Was re-reading the Transcript of last concall. VV has stated his pov, somewhat clearly, vehemently…

Things that are fairly clear:

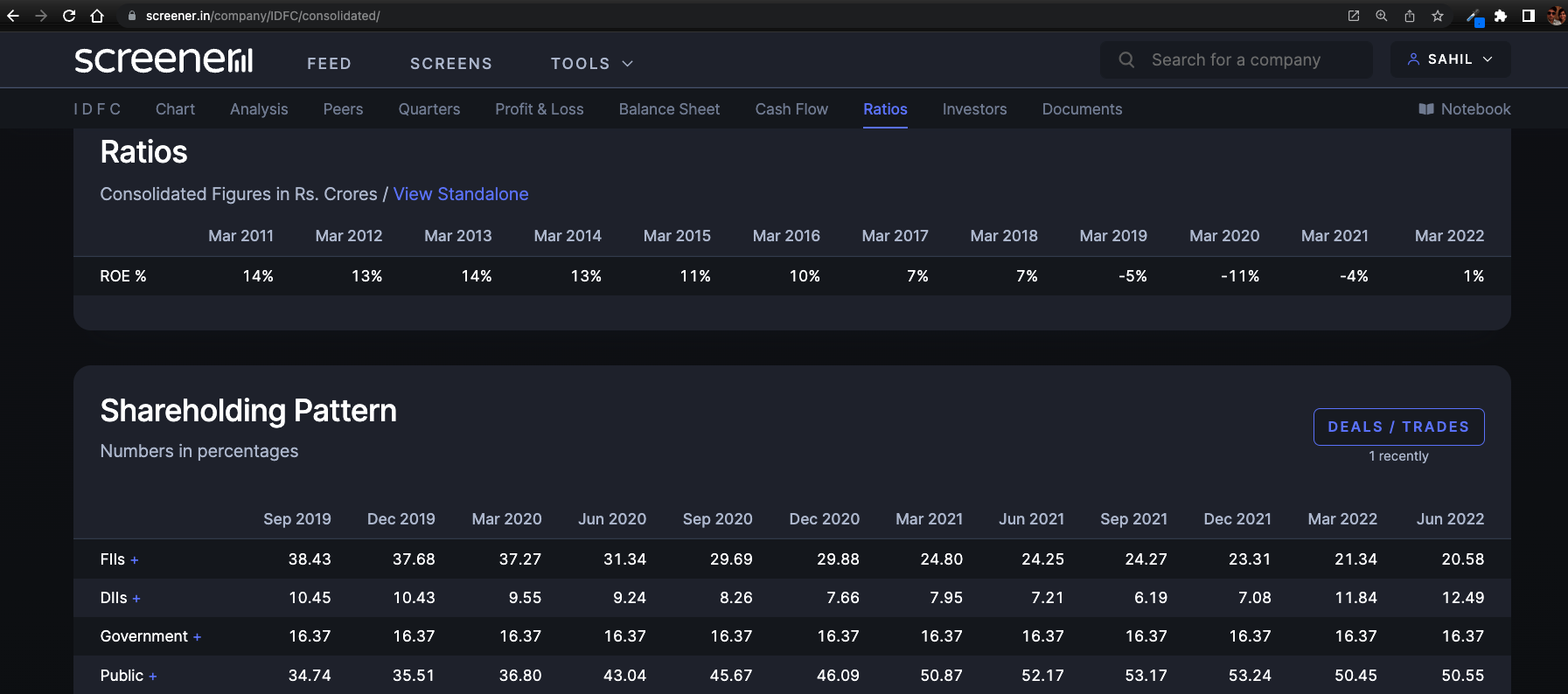

a. Any doubts regarding double digit RoE have been put to rest. VV said it himself. And his life depends on it.

“we are for three businesses; the ones that I named earlier; credit card, retail liabilities and legacy liabilities. These three alone if they were to just break even forget being profitable; if they were just breakeven, we will add on a PAT basis, post-tax basis Rs. 500 crores for quarter. You add that Rs. 500 crores to the Rs. 340 crores, that takes us to about Rs. 840 crores. And the annualized Rs. 840 crores into 4 that Rs. 3,400 crores and you

divide Rs. 3400 crores with Rs. 20,000 crores, you know Rs. 21000 crores, you get to see that already touching an ROE of (+15%)”

b. His words "And then (after ROE 15%) you can imagine what a well governed bank with a good ROE growing at 25%, technologically very abled, what we should be valued at.

He touched on “valuation” right after he was asked about RM (go figure!)

In that question he said… intention to RM is clearly there, no doubts… but “There are so many points to close before you get to that point.” And in the next question, he talked about how high the valuation will reach in the short term.

This makes me think, the bank will wait for peak valuations, before signing up for RM. To me, “so many points” means he wants to bargain, and he will be in a stronger position to bargain after RoE goes double digit: That and that alone is his focus for next 8 quarters.

After this quarter and next quarter’s results, the above laid trajectory will be very clear, and then this stock will be buy at dips. Ready for a long bull run.

However, COVID has taught us that, such calamitous events that can disrupt retail lending will be really bad for this business, will cause sharp swings. Being invested in this bank for the long term, wont be without its set of heartaches.