The sheer number of opinions shared on this thread is truly mind boggling (the most happening thread in valuepickr). Same result, N number of predictions everybody seem so Rosy and bullish when the price goes up. Scroll up, check before 6 months and you will see how bearish the camp was. I’d suggest the posters to wait for the numbers, slow down a bit than building castles in the air.

5 Likes

Bank_Loan_vs_Risk_Table (1).pdf (2.8 KB)

I have uploaded a PDF in which the loan book–to–provision comparison of ICICI Bank, HDFC Bank, Kotak Bank, and IDFC FIRST Bank has been shown for the last five quarters. From the table, it is clearly visible why the RBI specifically instructed only HDFC Bank and ICICI Bank to make adequate provisions.

Microfinance business is a part of every bank’s loan book portfolio. When the RBI mandates that every bank must allocate a portion of its lending to fulfill PSL (Priority Sector Lending) requirements, then how is it possible that large banks like ICICI Bank and HDFC Bank, with such massive loan books, have lower provisions than a much smaller bank like IDFC FIRST Bank?

Does ICICI Bank and HDFC Bank not participate in the microfinance business?

As of December 2024, ICICI Bank, HDFC Bank, Kotak Bank, and IDFC FIRST Bank had microfinance loan exposure of approximately ₹35,000 crore, ₹85,000 crore, ₹10,000 crore, and ₹14,000 crore respectively. Despite such exposure, provisions were kept very low, which is why the RBI had to step in and instruct these banks to make provisions properly.

5 Likes

This is not how it should be done

Ideally you have to look at microfin loans - and provisions done on it.

You can’t compare a total loan book which has a yield of 8-9% for hdfc to a loan book which has a yield north of 11-12% for idfc

It’s not an apple to apple comparison.

3 Likes

The amount of ‘storytelling’ happening here is incredible. IDFC is very much active nowadays.(Will beat Hitesh portfolio thread in couple of years)

If stock returns were based on the number of forum posts and complex projections, IDFC First would be at 1000 by now. We didn’t see this much effort even for stocks that actually went up 10x.

Real investors should ask why the stock price isn’t following the ‘superstar’ narrative being built here every day.

9 Likes

5 year returns of large and mid sized banks (as of today)

HDFC - 32%

ICICI - 151%

Kotak - 24%

Axis - 89%

Indusind - 6%

IDFC - 75%

Federal - 287%

Yes bank - 33%

RBL bank - 35%

Clearly, last 5 years have been rather tough for the banking industry, with only ICICI and Federal managing to clearly outperform IDFC First Bank. Of course, IDFC has not been the best performer, however it has been no laggard either - its right there at the top.

It must be noted that among all these banks, IDFC had the highest exposure to microfinance, barring Indusind. My best guess is that if IDFC didn’t have microfinance exposure, then it would have topped the 5 year returns table above. Very small exposure to microfinance is what helped ICICI and Federal Bank deliver segment leading returns.

As things stand today - IDFC has run off its microfinance book, and gotten rid of other problem areas like legacy infra book, huge investments in liability franchise, huge investments in new businesses, etc. If IDFC could be at the top of the returns table with all its past problem areas, then imagine what it could do after the problem areas have been sorted out.

The excitement may have been too early 5 years ago, but I believe the excitement is appropriate at this point of time.

2 Likes

Guys

Disclaimer- Holding good allocation of IDFC in portfolio since Long, however I am a curious investor trying to always check if all is well.

Seeing all these messages on IDFC thought of sharing one basic question for which I am not able to find an answer. For a bank and a seasoned banker on top, when they get into microfinance, they very well understand what they are getting into (Eg we investing in SME or microcap story based stocks ';-))

When microfinance(MF) crisis came, it was same for all. Ujjivan Small Finance Bank which had 80% aprox MF portfolio also managed it well. (June24 PAT of 301 Cr vs Mar25 Quarter PAT of 83 Cr , drop of 73%)

Whereas for IDFC if we see from peak of 732 Cr PAT in Mar-24 they dropped to 212 Cr , drop of 71%) whereas if you see they had very small portfolio of Microfinance. Also their customer profile was supposed to be much better as compared to other Small Finance Bank. (Please stick to the comparison of Ujjivan as it has done better than third rung MF banks and I guess can be compared with IDFC)

So I believe they have strongly played MF story to wash off many sins (eg the Toll Operator default/provision of some 200-300 Cr). The bank has very poorly managed MF portfolio and thus does not inspire confidence that it is well managed.

