Most likely the cash received from sale of AMC by IDFC will be invested in IDFC FB (approx. 4k crore) before reverse merger. It might be done at a price and swap ratio which will be beneficial for both IDFC and IDFCFB. Though it will not be immediate by most probably in next 2 years.

6 Likes

2 Likes

I think few people in the media and few brokerage houses purposefully belittling the performance of the bank. They won’t appreciate the bank even when it posts highest profit in their history. They are perennially bearish on this stock.

3 Likes

Don’t know about media, but brokerages don’t know valuation at all. They will give lower target for stocks in downtrend and vice versa. This is what I’ve learnt in my little investment journey so far.

10 Likes

considering consistent profits from now on , this year profits will come around 2k cr, at a P/E of 25 (which is reasonable if book grows at 25% cagr) valuation comes around 50k cr , share price of 75-80 comes as the intrinsic value of the stock. what is stopping markets from rerating?

one thing i feel is idfcb raising capital at cheap valuations which hurt the company fundamentally

2 Likes

P/E might not be the best metrics to value banks as they tend to be cyclical. I think Indian market has not experienced this cyclicality in the private bank as some private banks have been able to capture increasing share from public sector banks even during lean years.

It is difficult to see IDFCFB getting valuation of higher than 1.5 P/B when banks with higher scale, profitability and consistent track record are also available at cheaper valuation compared to historical trends.

I believe larger Indian banks should start to narrow valuation premium with global banks over next 3-5 years as Indian market get more integrated with global capital market with growing size.

What will be incentive for someone to own combined HDFC bank at $200 billion valuation when larger and more profitable American banks are available at cheaper valuation.

Indian banks might have higher growth but valuation premium will start coming down with decreasing incremental growth especially in dollar terms.

5 Likes

I think due to the above stated reasons and global sell offs, the FIIs sold HDFC twins and most of the Indian banks from last Sept and DIIs and retailers are still supporting it. but how will a retail invest in the likes of BOFA, WellsFargo…, no other choice he will keep investing in India, a known devil is better than an unknown angel.

Over 60% of Banking accounts just use the accounts as a piggy bank where no more than 4 transaction happen over a months time, hardly 2% of Indians invest in stock market,… can u imagine the money that will come to banking system and stocks in next 2 decades? were will the money go ??

HDFBank apps sucks big time, ICICIBank hidden charges will chase any honest retailer… I am customer of these two banks from past 2 decades , closed ICICI completely and have almost zero transaction with HDFC … Made my spouse open account with IDFCBank, oh these guys are so focused on customer needs and their app is awesome , ROI on deposit is mouth watering what more do i expect?

I believe that IDFCFB can give a run for their money to any big banks…

9 Likes

Fy19 core ppop was 1105 cr

In 3y it has become 2753 cr (36% cagr)

Our credit loss for last year was only 2.5% despite moratorium & covid 2

This year guidance is only 1.5%…can imagine what that does to RoA

Core ppop now 1000 cr / Q even if we take credit costs of 1.5% it takes us to a great profitability. It is our read that our bank will never post a loss in its life

RoA is 1% & trending upwards. A good number is 2%. Direction is to be taken note of.

Will get to double digit roe before q4. Advancing the guidance to getting there in Q2 or Q3.

Lumpy assets to deal with, couldn’t push it under the carpet.

Retail book is now 1 lakh cr. Mortgage is 33% of the retail & commercial loan book.

Credit card spends increased 20% sequentially

Infra book 6700 cr. 4.9% of total funded assets. Was 22% at merger.

Total customer deposits at 1 lakh cr

651 branches. 10 branches in current Q. 50 in last 1 year

High cost legacy borrowing of 2700 cr paid back in q1. Total now is 22k. Paid back 5700 in last year

Provision coverage ratio at 73% compared to 70% in last Q & 60% last year

Slippages: lower by 20% on sequential basis. Net of upgrades lower by 25%

Trending around long term sustainable targets

One large retail chain group slipped to gnpa that increased gnpa. Already 100% provided for. 550 cr.

Fee income increased 100% YoY. 899 cr. Covid base. Sequential basis increased 7%. Retail fees contributed 92%. Very granular. Fee income from toll & credit card at 68%

Had a treasury/trading loss of 44 cr. Bank proactively tightened limits, reduced treasury books, modified duration of the assft book at 0.84 years

Core operating income increased by 39% YoY. Operating expenses increased 31% YoY. Decline QoQ

C/I at 72.95%. Increased 325 bps QoQ

Annualized Credit costs in Q1 was 0.9%. Annualized RoA was 1%

Capital adequacy is at 15.77 %

Nii growth at 3% QoQ. Nim down QoQ. Lag in passing on rate increases. So we should be in upward trajectory in Q2

No one offs in provision. We see no reason why credit losses should go up in next 3Q. Could be in 1-1.1% range reasonably. Barring unforseen circumstances

Every Q opex will go up a little bit. Depending on disbursals. Could go up marginally every Q from here on. Normal collection expenses

Blended cost of funds in saving account is 5%.

