It’s in the last of the presentation. He is more focused on making a world class bank at balance sheet level not at per share level. We don’t make money unless EPS and Book Value Per share improves.

Great numbers. This will hold the price, and probably take it to new highs, as and when the index moves.

Observations:

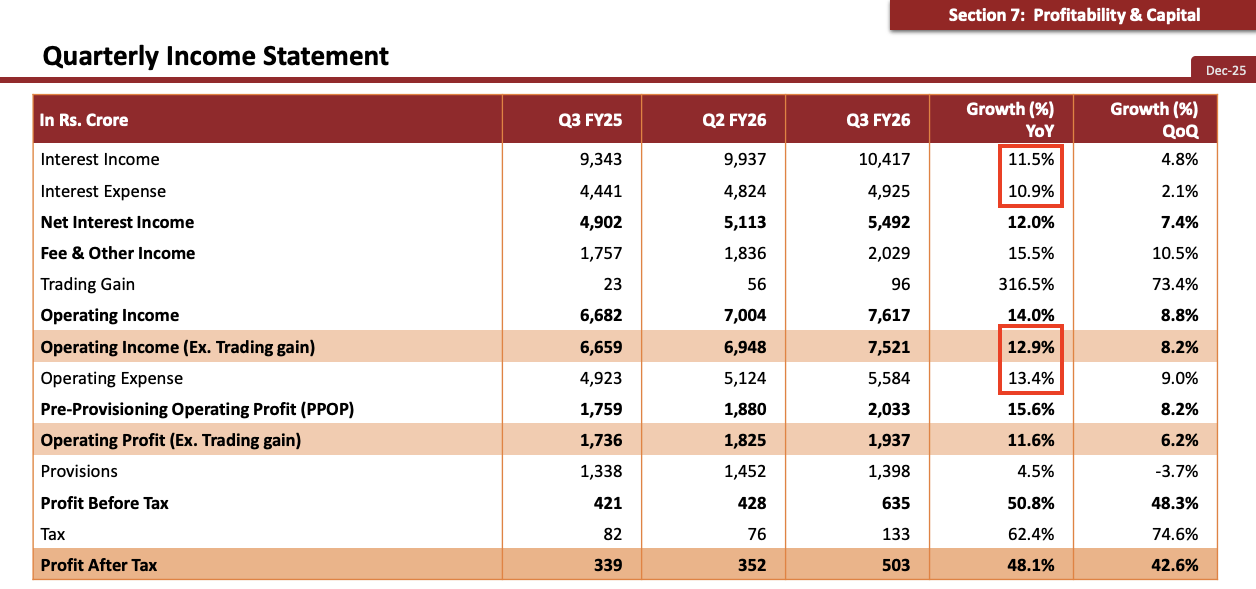

Biggest Loan growth in credit card, ofc, after gold loan, which is for the time being. CC are their forte. Keeps NIMs high.

PPOP growth QoQ is 8.2%, that helps me to hold my breath for a few more quarters.

Highest Quarterly net profit in a year.

Liked reading this… : “In FY25, total Business (loans + customer deposits) grew by 22.7% YoY, but Opex increased only by 16.5% YoY

In 9M FY26, total Business grew by 22.6% YoY, but Opex increased by 12.4% YoY”

Basically, there is noticeable improvement in Opex, which is now the only pain point.

Branches and CC are major contributor to high Opex, for that…

Credit Cards C:I has come down from 240% to 98% in ~4 years

Bank intends to grow branches only about 10% annually against estimated deposit growth of ~25%.

Good Quarter all in all….

My advice to fresh investors:

Wait for the price to come to it’s BV, 54. Else let it be. There are many other fish out there. See sectors like IT, EMS, defence, where there are clear tailwinds.

The best thing in this quarter is Interest Income growth beating Interest Expense growth. This gap used to be around -5.5% for many quarters. Seeing it reverse gives so much relief. This is a result of sequentially improving NIM.

Due to this, the gap between Operating Income and Operating Expense has also narrowed down. Once this reverses, we’ll see the real operating leverage that VV has been marketing for so long (Subject to no new shocks that this bank has become used to :P)

My sense is that from here on, these factors should dominate:

NIM remaining stable or improving slightly due to the SA rates brought down recently and expectation from RBI to keep repo rates unchanged in the next MPC meet

C/I ratio improving as the double load of raising CASA for growth as well as replacing legacy borrowings will be completely gone and it’ll only be for growth. Legacy high cost borrowings are almost gone now

But again, subject to no new shocks from VV and team. One-off provisions spike won’t be an issue but nothing structural should change.

Past learning is that micro-finance was not just a provisions issue but it impacted NIM as well as C/I because it was a very high interest driver at high cost. With the MFI exploding, the bank lost through provisions as well as through dented operating leverage

Thanks for sharing your valuable inputs. As a non finance person with some business understanding I see following points indicating significant upside for the bank

Projected cost to Income ratio of 65% in FY27. If they achieve that I guess it will add INR 1.5-2 Rs/Share on EPS Annually. does that make sense?

