Have you considered a fall in Treasury Income due to rising yields and its impact on final profit figure…???

1 Like

If you see the actuals vs their estimates on HDFC and ICICI Bank the number is off !

So am sure its off for IDFC First bank as well.

2 Likes

There was interest income from Vodafone idea (110cr) which was on cash basis. Won’t be there this quarter… This will reduce the profit. but other levers like lower interest expense, higher NII etc should pick it up.

Provisions are a toss every quarter.

Lukesh

In my view, the estimate posted by @valueseeker9 is quite optimistic. My estimates for this quarter are:

NII: 2650-2675 crs

Core Operating Profit(Excluding Trading Gains): 760-780 crs

Provisions: In the range of 350-375 crs

PAT cannot be determined as it gets influenced by Trading Gains/Losses.

I will be very happy if the bank posts numbers estimated by @valueseeker9

1 Like

How much unkind can the market be? It’s already trading at 1.2x BV. And the book value is all set to rise, now that the worst is “truly” over.

In my view, the suspicion is only on provision numbers because the street has always been a little disappointed with fresh provisions (even though VV calls them “technical provisions”).

Substantial drop in QoQ provisions will give street the confidence that the worst is truly behind.

4 Likes

Yes the stock is down 20% since the last quarter so expectations are very low for this quarter. Hopefully some of these niggling doubts will finally be laid to rest this quarter.

2 Likes

1 Like

Dear all, Apreciate if anyone can share the con call link or dial-in details. Thank you.

2 Likes

It has the link as well as the numbers

1 Like

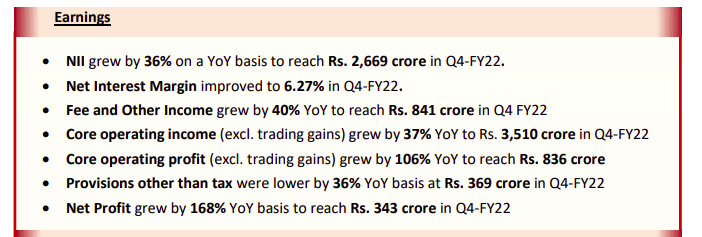

Actual NII: 2669 crs(inline with my estimates of 2650-2675)

Actual PPoP: 836 crs!! Above my estimates of 780 crs(Thanks to a superb Core other Income and lower growth in opex)

Provisions: 369 crs(Inline with my estimates of 350-375 crs)

Overall a superb performance!

9 Likes

Your numbers are factually incorrect on two counts. 1 is Networth and 2 on Cost to income ratio.

Networth is 21003 and not 19080 so price to BV is Just 1.17%

GNPA for all practical purposes is around 3.04% and NNPA is 1.02% (Excluding one Toll asset)

PCR for practical purposes is 77% (Excluding One Toll Asset)

Cost to income ratio is around 76% and not 80%.

VV has already guided for lower cost to income ratio each quarter from hereon.

6 Likes

I thought numbers were in fact pretty good.

- No new bad news.

- Vodafone saga finally over with return of bank guarantee.

- NII of 6%

- Profitability direction maintained. I see ROE 10-11% next FY and ~15% FY 24.

- Retail asset growth was very healthy.

- Fee income growing and granular.

- Only worrying thing for me is potential dilution at lower valuation if they maintain this level of asset growth.

- Would have liked them to give more info on toll account. I am sure we will hear more in conference call and interviews.

3 Likes

Q4concall Notes

-

Last 3 years we were consolidating & strengthening balance sheet. Built CASA franchise. Loan book grew at 6% CAGR, retail deposits grew ar 73% CAGR.

-

Incremental ROE of 20% for loans. Cost of funds is 5% now, so we are able to do 20% ROE.

-

GNPA is reducing every Q.

-

Guided that provisions will reduce every Q: Q1 > Q2> Q3> Q4. Have achieved that now. You get 2.5% credit losses for FY22 average loan book size.

-

Q4 annualised credit loss is 1.2%. Guiding for 1.5% in FY23 which gives enough cushion.

-

Home loan book grew 52% YoY. Strong traction on prime home loan.

-

Bank guarantees for spectrum have been released.

