Results are poor due to Rate Cuts. income growth has reduced, cuz they haven’t reduced savings rate but, passed on rate cuts, affecting Nim and income growth.

All these issues,

High Provisioning for so many quarters yet low PCR

Slower growth in operational income due to rate cuts

High CI ratio

Low RoA, optimal level still very distant.

all these issues are probably factored into its low market cap of 62000 Cr

Higher provisioning can indirectly impact your capital adequacy ratio, as provisions affect your P&L. This, in turn, reduces the room for lending.

However, each bank makes its own decisions. Aggressive provisioning can reduce negative volatility and potentially lead to positive surprises in the future. That said, banks generally have internal estimates of credit losses, and maintaining provisions based on those estimates, with a slight buffer, should typically be sufficient.

IDFC First has returned to its steady-state PAT levels, around ₹350-400 crore, with the previous quarter being an aberration due to abnormal trading gains and very high provisions.

Many of the major levers have already been utilized, such as replacing legacy high-cost borrowings. With CASA levels already higher, maneuverability in this area is limited (though the bank could push for a higher proportion of current accounts within CASA).

While NIM levels have reduced — primarily due to the non-passing on of savings rates — this was expected, given the bank’s focus on prime housing loans. This trend was inevitable, even without the rate pause.

There are still few key hidden optionalities for the bank which can lead to decent shareholder returns:

*PB (Price-to-Book) could improve if sector-related rerating happens.

*Consistent performance could lead to a re-rating of the bank, even without broader sectoral re-rating.

*Conscious control over operational expenses (opex). This is achievable i think

*Higher growth without capital dilution - possibilities aren’t high on this option

*Figuring out ways to improve fee income

Disclosure:- Invested, but in caution mode after capital raise detrimental to existing shareholders!!

I have generally been critical of repeated dilutions. I was horrified that they raised Rs. 7500 cr again. They have been raising every year since merger practically. somehow stock is up 25% from Rs. 60 to Rs. 75, can’t understand why.

For NIM of 5.6% (of assets), credit cost of 2% of loans (or 1.4% of assets) is not much, its pretty good actually.

But the issue is high C:I, large dilutions, makes no money, no ROE.

But stock confounds us. If you see from date of merger of this bank, they are up from 37 to 75. Other mid-tier banks IIB, RBL, YB, Bandhan, who have better ROE, better PAT through the cycle, better starting point than this Bank are down around 50%.

Can’t understand why they are so highly valued when ROE is so low (4-5%). Shouldnt we wait for valuations to correct before we buy? This bank confounds us.

On another note, why don’t we just buy ICICI HDFC and live in peace for ever.

The other mid-size banks mentioned have their own share of issues – IndusInd (asset quality issues, recent management restructuring, etc. ), Yes Bank (recovering from 2020 crisis, very low NIMs 2.5%, ~5% ROE, etc. ), RBL (almost no growth in BV since covid, C:I 70%, ~5% ROE), Bandhan (increasing GNPA around 5%, low CASA ratio, negative profit growth compared to 2020 levels).

As you rightly pointed out, the above factors are big negative today for IDFC First bank, The bank has few big positives as well - CASA at 50% (one of the highest in the industry), consistent 20% advances/deposit growth, NIMs close to 6%, new-age digital banking, etc. Yes, it is relatively priced higher at 1.5x BV (whereas other mid-sized banks mentioned are also priced around 1 to 1.5x BV).

But, the most important factor for IDFC First bank is Mr. Vaidyanathan (the skin in the game, “Bet on the Jockey!!”)

IDFC FIRST BANK’s Q2FY26 results have been quite good. We should focus on the core banking business, and from that perspective, the PPOP of the core bank increased from ₹6,664 crore to ₹6,948 crore QoQ — which is impressive, especially when the microfinance business is in decline and the repo rate transmission hasn’t yet taken effect.

If the bank had achieved the same level of trading gains as in the last quarter, the PAT could have reached around ₹700 crore. In that case, ROA, ROE, and EPS would have improved and everyone would be calling it a strong quarter.

We can give the bank another 1–2 quarters, after which both the MFI segment and repo rate transmission effects will likely be visible. With CASA above 50%, the bank also has room to reduce savings rates, which could further boost margins.

