize the lower throughput from semi urban and upcoming branches. A bank with 50% of the branches opened in the past 3 years will have high operating cost until it hits a threshold size on assets and fee income. But once it hits, operating leverage kicks and spikes the return efficiency rather quickly so long as provisions don’t spike too.

The key is to survive for a long period without credit events that can damage the asset quality significantly.

If you or anyone can share how much of their current overall housing loan book and current quarter growth is from developer loans and how much from retail, would be helpful…

Also, these Home loans will have tenure of 10/15/20 years and IDFCFB will have lots of opportunity to cross sell other loan products i.e. Vehicle Loan/Personal Loans/Credit Cards etc. This is good strategy.

It seems IDFCFB as well as a few other banks have put Spicejet loans on high alert.

Is anyone aware of the exposure to the airline? It would be a pity if yet another large legacy loan had to be provided for and ROEs get dented yet again.

I tried looking, but the only thing I could find was in SpiceJet’s FY21 Annual Report:

During the previous year, the Group had taken a loan of Rs. 500 million from IDFC First Bank Limited. The loan is repayable after 3 years from the date of the borrowing and carries an interest rate of 12.35% per annum. The loan has been secured by first pari-passu charge on the land of the Holding Company and one of the subsidiary (Canvin Real Estate Private Limited) and pledge on equity shares of the Holding Company for 1.0x of total facility. The loan agreement requires the Holding Company to maintain debt service coverage ratio of 1.25. The Group have not complied with this financial covenant and accordingly, the borrowing have been reclassified to current maturities of long term borrowings.

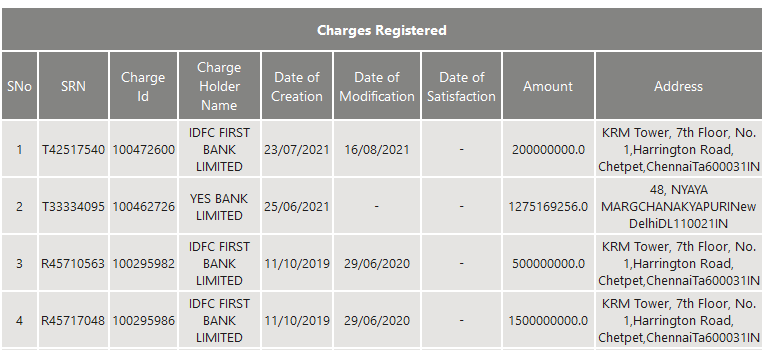

At most 220 cr. pleaase checkout the zauba charges analysis i had done a while back. Total charges created to date are 220 cr. Outstanding amount would be lower (spicejet has been paying all loans well up to date).

Also it is imp to understand that this reminds me of VI episode (banks are being conservative in calling out cashflow mismatch up front rather than wait for it to turn GNPA)

This is a non-event IMO. Not even 1% of the corporate loan book.

The bank has responded by saying that outstanding exposure is 46cr only.

Disc: invested, biased.

Atleast 220cr exposure as there might be additional exposure via NCD’s that don’t show up on the MCA website. All after 2019, so post merger and not legacy loans-

I think people do too much speculation. Here is the official statement from the bank

imp

sourse-fb link

An interview with IDFC First’s CFO, Sudhanshu Jain.

all private sectors banks result at one place.

source - internet

Top private banks Q1 results in one place_compressed (1).pdf (615.0 KB)

IDFC First Bank at Emkay Global’s Confluence, an Annual Conference.

V. Vaidyanathan, MD & CEO and Saptarshi Bapari, IR

10th August 2022.

Key Meeting-Takeaways:

-

Management guides for continued focus on increasing share of the secured retail portfolio and expects loan growth at 20-25%. The bank has issued +1mn credit cards since Jan 2021, with the credit card book now at Rs23bn. For the bank, the focused growth segments shall be Home Loans, SME and LAP.

-

CASA ratio remains stable at 50%, leading to lower CoF; the bank has thus been able to maintain industry-level high margins at 5.9%. Higher cost-to-income (C/I) ratio remains an irritant, but should trend down to less than 50% from the current 75%, supported by faster growth in income at 30% and slower cost growth at 20%.

-

The bank remains confident about the improving asset quality. One lumpy toll-based project (Rs7.8bn), which slipped during Covid wave-2, is expected to be resolved within the next 2 years and thus help to improve GNPA ratio by 50bps. The bank guides to credit cost at <1.2% for FY23E, due to strong recoveries, and should thus support profitability.

-

Covid has caused a hiccup, but the bank’s long-term strategic focus remains on maintaining credit quality, bringing down C/I ratio and reaching an RoE range of 13- 15% over the next 3-4 years.

*We believe the bank has done well on the liability front, but sustaining the momentum in a rising-interest rate scenario as well as bringing down cost ratios will be a key monitorable.

Just one statement from him that there are no legacy issues left to be accounted for. Stock up 40 to 50 pc from rs 30 or 35 Its insane how much people trust the man. Ive been critical of low profits for a while now, yet i grant the amazing credibility. Thanks… any insights if you truly believe that all infra and corporate accounts are disclosed and accounted for will help in my feeling better about the future. Retail looks fine … as per june 22 gross is 2.1pc and net is 0.9 pc which it was for a long time pre covid so i feel more comfortable about that part as the trend line is also good and infact trending down.

The premium between IDFC and IDFC First Bank has been reducing almost everyday and currently stands at 31.5%. Depending on the holdco discount negotiated between the two boards(at a minimum I expect it to be 12-15% and on the higher end could be 22-24%), the premium could range between 28% to 42% as we head closer to the merger.

The premium reducing is actually great news for IDFC First Bank shareholders as it means that the bank could experience higher capital reduction and hence a higher book value and higher EPS post merger.

July Credit card number is out.Another fantastic progress for IDFC Bank.Month on Month added 80k cards…