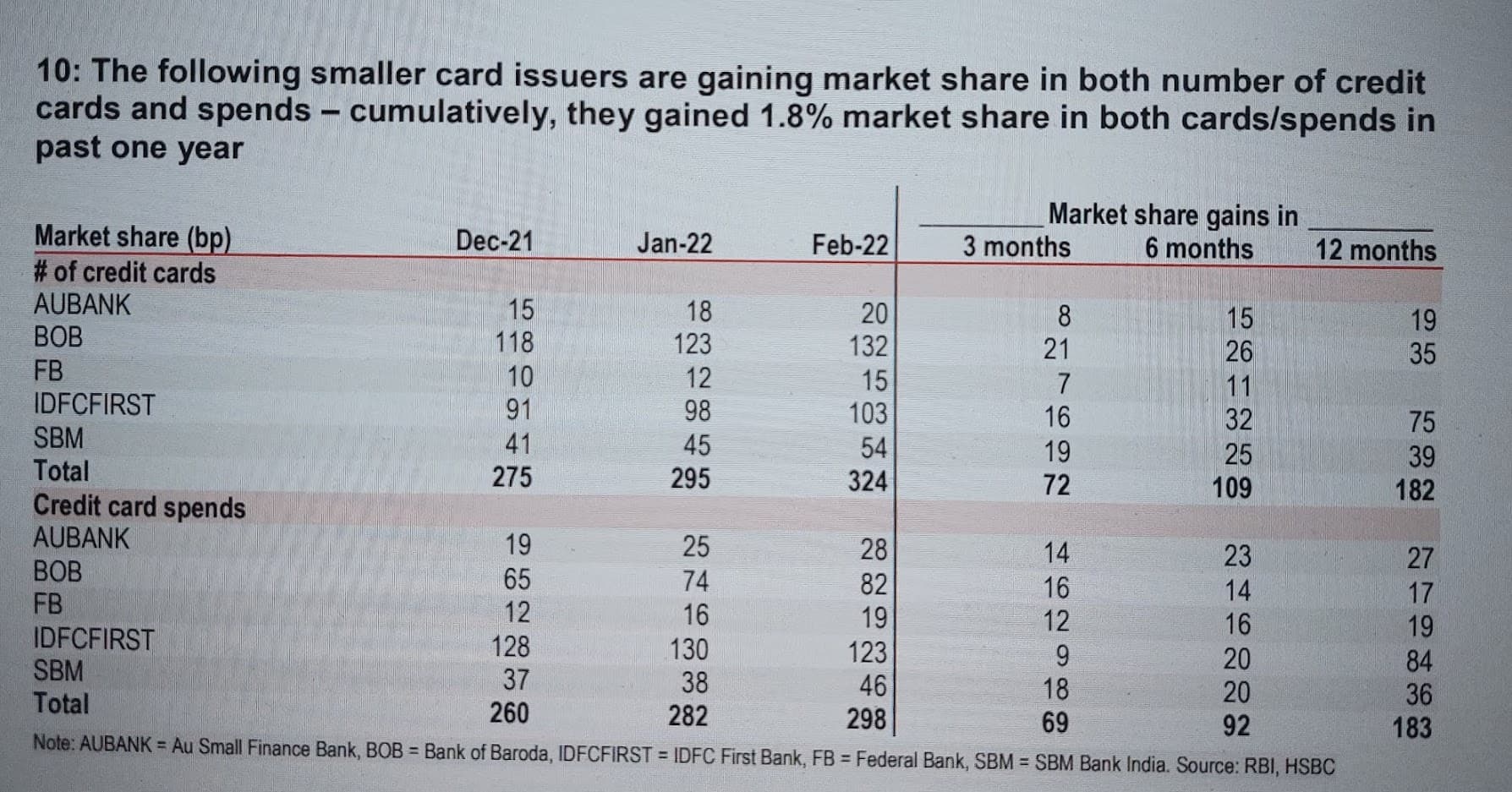

IDFC First is building a great franchise in credit cards, we can see Market Share in # of Cards is less than BoB but in spending it’s greater than all.

12 months market share gain is also the highest in issuing the cards as well as the spends

15 Likes

Feb is not usually a high spending month, and with 2-3 days less than a normal month spends per card are usually less

Coming to the case of IDFC first, they are closing down their partnership with OneCard and most of the old OneCard users are shifting from IDFC issued cards to other banks issued CCs, so maybe that’s the reason. Can’t really say when the shift started, but it’s definitely on.