If provision stabilizes to around 1000 Cr it will add further to EPS?

Loan book growth of 20% even with current NIMs will give a 20% upside in EPS?

So I guess it looks like a marathoner who is now picking up pace for the laps which matter the most?

Great observation. I think this is true of numbers for FY 24 as well. The only explanation I could come up with (after unsuccessfully trying to adjust numbers here and there) is that these “Operating profits” are computed differently from the headline numbers. This is also partly buttressed by the fine print “above numbers are based on internal transfer pricing of the Bank” on the above slide and similar slide across other quarters, and from change in Assets - credit card has been included and FY 25 numbers have changed vs shown in prior quarters.

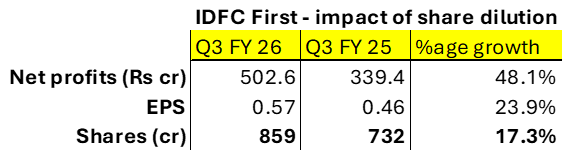

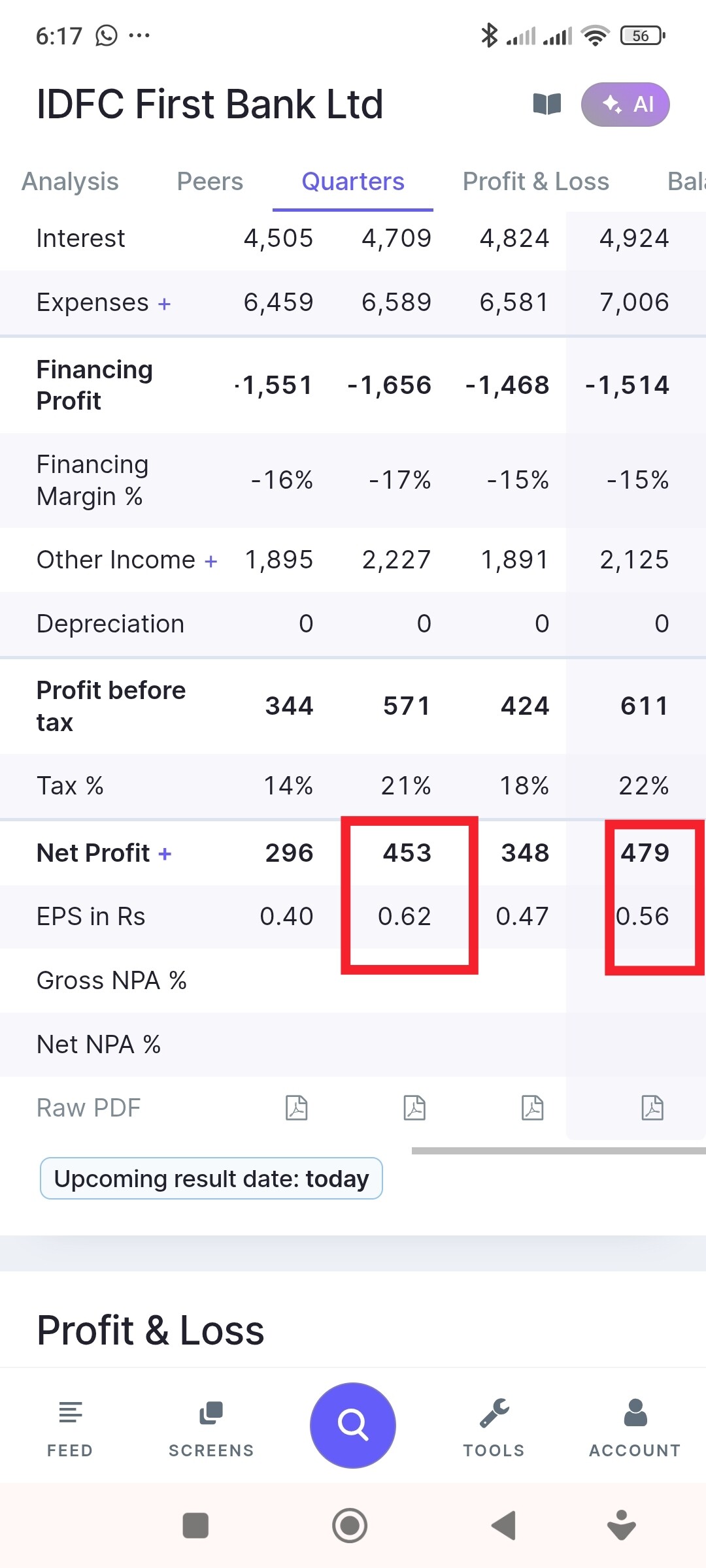

The results also show the impact of dilution on per share earnings; even as the bank may show tremendous growth in net profits. In Q3 FY 26, net profits grew 48%, but per share growth was about half of that at 24%, with ~ 1/6th share dilution.

