I am not sure about the RBI / Banking regulations but I think the best option for IDFC Limited shareholders is as follows

1.) IDFC Limited distributes its shareholding of the IDFC Bank and cash post sell out of AMC business to its shareholders in ratio of 1.4 share of the bank + cash for every 1 share of IDFC Limited. That way they dont have to wait for the bank’s decision regarding reverse merger.

They can continue to have other JVs with state governments in IDFC Limited for the time being and exit as and when that happens. Post exit they can close the IDFC Limited as it is anyways a non-operating company.

Rather than trying to add a ‘imaginary discussion’ angle in the conversation between the 2 entities, it could have been directly highlighted that IDFC could sell the shares to an investor or a set of investors. 4 things to consider here:

IDFC Ltd in the same Concall had also mentioned that IDFCF should have an incentive to merge with IDFC. That incentive is the sale proceeds of the AMC.

If IDFC Ltd decides to sell, it will probably happen at a depressed price which is not beneficial to either parties.

Even if sold at a good price, IDFC will have to pay Capital Gains on the proceeds(wipes off 10%).

After paying taxes, what will IDFC do with the proceeds? Distribute to investors? Say, it gets X amount from the sale. After tax it is 0.9x. It declares dividend of the full amount. Most HNI investors and institutional investors will frown at this as they will have to pay 34% tax on 0.9x, which means actual realization is 0.59x

So X value fetched by sale will translate to 0.59x in the hands of the shareholders of IDFC Ltd which clearly the management of IDFC does not want.

Also, why will an institution buy from IDFC Ltd when IDFC First itself can attract them in a QIP at the same price? Atleast the Institutional money will go to the bank for productive capital.

From whatever I can infer from the interactions of the 2 management teams, it seems a merger will happen; timing is still a year away in my view.

Rationally, I do not expect IDFC Ltd to trade at more than 37-42% premium over IDFC First. May be even lesser.

All the negative you mentioned would not be there if a big lender was to come in and make an all share offer to acquire IDFC Ltd. So imagine someone like Kotak offers Rs 80 per share to IDFC Shareholders to acquire the entire company? This payment would be made via giving Kotak shares of equal value to IDFC shareholders. No discount, no negative tax implications, no capital gains tax etc.

It really is in IDFC Bank shareholders and VV’s interests to complete the merger as soon as possible. IDFC Ltd shareholders and the Board will do what is in their best interests, if they get a better offer from someone else why wouldn’t they go for it? Don’t get me wrong, I am fully invested in Vaidya and the future of the bank but we need to be realistic about such issues.

Why would any entity(like kotak or for that matter any other bank) want to buy 36% of idfc first bank’s shares without gaining the bank board’s control/voting rights/management control.

If you are well versed with RBI rules, you will know that even though an entity can own 36% stake in the bank, their voting rights are restricted to 15%.

So say that optimistically, kotak does want to buy IDFCFirst Bank, they will achieve no board or management control by buying idfc ltd stake.

Can you give me any rational reason why a bank would want to buy 36% stake without board/management control?

The fact that 10% will go into cap gains, and even out of the 90%, 34% will be payable as tax by shareholders of Limited is a well known fact. that is the only reason it makes great sense for Limited to merge. dont think they can sell to any other party… will take a lot of approvals… as pointed by someone, the buyer will buy only if they are clear of the overall picture for the whole holding. instead of all this, limited might as well share the benefit and be done with the merger rather than lose 41% to tax. it would be a win win.

As for the bank, it has cap ad of 16% plus + have lot of headroom to raise T2 + will start posting strong profits from this year as per trend line (343 cr cr pat with no one time, with growing book means big operating leverage taht will flow to bottomline)+ have track record of raising equity at good prices (last raised at Rs. 55 or so). plus since the turnaround is quite visible already and will be more visible by next year, I feel they can raise as well say from QIP in fy 24. But the body language of the management of Bank has been positive… saying “we are ready, just waiting for the other party to clear their structures.” there was no ifs and buts this time, there was no words like lets see… etc. so overall the intention of both parties looks clear - to merge. just an analysis.

If anyone were to ever acquire IDFC that would be deemed to be a change of control at IDFCB and would trigger an open offer. This would mean the acquirer would need to buy an additional 26% from the market taking their shareholding to 62%.These are all hypothetical discussions but if someone wanted to take over IDFCB via IDFC they could easily do so.

Hostile takeover of any bank in India is highly unlikely in my view given the regulatory rules regarding voting rights, shareholding, permissions etc.

Let us see how it plays out. By the way, hypothetically speaking, even with your very optimistic assumption of 62% holding, voting rights will be capped at 15%. I don’t see any logic for anyone looking to gain control to do it via IDFC without taking the board of IDFCF into confidence.

