This topic was automatically opened after 4 hours.

Something noteworthy about the management is that it has been honestly guiding. Hyperbole, deception, avoidance are not a part of their repertoire. Hence, their Quarterlies are a nice read. They set my expectations.

Some members in this forum are disappointed with the results, and so is the management. Their wordings are pretty clear and honest.

"Net Profit for Q4 FY22: The bank posted net profit of Rs. 343 crores in Q4-FY22 driven by core operational income. Due to three specific factors

(a) legacy high-cost liabilities

(b) retail branch/ ATM/ liabilites set up expenses, and

(c) set up of credit cards, there is a net profit impact of ~ Rs. 500 crores/ quarter. This is reducing every quarter. "

We are happy about

- the growth in CC biz (370% YoY)

- CASA%

- Higher NIM due to retail exposure

But that comes at a cost: Branches lead to Retail Exposure and CASA build up. Credit Card growth comes from an organic setup. Seeds must be sowed and soil nurtured.

This drag of 500 Cr will reduce with each passing quarter. 500 Cr is a big number considering net profit of 352 Cr. But, the good thing is 500 Cr drag is due to an investment, its a part of the overall strategy. Its under control. Unlike, NPA or some ego driven acquisition.

Cost to Income

Was 84% Fy21

Is 76% FY 22

Target 55% by FY25

The trend is good: 8% reduction this year. And that is what was exactly promised by the management. We were told that this target of 55% wont get achieved in the near term. But, will happen eventually.

Trend in expenditure for new branches is flat 601,599,599,641 (number of branches each quarter)

A major reason for high Opex, along with CC biz.

Furthermore:

We expect the drag caused by these three factors to be largely eliminated by FY 25 based on our internal analysis and trends. Adjusted for these, the return on equity of the bank is already at ~15%, and we expect our return on equity to stabilise at 17-18% based on calculations of incremental unit economics

Investors have been given a target of FY25 for the bank to meet the set standards by top tier Indian banks. If its acceptable, if you buy the story, buy and hold is the best course of action. No point hyperventilating every quarter. Cause till Fy25 this story is going to be bittersweet.

Some strong set of numbers here:

Strong Growth in Operating Profits: While the loan book grew by only 13% YoY,

the Core Operating Profit has risen by 44% from .... This clearly demonstrates

that our incremental business is highly profitable and we are beginning to see

strong improvement in operating leverage. We expect this phenomenon to

continue to play out over the next few years, which will result in increase in

overall profitability and ROE

44% growth against 13% loan book growth is impressive. With CC biz picking up (370% YoY) profitability wont be an issue in the next FY as well.

15 Likes

In the quarterlies, I want to check NPA. What steps the management has taken to set it right.

I am happy to note that NPA is under control this quarter, again, as promised. Covid is behind us. The Credit Cost estimate guidance has also been reduced. That’s a cheer.

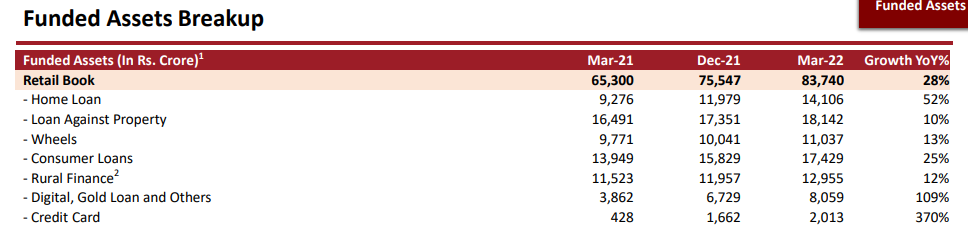

The loan book growth has been healthy. I am happy to see that the secured loan book growth is far more than unsecured.

Wheels, Con Loans, Rural Fin growth rates are clearly low numbers comapred to HL, Gold, LAP. Credit Card growth is the highest. Clearly shows the intent, where the management will focus in the future. Axis has paid 12K Cr to acquire CC biz (ofc the scale is different). The potential seems to be huge.

