sorry to say, but I feel youre assumptions of 2x are rather optimistic. there is no basis for that. why would bank agree for diluting 4000 cr at todays prices which is the assumption baked into your 2x theory. they dont need that kind of money today, at todays prices with strong cap ad. they might as well wait for a while.

there is probably ownership bias (not saying in a negative sense) in your thinking. both parties have announced their intent to merge to the exchanges, the stock of idfc has reacted positively, and risen sharply, and amc is sold. so in the market’s eyes, the merger is fully factored in the value of idfc limited. which at current market price (fully discovered price after all news baked in) is 1.45 or 1.5. so remember if the merger does not happen at the price you are thinking, you could be in for a big -ve surprise since it seems you are holdng IDFC limited. from the bank point of view, if merger does not happen, makes them no difference, they can raise capital from the market when required. remember shareholders of the bank will need to approve the deal as well, so there has to be fair value. and fair value is certainly not what you are saying look at other deals to understand the fair value… fair value is not full value… there is a discount whcih is what the market is factoring at the current prices. beyond this price you should wonder whether any aribtage exists at all.

just my opinion, if you differ pl correct. thanks for this discussion, thank you.

Thanks for this; seems like from the ET Now interview that the merger is definitely on and the only delay is the sale of the Foundation which is ongoing and should conclude soon. Hopefully should hear something on this front prior to IDFC’s results on 20th. Very positive news.

“I understand the question. As far as we are concerned, eventually when values are discovered appropriately, that phenomenon will matter a lot (and) more importantly as far as merger is concerned we are very clear about that.” so said VV at the end of his interview with ET.

So far the only contribution IDFC Ltd has brought to the table is the banking licence. Apart from that it has been a pathetic story. It is very clear now that without Capital first merger, IDFC Ltd would have sunk without a trace with so many loans becoming NPA and bulk depositors making a quick exit at the first sign of trouble. It is therefore ironical that while the IDFCF bank has done the entire heavy lifting and straightening out everything for three long years but many investors are selling IDFCF and buying IDFC Ltd with consequences to their price.

I therefore like VV’s assertion above that he would take that into account at the time of merger. The merger ratio should be decided accordingly so that both set of shareholders get what they deserve.

The bank is performing even on the ROE and profitability front, and there seems to be consensus. If the BV and ROE keeps going up, then value is being created even if it’ll be recognised later whenever the reverse merger happens, assuming neutral swap ratio.

There seems to be much debate on the details of the merger. I don’t know but I would trust any prudent management to ensure it’s at least neutral for shareholders. Is there any reason why the management would be compelled to agree to anything else? If not, we can rest assured that the stock will catch up sooner or later. If the merger is a negative, then the improvement may not reflect in stock prices even at a later date because of value destruction.

The short question seems to be will the management be able to negotiate at least a neutral ratio. And when.

Here’s how I would like to posit this whole issue.

What happens if the merger is delayed by a year? Which set of shareholders suffer more?

Keep in mind that IDFC FB is unlikely to report a loss from hereon and will in fact report QoQ improvement. Conservative metrics would suggest 1800crs of PAT in FY23, taking the BV to near about 23k cr, placing the bank’s current mcap at 1.04x 1 year forward book value.

Who suffers in a case of delay? How desperate would IDFC FB be for capital? Yes capital for banks is always desired but how desperate would IDFC FB be 1 year down the line?

Key thing to remember is that if the bank wants to grow faster than the ROE it is able to achieve, it will ended up needing to raise capital fairly quickly. Bank wants to grow overall loan book by 20-22%, but at best will be achieving ROE of 10% by FY23 end and 15% by FY24 end. I’d estimate that bank will need to raise capital in FY 24 and merger with IDFC and use of the 4,000 cr from AMC sale is a win-win for both parties (of course at a negotiated swap ratio that takes into account the 4,000 crs plus 227 crore shares that IDFC owns in the bank).

VV mentioned that the Future retail NPA was provided earlier.I was wondering when was this done since it wasnt even part of Watchlist.

Anyone has any ideas ?

Also Watchlist data was missing this quarter.Was keen to check how they much more they were able to bring it down further.

Think the market is starting to now realize how beneficial a rising interest rate environment is going to be for IDFCB. So it’s pretty common knowledge that a rising interest rate environment acts as a tailwind for bank’s NIM’s as the rates on advances tend to rise much faster than rates on deposits, this is especially true for retail focused banks with granular loan books and limited bargaining power of customers. So like other banks IDFCB will benefit because of this too, maybe slightly more due to its retail heavy book.