I see better days ahead for the bank, with several key trigger points:

Repo rate transmission

Provisions related to the MFI segment being released or reduced

Consistent loan book growth QoQ, outpacing OPEX growth

Reduction in savings rate, a major potential boost

All these factors could drive the bank toward its next phase of strong profitability.

It’s truly fascinating to see the enduring and unconditional love at this counter for Management - very very rare. And the envy of other Managements that thinks it can win over shareholders by delivering good earnings on their money.

A Bank that delivers an ROE of less than FD rate (over the past 5 years - worse if extended), but races to grow loan book has to keep raising capital again and again and again - irrespective of market environment. This was raised as a concern in this very forum many years ago before the capital raises.

Approximately Rs 14,700 crores has been raised since May 2020. The shares outstanding from the time of new Management till the time the CCPS gets converted have increased from 340.44 crores to ~ 857 crores! A rupee of profit earned for the “keeping-the-faith” shareholder in early 2019 has now has to be given away to others that he gets only 40 paise. Never mind that the bigger shareholders are not so much “keeping-the-faith” kind having put in capital via CCPS at a price that was decided post facto at market lows of around Rs 60 / share (not to forget an 8% dividend); and converted conveniently at a time when prices went up 25% since.

I think it’s time for Management of other companies who think their job is to “add shareholder value” to get lessons at the feet of the masters here!

i concur with your views. Too much of optimism driven more by (blind?) faith rather than actual performance. Constant dilution of shareholder interest adds to the underperformance for the shareholder.

Management sees weakness in asset quality, so they use part of profits as reserves.

However, this reserve is just a book entry. Meaning, the bank can use this reserve in the course of business. The benefit is in not having to pay taxes.

Can you help me spot that post? I searched ~ 50 posts with ICICI and could not find any.

Rough calculations show ICICI bank diluted by 1.11 times in the 23 years since it was reverse merged (i.e. 100 shares became about 211 shares adjusted for bonus and stock split). During this time, the book grew from 1 lakh crore to 21 lakh crores - 21 times growth for a 1.1 time dilution.

IDFC First has diluted by 1.52 times since 2016 (i.e 100 shares became 252 shares). During this time the book has grown from 1.12 lakh crores to 3.43 lakh crore - just 3 times growth more dilution at 1.52 times

So how is this similar trajectory?

Even while this is vague, it is incorrect. The amount of Provisions that can be used as a deduction against Taxable Income is governed by Bank specific Income Tax Rules in India; and it cannot be that provisions are made just to reduce tax liability. Further Provisions affect Net Profit, which brings down the Capital Adequacy Ratio (i.e. the shareholders’ money bank must have to cushion losses); and that affects that growth in the loan book with existing capital. So “banks can use this reserve in the course of the business” if it means that the CAR is not affected, it’s incorrect.

