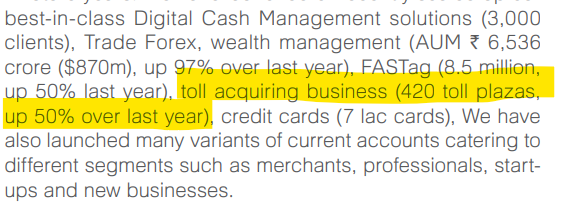

I was going through the Annual Report there is toll acquiring business with 420 toll Plaza. How does this business model works?.

1 Like

Please refer to the attached link to understand the NETC FASTag Business Model

there is 4% MDR on every FASTag transaction on toll . Of which 1.5% goes to the issuer bank, 1.25% to the acquirer bank, 1% to IHMCL and 0.25% to NPCI.

IDFC in 3rd in terms of issuer banks and 1st in terms of acquirer bank ( as of May’22)

https://www.npci.org.in/what-we-do/netc-fastag/netc-ecosystem-statistics

8 Likes

Thanks, this finally answers my question IDFC First Bank Limited - #1195 by Akhilesh_Halageri

Came across this article which mentions the same rates https://thewire.in/political-economy/fastag-will-datafication-of-indias-tolls-boost-highway-development. This is from 2019, is there any official source?

If this is true then the bank’s involvement in this toll business might prove to be a blessing in disguise in hindsight. They got into this due to legacy reasons but foresaw a good opportunity and grew it organically over last 2 years. Given India’s early stages in e-commerce the bank will be a big beneficiary of increased logistics movement this decade. Lots of new infrastructure corridors are under construction. But I hope they don’t get involved further than this, NCPI is a govt entity which means more regulatory risk, they can change these rates overnight.

At this rate, considering other initiatives as well, in the coming years we will see a big jump in non-interest income. But core banking business should always be the top priority.

5 Likes

Merchant discount rate(MDR) could change and it might have higher impact for acquirer bank as opposed to issuer bank as they own the customer. However acquirer will have more visibility on overall transactions made by customers across different bank. They can intelligently use this data to improve their issuer coverage.

But FAStag rail has lot of potential to grow. This can be used for commercial parking lots, state highways. Even can be used for car servicing etc… it’s all upto how someone can innovate and launch payment solution using this rail…

1 Like

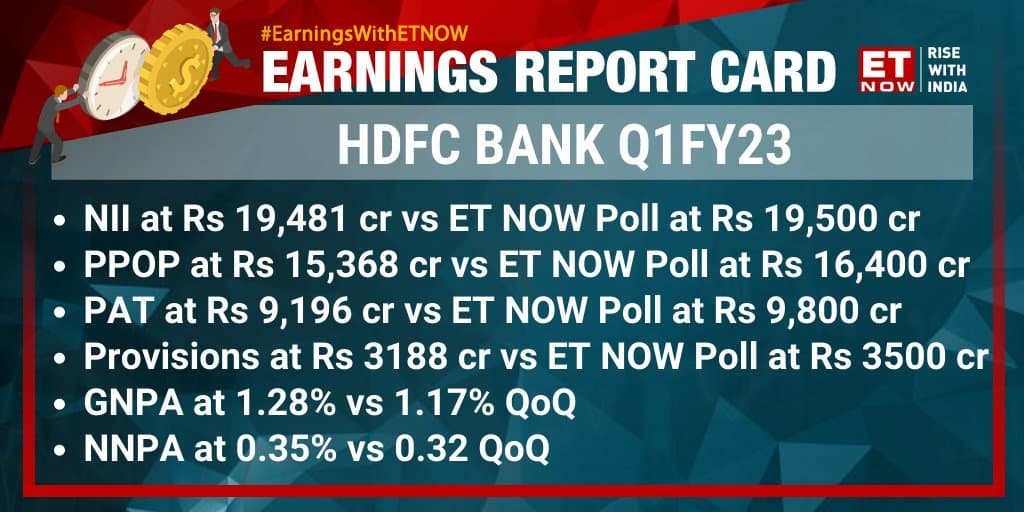

I think HDFC bank derating is mainly due to merger. Market is anticipating that due to SLR/CRR requirement growth will be slowed down temporarily.