-

Spends for active cards are 35% higher than industry average.

-

18% CA in CASA. 11% in Fy21.

-

No DSA in credit card business. 7 lakh cards organically grown. Developed good tech enabled processed.

-

Very low attrition in senior management. Our credit will hold up with scale. Credit architecture is built ground up. First emi check bounce is lower than pre-covid. If it was 1 pre-covid, now it is 0.7 (70%). We check bucket 1,2,3, sma, recovery. We are very cautious about this.

-

Gross slippages in Q was 1400. Net slippages were 700cr. Strong recoveries during Q. one legacy corporate account of 200cr slipped during Q.

-

Nims could still rise from here.

-

Opex growth will be lower in FY23 than loan growth.

-

Q4FY23 we will get to double digit ROE. When things stabilize we will get 17-18% ROE bank.

-

Launch an upgraded mobile app where customers should be able to purchase mutual funds on the fly. Customers will be able to see what companies are under the mutual fund.

-

We dont need to expand the team for some of the loan types. But for new category of loans we will only hire for those. That is why we will see operating leverage play out.

-

Last year we were running LCR of 150%. So this year onwards we will grow CASA faster than loan book & CASA of 50% should not be hard for us.

-

CA is 15-18%. 30% in due course. We will start working on current account a little more. It takes time toi build it. Need to build tech, flow of money, end to end. Multiple solutions which re not just banking related, HR, legal, accounting. We are confident of growing here.

-

25% is revolver, 25% is instalment base, 50% straightforward transactors. Little behind industry but as this plays out in next 1-2 years we will definitely get better. Customer complaints are really low. Delinquencies are very low.

-

Mortgages & LAP will grow faster.

-

Incremental cost to income ratio. That number is trending down quickly. 3 biz is dragging it down: credit card (320cr losses), retail liabilities is incurring 1300cr each year. Will come down to 50% cost to income ratio soon. We will make PAT of 500-600cr in credit card business eventually. GOod norms from RBI inactive cards will get weeded out.

-

Upper income customer base.

-

Nims could inch up from here. Should stay in 6-7% league.

All in all, great set of numbers. Everything is proceeding well. We should see rerating from next year IMO. This bank wont be available at 1.2 p/b in FY24 imo. Key variable to track now is cost to income which will decide when 15% ROE happens imo.

Disclaimer: invested in idfc, biased, might add more next week based on good execution in this Q.

27 Likes

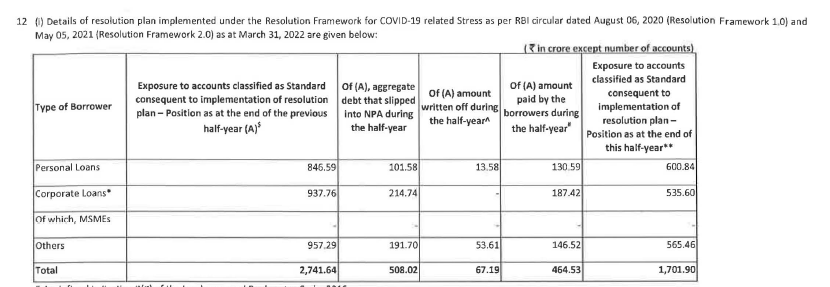

Good summary, restructured book on account of Covid has come down to 1.3% also now. Bank is still carrying Rs 165cr as additional Covid provisions.

This is down from 2.9% in September 2021, so the drop is significant.

3 Likes

As discussed above the toll road is one of the projects in Mumbai run by IRB. They just finished a fund raise of rs 5,000cr last quarter for paying back debt which is prob why VV is so confident it will be eventually repaid.

1 Like

One more point to consider while reading the result is that in the last quarter(Q3FY22) there was a prior period income of 110crs odd(related to Vodafone idea- source concall) that was recognized in the NII.

Normalized for that, NII is up by 8.03% QoQ which in my view is the best in the industry. NIMs are up from 5.90% to 6.27%.

Double digit RoE by Q4FY23 means an EPS of almost 1 rupee quarterly by Q4.

4 Likes

This topic is temporarily closed for at least 4 hours due to a large number of community flags.