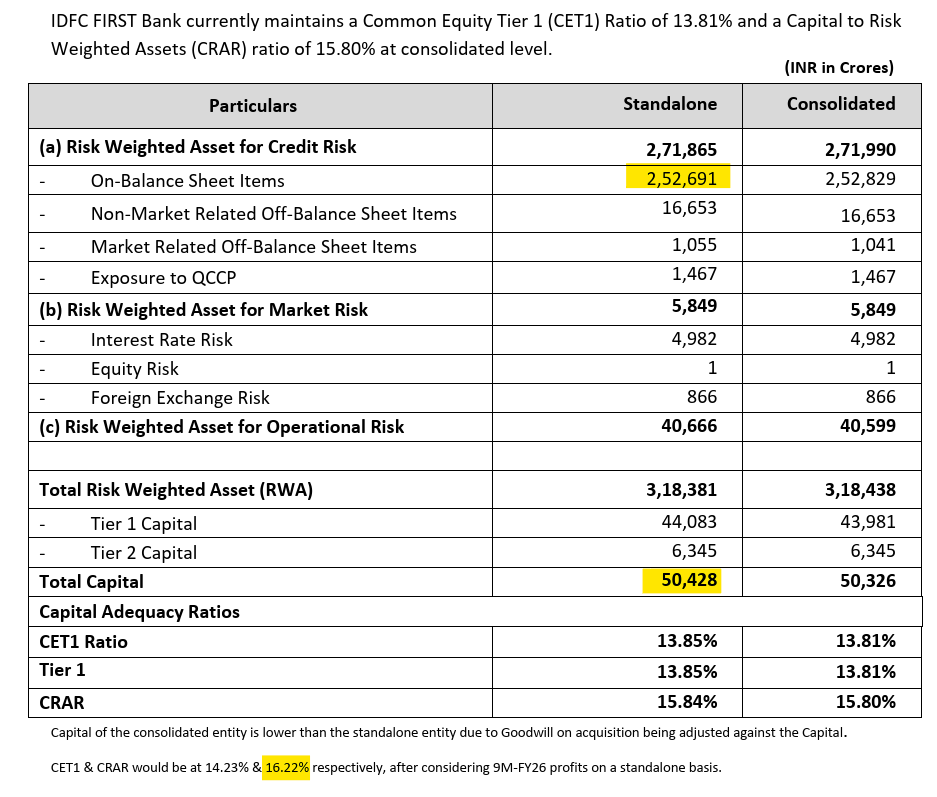

But worryingly ROE still remains very low, this quarter it was 4.7% annualized. The CAR stands at more or less where it was in Dec 24 (16.22% vs 16.11%) even after a 7,5000 cr raise diluting then shareholders substantially. If the low ROE continues even as the bank tries to grow, it will have to dilute again but with a larger amount.

Let’s run through very approximate back of envelope calculations:

Here are the CRAR (or CAR) numbers for Q3 2025 from Basel III report

As per this report, the bank has Rs 50,428 cr of capital supporting Rs 2,52,691 cr of assets. Adjusting for additions till Q3 FY 26, this number grows to Rs. 51,641 cr. Now let’s say the bank grows the asset book by 20%, i.e. 20%* 2,52,691 = Rs. 50,538 cr. Let’s assume the (a) asset composition of this new assets is the same, (b) other assets and (c) Credit Risk / Ops Risk capital requirement remains the same as in Q3 2026. Then the total RWA is now Rs 368,919.2. To maintain CRAR at current levels of 16.22%, the total Tier 1 + Tier 2 needed is Rs. 59,839 cr. Of this if Tier 2 is not raised (already at higher levels), the entire capital must be supplied by Tier 1 or Equity Capital. This comes to about Rs 8,200 crores.

Where will this Rs 8,200 crores come from? Only two sources - profits and/or capital raise. Looking at Q3 profits of Rs 503 cr, or ~ Rs 2,000 crores annually; falls far short of Rs. 8,200 cr. needed. So if IDFC wants to grow at 20%, but does not get high returns on equity, it is the inevitability of mathematics that IDFC will need a fund raise, mostly diluting current equity owners.

Worse, if it happens by diluting existing shareholders at a low point of share price, the dilution would be even worse. For eg the ~ 124 cr new shares issued was done at Rs 60 for raising Rs. 7,500 crores. Now if the same Rs. 7,500 crores were raised at Rs 85, the dilution would have been lower by 30%!!

So nett the bank has to improve it ROE for current minority shareholders to benefit from the stupendous frowth in the Bank. If not, then the ~ 100 year old Ben Graham adage that “Obvious prospects for physical growth in a business do not translate into obvious profits for investors” will have a new use case!