As of now, they have 7 lakh Credit Cards and 39 Lakh Debit Cards, we have to see how much they can cross-sell to ETB customers.

5 Likes

IDFC owns 36% in the bank at the moment and regulatorly can own 40%, hope they are looking to increase their holdings at these prices prior to the reverse merger. Will be a win-win situation for both set of shareholders. They should have a decent amount of cash especially with the AMC generating roughly 50cr in profits every quarter.

3 Likes

Can any senior member help understand whether IDFC First bank gets back some money due to this☝️

Thank you for this vibrant thread

1 Like

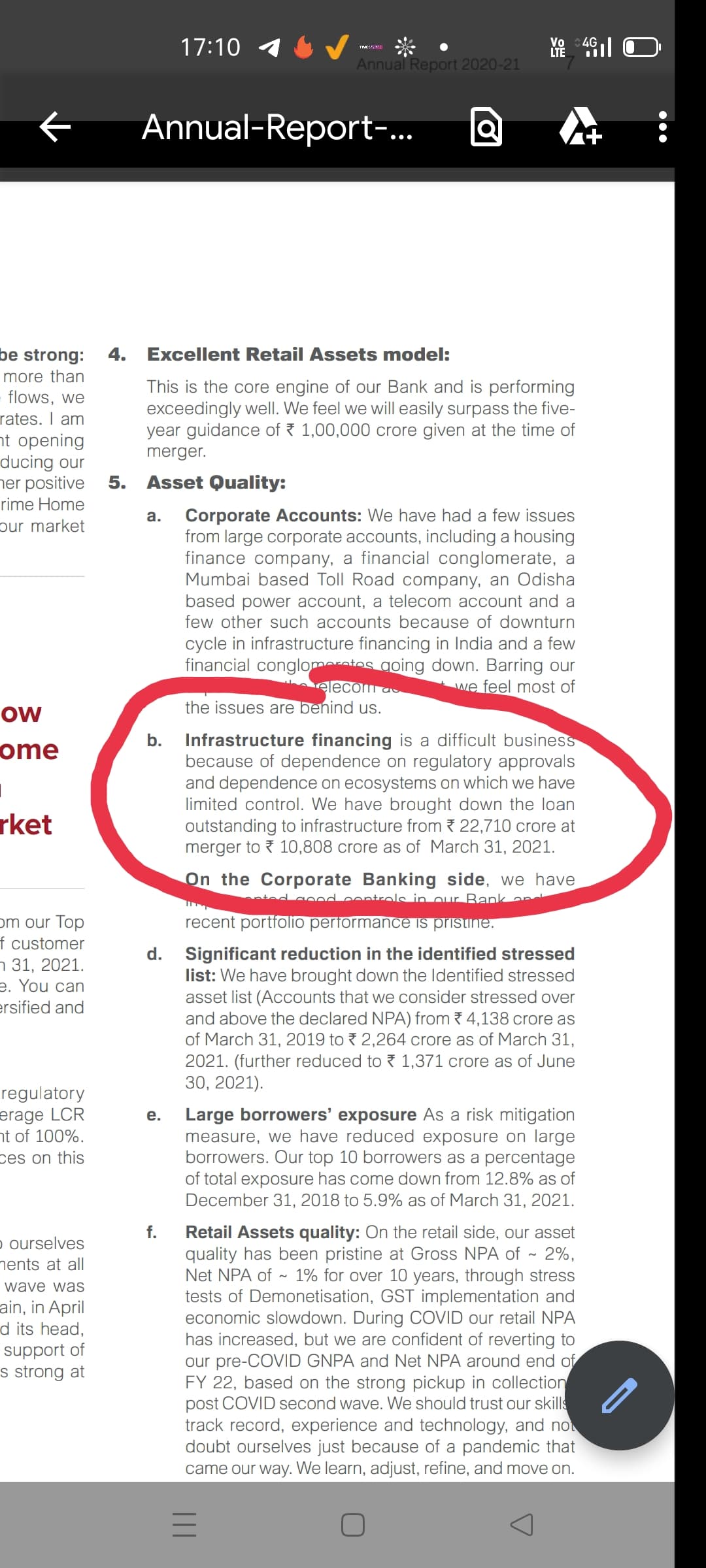

IDFCF had no exposure to ILFS so makes no difference.

3 Likes

This topic is temporarily closed for at least 4 hours due to a large number of community flags.

This topic was automatically opened after 24 hours.