Cost to income or cost to asset high due to vintage of branches. When these branches really scale up from here cost measures will measure up with other banks. Asset side opex should be a bit higher due to product mix but offset by the higher NIMs. Our cost to income in home loan might be 90% since we just started. Credit card cost to income is 130-150%. That’s how businesses are built.

We spend 2-2.5cr to maintain each branch. 650 branches.

As a bank we just started the cross selling journey

Throwing the best offer on the RM screen

If we bring down cost to income by 10% the RoE will jump by 5%. In long run want to be around 55%. In 2 years it should materially come down to 65%

High cost liability should give us 750 cr pbt

No plans to raise deposit rates right now.

We have not passed on the rate increases to customer yet. Comfortable to maintain NIMs around 6%

Tech costs to plateau from here. Tech costs are a bit higher due to vintage of bank. App, cash management, current account management we have been building

For our kind of bank 2% RoA is a bit of an under ball. (Can do better)

Unsecured vs secured is one dimension. Lending has to be cashflow based. Personal loan to infy etc does very well. No moratorium. 2W business is secured but does badly in economic downturns. Evaluate for cashflow. Cashflow is paying you back equity is not paying you back

Wealth management, cash management, toll collection will scale up

Blended costs is 5.2%

37% is linked to external bench marks. 63% is fixed rate book.

We don’t have a 0 balance product. Quality of customer is very very important. Minimum balance is 25k but customers typically bring in 1.8L etc

great questions from @ishanagarwal89 bhai in the concall. Looks like we might hit 10% RoE in q2 or Q3 & exit fy24 with 15% RoE headed to 18-20% RoE in fy26 end

17 Likes

MANAGEMENT COMMENTARY

V. VAIDYANATHAN

- You’ve been a very patient investor with us

- You passed the test today

- We’ve come a long way

- We can now say the foundation is very big for the bank

- We are able to raise deposits very comfortably now.

- Deposits grew even after covid, even after dropping of rates

- Quality of customers, Quality or origination has improved

Lending Side:

- We already had a tried and tested model

- That machine is holding well

- The ability to disburse as well as quality of disbursements

- SMA0, SMA1, SMA2 all are not only at pre-covid levels, but is now better

- Lowers SMAs = Lower flow into NPAs

- Asset Quality numbers are looking good

- We are very confident that credit loss for the year will be less than 1.5%. All of this has a basis.

- Asset Quality numbers are looking quite good.

Profitability:

- If you’ve noticed, over the last 3-years, loan book hasn’t grown much, 3-year CAGR, has grown by 6%

- But ex-treasury pre-provision operating profit, FY19 – the annualized of the 2nd half, post-merger, was 1105 crore.

- Now 3 years have gone by, we have spent a lot of money building various capabilities and all that, it has grown to ~2753 crore, at a CAGR of 36% - this gives us confidence in the business we are building.

- According to our internal modelling, by FY23, it should add by another 45%. By FY24, another 45%.

- This really augurs well for the bank

Provision:

- Despite 2nd wave, where there were no moratoriums, and we had to take all those provisions, our overall credit loss was only 2.5%.

- We are guiding this year for 1.5% and we will beat that very comfortably.

- This reduction in credit loss, you can imagine what it will do for our RoA and RoE.

- Significant event that has happened has the Pre-provision Op. profit was 986 crore – this gives me a lot of confidence

- The issue was not provisions, but the bank just didn’t have operating profits

- Q1FY22 – We had provisions but no profit

- But now for the bank to have an operating profit of 1000 crore, is a big thing

- Our bank will never post a loss again in our life , we will now continue to compound equity

- This translates to RoA

RoA:

- PAT trajectory QoQ is phenomenal

- This has reflected in RoA

- This story can progress up now

- A good number is probably 2%, but what is more important is the speed at which the RoA is improving

- Research reports saying we are not making good RoA are making a fundamental mistake, they are missing the point

We had guided that by Q4 of this year, RoE will be double digit RoE, but we will be there even before that. We change our guidance .

- Our exposure to NPA, legacy accounts, we have dealt one-after-one of them. I can say they are now out of the way

- It shouldn’t be surprising to you that our profitability is improving

- We are looking at a very good FY23

- We are internally feeling very, very confident

MR. SUDHANSHU – FINANCIAL RESULTS

- Credit Cards – more than 1 million cards issued

- CASA ratio is stable at 50.04%

- Average Casa Ratio grew at 10% on a QonQ basis

- Bank has excess liquidity

- Bank opened 10 branches in the current quarter

- Substantially granularized the CASA book

- 5550 crore legacy borrowings have been resolved

- The Decline in GNPA and NNPA was much sharper

- Gross Slippages were lower by 20% on a QonQ basis

- SMA positions have improved from the previous quarter

- PAT growth was driven by strong growth in operating income and lower credit costs

- Modified duration of trading book also reduced

- Trading loss was (44 crore) due to sharp increase in yields

- Provisions were lower by 17% on a QonQ basis

- CET Ratio = 14.01%

Q&A

Ishan Agarwal – Erevna Capital

(Erevna Capital – Mumbai based firm; Designated Partners: Anubhav Goel, Ronak Gala and Ishan Agarwal)

Q: Relating to NII Growth, NII growth QoQ stands at around 3%. This is the lowest QoQ growth since merger, and maybe the first time decline in NIMS QoQ. Is it because of the lag of passing on of funds from the ledning side or is it structural in nature?

