apart from idfc amc , what else has to be sold by idfc limited before they can approach rbi for merger request.

why is idfc share price climbing up and idfc first bank share not moving. If idfc limited gets favourable deal in merger process like 1.4 etc, what changes fundamentally for idfc first bank shareholders, anything like voting rights etc of idfc first share holders. Any idea if idfc limited at present 36.5 % holding , how much voting rights they have

If you are a idfc first bank shareholder then a unfavorable deal would actually be better for you.

As if that is get done then the number of outstanding shares will go down and market will correct that and you will benifit in more ownership and if market capitalisation comeback to normal then you will gain and extra alpha as it’s more like a open market buyback type deal for you without using any company money.

If they get 1:1 deal ie what they hold in percentage will be no net loss for you or a gain for you.

If you are a idfc shareholder then a 1:1 would be best for you and even little bit underpay might not be the best deal but not a worse deal either as your arbitrage would be less but some may or may not be there and if idfc first share Market cap return you will get some diffrence back.

[

“We are financing close to 500,000 loans every month, and are investing heavily in technology, the customer interface, stack and code, and will be in a good position to give good-quality solutions to startups for their banking needs,” Vaidyanathan said.]

Does anyone know average ticket loan size?

3 Likes

5 Likes

Some times it seems like his contributions to the society (or at least his concerns for his colleagues and friends) are too good to be true. One more gesture which cements my belief in his leadership

8 Likes

Nothing against Vaidyanathan. As investors we are suppose to evaluate business quality and its leadership capabilities on execution. All CSR news or such stories are just a distraction. Let us NOT fall in love with management or their actions.

Remember - we all are suckers for good stories. It is a cognitive bias we all carry. Let us always be mindful of it whenever we make financial decisions

Just my 2 cents. If post feels offendable, please flag and I will delete it.

26 Likes

Every time I hear the capital first story (loan book increase) in every quarterly review and other external forums and speech by the management , I feel now it’s too much of a broken record. It’s time for them to start mentioning the IDFCFB stories going forward. Hoping for the best. Awaiting the next quarterly result.

8 Likes

The book value per share has come down from 38 at merger to 32.5 now. thats a big drop. they posted losses six times in a row after merger and wrote off Rs. 2000 crores that led to this. (details of corporate and infra loans listed in AR). frankly, for a stock that has reduced book value per share, wonder why the valuation increased from 0.93 p/B at merger (share price prior to merger date used for this calculation) to 1.4 X book. even today ROE is quite low, so p/B is 1.4, well, am not able to understand this.

2 Likes

Valuations are forward looking, what’s happened in the past is less important than the future trajectory of the business…

8 Likes

Thanks for the reply. Actually, I agree with every bit you mentioned. So, no offence at all. In fact, very good to see logical points with differing views.

On the part of management, there is history of more than two decades to judge an individual (Vaidyanathan here). Additionally, one can analyze the guidelines they have been giving since IDFC and capital first merger and the results to compare against those projections.

I believe the quality of the business is also improving though may not be best in Industry but it is getting better incrementally. Hence, my belief. Agree, I may be biased.

Disc: invested

1 Like

Disc: invested

I have a stupid doubt on this share gifting (which I personally in awe of) BUT wearing an investor hat - can this be seen on the negative side by institutional investors in that the skin in the game of Mr. VV has gone down. Is this even a relevant aspect to be discussed?

Thank you for having such a vibrant community.

2 Likes

My two cents on this gifting shares…

- Gifting shares is most transparent way of helping ( Tax & auditing), and informing shareholders. I think this is why we are speculating. I don’t understand why it is so scary…an Individual is saying , see I am helping who are in need and letting you know via disclosures. And person received also pay tax.

- Skin in the game? come on guys… Think this way …do you gift crap to others. you gift someone something which you think it will be useful for them. VV clearly knows , the value of his company and the stock.

- He mentioned in the AGM, that his only wealth is his stock and if he has to help it has to be via stocks.

we all know there are several instances where the key management personal (kmp’s) hedge their stock, do pump and dump based on insider information and other sort of shady stuff. If those are allowed why gifting and helping is negative

11 Likes

After seeing your query, I went and compiled the value of his past gifting by multiplying the number of shares with the share price on date of gifting. Frankly I was a bit shocked to see the value of his give away… it comes to about Rs. 70 crores including to social causes. And this process of gifting has been going on for a long time even pre merger except it did not come to light because CFL was not a big company. Since this has been going on for years together, I think the market will see this as a regular trait and not bother about it.