As I am not an expert in Finance (Forget Banking) I might be totally wrong but that is how it looked to me from top level understanding

Any views on this?

Regards

3 Likes

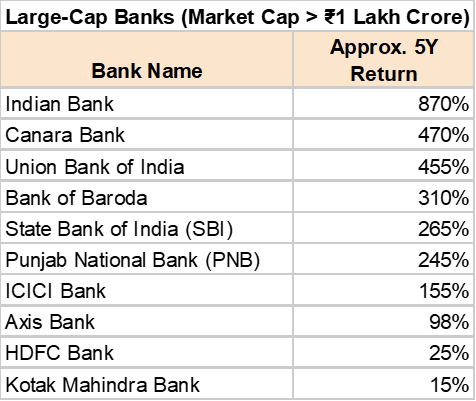

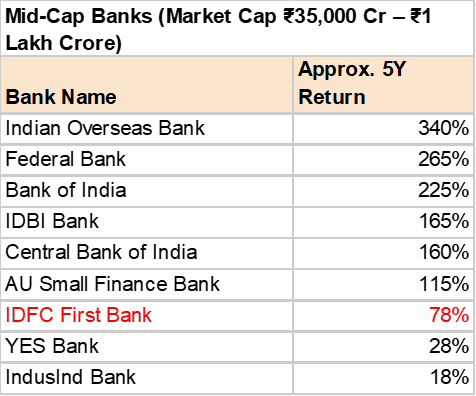

To make a proper comparison of the performance of Banking industry, we should consider all banks and not select banks. If you throw other banks you have left out, into the mix, here’s what it shows (sourced from asking Gemini, so not updated to the latest 5 years until 23rd Jan 2026 but broadly around that):

Out of Large Cap Banks, 8/10 beat IDFC First returns

Out of Mid-Cap banks, 6/9 beat IDFC First returns

So IDFC First is a big laggard in the stock performance of the overall Large and Mid Cap banks in India

5 Likes

PSU bank stocks have clearly done well in the last few years. But that’s mostly due to base effect. All of them were trading at 0.1x to 0.4x PBV, and got rerated. But that game is largely over - there is not much scope for further rerating, and their growth is slow and they continue to lose market share to private banks. So, if you want to hold PSU banks going forward, you are most welcome.

Regarding, comparison between microfinance business of Ujjivan and IDFC - just want to point out few things.

- Not all microfinance exposure is the same. For example, microfinance stress in Karnataka and Tamil Nadu was far more severe than say in Gujarat.

- Everyone has different provisioning policies. IDFC is doing 100% provisions on microfinance bad loans. Others might be doing 80%. Which means that IDFC will have some writebacks when some of these bad loans are eventually recovered.

- IDFC is so conservative that they have provided 100% for even the insured microfinance loans. The terms of the insurance are that 72% of the loan amount will be compensated by the insurance provider after 12 months. So at least in theory, 28% provision would have been enough. This policy means excess provisioning which will be written back in due course.

1 Like

Hi

Many thanks. Your response is very logical and I also understood that way.

Only two points 1) Ujjivan is south focused heavy on portfolio in TN, AP, Karnataka zone and so was badly impacted. Same is for IDFC where they were TN focused on MF 2) conservative is ok, but you can’t shout and cry of MF issue, do 100% provision and than claim to be a prudent bank ( imagine if SBI do so for Adanai…:-))

BTW the same they did on 200 odd Cr Mumbai toll operator and we are yet to hear something from bank. May be will.ask in this investor call

Anyways thanks for sharing your views. That helps

Regards

My thoughts on Ujjivan vs IDFC.

Less than 30% microfinance exposure of Ujjivan is in South India. For IDFC bank, 76% microfinance exposure was to TamilNadu (61%), Karnataka (10%) and Kerala (5%) - the three most heavily impacted states (Reference: page 35, of Q2 FY25 investor presentation). Fair to say that among all listed banks and nbfcs, IDFC had the worst geographic exposure to the microfinance crisis. Clearly, a judgement mistake from Vaidya that he allowed this to happen.