- We have a lag in passing on but this quarter it should be fixed.

- It should be on an upward trajectory from Q2.

Q: Provisions at 308 crore in the Quarter. look very low. 0.9% of the average book. Are there any write-backs or one-offs in this quarter?

No

Q: You had given a guidance of 1.5% provisions. Will Provisions will be higher than 1.5% in the coming quarters for the year for the credit cost to be at 1.5% in the current year?

- We don’t change guidance just because we had a great quarter this one time.

- We don’t see any reason why credit loss in the subsequent quarters should go up materially

- We think we will we do better than 1.5%

- Right now it is 91bps for the quarter – I hope ypu agree it is very good for the kind of yield we get on the book

- 1-1.1% is our internal guidance and a fair base.

Q: Also, OPEX has seen a QoQ decline. What is the trajectory for the next 3 quarters?

- It should go up a little bit. This quarter it didn’t materially go up.

- You should expect normal QonQ growth to happen

- This time it was low.

- It should go up marginally every QonQ – because there will be more disbursals, more upfront payouts, collection expenses, but nothing material should shake it up.

Q: On the savings side, we are offering 6% on balances above 10 lakhs. How much has it impacted our blended cost of funds? What is the blended cost of funds on the savings account right now?

It would be around 5% blended savings cost on savings account

Vishal Shah – Athena Investment

(Mumbai-Based firm; Directors: Nilesh Bhagchand Borana and Shraddha Nilesh Borana.)

Q: Our Total Expense to Assets Ratio is at around 5-6%. In comparison, only Equitas Small Finance is higher than that. Even AU Small Finance is at 3.5%. The larger, private sector banks are at below 2%. Can you just help me understand this?

- Let me ask you a question, what is the vintage of these banks?

- So, if you take all the big 4 banks, they are operating for the past 25-30 years

- When you put up a branch or an ATM, it takes time to leverage.

- Our 640 branches they will have an average lifetime of 1.5-3 years. We are not 20 years.

- Everyone forgets we are a new bank. We have had a very short life here.

- As these branches really scale up, year on year, in the next 15 years, naturally the cost measure will measure up with every other bank. It has to. That is on the liability side.

- On the asset side, the established banks will probably have a large mortgage book. And the cost to assets on the mortgage book will be pretty low.

- Most of our assets are not exactly those low-rate, long-division mortgages, etc.

- Our products are of course giving us more yield, which you can see in the NIMs, but they are relatively high opex on the asset side

- Think of any product we have, 2-wheeler financing, or used cars or new cars, or LAP, you get the drift.

- As branches age, it should help

- On the liability side, branches have not yet scaled up.

- We are operating in the same country, same kind of people we are hiring, no reason why our cost structure should be different than any other private sector bank.

- Only on the liability side, only with the scaling up, that we will scale up, will we be like any other good bank.

- 2-2.5 crore spend on each branch is our annual run rate.

- On liability side, we will scale a little better than any other bank.

- On the asset side, the product suites we have are at a higher cost structure than the big banks of the country.

- Let me take a large bank of the country, they probably have a 5 lakh crore home loan book. They must have started 20-25 years ago.

- If you look at our Cost-to-Income ratio in our Home Loan book, it is around 90% or something. The prime home loan that we started just a year ago, the yields are just 7-7.5% or something.

- But today who are building it have to incur the costs. We have started.

- If we take car financing business, it is also a high cost structure. It is true our asset side is relatively higher cost. And liability we have comparatively just started.

- Our Credit card business is loss-making.

- Cost to income for credit cards is upwards of 120-150%.

- This also tends to put load on the cost-to-income ratio.

- The prime home loans we started about a year ago – NIMs are pretty low there – Today people who are building it have to face those costs

- I am not worried about this, as that’s how things are built.

- If I put pressure on this, then there’s no way we can grow.

- The businesses we are building, are built for the future. Our job as management is to get payback.

- Payback will happen when scale happens and cross-sell happens

- Our processes have just started to gather steam.

- We were a liability gathering machine till about a year ago. We have just started on this cross-sell

- We are certainly underperforming on the extent of cross-sell on the liability side.

- Once we set up the businesses and incur the expenses, our job is now to bring it to profitability.

Q: In the next 3-5 years, what should one expect on the Cost to Assets?

- You should come back to Cost-to-income, because Cost-to-assets depends on the line of business you are in.

- Cost to income we are at 75% right now. YoY it is coming down. It will still come down. We’ve done the math.

- If we bring down this ratio by 10%, our RoE will increase by ~5%.

- It will come down, it has to come down. Because income will go up.

- We can’t be at 75% per se. Definitely in the long run, we want to be in the mid 50s. Within 2 years, it should definitely come down, but might not come down materially.