The profitability has an impressive clip to it. With NPA under control, this bodes well.

32% YOY in NII, that is really nice. This is likely to improve quite a lot next year, because the bank has made a high Operating Expenditure this year, which is up by 36% YoY and has said it wont spend on branches as aggressively.

So Op Ex will see a single digit growth, this will unleash PPOP.

5 Likes

Went through the concall and just put the numbers in a spreadsheet to try and see what sort of year FY23 will be based on VV’s guidance. Most of the assumptions are mentioned in the notes and are in-line with what VV mentioned during the call. I end up with a PAT of around 2,100cr and an ROE of around 9% if trading gains are assumed at 100cr a quarter, without trading gains the PAT is 1,780cr and the ROE is 7.8%. I think the numbers are an accurate assesment as if you annunalize the Q4 PAT you end up with a profit of 1,300cr itself. I have assumed NIM’s to remain at 6.20% even though VV mentioned they should continue to drift upwards to 7%.

The joker in the pack ofcourse are the trading gains and they could determine if the year ends with a double digit ROE or not. Yields have been moving upwards over the last two quarters negating any gains but if we have a stable year, esp with the 10 year risk free already at 7.15% then there could be trading gains of 100-200cr every quarter.

13 Likes

Next year net profit is like to see a big jump for two reasons:

- Operation leverage is going to improve:

operation expense is going to grow in low single agents digits because branch expansion has stopped, and the credit card infrastructure expense is mostly done.

- Provisioning is going to be much lower due to absence of Covid like crisis.

Going by your estimate of 2100 Cr of profit after tax, and 621 Cr equity shares, EPS comes to 3.31

Considering a PE 20, stock price of 66 is on the cards.

6 Likes

Can someone share link for conf call for q4 please.

Link to audio of conf call Q4 FY 22 https://www.idfcfirstbank.com/content/dam/idfcfirstbank/pdf/financial-results/ICI0420220430140687.mp3

1 Like

Check the branches count, they added 7% or 41 new branches in Q4 inspite of that Cost to Income fell to 76% or 8% YOY. Operating leverage is already playing out…

3 Likes

A concern.

165k Cr of Loan book, will require close to 33K Cr of additional capital to grow 20% YoY.

Leverage is 7.5x which means 4500 Cr of equity will be required. If this doesn’t come from reverse merger, then there will hv to be a round of dilution.

Any mention of this in concall?

As long as RoE is below 15% this will be a concern each year.

3 Likes

Management clearly mentioned about NO equity dilution in FY 23 …

.

I think they will raise TIER 2 capital if needed.

1 Like

VV said they have headroom for T2. Frankly, i feel the key issue is the merger. meaning as long as there is idfc limited, investors will always feel they might as well buy idfc limited and get the bank share with some discount. if you study the track record of idfc limited, the stock used to trade in the 30s a year ago, in the 40s 6 months ago, and in the high 50s these days. well there is nothing that idfc limited has achieved to see this sort of appreciation, when most other banking stocks including blue chips like hdfc bank and kotak have dipped.so idfc limited has gained in a falling market, and the only reason is that investors have sold idfc bank and bought idfc limited once the news on the merger became positive from both sides.

so frankly all benefits of performance will go to idfc limited.

until markets figure out the benefit of discount is all captured, after which it does not matter what an investor buys.

thats exactly whats happening imo.if i am missing anything please let me know.

6 Likes

The thing with IDFC is that the numbers are so compelling that its an absolute no brainer if you believe in the IDFCB story. Its my personal opinion that whenever the swap ratio is decided it will end up being between 1.90-2.00x and IDFCB will end up getting the 4,200cr as Tier 1 Capital that the holdco has from the sale of the AMC. This will be enough to manage the growth until FY24-25 and by then the ROE’s will reach 15%+ and the bank will become self-sufficient on the capital front.

Why a swap ratio of 1.90 to 2.00x? Well you can run the numbers yourself but if the 4,200cr is converted at a share price of Rs 55 the swap ratio is 1.90x and if you do it at Rs 45 its 2.00x, so I believe that it will be somewhere in between and probably closer to 2x.