Another reason is that Ujjivan reduced its PCR (provision coverage ratio) from 80% in Dec’24 to 73% in Sep’25, while IDFC maintained stable PCR during the same period.

Another reason could be that, Ujjivan didn’t de-grow its microfinance book. Which means, they possibly evergreened at least some of their borrowers. If you disburse a fresh loan to your defaulting borrower - then he will not default. IDFC de-grew its microfinance loan book by around 50% from it’s peak. So, they didn’t do any evergreening or only did so slightly.

That should make us ask a related question - what would have been the profits of IDFC bank if it didnt have take such a huge hit from the microfinance crisis? My rough estimate is that IDFC did around 3000 crore of provisions over the last 6 quarters for the microfinance book. Which means to say that the actual profitability of the book can be estimated by adding 3000 crores to the PBT of the last 6 quarters - around 500 crore extra per quarter. The PAT for last 4 quarters would have been around 3000 crores vis a vis reported 1450 crores. That is an indication of the true profitability of IDFC bank going forward. Of course, FY27 profits will be further sweetened by reversals of excess provisions done for microfinance in the last 6 quarters.

The Mumbai toll account is unrelated to microfinance. It was already classified as NPA during covid, and 50% provided for. In 2024, just before Maharashtra elections code of conduct came in, the govt disallowed the toll operator from collecting tolls as a populist measure. So, IDFC increased provision coverage to 100% on that account. No smoking gun there. But just like microfinance, its an issue from the past. The bank has said goodbye to its legacy infra book.

2 Likes

These lines of arguments illustrate the irresistible power of hindsight bias and its grip on our minds in building conviction.

The argument started off by saying

But when pointed out that “even so IDFC First performed worse than the a vast majority” the argument was changed from “tough times for all” to “why it was easier for some to perform better than others.”

This explains why something did well after you knew what did well, not before. If this argument was made in 2021, that would count for something.

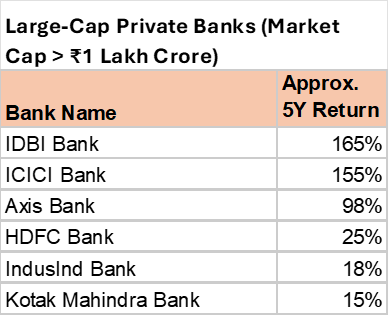

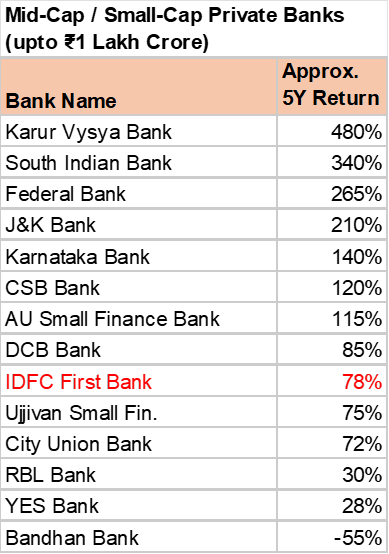

But let us counter that too. Let’s compare IDFC First bank stock performance with only private sector banks.

Again IDFC First has lagged the private sector bank. And again one can come up with explanations that would perfectly fit why this was so!!

I hope you get what I am saying. Think of a suspense movie where, before the real villian is revealed, we keep guessing and are sure that this or that suspect is a villian. But once the villian is known; then we say “oh, it was so obvious”. There’s a book by that name to help: Everything Is Obvious: Once You Know the Answer.

Disc: no investments in any bank above during this time period

4 Likes

I appreciate your effort to warn about the risks of hindsight bias influencing how we build conviction.

On the other hand, its clear to me from your posts that you haven’t held any bank stocks, or done any serious research on them. Instead you merely asked Gemini AI a couple of questions and used the AI answers to conclude that all others posting in this thread are afflicted by hindsight bias. In reality, many here have done painstaking research on IDFC and other banks, and have formed our opinions or convictions based on that research. The convictions and opinions may turn out to be right or wrong - but what matters is that most people on this thread have done at least some research before posting.

It would be helpful, if you do some research too, and share your opinions formed from such research, instead of merely sharing some Gemini AI answers. Otherwise, you will keep believing that everyone else is afflicted by psychological biases, when the real problem is that you are commenting on topics which you are mostly ignorant about (call it ‘ignorance bias’ if you like).