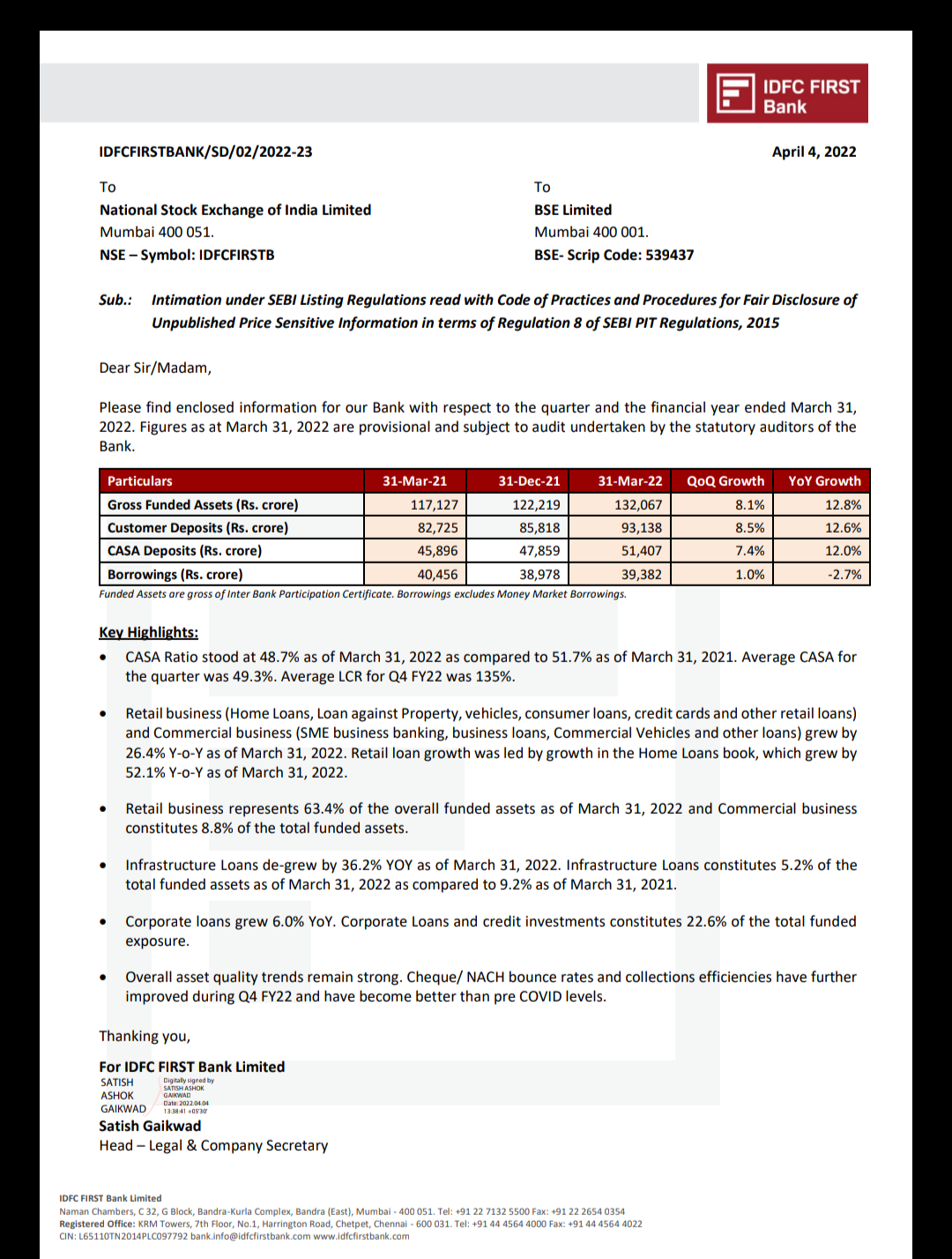

First quarter that one can confidently say that growth is finally back and is likely to continue in the coming quarters and years. Gross funded assets are up by almost 10,000cr QOQ, just to put that number in context Bajaj Finance has reported a similar figure with a much larger balance sheet.

18 Likes

It should be noted that CASA ratio dipped by 300 bps… looks like if loan growth is strong, casa % will be under pressure.

1 Like

If CASA ratio is down because higher loan growth, it is still ok but if it is down because of low interest on Savings Account then it will be concerning if outflow continues.

2 Likes

From 1st April 2022, savings account interest is hiked to 6% (from 5%) for the range 25 lacs to 1 cr. This could be due to the CASA dip.