However the part that is most interesting and which will act as an additional tailwind for IDFCB’s NIMs is below-

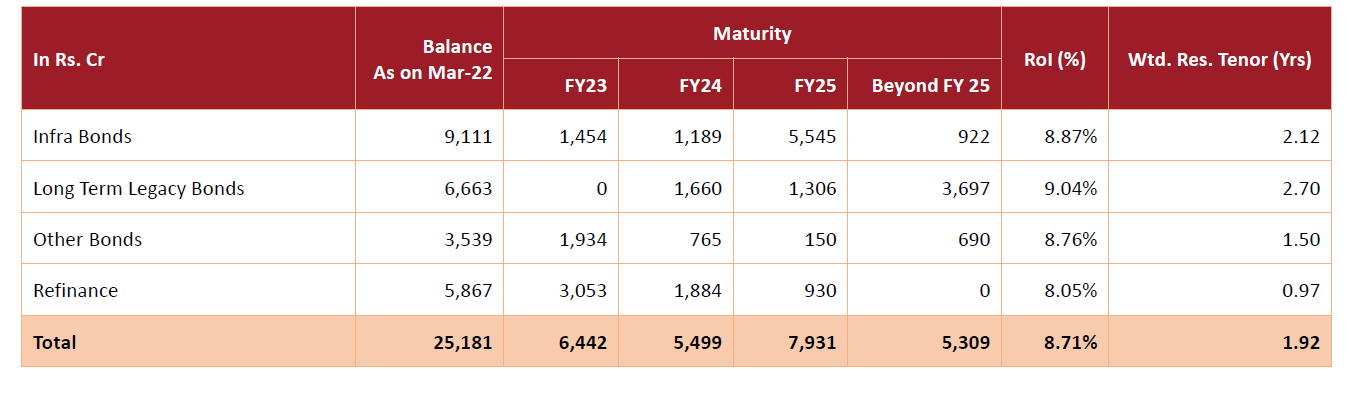

These ofcourse are the dreaded high FIXED cost deposits that IDFCB inherited from IDFC and that have been a drag for the bank over the last few years. Now as we start transitioning into a high interest rate environment what will start to happen is that the drag these deposits were on the overall NIM’s will start to dramatically reduce. The average ROI on these deposits is 8.7%; now 12-15 months back IDFCB was able to raise term deposits at around 5-5% so the drag was almost 3-3.5% due to these deposits. Now fast forward to today and the 10Y Govt bond is trading at 7.5% and AAA Corporates are issuing bonds between 7.5% to 8% in the markets. Pretty soon term deposits and FD’s of banks will also be at similar levels; as a result the drag from these high cost deposits will dramatically reduce and possibly be just around 1% for IDFCB. This is a pretty big deal and the relative loss the bank was suffering due to these high cost deposits should reduce dramatically.

In Q4FY22, IDFCB reported NIM’s of 6.2%+ despite paying 8.7% on 25,000cr+ of legacy deposits. What will change going forward? IDFCB will still pay the same amount on these fixed cost deposits but the lending rates for the ENTIRE system will move up. So IDFCB’s average retail lending rate will move up say from 14.5% to 16.5% (along with the entire banking system due to the higher costs of deposits) while the cost of deposits on this book will stay the same. This along with the first tailwind can have a dramatic impact on the banks NIM’s and I wouldn’t be surprised if at the end of FY23 IDFCB NIM’s are closer to 7%. Remember every 0.5% or 50 basis points increase in IDFCB’s NIMs means an additional 1,000cr to the pre-tax bottom line (as there is no additional cost and operating leverage kicks in) which is pretty significant for a bank expected to report around 1,500-2,000cr in profits in FY23.

Most interest rate increment cycles last 2-3 years so the other good part is that most legacy borrowings will be over by the time system interest rates start to decrease again.

Some thoughts occur after reading the latest con call script.

IDFCF bank share price has taken a serious beating in spite of continuous fabulous performance and results . Perhaps the market can’t decide which is a better buy ? IDFC Ltd or the IDFCF bank ? If one buys the dubious IDFC Ltd and the reverse merger does not go through for any reason, then it would be a risky investment as IDFCF bank share holding is the only noteworthy asset which provides it value. Therefore there is a real risk in investing in IDFC Ltd. And VV doesn’t appear to be overjoyed with the prospect of the reverse merger. His expression changes and his body language changes. On persistent questioning he has he hawed and admitted to only an intent to consider it after many things happen first. So my impression is that he may agree to the merger but only after 2 or 3 years. He has clearly said that he does not require Tier 1 capital. That creates a possibility that he may not agree if he feels that the merger terms are not just. By Q4 22 concall indications, the bank is quite likely to reach an ROE of 15% by FY23 and then get into the smooth stride, all distance runners are familiar with. This is of course presuming that no further viruses/wars are let loose on the world.

It might be worthwhile to see the argument from the side of idfc.

Here’s a imaginary discussion between the boards of idfc and idfc first

Idfc: hey we want to reverse merge with you.

Idfc bank: ok we are open to it . What’s your proposal.

Idfc : it’s x : y

Idfc bank: no we don’t like it. We want z:a

Idfc: that does not work. We can adjust somewhat but it’s x:y

Idfc bank: it’s z:a .take it or leave it

Idfc: well, if you don’t agree we are selling our 36 percent by auction to highest bidder. Whoever wins can decide what he can do withyou. Maybe they will fire the board

Idfc bank: you will do what ???

Idfc : so let’s sit and agree on anumber that works for both of us.

Idfc bank: yeah . Let’s work it out

P.s : this is an attempt a making this discussion insightful yet less serious.