1 Like

Kotak has proven to be totally wrong in case of Federal Bank, results are announced today and profits from treasury segament is 130 crores (increased QoQ), instead of a loss of 240 crore as predicted by Kotak.

Lets see what happens in case of IDFC First Bank.

13 Likes

Banks can classify investments in HTM which is what Federal has done. MTM provisioning is not required on HTM book.

In any case, this treasury loss is likely to be a short term hiccup for others. Long term yields might be peaking out. There can be treasury gain in the next quarter in that case. This is not something that I would base my investment decision on.

1 Like

In my view that is why it is important to do your own research based on data and management commentary after going through brokerage reports. In my view, treasury losses (if any) should not exceed 40-50crs in this quarter for IDFCB. Kotak has been way off the mark wherein it estimated a MTM loss of 240 crs and federal bank reported a treasury gain(in other income) of 25 crs.

4 Likes

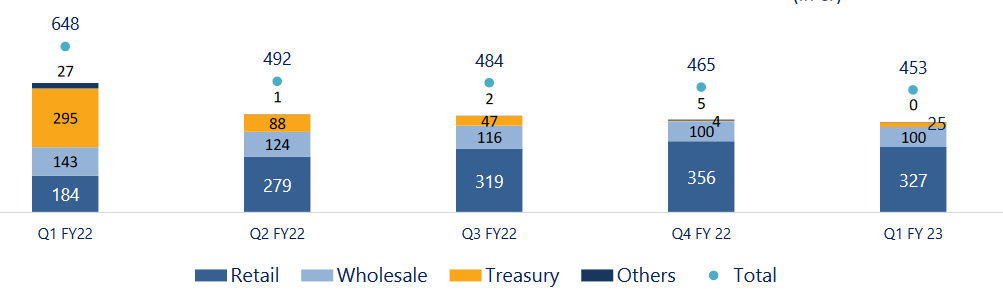

Treasury income has fallen 270cr vs Q1FY22. Banks can shift securities amongst buckets in Q1 so they typically show higher treasury income in Q1. Let’s see what IDFCFB numbers look like

I read somewhere that banks have to sell the investments categorised under HFT within 90 days of purchase…

correct me If I am wrong, but I think possibility of yields rising was visible to everyone since Jan-Feb 2022, so I dont think banks would have made a losing trade in that category… AFS category is anyways small…so in my views there is a possibility that performance in Treasury segament may be better then Q4 of F.Y 22 this time for most of the banks…

The brokerage is again way off the mark in the case of HDFC Bank. They estimated MTM loss of Rs 2960 crs and revaluation loss has come in at Rs 1311 crs. The brokerage house has been way off the mark in the case of two banks in a row now.

Also, given the fact that HDFC Bank’s investment book with a maturity of more than one year stands at 2.4 lac crores(From basel 3 disclosures) and IDFC First Bank’s investment book with a maturity profile of more than one year stands at 15000 crs( 6% of HDFC bank) I expect IDFCB’s treasury loss of less than 50-60 crs.

8 Likes

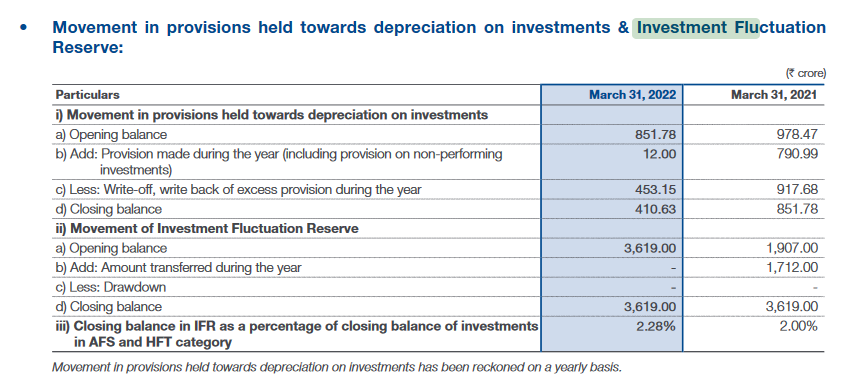

Depends on how much they used from the IFR this quarter, as of March 2022 they had 3,619cr lying in that account. Even after that the loss is still 1,300cr. Remember IDFCB has 0 in this account.