I saw the startup awards show where the anchor was asking different questions from different leaders in the audience… he sked him why he gifted so much… he was visibly short of words and mumbled some answer like stock in demat account is of use only if someone sells it and uses the money … or something to this effect… think investors will ignore neither positive nor negative. Think we can ignore.

6 Likes

As per this article IDFC First seems to have good hold in EV financing. "IDFC First bank was an early adopter of the EV market and has established itself …

Read more at:

2 Likes

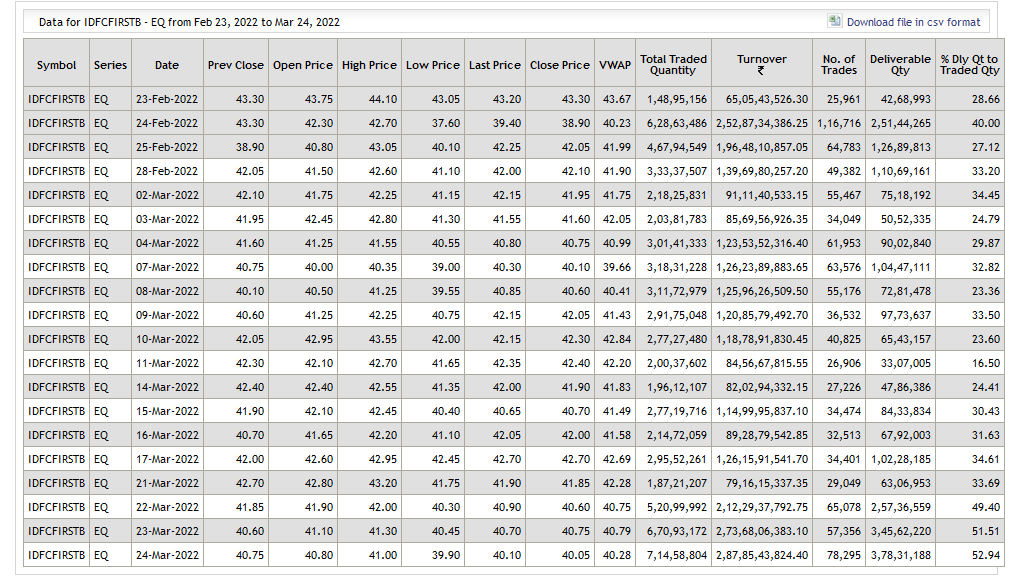

Interesting delivery data on IDFCF over the last three days, someone is accumulating large quantities of the stock at this price. Massive jump in delivery volumes.

15 Likes

Following up on this post, as per this story seems the volumes have jumped as one of the FIIs has been selling. My guess is Odyssey as its an Eastern European fund and might have been impacted by the Russia crisis

Details of Odyssey 44 Odyssey 44

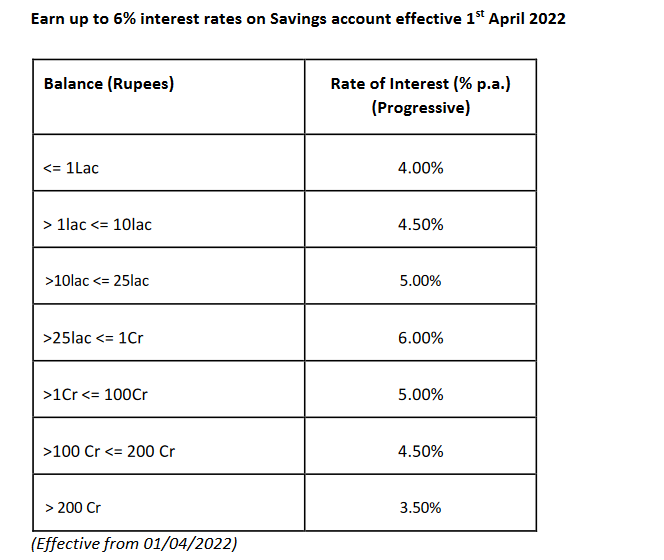

Looks like all the excess liquidity has been drained out by growing the loan book and now IDFCB is looking at growing their CASA again; offering 6% now for deposits between 25Lacs-1Cr.

Not sure how many people have such deposits in their savings accounts but will definately attract new customers from other banks!

2 Likes