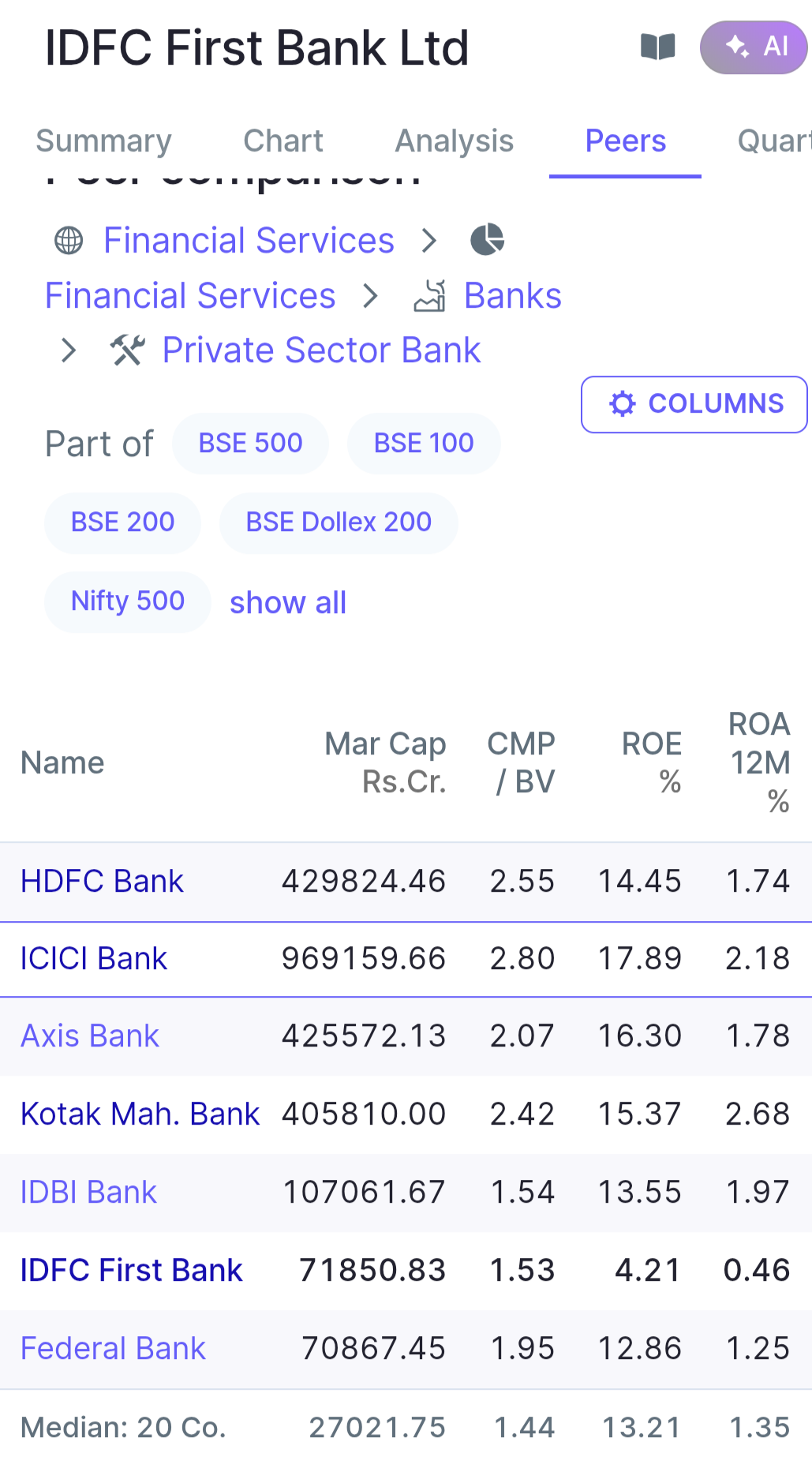

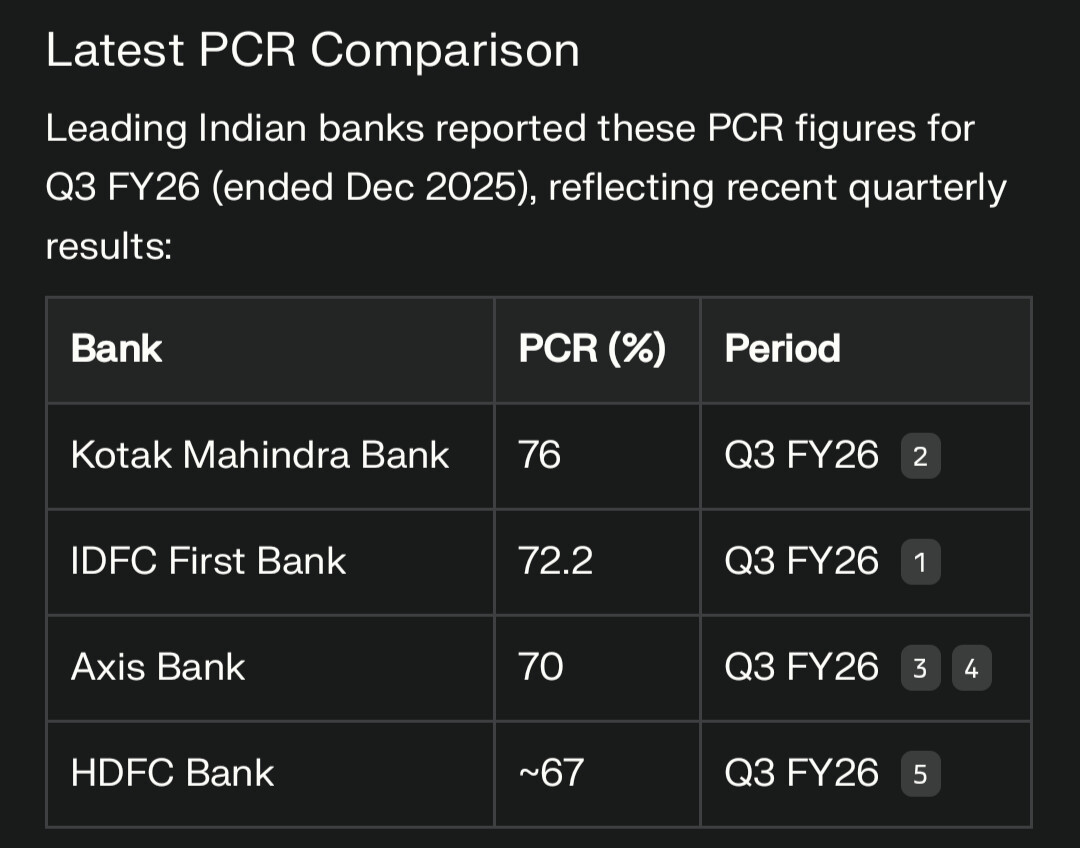

The answer probably lies in the same screenshot. Compare columns 2 and 3. All other banks have return on book that is more than 3 times IDFC First. Imagine your stock to be a bond with the EPS as your coupon. At 4.21% (or 4.7% per my calc) it would take 20 years to double the book for IDFC First, for others it would