- Our RoE has already touched 9%. If we just pay off the high-cost liabilities, that should give us about 750 crore, and then you reduce Cost-to-Income

- We should expect the bank to reach mid 60s in the next couple of years.

Q: I just wanted to inform you that the new app is phenomenal but Downtime of the app is very high. So, it would be great if you could look into it.

- We are aware of that. But thank you for informing us.

- It is a starting phase, but now it has stabilized. We have solved it.

Pritesh Bumb – DAM Capital

(Mumbai-based firm; MD And CEO: Dharmesh Mehta)

Q: A medium term question, How do you look at deposit rates as we are in the upcycle? So do you feel that we have to be ahead to raise rates in the industry? Is there any change in the mix to safeguard NIMs?

- No discussion going on in the bank, no plans right now.

- On the CD ratio, we are higher than other banks, but we are carrying high cost legacy borrowings, we have since merger – we have reduced these borrowings, but to that the funding requirement was lower to that extent

- if we include these long-term borrowings in the denominator, the CD ratio gets adjusted to 80%

- So once liabilities get paid off in the next 2-3 years, and we have deposits for replacement, automatically this ratio should correct in due course.

Q: Do we have room in our mix to raise NIMs? Do you see any mix-changes we can do to keep NIMs intact?

- The NIMs are quite healthy.

- It is at 5.9% in this quarter.

- We are seeing rate increase, etc. but we have not yet passed on the increase to customers – we will do this in Q2

- We feel we will maintain this.

Q: What are our Tech cost as a % of OPEX? As some of the banks are disclosing this

- We haven’t called out that number but we continue to invest in technology

- It’ll be a bit higher than other banks, but will plateau now

- Other banks, they will already have an app, already have a solution for current account management solution. For us, we have to build everything.

- We were just an NBFC who have now converted into a bank.

- Some portion of our expenses are just catch-up expenses to match capabilities.

- And others are performance enhancing expenses and we are incurring both.

- You see how quickly our story is building out in terms of Operating profit. Once we start normalizing these expenses, think about where this bank will head

Q: We can see Solid unsecured growth in all major banks. Do you think you will take a step back to see how it works out?

- We will watch closely and see what the data speaks to us.

- Our general assessment is unsecured is one dimension. When we lend a personal loan to a Wipro or an Infosys or a company, they paid back even in Covid. But if you give 2-wheeler loan, it would struggle in Covid.

- We have to see the ability to payback. It depends on how we evaluate the cash flow.

Aadar Shah – Phillip Capital

Q: Regarding Opex, you said as income grows…pace of income growth will surpass opex growth and that will contribute to RoE. Is that right?

- Both will play out

- If Retail books grows by 25% YoY, that is what we have guided for…and what will happen, we don’t have to do anything for that…when that happens, income goes up 25%, and that gives us leverage.

- Just to be clear, we are not doubtful about double digit RoE

Q: Regarding Cost of Funds, By 20th July, you have decreased the rate on personal accounts.

- In the delta sense, our business model has been made for this sort of situation

- Fundamentally, our yield is slightly better, our origin is different, NIM of 6% also we are happy with – all we have to do now is about scaling of the book

- We won’t even think twice if rates increase by 50 bps because our margins are so strong

- Wealth, Cash management, FASTag will scale up, so some bps here and that will not matter much to us, income will grow.

- Commercial Finance increased marginally on a sequential basis; we expect it to increase in subsequent quarters.

- Blended cost is now 5.2%. But don’t bother about it too much.

- If yields in the market rise for any reason, it doesn’t matter to us much, because operating leverage is yet there, we have so many buffers we are sitting on, this will be a round-off item.

- Asset Repricing will also happen which will take care of cost of funds expense increase

Q: Have you utilized Covid provision?

- We have utilized around 75 crore of Covid provisions for the corporate, retail chain loan that slipped into NPA in this quarter.

- Exposure to that account is now zero, it was 550 off crore. It was a legacy account so we couldn’t do much about it

Q: Infrastructure Portfolio at 6700 odd crore – are you confident of existing portfolio or are you planning to cut-down?

While we are getting revenues there and expect a resolution to happen in the coming year, we don’t see any incremental stress coming in.

Ashitosh Mishra – Individual Investor

Q: How much of our loans are linked to MCLR, etc and how much is fixed?

- 37% of the book is linked to external benchmarks

- 60% - Repo

- 40% - MCLR

- We have passed on repo increase in case of new loans

- Pricing benefit for existing book should reflect from this quarter – Q2

Q: We are in a Rising rate environment. How do you plan to manage?

- While we are not able to pass on the rate increases on existing book, we have passed on to the new book

- Our margins will be strong because of comfortable NIMs

- Average tenor would be around 8 months – but will differ from product to product

- On a blended basis, average tenor is around 2 years

- Cost of funds is 5.2%

- We will be able to replace the bonds as they mature, at. Cost of 5-5.5% - that much release will flow into the P&L as and when it happens.