At 2x what are the economics of owning IDFCB through IDFC? Imagine I offered you IDFCB shares at Rs 28.5 or 0.80x BV today, would you buy them? This is not too far from the 2020 low prices and if you believe in the IDFCB story you would probably buy them without any hesitation. This is exactly what you are getting by buying IDFC shares over the bank and unfortunately until a swap ratio is announced or IDFC shares are close to Rs 70 -75, this situation is unlikely to change.

This is precisely the reason why mutual funds have doubled their ownership of IDFC in the last quarter. You probably wont find a safer growth+value opportunity in the current market today while having valuation comfort that provides downside protection. My advice would be ignore what the bank shares do and look at IDFC till Rs 68-70, this is basically getting the bank at trailing book value.

Disclosure: heavily invested in IDFC with 30% of my portfolio in the name. Will keep shifting capital and also SIP’ing into the name as long as its below Rs 68-70. Happy to allocate upto 60-70% of my portfolio to IDFC. This strategy only makes sense if you believe in the IDFCB story and plan to keep the shares even after the reverse merger; if you only want to play the valuation arbitrage then no idea.

Edit: Don’t treat the above as investment advice and I am not a SEBI registered investment adviser.

14 Likes

From Banks perspective, they must not be wanting to merge at CMP.

The growth trajectory is strong. The holding company brings nothing to the table, except capital. It is equivalent to equity dilution for the banks share holders.

If there is a fall out, and this reverse merger gets cancelled, I’d be happy.

2 Likes

Is there a risk of reverse merger being cancelled or obstructed?

Just a hint of it will cause an UC.

A news article reads

Indeed, the company’s investors were promised that their value would be unlocked even before the merger of IDFC Bank and Capital First Ltd in 2018.

All of this assumes that VV would just cheat IDFC FB shareholders and go for a reverse merger on a poor swap ratio? I believe that merger swap ratio won’t be finalised until desired valuation of the bank is reached.

I don’t think funding would be that big an issue. IDFC FB on 30th April has also approved raising 3k cr Tier 2 bonds.

5 Likes

I don’t think it will lead to an UC as the reverse merger is as beneficial for IDFCB as it is for IDFC. Apart from the capital the bank will get (at 1.90x ratio works out to Rs 55 a share, will it be able to get that valuation today in the market?) it will also leave the bank’s destiny in its own hands. As long as IDFC is there with 37% ownership the fate of the bank will be in IDFC’s hands and if some NBFC or larger Bank buys out IDFC they could effectively take control of the bank and do with it as they please. They could remove VV and merge the bank with themselves. Nobody wants that, either IDFC shareholders and definitely not the bank shareholders, so its really important to get the reverse merger done asap and have 100% of the bank’s ownership in the markets hands, similar to HDFC or ICICI.

14 Likes

I have nil technical competency to comment on the timing of the proposed merger. Still I feel that IDFCF bank should not allow itself to be hustled into a quick merger and it should do so only when it feels that it is suitable.

The bank should be able to manage its target growth this year with 3K proposed to be raised as tier 2. Next year it will have a higher equity as FY 23 would contribute decent amount of profits especially if toll road a/c also becomes standard. For FY 24 additional equity if necessary, can be sourced by issuing rights shares to existing shareholders. That will ensure that there is no dilution of holding.

The bank can take a call on the merger in FY 25. Will this line of action give the bank shareholders a better deal compared to now ??

2 Likes

There was one thing that I noticed during the conference call that there was hardly any big name brokerages/investors represented. All questions seemed to be from individual investors or PMSes. Questions asked actually were pretty good but I don’t think they represent a lot of current or potential investors money.

A lot of money that gets invested in stocks comes from advise of these brokerages/investors. I am not sure if it was the weekend effect but that is something bothered me a little bit. Institutional money moves the stock.

Not sure if others feel the same.

I guess that’s because brokerages lost interest. When a share goes up a lot of brokerages publish reports on it. And they loose interest when it goes down. Happened with CAMS and many other companies. Maybe I’m wrong.

1 Like