This is the legacy book from pre-merger, which they are trying to bring down, as guided. It had lot of issues leading to defaults and NPAs, which the bank is having to clean up even now

1 Like

In several concalls and interviews V.Vaidyanathan clearly stated that they would not like to to do any infrastructure loans in the future. I request you to go through them in YouTube. I don’t know whether he would change his mind but as of now I’m sure about their strategy.

1 Like

I feel it is very hard to give such detailed guidance at the time of the merger. imagine youve just merged. there are so many possibilities, people, business environment, unknowns that woudl hit you over the next 5 years, investments that would be required to be made, unknowns such as PSL cost etc. for example you would need to guess the interest rates at which you would be lending, what products, what your cost of funds would be, etc. and indeed, so many variables changed, they took big hits (Rs. 2000 cr as per managment account wise disclosures on Dewan, Reliance Capital, infrastructure accounts), then there was COVID. wondering how a management puts out numbers when there are so many uncertainties in life/ business. Not surprising they are behind the curve on ROE, ROA.

3 Likes

And its not that it was an establised business to start with, the bank was in its nascent stage and the uncertainties would have been that much higher at the time of guidance. so the guidance woudl have been broadly “directional”, so we should be aware that some guidances may not be met… I am doubtful about ROA, ROE.

Hdfc Bank has a sizable position. It is not too far fetched to think that it’d impart necessary guidance in positioning it on the Indian landscape.

The guidance they gave is for F24-25. I don’t think they are lagging behind on any of the parameters. Even ROE and ROA I’m confident they will achieve the numbers.

3 Likes

As an industry standard every bank has their settlement waiver grid for all NPA n write-off accounts where banks used to settle these write off retail loans on an average 50% of principal outstanding of loan whereas IDFC first is doing at an average of around 30-35% which is denying their recovery amount

1 Like

Does it mean that IDFCF bank is doing one time settlements for ‘retail NPAs + write offs’ at recovery rate of 35% of the principal amount, for closing the chapter, whereas industry rate is 50% recovery of the principal ??

1 Like

I feel, at this stage IDFC should make an offer to IDFCF bank to compensate for the unexpected large NPAs of several thousands of crores. These were totally unexpected surprises for the shareholders who invested at the time of merger and shareholders of capital first. I am sure the IDFC management must have had an inkling of the impending defaults. That would help to accelerate the growth of the bank and create a win win for all shareholders.

1 Like

Rating Action

Rs.3000 Crore Tier II Bonds (Under Basel III) CRISIL AA/Stable (Assigned)

1 Like

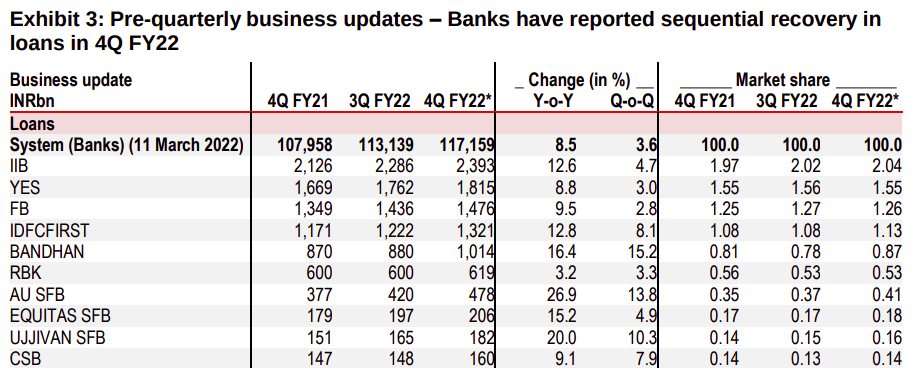

IDFC First has increased its Market Share in Loans as well as Deposits, everything is falling into place for IDFC.

12 Likes

It’s ok with the legacy book running down organically (given its already reduced) or being brought to zero.