PS: Bought IDFC ltd at 14.5 rs/share during covid, which got converted into IDFC bank shares. Including dividends, it has been at 10x bagger for me.

Not in India, but I hold bank stock listed in Singapore; and I look at India banking stocks from time to time because we hold one large-cap Bank stock in the fund we sub-advise; though not my pick. I have also posted earlier in this thread (Oct 2021 making a case as to why IDFC First is likely to dilute a lot over time unlike other peers - post 1861)

An analyst should take the path of least effort that validates or invalidates the hypothesis, and in this case Gemini was enough (with a bit of validation of what it spewed).

1 Like

How I look at the bank is that sitting on FY28, if ROEs are 12-13%+ with clear trajectory towards 15% ROEs, the stock should atleast trade at 2x P/B on a trailing basis & 1.5x 2 year forward considering the quality of the book as on that date, which easily gives an IRR of 26-28% over the next 2 years

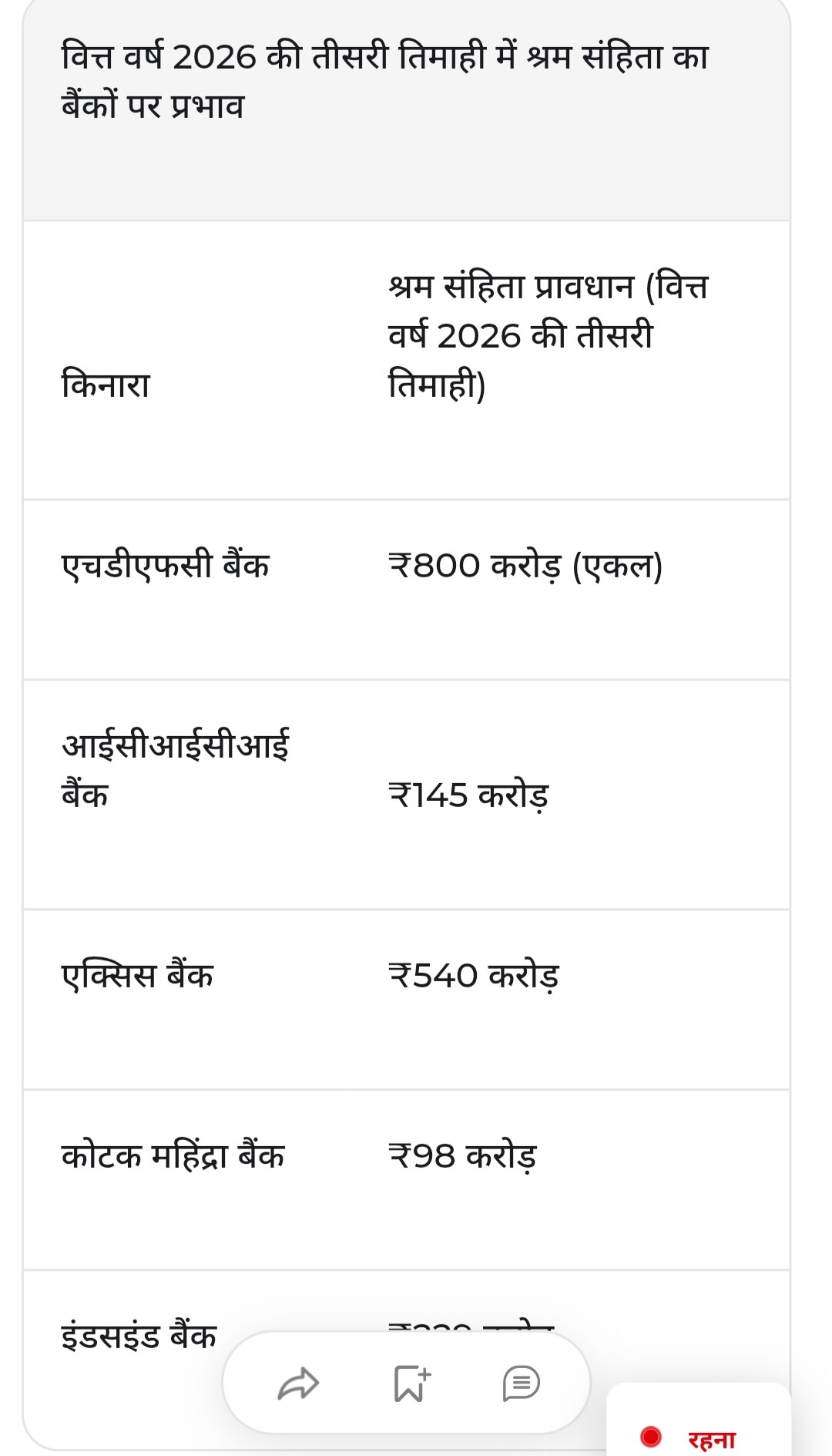

Can someone explain what this new labour law is and what impact it will have on banks? Is a one-time provision required under this law? On what basis have the top 5 banks made their provisions? Also, what will be the impact on IDFC First Bank, and how much provision will it need to create?

We’ll know the exact impact tomorrow, but as per some, impact on most of the companies should be around 3 to 5% on profits. See this for more details on generic calculations - https://x.com/deepakshenoy/status/2016164344204296571

From that article:

Normally, such one time hits should be provisioned across four quarters

Given the aggressive provisioning nature of VV, we can assume that the impact would be more on higher side in this quarter itself. Hoping for the best tomorrow.