take no more than 8. So it appears okay to pay a higher markup over book for others than for IDFC First. Not saying whether market is right or wrong, but why a business who’s profits depend on book, may command a higher value.

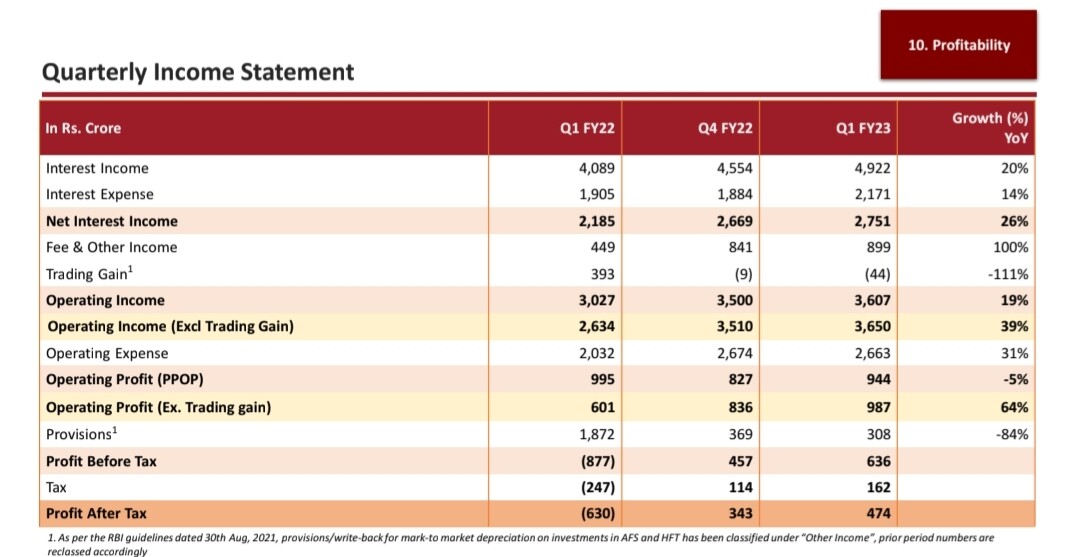

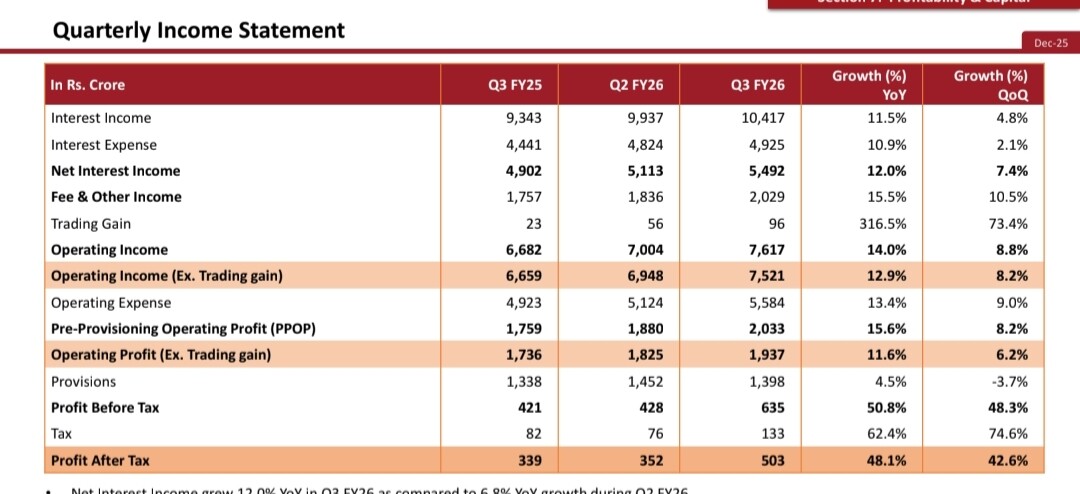

If we compare Q1 FY23 and Q3 FY26 in the two images given above, what do we actually get?