Secondly most analysts were forecasting very low losses, so kudos to Kotak for forecasting that the losses would not be unsubstantial. The main reason the bank has missed most analysts earnings estimates even though provisions are much lower are these MTM losses.

1 Like

This is again pure speculation that HDFCB has dipped into the IFR in this quarter. No where in the press release or notes it is mentioned that the company dipped into IFR during the quarter.

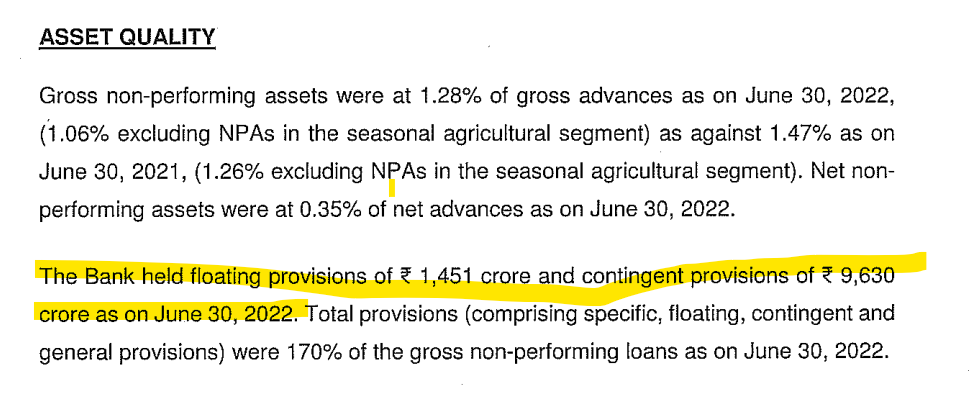

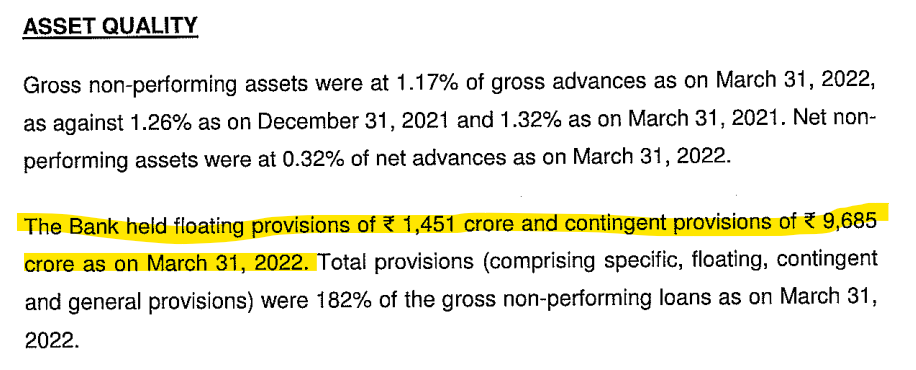

The floating provisions as of 30th June, 2022 are 1451 crs and contingent provisions are 9630 crs. As of March, 2022, the floating provisions were 1451 crs and contigent provisions were 9685 crs, which CLEARLY means that the bank has not dipped into any provisions.

Provisions Held as on 30th June, 2022:

Provisions Held as on 31st March, 2022:

And if any item from Reserves and Surplus of the bank has been dipped into(specifically IFR) during the quarter, it will reduce the reserves and surplus of the bank and hence has to pass through via the P&L in my accounting knowledge.