Do read the RBI rules on shareholding in private sector banks in the link below. Most of the enthusiasm of takeover will wane off.

Some highlights are:

No bank can acquire more than 10% holding in any other bank(except in cases of weak balancesheet, restructuring etc).

Voting rights capped at 15%

Any entity looking to acquire more than 5% stake can ONLY do so after prior RBI approval.

Then its clear, no arm-twisting can happen, hence VV and Warburg Pincus can decide to go ahead with the RM as per their need for cash. So when they feel the need of diluting in open market, then can merge.

The issue is, timeline for this is uncertain. Talks of RM have been around for some time now. Then will the proxy investors profit? Wouldnt they be better off investing in the bank at these levels?

The outlook looks good for the banking sector in the near term. Results are good. And like @Puch pointed out, in a well informed post, the margins will expand. And particularly for Idfc First Bank.

Regarding the old investors of Idfc Ltd, they shouldn’t feel they are getting a raw deal with delayed RM (or no RM), because they chose to take sides when the bank was cast aside with the liabilities of Infra Loans.

IDFC Ltd will have cash from AMC sale

Can’t they buy IDFC First Bank shares from Open Market? IDFC Ltd will get a better swap ratio, Bank’s price will stabilise.

IDFC Ltd will have to get RBI’s approval/ or its not allowed to increase stake like this?

IndusInd and IDBI are trading at P/B of 1.6 and 1.1 respectively and ROEs of 10% and 6.7% (over 4 qs including 2nd wave) respectively. IDFCFB is at 1.3 with ROE of 6.7% (Q4 annualised). Am I missing something or is the rerating potential inaccurately amplified by comparisons with Axis and ICICI?

Analyst coverage seems far more positive for IIB with ROE of ~15% projected for FY23. Objectively, is IIB seeming a better investment with more certainty?