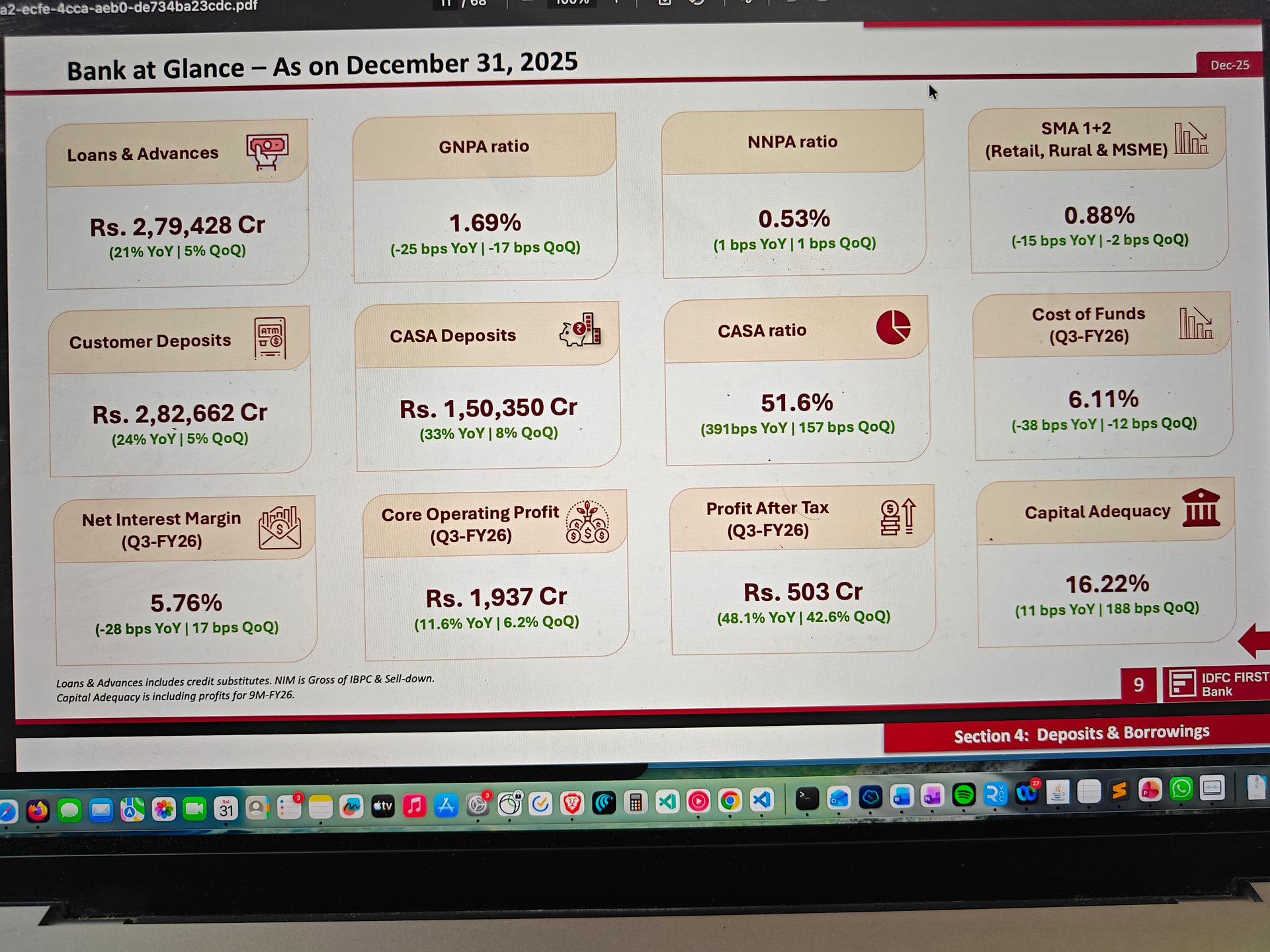

IDFCFIRSTB-Earnings-Call-Intimation-Jan-23-2026.pdf (261.1 KB)

Incase someone wants join tomorrow’s investor con call for Q326

1 Like

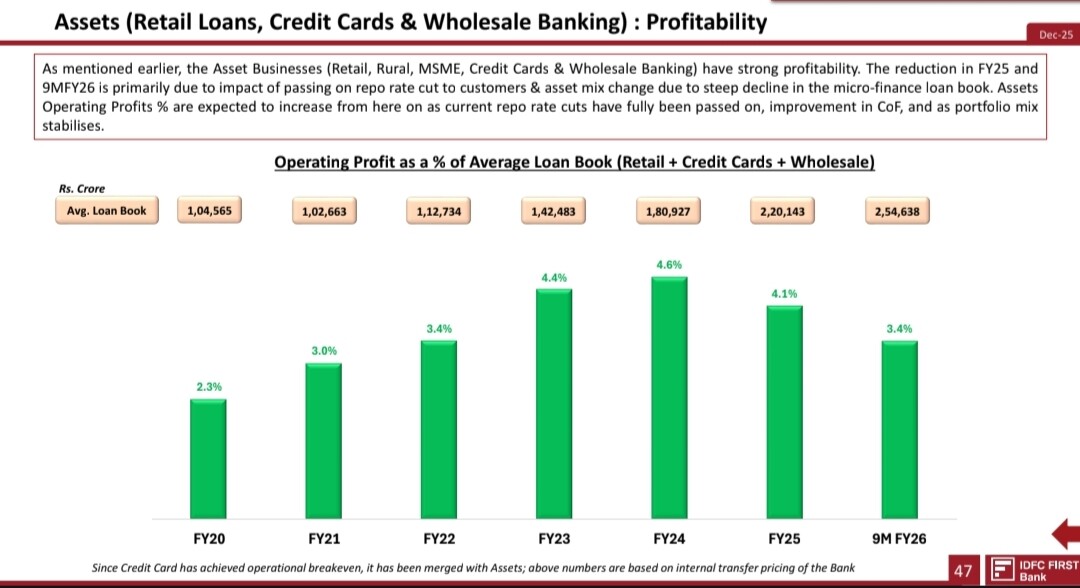

The results are good, but not very good. First of all, someone needs to help me understand how the operating profit shown in the upper image has been calculated as a percentage of the average loan book.

If we calculate for FY25, 4.1% of the average loan book of ₹2,20,143 crore comes to around ₹9,026 crore, whereas the operating profit for FY25 is ₹7,415 crore. How is such a big difference arising?

The cost-to-income ratio has again come back to 74%. Provisions are almost flat. Overall, the numbers look okay, but I don’t understand why management (VV) has opened the tap so slowly, due to which profit flow remains very slow.

Last quarter, operating expenses increased QoQ by 4.1%, and this quarter they have increased by 9%. I genuinely fail to understand the pattern — whenever provisions are flat, operating expenses increase. When operating expenses and provisions come under control, interest expenses go up. Some factor always comes in and wipes out the profit.

After the merger, IDFC First Bank always seems to be facing one issue or another — sometimes legacy loans, sometimes cost-to-income and operating expenses, sometimes microfinance issues. I honestly don’t know when VV will fully open the tap and allow profits to flow at full capacity.

2 Likes

65 odd crores only for labour code related. Such a relief ![]()

Overall provision came down QoQ.