- If you add this to current levels of ROA, this problem should go away

- This report that always is bearing on us, just can’t believe we can’t get to RoA – when they don’t see the source of this growth, the quality of the organization – they don’t realize it will show up down the line

Q: What is our Customer Acquisition Cost?

- We did not grow the liability base too much last year

- This year on wards, we need deposits to grow at 20-odd %, you may see more presence in marketing for subsequent times

- It doesn’t matter the number of customers – the thing to notice is the quality of the customer

- We don’t have zero balance products – the customer will bring in something 100%

- Because then we can make good use of infra for meaningful relationships

Closing Comments

- We are building a very high-quality bank and a strong customer franchisee

- Even if you are not an investor, Anybody and everybody should be our customer – we genuinely have great products and don’t charge for things we don’t believe should be charged for.

- When you look at our company 1 year from today, I am sure you won’t be disappointed.

28 Likes

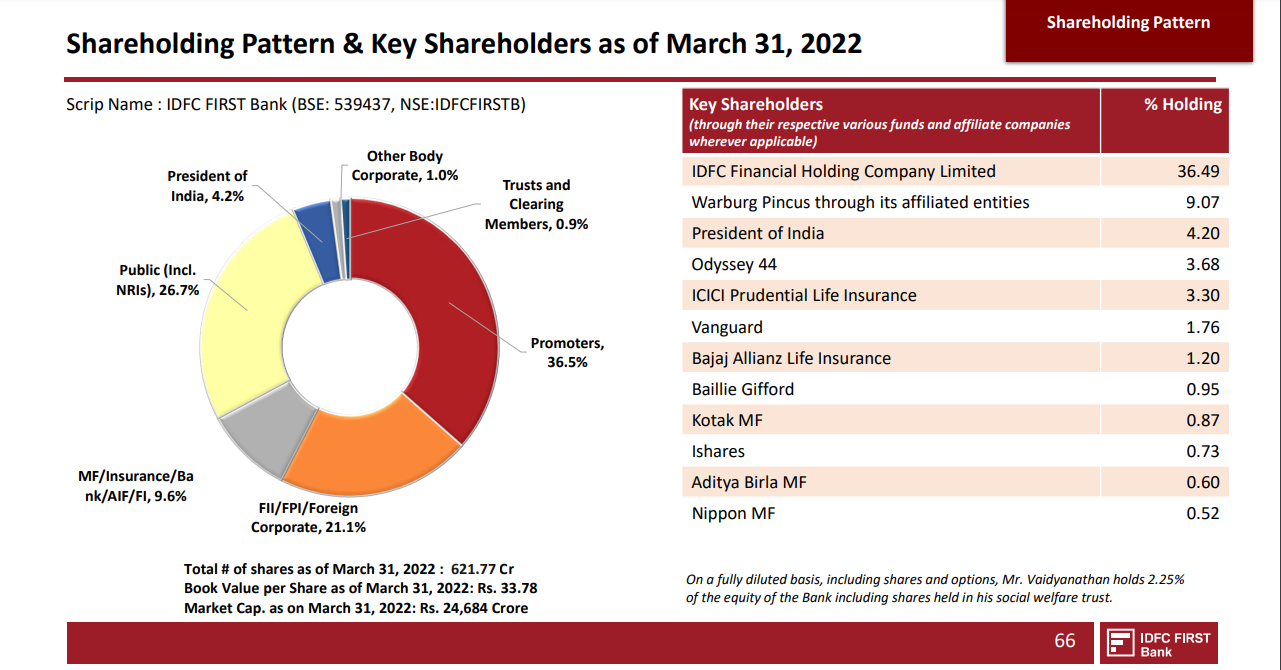

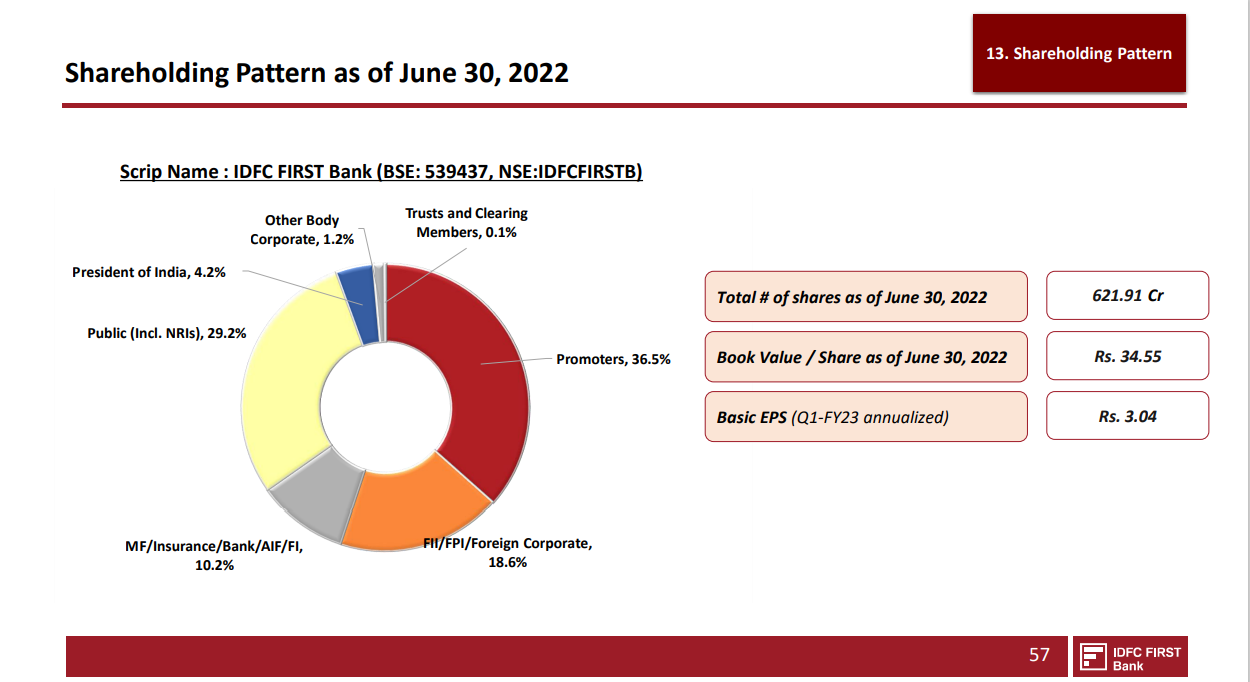

One things to note. The management has chosen not to mention Key Shareholders in the Q1FY22 Investor Presentation.

Q4FY22:

Q1FY22:

1 Like

V Vaidyanathan, MD & CEO, IDFC FIRST Bank, speaks to CNBC TV18 on Q1FY23 results

V Vaidyanathan, MD & CEO, IDFC FIRST Bank, speaks to ET Now on Q1FY23 results

8 Likes

Over the last one year or so VV has become more upfront with the bank performance and future projections. At times he does not mind sticking his neck out. Perhaps the bear hammering has got to him.

VV has concentrated on restructuring and refurbishing for last 3 years and the bank’s structure has been reimagined, redesigned, expanded, restaffed and retooled with a brand new work culture. It is now looking like a formidable compounding machine but the market is still hesitant. The confidence may start coming back when the share price comes in the vicinity or crosses 60. This could entail a wait of another one or two quarters with ROE>12 and ROA>1.2.

Another point to note is how VV starts stonewalling when asked about the merger. I find it very encouraging as it shows that he prefers to delay it a bit so that the bank can get a decent deal which will reflect the immense value he and capital first have brought to the table. The bank apparently does not need any more capital this year for a 25 to 30% loan book growth. So the merger should ideally be timed for fy 24, for arriving at a fair deal for both parties. A fairly senior manager looking after 40 branches, told me in an informal chat, about 10 days back, that he is targeting 30% loan growth this year.