Incidentally in an investor call with the idfc management when vinod Rai was still chairman, enam was on the call and made exactly this proposal. So this is not an imaginary situation.

Investors were so unhappy with the slow progress of divesting the idfc subs that they chose to vote him out immediately after that.

Arm twisting is not the way.

VV is the key here, rest all is structure and replaceable.

Anyone even thinking of taking over the business will have to have VVs approval, else it wont be business as usual.

If RM happens, then it will be on VV’s terms, which are going to be, very simply, something which benefits the bank and its shareholders (Warburg Pincus), and ensures VVs strong hold.

VV is going to be the D.Parekh (whether or not IDFCFB is the next HDFCB)

Rs 55 was proposed but apparently that is not enough. Some quarters down the line, this number might double. So more the delay the better for the bank’s shareholders, and not so much for the Ltd.

Rajivji has no option but to wait, till VV gives a go ahead. It might even be a long time. I did see the 20% odd arbitrage benefit in buying IDFC Ltd… but since i intend to hold the bank for a long time, i did not want to take the risk. There are many variables. Proxy investing, in this case, has a very poor risk reward ratio.

Why don’t they distribute 36% Bank shares to idfc shareholders and cash as dividend and shut the whole idfc limited.

I don’t think increased free float will be of concern.

Swap ratio favorable to bank won’t be accepted by idfc limited shareholders and vice versa.

Yeah, there are lots of possibilities and we don’t sit in the board room so we don’t know. Plus we are not in charge of executive decisions.

Rajiv lal is no longer in charge of idfc. Anil singhvi is now chairman. He has in the past run a proxy advisory firm and is known for high governance standards.

VV is considered crucial for the bank , but ONLY HE can run it well is not true. There are many more talented bankers in the world and the board just has to find them if it comes to a fight and VV exits.

The bottomline is saner heads and rationality will prevail and there will be a merger ratio agreed on. We can debate the timelines and it might be a few months here or there I don’t think that makes a difference.

Both parties are in it and they know they have to compromise to put this uncertainity behind them and look forward to create value fast. I am sure VV knows this and he will help find middle ground. All his hard work over the last decade will go waste if he leaves now. He will have no lasting legacy. He is a reasonable man.

From my point of view the longer this uncertainity the better it is because the price will be continue to be lower and one can buy on the basis of stronger earnings delivered by every coming quarter. Just for record I think VV is an amazing guy and I am.invested mostly because of him

P.s: not going to stretch this point more since my essential point is already made. Rest is details

I agree with all your points… just that in the early stage of an institution … someone who takes serious ownership and drives it, sets the foundation, takes the bank to ROE of 16-17% ROE, is critical… that job … looks like is on its way… once that is set than frankly anyone can run it… AP left HDFC Bank goes on for example, Sobti left, but IIB goes on…

In 2015 IDFC Bank was formed, where Infrastructure Finance and liabilities were transferred.

Essentially means, what didn’t work was cast aside, and what seemed to be doing alright was retained.

Now, in recent past, things look good at the bank, so they want a RM.

What else could be the motivation for RM, other than being an opportunist?

What’s in it for the bank?

Well, the only thing the bank can possibly get out of this RM is cash. So, when bank reaches a point where it must dilute equity, then it will give a go ahead for RM.

Excellent points to ponder. The discussion has become very rewarding.

The two managements should reach a conclusion and amicably as it is the only way forward. Any whiff of a controversy will likely put a cloud over the bank for sometime.

In my opinion, the best course of action would be the reverse merger but as per the timing decided by the idfcf. IDCF Ltd management should remain patient and avoid being pressurized by its shareholders. Their performance record has been pathetic so logically they should not interfere or advise.

If theoretically IDFC Ltd becomes impatient and offers 36 percent in the market, then it could also perhaps solve the problem. Since it is a bank, the shares will not go to a single entity as I think RBI puts a 10% ceiling plus various approvals including directors approvals and sebi also has some regulations which may scatter the shareholding. The other 64% would largely vote for VV along with many in the 36% offered holding. VV is a continuously well performing and proven winning horse for last ten + three years. Why would any stakeholder even think of changing him for an unknown entity.

The other point is that the reverse merger is not a must for the bank for its growth. The bank may never need any cash from IDFC Ltd. But it definitely needs to be free from IDFC Ltd linkage otherwise the bank share price will always remain shackled. So this factor says, merger at the earliest.

IDFC Ltd has Cash and 36%+ stake in IDFCFB. From IDFC Ltd point of view, shareholders want the value to be unlocked through reverse merger ASAP.

What does IDFCFB need? It is still unclear from IDFCFB management whether they want cash through RM or not.

Case1: IDFCFB doesn’t need cash and is capable of raising cash whenever it wants through QIP.

What is the point of delaying Reverse merger?

IDFC Ltd can reward it’s shareholders through buyback/dividend and get rid of cash. Can it even buy shares of IDFCFB from the open market at INR 40/-? This is even better for IDFC Ltd shareholders.

Case2: IDFCFB needs cash at the moment

.

This is a win win situation for both as IDFC has cash and the bank needs it.

Both ways RM should start as soon as the AMC business is sold and regulatory hurdles are cleared.