Almost all parameters have more than doubled, yet profit is still at the same level.

The bank is making ₹500 crore profit on a total income of ₹12,500 crore.

Now look at Federal Bank’s latest results—with total income of around ₹9,500 crore, it has reported profit of more than ₹1,100 crore.

What’s more confusing is that Federal Bank’s NIM is lower than IDFC First Bank’s.

Despite having such a large loan book, I fail to understand how the bank is generating such low profits.

The cost-to-income ratio this quarter is 74% (excluding trading gains).

How will it come down to 65% by FY27 when the bank is not even able to bring it below 70% so far?

In both images, every parameter has improved, yet there is no meaningful improvement in profit.

I also don’t understand the provisioning—it should ideally come down to low three-digit levels, but that doesn’t seem to be happening.

It feels like there are still many unresolved problems in IDFC First Bank.

Honestly, it seems VV has been delivering the same kind of results for the last 7–8 quarters—the top line keeps improving, but by the time we reach the bottom line, things look worse quarter after quarter.

I am sure Federal Bank isn’t adding 10% new branches. Therein, lies your answer.

Idfcfirst bank is using a bulk of its profits into growth, FEDERAL Bank and others are mainly building equity. Hence, they don’t need Equity dilution. Old banks, established banks, whereas idfcfirst is still new.

interesting bit is, Federal Bank in its 50 years of existence is only at 70K Cr market cap. Which Idfcfirst did it in only 7 years.

Results from a layman’s POV won’t be fun. It’s expected. If u want to see excitement, see it’s Operating income, and compare it. But, if u go to Operating profit, then it’s ugly. And that’s what this thread has been discussing, Opex nahi hai! It will take time, 2029.

Will share my views on some of the points raised in the last few posts.

Can IDFC Bank deliver 65% cost to income (C2I) in FY27?

Q3FY26 cost to income is 71.8%. If income grows by 20% in FY27 (in line with loan book growth of 20%), and opex grows by 11% in FY27 - then the cost to income ratio for FY27 would be 66%.

Note that opex growth is showing a declining trend - indicating operating leverage playing out - it was 16.5% in FY25, and much lower at 12.4% in 9MFY26.

Why did cost to income ratio not come down in FY26?

Because the bank decided to change its loan book mix to less risky, and lower yielding loans. For example the microfinance book has degrown from ~14500 cr to ~6500 cr. This meant that Net interest income in 9MFY26 only grew by 8%, in spite of the loan book growth of 20%. In the earnings call, the management said that loan book mix adjustment is over, and so Net interest income growth will start matching the loan book growth again.

How did the bank benefit from change in loan book mix?

Change in loan book mix meant that bank is now lending more to segments which carry lower risk weightage. The direct consequence of this is that Capital Adequacy Ratio went up by 11 bps QoQ in Q3FY26, inspite of loans growing by 5% QoQ.

A combination of the bank lending to segments with lesser risk weightage, and with improving profitability - the equity dilution in coming years will be much lesser than in the past. Dilution is more of a demon of the past, and a much smaller concern going in to the future.

How does IDFC bank compare with Federal Bank?

At the time of merger of IDFC Bank and Capital First (Dec 2018) - the total business (loans + deposits) of IDFC First Bank was 1.4 trillion rupees. At that time, the total business of Federal Bank was 2.25 trillion. Today the total business of IDFC stands at 5.6 trillion, and the total business of Federal Bank stands at 5.6 trillion too. That is to say - IDFC business grew by 300% in the period when Federal business only grew by 150%.

What would happen if IDFC lowered its pace of growth to around the same as the rest of major private banks?

If IDFC decides to grow its loans and deposits at only 12%, instead of the current 22% growth - then IDFC can get away with giving only 4% max on savings accounts (instead of current 6.5%), and cut down lots of employees and other operating expenses. Its profitability will easily shoot up to low or mid teen ROE. That’s the growth vs profitability conundrum that IDFC is facing today. But, the good part is that once operating leverage plays out, and the big investments taper down - IDFC will be the only major bank delivering both growth and profitability. Others will only be able to deliver only one of the two - either growth or profitability.

And that is out in the open, and well accepted fact about this stock.

However, my hope is, with this mfi episode behind us and the stock story does not meet any more speed bumps in subsequent quarters, then it is likely that the market will factor-in the future where RoA>1, even before it happens. Probably, in next couple of bull runs.