Key Monitorables for me based on th last quarter results:

- Growth in Loan book size and 2.) Reduction in opex.

Loan book size

I was pleasantly surprised by the significant increase in gross funded assets.

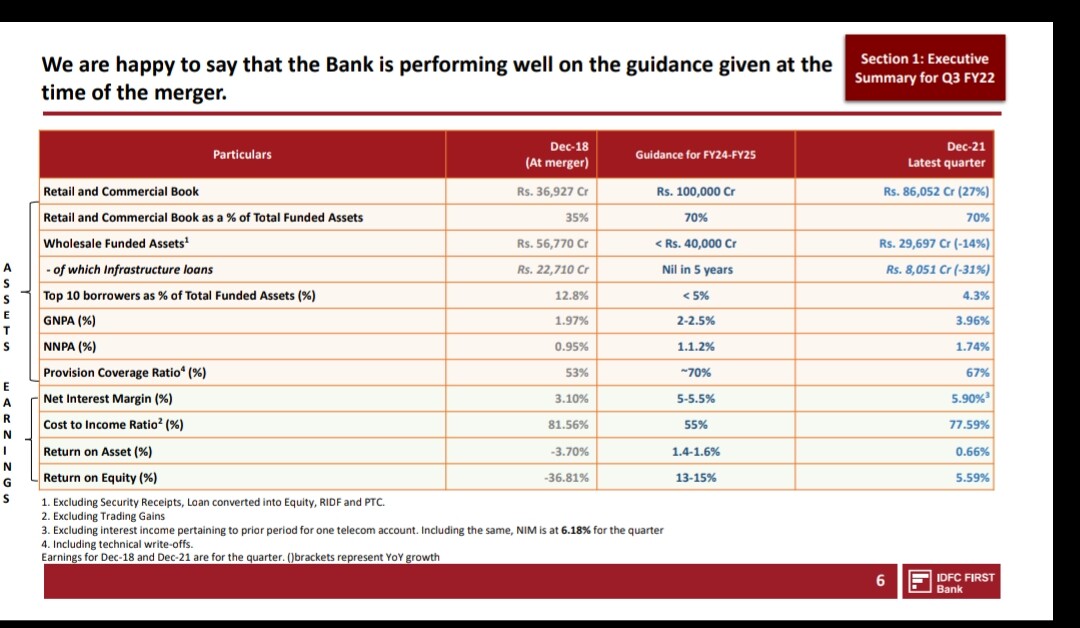

The company achieved 25%+ annual growth rate in the retail+commercial loans (72.2%) despite one bad quarter due to covid in FY22. Corporate loans (22.6%) grew 6% yoy. Infrastructure loans (5.2%) degrew by 36.2%.

You can observe that both retail+commercial and corporate loans are increasing. Infrastructure component is only 5.2% and it will be gradually decreased to zero. The loan book size didn’t grow meaningfully in the last three years but we can expect 20% annual growth from now on.

However, we need to watch out for any drop in NIM because of increase in Home loan component in the total loan book.

Management is walking the talk as far as loan book is concerned.

Im waiting for the quarterly results for opex, and I hope management surprises on this front too.

4 Likes

Being I m from collection background what I have observed that IDFC first is doing settlement of unsecured retail loan NPA account at higher percentage of waiver which is denting their NCL

Disclosure- Already Invested

5 Likes

Can you please elaborate on what you mean by that ?

3 Likes

If every other financial institute shy from infra component, then who will fund those projects?

I read in PEL that they are also reducing exposure to infra, real estate.

Please throw some more light on it and what is NCL?

2 Likes

I hope these get back into the green. Capital is required for growth of loan book.

Yes, @sritej_king we need to watch…

*NIM

*Cost to Income ratio

But, most importantly… For a retail facing Bank we need too watch for amounts of accounts slipping to NPA. If the Credit Cost goes beyond guidance of 2% we must raise a red flag. This alone can be a hindrance enough.

2 Likes

I agree. It is really surprising that many are expecting Infra book of IDFC bank to come down to zero. It may be true for legacy book but expecting that the bank will never fund infra projects is really impractical. As long as underwriting is good and loans are adequately ring-fenced, banks will continue to fund Infra projects. If Tatas or Reliance are executing an Infra project, will IDFC shy away from funding it… i don’t think so? Banks can take a call on their mix but expecting zero for a large domain like Infra is really unrealistic

2 Likes