I would see it a big negative if the bank does incremental infrastructure funding because:

- Infra lending is a difficult business: Many reasons but the main ones are a) infra projects are complex and take a long time to complete (true for power plants (hydro/ thermal / nuclear) / metros/ large roads / irrigation projects). Projections say completion in 5 years, when in practice it takes 10+ years (project challenges, environmental clearance, land acquisition, etc.) A big delay derails project economics and security of lending. You also have to then fund the inflationary growth in costs or roll over the credit b) There is v high asset liability mismatch: projects start generating cashflow after a long period but you have to refinance your liabilities side in that time (retail deposits are not a good solution) c) The margins are very thin and don’t compensate you for the risk. Funding for infra projects is competitive (you can borrow globally) and you have v. low spreads. You make the money in good times by doing large loans and keeping Opex/AUM down but your loan book gets less granular. A single NPA could dramatically impact profitability. (Yes, I know solar projects don’t take that much time but what I say still stands. There are risks and spreads are still too thin and solar is the best case)

- Change in commentary: Management has said they don’t believe this is a good business. If they go back into it, it would be concerning because of the about turn. They would need to explain in a transparent manner what has changed so dramatically.

6 Likes

.

There may not be any non-funded exposure now and total exposure must have been reduced to just 500 crores…

4 Likes

This is a very detailed report on functioning of the bank. I recommend that folks read it.

This report, too, focuses on:

*NPA

*Cost to Income ratio

1 Like

Yes absolutely they are doing settlement with high POS waiver compare to other banks

2 Likes

Sir,

Can you please explain what does “high POS waiver compare to other banks” mean? And how does it affect the long term avenue of the bank ops.

Thank you in advance.

2 Likes

2 Likes

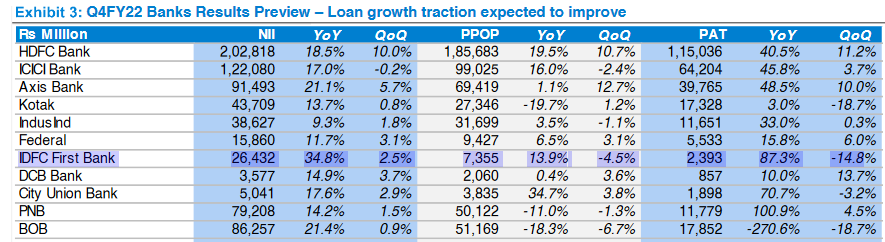

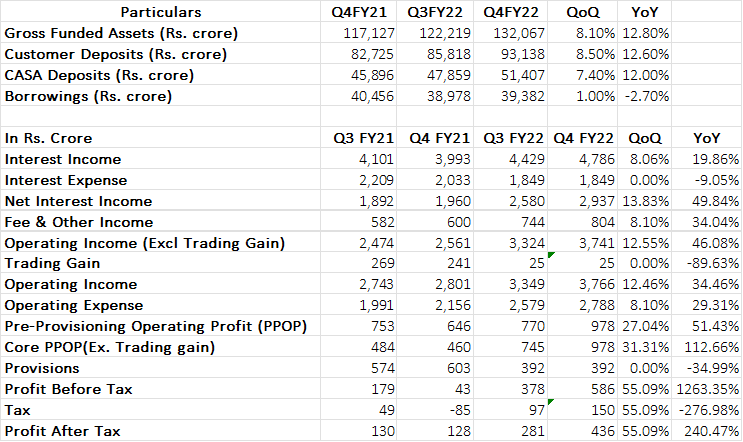

Was looking at the broker estimates for Q4 expectations and saw that the street is expecting a QoQ drop in profits for IDFCB? Below is from a PL report on the sector-

As you can see they are only expecting a profit of Rs 239cr in Q4 vs Rs 281cr in Q3 despite Gross Advances going up by 8% QoQ and even CASA going up by 7.4% QoQ.

I have run some very rough calculations and frankly am surprised by the street expectations. Maybe that’s why stock has fallen so much as very low expectations are baked in.

Below are my calculations-

I am assuming yields remain the same as Q3 as does the cost of funds and trading gains. Fees Income and Operating Expenses are growing by the same amount as adances did QoQ. Provisions also are assumed to be same as Q3 largely inline with trends of recent banking results where provisions have fallen both QoQ and YoY for all banks.

Despite what I feel are very conservative assumptions the bank still ends up with a profit or Rs 436cr. This is an increase of 240% YOY and 55% QoQ. Even the PPOP is increasing 55% YOY. Keep in mind that all of the provisions released from Vodafone in Q3 were utilized to increase provisions on legacy assets and increase the PCR and were NOT written back to the P&L. So provisions shouldn’t increase massively QoQ all things being equal.

Basically expectations are very low and IDFCB could easily surprise us on the upside. Even the shares dont seem to be pricing in much.

18 Likes