19 Likes

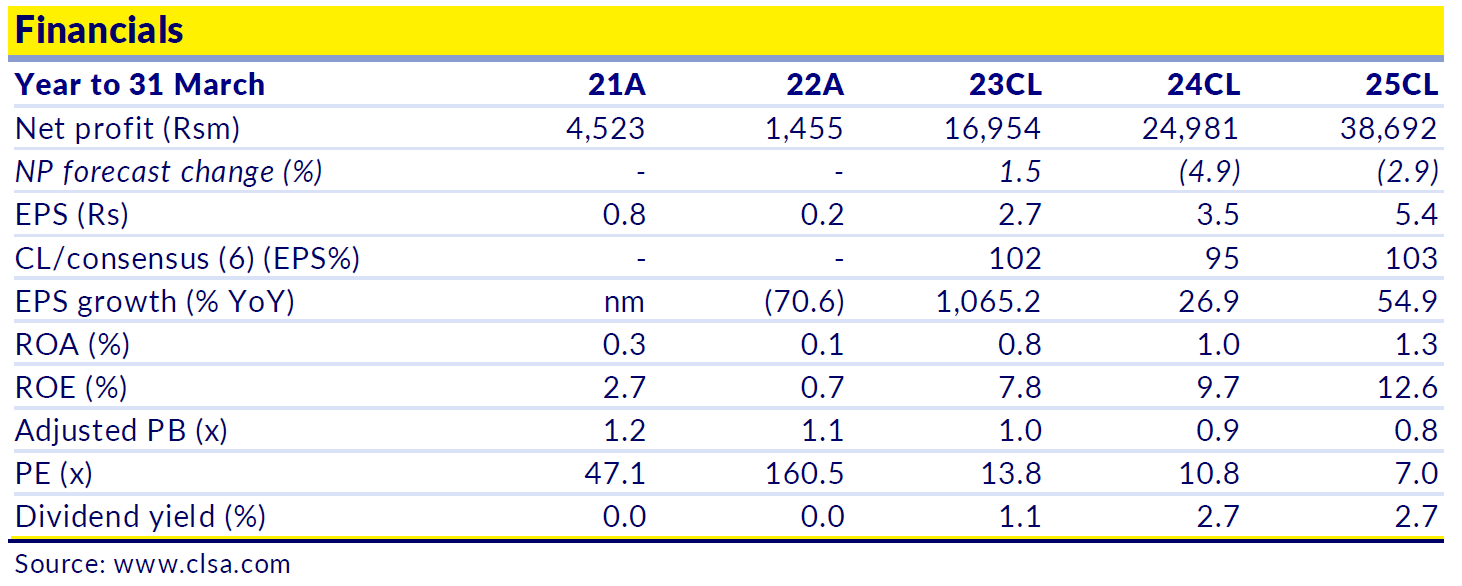

CLSA does not see RoEs hitting 15% even in FY25. Same thing for low estimates it has for RoAs 3 years down the line.

Disc: Invested

Banking is a balance sheet business for the most part. Lending will always be the core activity and it is not easy to run a lending book in a country like India (~6 Cr odd people filing taxes in a population of 140 Cr) without an adventure every now and then.

Lending is underpenetrated for a reason in India, a good chunk of the population is simply not worth lending to as of now. Given this situation all large and med sized banks end up competing for the same set of credit worthy customers and companies. The lowest risk lending deals are most likely to be won by those with the lowest cost of funds for obvious reasons. The least risky areas of lending like secured assets will be dominated by the larger banks.

More often than not, high NIM is a sign of risk rather than of superior lending capabilities. Capital is a commodity, which is why the rate of lending is the only thing that matters to borrowers. A loan from HDFC Bank is no different from a loan from ICICI Bank, unlike in some other business segments. A handbag from LV and VIP Industries are not the same, even if the utility is the same.

The other aspect of running a bank well is the ability to build scale and to do cross selling well. Each branch is a micro catchment area where the bank has access to customers who can consume financial products in addition to giving deposits and taking loans. Cross selling fee based services like cards, wealth management and transaction banking to companies do not induce additional balance sheet risk. They call for investment into technology, people and processes and regular operating expenditure in the form of salaries, rent and other overheads. To issues even 100 cards, technology, customer service and processing teams need to be in place from day 1. These expenses do not scale with an increase in the customer base. So when VV talks of C/I coming down over time, he obviously is taking of higher scale doing this, not more operational efficiency.

The best way of assessing these aspects is to see the cost to income ratio and the success in cross selling services and products. Ideally new customers (NTB) contribute to liabilities before they contribute to assets. Leading customer acquisition with lending has been a sure shot way to disaster in India for obvious reasons. VV himself was part of this mistake at ICICI Bank, he is unlikely to make the same mistake again.

Most smart and experienced management teams manage to do branch expansion, expense management and cross selling well.

In my book, Q1 results provide good comfort on the expense management and cross selling parts but doesn’t yet do much for the first part - prudent lending. Not to say that the current lending processes are lax but that there are miles to go before the market gets comfortable about the quality of the asset side of the business.

The foray into prime loans and the focus on mortgages is good from a risk management point of view, even if it dilutes the NIM over time. Growth in the newer areas like digital loans, consumer loans, gold loan etc will take time to season and give comfort to investors.

Keenly watching developments here over the next few quarters. There are obvious positives here after the Q1 results but it doesn’t yet address some of the risk investors have about mid sized banks that are under pressure to deliver 20% loan growth while suffering disadvantages on the cost of capital front.

These will only get addressed with scale and time, even if the operating numbers look very good 3-4 Q’s down the line. Even behemoths like ICICI Bank and Axis Bank have grappled with credit issues - due to both the economic cycle and the specific bank’s lending cycle.

The second part (specific bank’s lending cycle) is the more important one to understand for long term investors. Economic cycles are the same for every bank while which segment to focus on/avoid to build assets is a conscious call taken by the management. A good assessment of this is unlikely to come from going through financials or debating about numbers already declared by the bank. It can only emerge from a good understanding of the credit culture and the decision making hierarchy within the bank. It is truly an intangible and is rarely apparent even to internal folks, leave alone investors observing numbers from a distance.

While banking sector has been a wealth creator in India, the bulk of the wealth creation has been done only by a few banks while the rest of them have only burnt investor capital over decades. In mid sized banks and lenders I guess it is important to play the cycle well. I hope this bank turns out to be a successful one over time but not coming to any hasty conclusions yet based on Q1 results and the obvious improvements in operating efficiency & the steady asset quality so far.

Disc: Holding for self and customers

45 Likes

Kedar bhai…

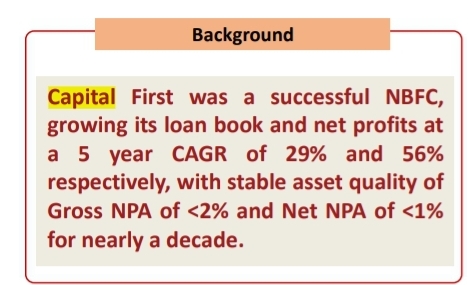

When a conversation comes to credibility, VV refers to his Capital First days. And rightly so. Idfcfirst is nothing but an extention of his career from Capital First.