In fact that’s my investment thesis. When PBV becomes at par, around 3, i will exit. I won’t be interested in plain vanilla 18% growth.

Your comparison for overall numbers looks great but there was a lot of dilution which didn’t let the shareholders gain anything much.

There were times, when IDFC could have prioritised showing profits rather than being extremely conservative and raised money at a higher valuation. I’m not saying to throw prudence totally out of the window but a bit of smartness there could have been beneficial for the shareholders without harming anyone.

Thank god they reduced the SA rates in Jan. Even on that they should have done earlier and the the CFO, Sudhanshu Jain was also of the same opinion but VV being VV, does mostly his own thing. This was discussed in the last (Q2) concall.

Another thing, I don’t understand is how come the provisions are always so high despite all major issues behind us

Yes, I agree with you that IDFC is doing everything it can to delay profits. When RBI cut repo rate by 100 bps, all other banks cut SA rates, while IDFC alone cut FD rates. This suppresses margins and profits for 3 - 4 quarters. But this also means that the profits will come with double intensity in FY27, as Fixed Deposits get rolled over at the lower rates.

Similiarly, 81% of IDFC’s microfinance book is insured by CGFMU credit guarantee. This means that CGFMU will reimburse 72% of defaulting microfinance loans 12 months after the default date. All other banks are provisioning only the uninsured portion (28%) of such microfinance loans. IDFC alone is providing 100% for the insured microfinance loans. These excess provisions will also be reversed when the payments are received from CGFMU. This again means that profits in FY27 will be bumped up.

Regarding your question as to why provisions are so high in spite of the slippages reducing quite a bit - I can quote one example of provisioning policy playing a role here. So, for defaulting microfinance loans, 75% provision is done at 90 days after default. And 100% provision is done at 180 days after default. Which means that loans which slipped in Q1 are still causing higher provisions in Q3. This means that provisions will start reducing from Q4 onwards, as slippages started moderating from Q2 onwards.

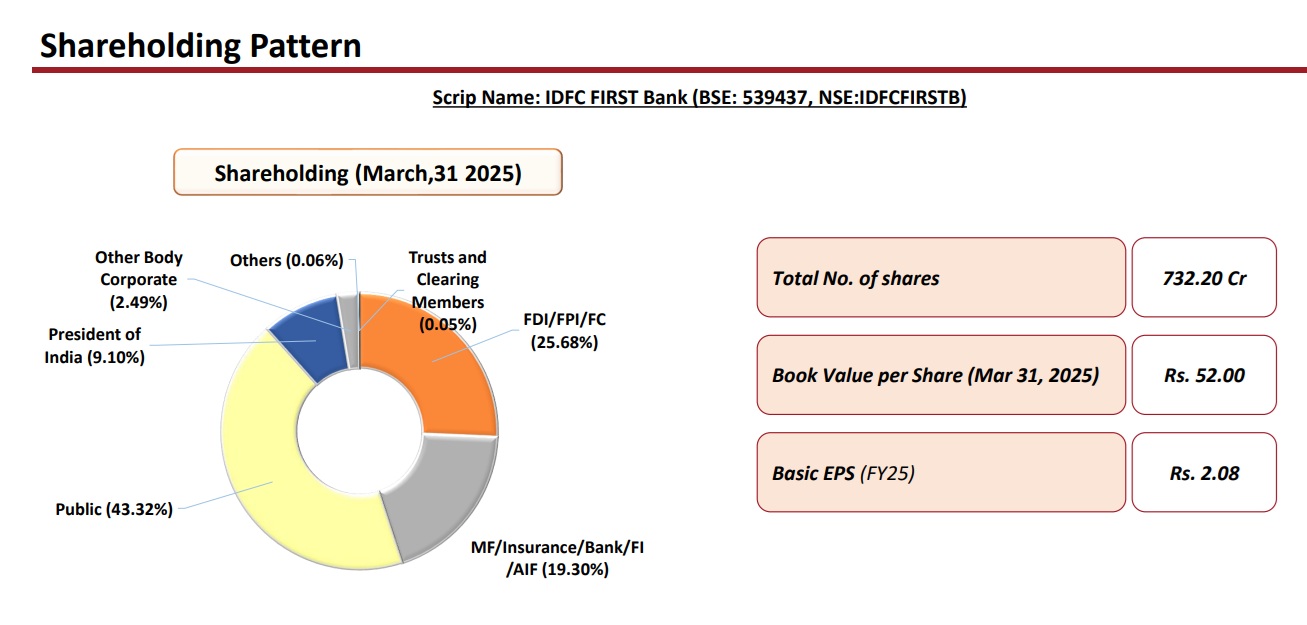

On 31st Mar 2025, public (retail) shareholders held 317 crore shares of IDFC bank. As of 31st Dec 2025, public (retail) shareholders are holding only 254 crore shares of IDFC Bank. Which means, retail have sold 63 crore shares to institutions in a short span of 3 quarters. Retail is selling because they are not able to comprehend the long term story, and only see the lack of profits right now. Institutions are buying because they like what they see coming in the days ahead.