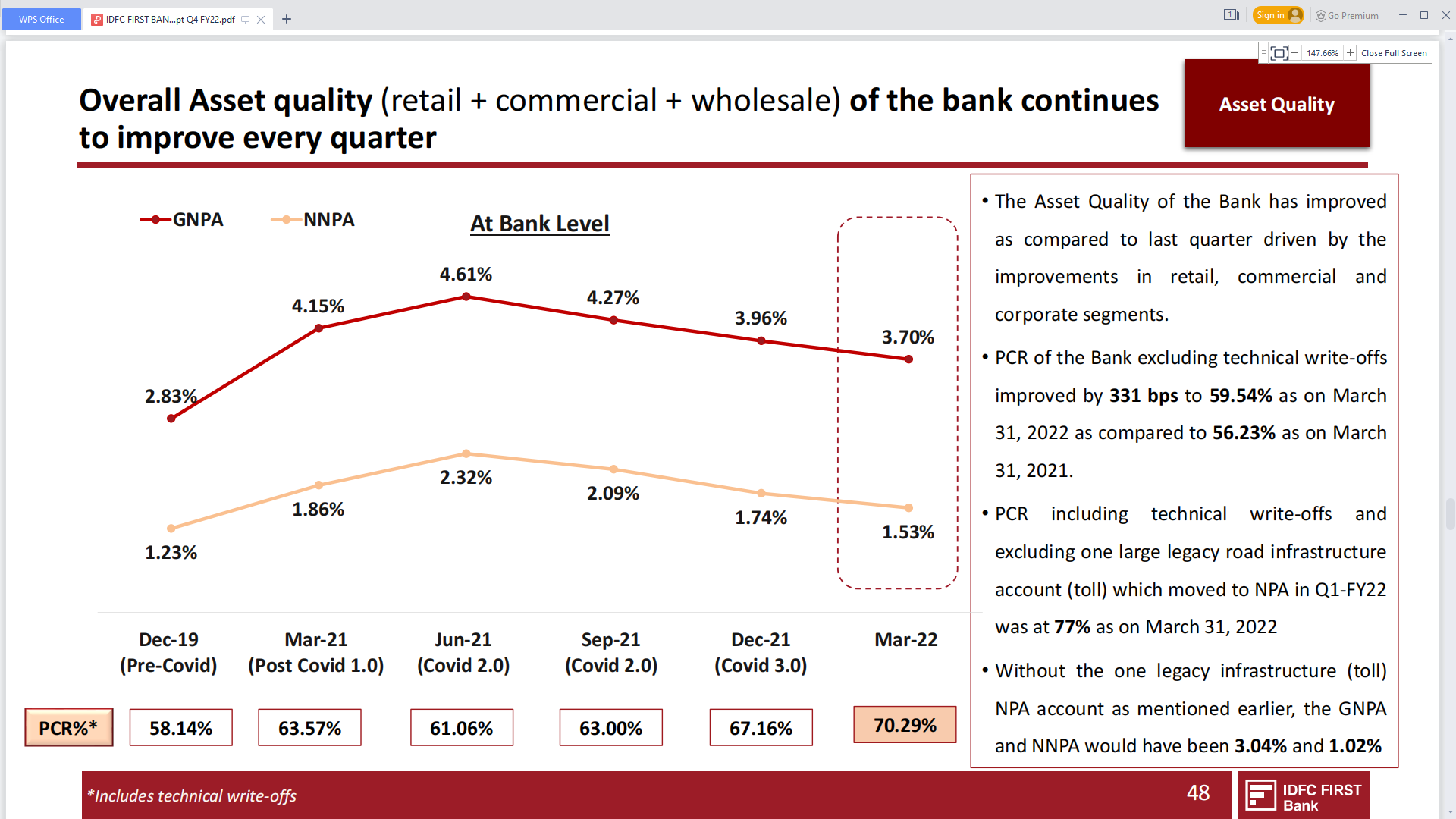

Loan book to grow from here on: We have made significant progress during the last three years (FY 19-22). We expect the loan

book to grow at ~20-25% on a sustainable basis from here on for the foreseeable future. We have strong and proven

competence in building retail lending business with high asset quality (GNPA ~2% and NNPA ~1%), strong margins, and high ROE

(~15%, incremental ROE ~20) for over a decade.

I don’t doubt why market is rating idfcfirst bank above Indus Ind and IDBI. In fact, I feel it should be rated all the way upto Kotak at PBV of 4.

Some reasons that come to mind…

*25% growth in Loan book for the foreseeable future

*Improving margins, one of the best in Industry

*Ethical management (most important, which is not the case with IDBI or Indus Ind)

I haven’t studied idbi but indusind has a chequered past of corporate misgovernance

Banking is last space to look at through the lens of numbers. Numbers are a multi year lagging indicator of success.

Top 3 leading indicators are:

Management

Management

Management

But for that one has to go through 5 years of annual reports, dozens of concalls, dozens of investor presentations, many QIP documents, and of course dozens of varied scuttlebutt

Vv has executed a turnaround at capF and see what capF valuation were and how p/b rose with higher roe (since growth was always there)

The exact same thing will happen in idfcf due to the growth

Being able to grow a retail lender with low credit cost is an art which vv has perfected not all banks can do this

Retail lending with low credit costs (compare credit costs not to hdfc bank or kotak bank, compare them to Bajaj finance or some other retail focussed nbfc)

Building a casa franchise from 0 in 2 years (remember that indusind always gave higher saving rate too, but was unable to gather as much casa as idfcf. Idfcf has truly build a brand. Despite sa rates of around ,4-5% for the most of savers, casa is growing 7-8% QoQ this is extraordinary. Compare to casa growth of indusind & idbi)

Observe the subtle hints of conservative underwriting shown be it early recognition of NPA as soon as stress appears (don’t wait for repayment), or whether it was upfronting all the credit costs in q1fy22 in order to clean up books asap rather than delaying the pain by offering restructuring (some banks like equitas have delayed pain by offering restructuring aggressively. Imo this is it conservative banking)

Deep tech investment & also innovative market products. One does not need to look beyond credit card to see how innovative bank is willing to be in order to please the customer

When one sees from this subjective lens of the softer aspects one is able to develop a keen knack for leading indicators rather than relying on screener.in headline numbers which are a commodity in today’s day & age

This is inaccurate. IDFC FB’s networth is 21k cr as on March 31, 2022. Based on that, the bank is currently trading (mcap of 23600crs) at a P/B of 1.12, which is much much lower than IndusInd.

Trading at around 0.85x on FY24 numbers, this is without factoring in any benefits from the reverse merger. Also the PE is around 8x on FY24. Imagine a company growing operating profits at 45% for the next two years available at 8x earnings, IT companies growing earnings at 20% are trading at 40-80x PE!

This is true.I tried looking at various screeners like screener.in,moneycontrol,tijori etc where the book value mentioned is inaccurate and much lower than Rs33 mentioned in their presentation.

So that gives a wrong picture for the potential investors if he is just looking at the screeners to make his decision.

Watch The Business Standard Banking show in You tube at 11 am today.

Vaidyanathan will talk about IDFC First bank.They also discuss about Equitas merger.

Should be Interesting…

The article flags asset quality issues…

Note: I’ve not studied the stock in any detail… just sharing a contra view trying hard to understand why an apparently high growth stock is getting slaughtered in the markets