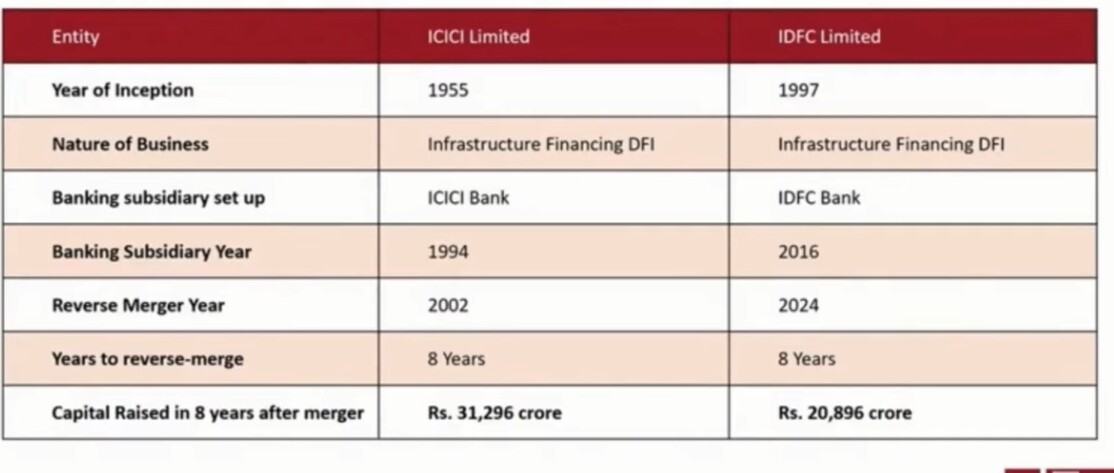

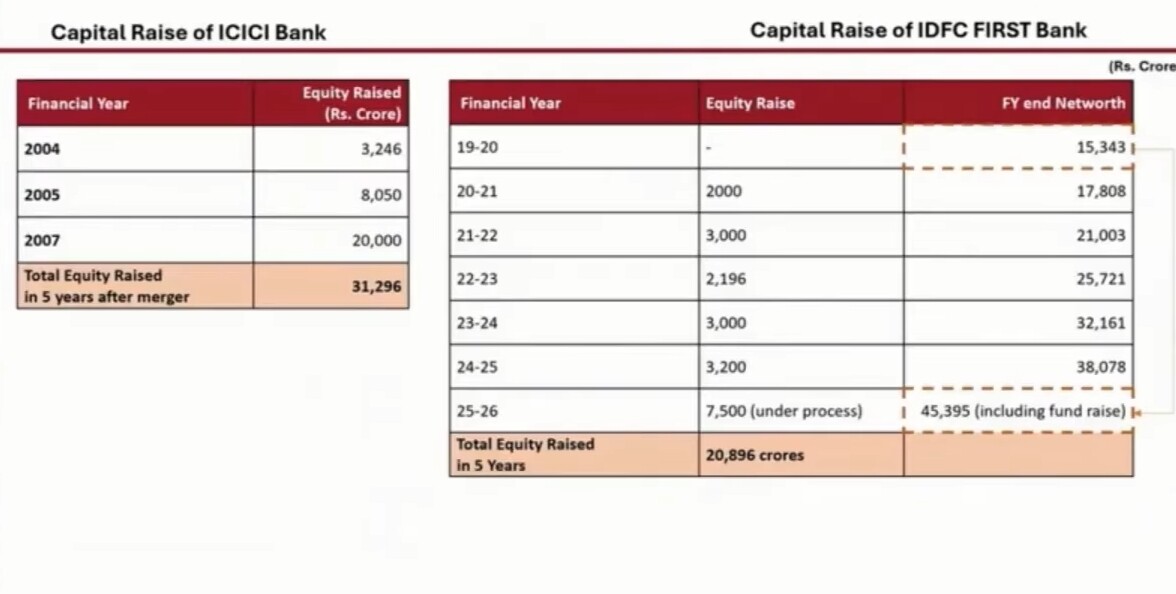

ICICI Bank raised ₹31,296 crore in capital between 2004 and 2007, while IDFC has raised around ₹20,800 crore between 2016 and 2024. To build a strong bank, capital needs to be raised from time to time — because a bank needs funds both for growth and to write off old legacy loans.

When you look at IDFC First Bank’s condition — its asset-liability position, credit-deposit ratio, and other parameters before the merger — the situation was quite poor.

To build a bank, initial capital is essential. Once the Return on Equity (ROE) crosses 15%, the bank becomes self-sufficient in terms of capital generation.

IDFC First Bank should also be given around 15 years before comparing it with ICICI Bank’s 23-year journey. If we are only comparing the initial 8 years, then IDFC First Bank has actually raised less capital than ICICI Bank did during its early years.

Given that background, comparing it today with ICICI Bank’s early history shows how far it has come. I believe the bank has already proven itself and is on track to establish its position among the top banks very soon.

ICICI Bank 2002 shows a paid up capital Rs 220 crores with another Rs 740 crores issued to shareholders of ICICI Ltd on amalgamation Page 70 of ICICI Bank AR 2002 - 2003

In other words about Rs 70 crores (being the difference of the paid-up capital between 2002 and 1996) was raised

So, the Rs. 31,296 is NOT between 1996 and 2002, you may want to correct your post.

It is from 2004 until 2007. So would you like to take up as an exercise how much ICICI Bank diluted to raise this 31,296 crores? And how much did they grow their book by?