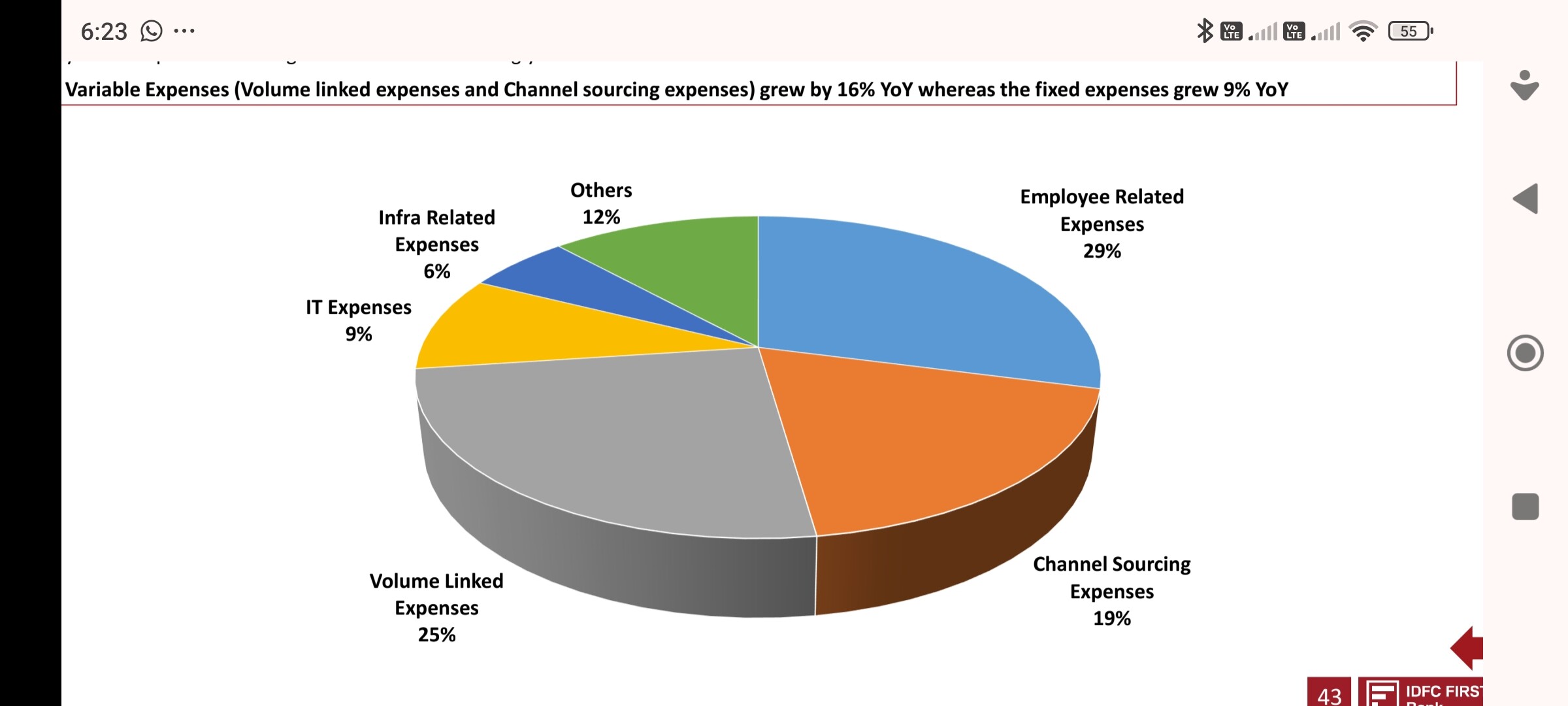

Time and again, I have been repeating on this thread, C2I is the only limiting factor for this bank…and that cannot come down easily as it’s perceived to be. There is a slide in this quarters ppt, which gives a breakup of opex , if we exclude employee expenses , then 65% of opex is volume driven

The key point to note is , if volume(growth of loan book) is high these expenses will remain elevated. And hence c2i wil be elevated.

If C2I remains elevated, the ROE will remain muted while growth continues, which leads to dilution of tier 1 capitaland hence a further fund raise is imminent in next 3 quarters( I won’t be surprised if VV come sout in June quarter and says we don’t need more funds and then raises in August)

Here is a snapshot of what dilution is doing to shareholders, despite higher profits, the eps is going down.

Based on earlier excel shared, IDFC is moving in line with fund raises, increasing it’s profits, but equity shareholders getting a sizeable return will be very difficult as even after achieving 65% C2I, he will be able to achieve a max RoE of 13%, mainly due to repetitive dilutions.(I have shared my workings in the past)

In order for shareholders to make sizeable return, the roe needs to go beyond 15-18% which will unlock book value compounding and stop fund raises - but this is only possible at C2I below 60%, which VV isn’t even dreaming of.

I strongly urge all boarders to work on projections on what VV has been saying and plug in all his assumptions, you will see the results urself.