A chunk of that book is carried under the new banner. That business is a time tested one. Those Customers are well understood.

This also gives us relief to know that VV has been doing this core lending business since FY 10

NPA is one thing he knows how to keep under check. His team has good experience in collection systems etc.

Most importantly, he has passed the litmus test: Covid. If he can survive that, get away without major NPA, then he is good for another decade.

What appears new to his experience is the technology bit, the in-house credit card and loan disbursement tech where they will bypass the need for DSA. Hence, reducing cost. It appears, that couldn’t be a huge threat.

6 Likes

Wow this post has given me a very good understanding how the valuation works for banks, it’s part of past track records, why hdfcbk gets a pb ratio of 3-6.

So I guess market will give it a good PB ratio once it’s convinced about the asset quality of the bank for long term. So inspite it hitting a 15% ROE unless market is convinced of it’s underwriting quality over long term it won’t get premium valuation. But if banks like Bandhan Bank can get a pb ratio of 2 I guess IDFC first bank also deserves a PB ratio of 2 because it’s loans are less risky compared to Bandhan, provided that IDFC hits 15% ROE.

Disclosure: Invested at average price of 36 so has valuation as margin of safety.

Nice post. Have been invested since Jan 2019, first with bank and then switched over in July 2020 to IDFC Ltd. So I’ve gone through the roller coaster, but overall significantly in the positive. Agree totally about asset quality being the key determinant for future….credit costs maintained in the 1% range over several years is what is going to drive meaningful re-rating and BVPS compounding from profits and raising capital at higher multiples.

Having said that, his focused execution of the plan laid out in 2018 is very commendable and gives me confidence to stay invested and watch the story unfold here.

3 Likes

Thank you very much Ayshi and Sahil for so well capturing the conference call. Without hearing the call, it feels Ive heard the call.

I have been an investor in Capital First and have made multiples of my money. There was never a credit issue for 9 years and I remember those days CAPF was lending to lower income segment for purposes the banking system were not lending. I was always minutely tracking the credit loss and NPA, but credit costs was well managed. (I used to call it subprime, but he never used the term in AGMs even when asked on the same). Even at ICICI, all people I talked to swear by him. They say he practically built the entire retail banking and built it amazingly. Literally, I used to be amazed that people were falling all over him to meet him in AGMs and all that. If in that segment, the credit losses were only 2.5%, then in the current segment, it should be lower.

So credit quality is not the issue. the issue is that since the merger, there have been no profits, only losses and I was disappointed. Even now the profits are only ROE of 9%. frankly, so many banks post 12-13% ROE. I know the starting point at merger was weak with no ROA ROE and he has done a great job taking ROE to 1%, but he could have upfronted the losses in the first one or two quarters after merger, than bleeding the P and L for 6 quarters after merger. In his current approach by stretching the issue for 6 quarters, we were always on an edge. Lets see when the bank can post an ROE of 15%. Even 10-12% ROE will establish the proof of concept and we can believe the 15% after that. Lets wait and see.

7 Likes

I have nothing but high regard for what VV has accomplished at IDFC FB so far. If anything they have gotten to many of their targets much sooner than what they had initially projected. And his experience at Capital First is no doubt very valuable, growing an NBFC while keeping NPA’s in check is no mean achievement.

It is just that the base rate of success in banking in India is not high. Most players have struggled to become pan India players, leave alone becoming a leading bank. In that sense IDFC FB has the right mix to become an urban centric pan India bank without having too much allegiance to a particular region or customer segment. Many banks with good underwriting skills struggle to get a cosmopolitan, contemporary culture going which prevents them from expanding successfully outside of their comfort geographies and areas. IDFC FB has this part sorted out so far.

However, in the quest to grow assets at 20% without having the advantage of low cost of funds there is always the possibility that certain risks have to be knowingly taken. Large banks have already built switching costs (credit card, demat account, insurance payments linked to account, mutual fund investments happening from the account, lifestyle benefits, automated mobile payments) for the customers who are already credit worthy.

There is a chasm that every mid sized bank needs to cross in India before it becomes a large bank with a strong competitive position. Take enough calculated risks to build scale but the risks should be granular enough to not affect balance sheet quality too much. It is a very tough task to pull this off even in a developed economy, leave alone one like India where the real addressable target market for lending is hardly 6% of the population on the retail side.

There is potential in IDFC FB for sure but investors should not conclude too much too soon, even if the operational piece of the puzzle is falling into place. We always need to do qualitative checks before developing a high conviction on lenders (any lender for that matter, not just IDFC FB) before we start thinking about whether they can become the next big, successful bank. There have been too many misfiring engines in the lending space over the past decade for a variety of reasons.

I sincerely hope that VV takes IDFC FB on the path to becoming a large, successful bank for many years to come.

21 Likes

The bank is growing housing loan book rapidly. The highest growth came from the housing loan book if I’m not mistaken. That’s a secured portfolio and the alpha to the nim will be provided by unsecured personal loans . It’s like running on knife edge but they have to do it to get into the big league.