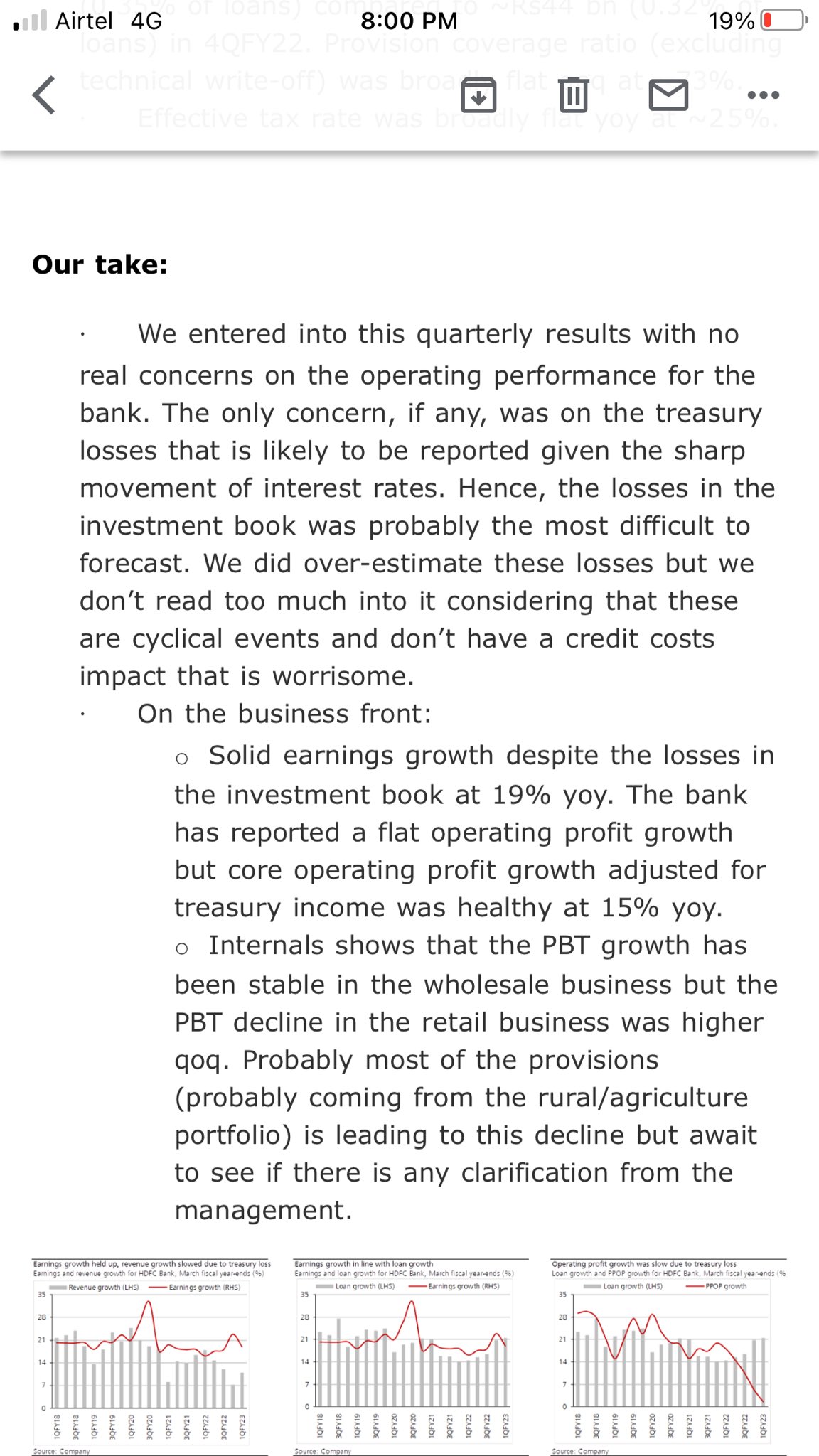

Also, PPoP in the case of HDFCB has missed estimates mainly due to higher than expected employee expenses. We should wait for IDFCB numbers to have a clearer picture

6 Likes

.

Kotak on HDFC Bank results, they have admitted their mistake in overestimating these losses…

So things won’t be as bad as feared in case of the rest of the banking names also…

5 Likes

IFR is considered Tier 2 Capital so won’t be included in these figures, but yes best to wait for IDFCB results as we wont get anywhere with this discussion.

7 Likes

Bank confirmed in Concall that they didn’t dip into the IFR. Kotak seems to have over-estimated the losses.

7 Likes

The good thing is that speculation has been put to rest as HDFCB has clarified that IFR was not dipped into and Kotak has admitted that it overestimated MTM losses. Both things are good for IDFCB estimation of MTM losses(if any) and I hope this reduces some fear on MTM losses

8 Likes

They haven’t increased interest rates.

Will probably cause margin expansion, if lending rates increased. If not, then sales will increase.

1 Like

1 Like

Double digit ROE by end of FY 2023.

Next target is 16%

Ultimately high teen ROE.

12 Likes